Futu news on July 9th. The three major stock indexes in Hong Kong rose slightly in the afternoon, the Hang Seng Tech index once rose by 1.6%, and finally closed up 0.96%, while the Hang Seng index closed flat, the China Enterprises Index fell slightly by 0.14%, both of which rose by up to 0.5% in intraday, but failed to continue the upward trend.

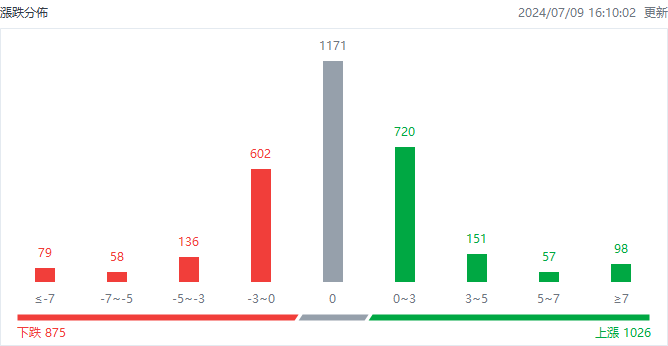

At the close, 1026 stocks in Hong Kong rose, 875 stocks fell, and 1171 stocks closed flat.

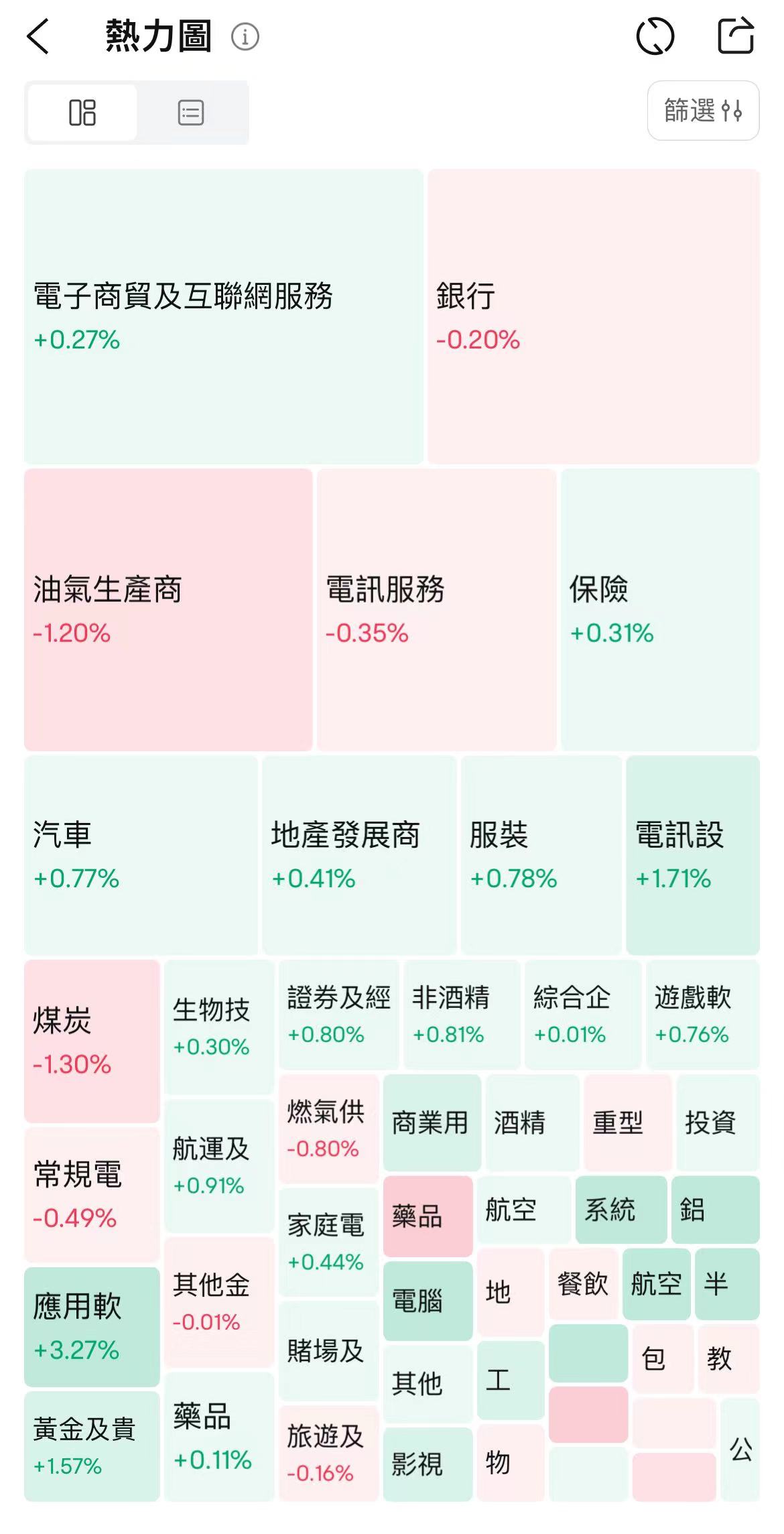

The specific industry performance is as follows:

In terms of sectors, network technology stocks fluctuated, with Kuaishou up more than 4%, Bilibili up more than 3%, Alibaba and Netease up nearly 1%, and Meituan down nearly 2%, JD down nearly 1%.

In terms of sectors, network technology stocks fluctuated, with Kuaishou up more than 4%, Bilibili up more than 3%, Alibaba and Netease up nearly 1%, and Meituan down nearly 2%, JD down nearly 1%.

Apple concept stocks rose across the board, with Sunny Optical up nearly 8%, Cowell up more than 7%, BYD Electronic and Q-tech up more than 6%, FIH Mobile up nearly 5%, AAC Tech up more than 3%.

The semiconductor sector performed strongly, with Hua Hong Semiconductor up nearly 8%, Shanghai Fudan up more than 6%, and Semiconductor Manufacturing International Corporation up more than 3%.

Electrical utility stocks were weak, with CGN New Energy down more than 4%, China Longyuan down nearly 3%, Huadian International Power down more than 2%, CGN Power down nearly 2%.

In other sectors, oil and gas stocks and coal stocks fell significantly, mainland banking and mainland real estate stocks fell slightly, biomedical, golden industrial concept, insurance and new energy vehicle enterprises rose slightly.

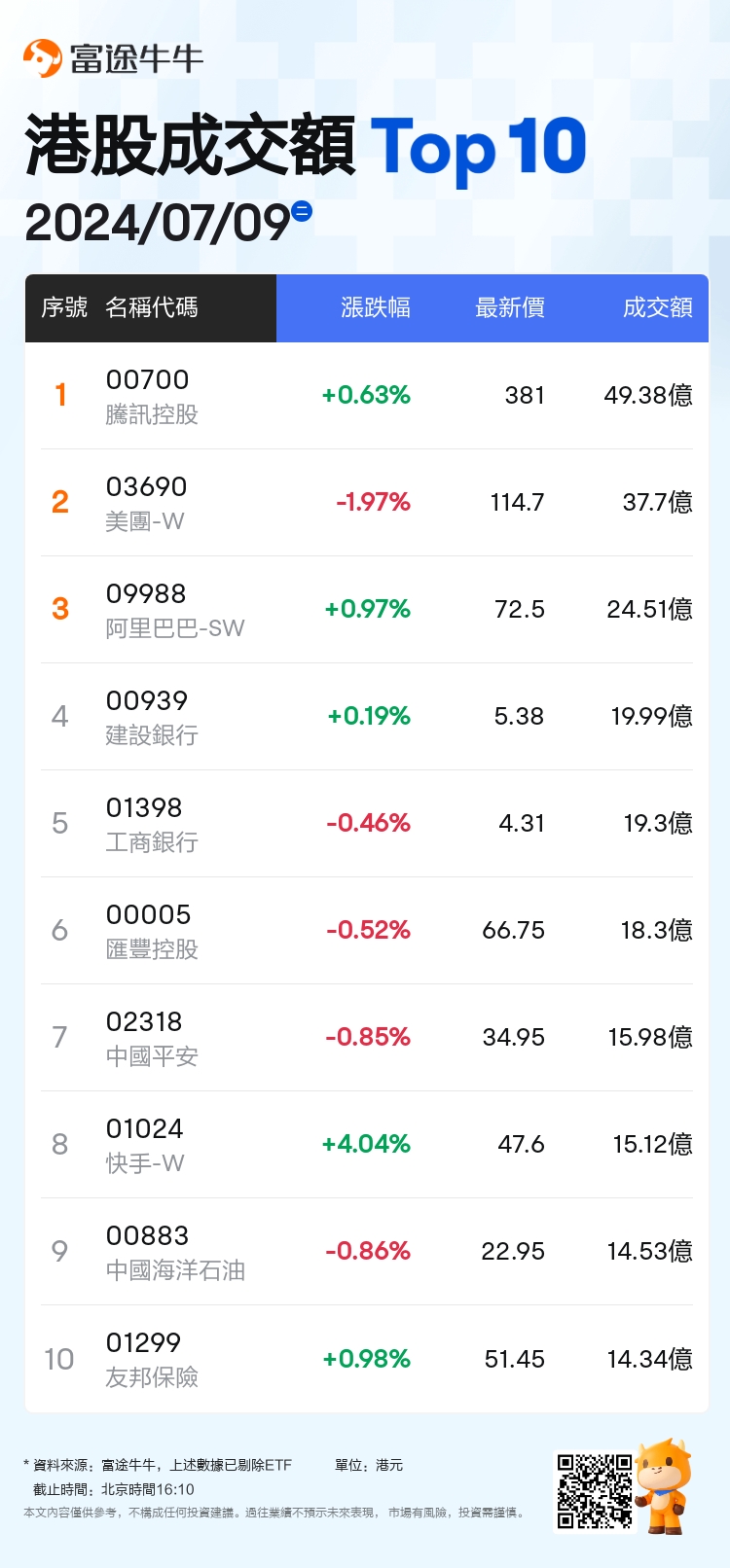

In terms of individual stocks,$FIT HON TENG (06088.HK)$Fih Mobile rose more than 21%, expected to turn a profit of up to $33 million in the first half of this year, and plans to acquire assets of several auto business companies.

$GDS-SW (09698.HK)$GDS Holdings rose more than 9%. RBC Capital raised its rating on the company's US stock to outperform the market, while raising its target price from $13 to $14.

$HUA HONG SEMI (01347.HK)$Taiwan Semiconductor rose nearly 8%, and most of its clients have agreed to raise contract prices, with Hua Hong expected to raise prices in the second half of the year.

$EAST BUY (01797.HK)$Q-Tech fell more than 4%, reaching a new two-year low, with numerous negative developments hurting the company, with institutions adjusting valuations and significantly cutting target prices.

$CNBM (03323.HK)$China Power New Energy fell nearly 14%, and is expected to report a mid-term loss of about 2 billion yuan, with a year-on-year reversal from profits to losses.

$SPACE GROUP (02448.HK)$Flash crash plummeted more than 77%, hitting a historical low, with a total market value of less than HKD 0.1 billion.

Today's top 10 Hong Kong stock turnover

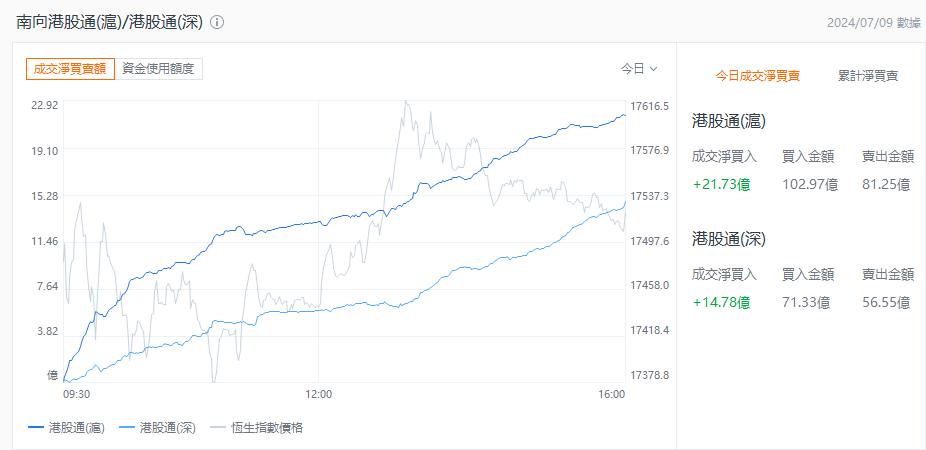

Hong Kong Stock Connect Fund

As a result of the accelerated growth in China's power consumption, Citigroup has raised its end-2024 target for the Hang Seng Index by 3.5% to 20,500 points and set a new target of 22,000 points for the first half of 2025. Liu Xianda, Citigroup's China stocks strategist, said he was bullish on stocks that would benefit from export growth and rising commodity prices, and expected the third plenum to bring eight catalysts, with structural reform, cross-border trade development, state-owned enterprise reform, relaxed real estate policies, tackling overcapacity, responding to aging population, recovering consumption, and encouraging private enterprise being assigned probabilities. From an industry perspective, Liu Xianda is more inclined towards technology, industry, basic materials, and the internet.

Institutional perspective

Citigroup: Hang Seng index target raised by 3.5% to 20,500 points by the end of 2024.

Morgan Stanley: China National Building Materials' Q2 net loss of RMB 650 million is lower than expected, target price of HKD 3.8. Morgan Stanley issued a research report pointing out that, issuing a profit warning, it is expected that the group will report a loss of about 2 billion yuan for the first half of the year ending in June, compared with a net profit of about 1.4 billion yuan in the same period last year. This reflects that the group's net loss for the second quarter is RMB 650 million, which is lower than the bank's expectations, and believes that the cement business is the main drag. Morgan Stanley believes that due to the tightening of mainland capital, slow construction progress, and few new projects, China's cement production declined by 10% YoY in the first five months of this year. Cement shipments slowed further due to rainfall in June. Under the influence of industry self-monitoring and off-season shutdown, cement prices in several regions began to rebound at the end of June, which is expected to support China National Building Materials' profits in the second half of the year. The bank gave it an "overweight" rating with a target price of HKD 3.8.

Morgan Stanley issued a research report stating that

it has issued a profit warning, and it is expected that the company will report a loss of about 2 billion yuan for the first half of the year ending in June. This reflects a YoY reversal from profit to loss. This is believed to be due to the cement business being the main drag. $CNBM (03323.HK)$China Titanium fell by more than 4%, reaching a new two-year low, amid numerous negative developments hurting the company, with institutions adjusting valuations and significantly cutting target prices.

Goldman Sachs: Raises target price for Anta to HKD116, with healthy and resilient sales performance in Q2.

Goldman Sachs released a research report indicating that $ANTA SPORTS (02020.HK)$This year, Anta brand, FILA, and other brands grew by high single digits, mid-single digits, and between 40% and 45% YoY in Q2, respectively. Goldman Sachs believes that overall, Anta's Q2 sales performance is healthy and resilient, and multi-brands help offset the impact of each other. They believe that the operating profit margins for all brands have room to grow and maintain a 'buy' rating, raising the target price to HKD116. The bank's net income forecasts for Anta in 2024 to 2026 are on average raised by 1% to reflect the company's strict control over costs such as marketing and promotion. It is predicted that revenue, operating profit, and net profit for the first half of this year will increase by 10%, 1%, and 47% YoY, respectively, excluding non-cash income from the Amer listing. The net profit is expected to increase by 10% YoY.

Editor/Feynman