According to Futu News on September 4th, affected by the decline in the external financial market, the three major Hong Kong stock indexes performed weakly throughout the day. The Hang Seng Index and the China Enterprises Index fell by 1.1% and 1.12% respectively, while the Hang Seng Tech Index fell by 0.39%, with a relatively small decline.

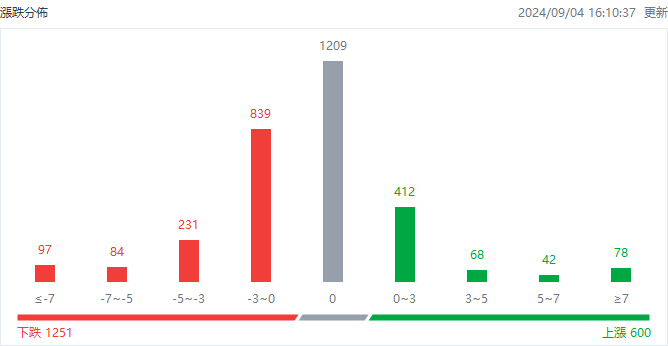

At the close, there were 600 gainers and 1,251 losers in the Hong Kong stock market, with 1,209 unchanged.

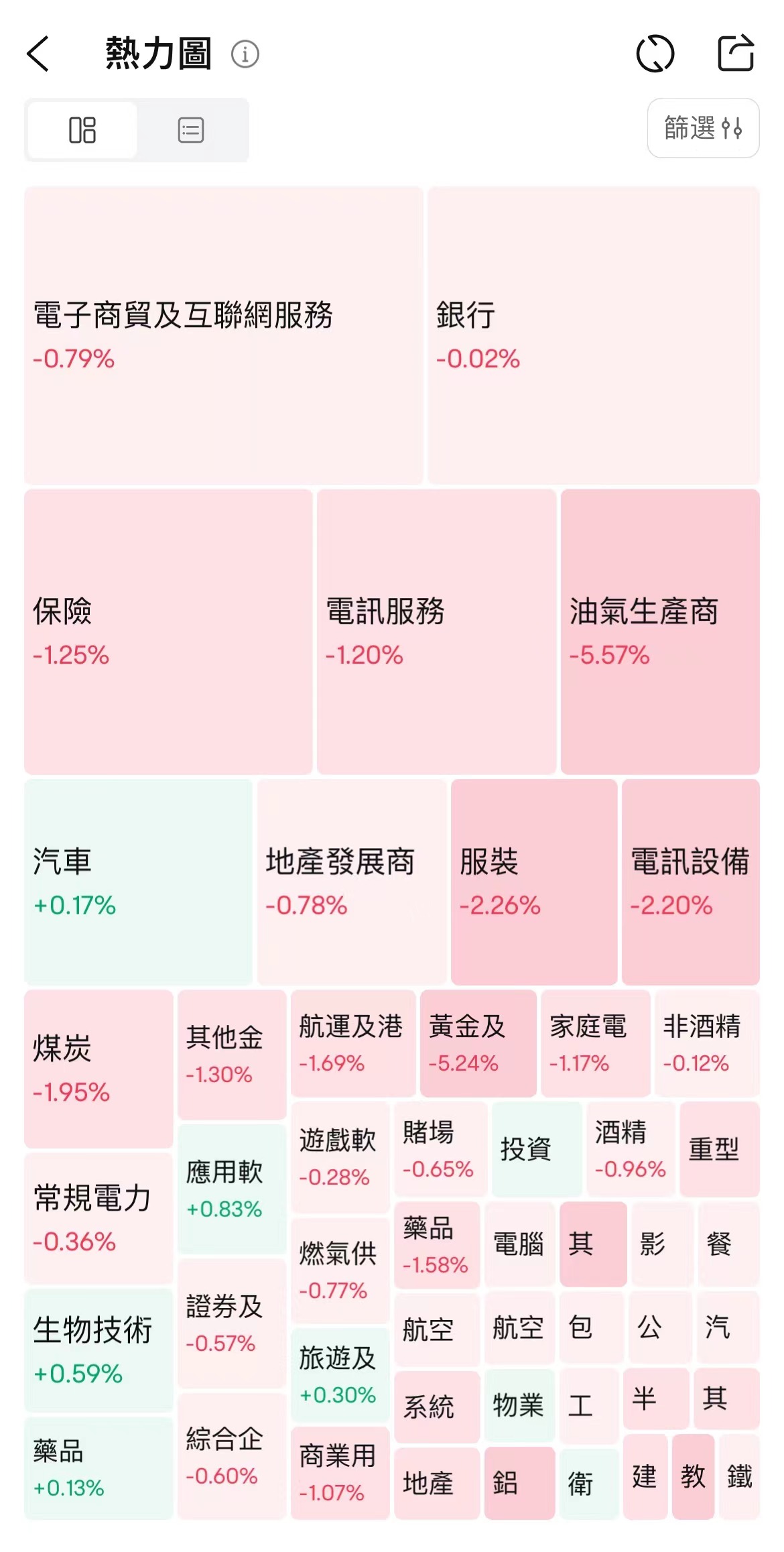

The specific industry performance is shown in the following figure:

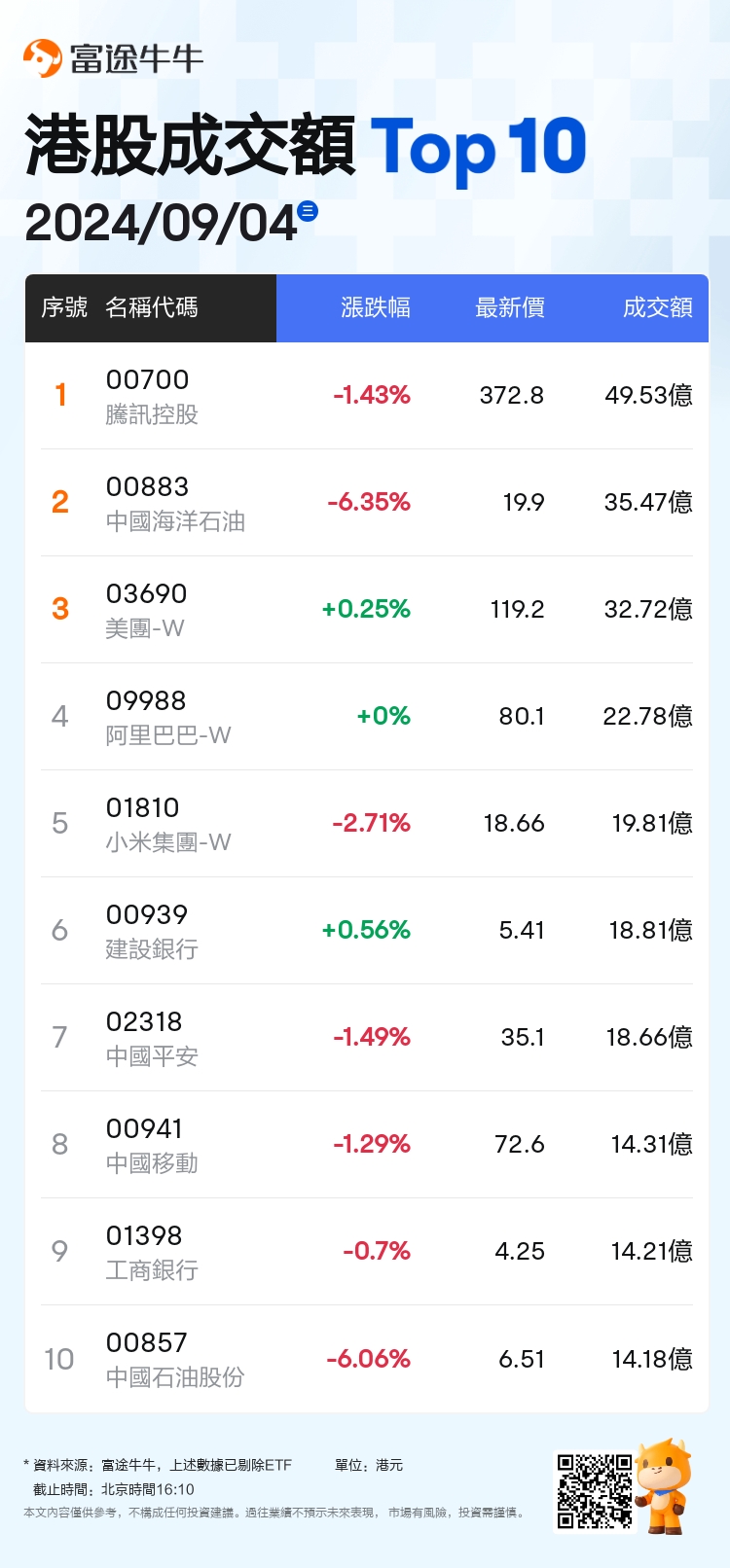

In terms of sectors, network technology stocks showed mixed performance. Bilibili-W rose 3.35%, Xiaomi Corporation-W fell 2.71%, Kuaishou-W rose 1.67%, Tencent Holdings fell 1.43%, JD.com-SW rose 0.86%, Baidu Group-SW fell 0.74%.

In terms of sectors, network technology stocks showed mixed performance. Bilibili-W rose 3.35%, Xiaomi Corporation-W fell 2.71%, Kuaishou-W rose 1.67%, Tencent Holdings fell 1.43%, JD.com-SW rose 0.86%, Baidu Group-SW fell 0.74%.

The three major oil companies retreated, with PetroChina falling 6.06%, CNOOC falling 6.35%, and Sinopec Corp. falling 2.48%.

Semiconductor stocks generally declined, with ASMPT falling 3.81%, Hua Hong Semiconductor falling 2.99%, Semiconductor Manufacturing International Corporation falling 1.59%, and Shanghai Fudan falling 2.59%.

Coal stocks declined, with China Coal Energy falling 2.58%, Yancoal Aus falling 2.56%, Yankuang Energy falling 1.59%, and China Shenhua Energy falling 1.85%.

Gold stocks continued to decline, with China Gold International falling 10.03%, Zijin Mining Group falling 6.15%, Lingbao Gold falling 2.42%, Zhaojin Mining falling 2.78%, and SD Gold falling 1.93%.

In terms of individual stocks, $NIO-SW (09866.HK)$ Rose nearly 6% against the market, will release second-quarter performance tomorrow, with a year-on-year increase of 60.2% in delivery volume in the first half of the year.

$DIDA INC (02559.HK)$ Surged over 29%, adjusted net profit in the first half of the year increased by over 50%, and has reached cooperation agreements with multiple leading internet platforms.

$CHABAIDAO (02555.HK)$ Increased by nearly 8%, the company was included in the Hang Seng Composite MidCap Index, and is expected to become a target of Hong Kong Stock Connect.

$DEKON AGR (02419.HK)$ The company's profit turned around in the first half of the year, with a nearly 7% increase, due to the rebound in livestock and poultry prices and the downward trend in breeding costs.

$CGN MINING (01164.HK)$ The stock fell nearly 4% to a new low for the year, with profits affected by tax provision and investment income falling short of expectations due to unsold uranium mines.

$EVERG VEHICLE (00708.HK)$ The stock continued to fall nearly 4%, with a loss of over 20.2 billion yuan in the first half of the year, and there has been no substantial progress in the acquisition.

TOP 10 trading volume today

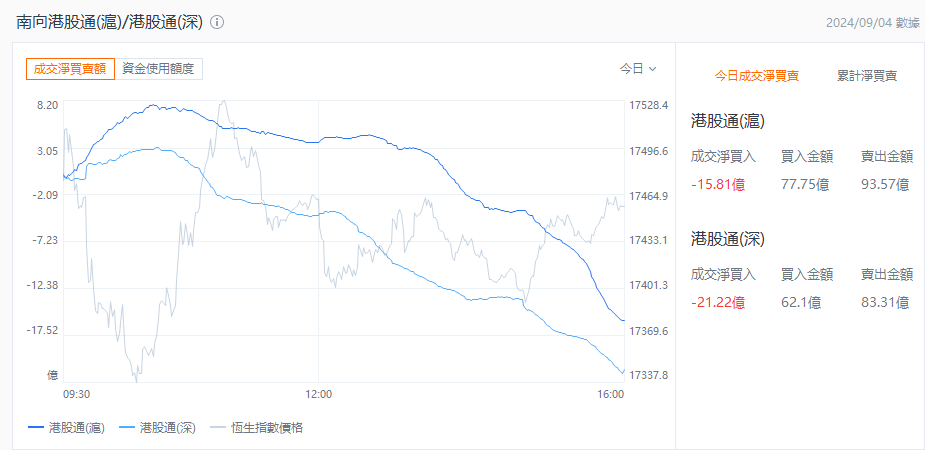

Hong Kong Stock Connect Fund

In terms of the Hong Kong stock market, there was a net outflow of 3.703 billion Hong Kong dollars through the Hong Kong Connect (Southbound) today.

Institutional perspective

JPMorgan: Expected short-term weakness in China mainland banking stock prices, but stable dividends may present buying opportunities.

JPMorgan issued a report stating that China mainland banking management maintained a relatively optimistic tone at the second quarter performance briefing. China mainland banking is confident in the continued stability of net interest margins and the potential easing of expense income contraction, implying that income growth in the second half of the year may stabilize. Although the capital positions of some banks are tight, such as Bank of Communications, China mainland banking reiterated its commitment to maintaining a stable dividend payout ratio. The bank believes that due to policy headwinds, the market may hold a skeptical attitude towards China mainland banking's optimism, especially in terms of net interest margins. Therefore, China mainland banking's stock price may continue to be weak in the short term. However, it is believed that China mainland banking is determined to provide a stable dividend per share, hence there may be buying opportunities in the short term weakness in stock prices. The next catalyst will be the third-quarter performance announced at the end of October.

Goldman Sachs: Maintains a 'buy' rating for BYD Company Limited, with the target price raised to 310 Hong Kong dollars.

$BYD COMPANY (01211.HK)$ Maintains a 'buy' rating, with a 1% to 6% upward revision of the net income forecast for the 2024 to 2026 fiscal years, and a 5% increase in the target price to 310 Hong Kong dollars. The company started to increase new car deliveries in May this year, driving continuous sales growth. In August, sales reached 0.371 million units, hitting a historic high. The bank expects that BYD will launch at least 6 new car models in the remaining time of this year, supporting further growth in monthly delivery volume. Therefore, the bank has raised BYD's full-year sales expectations from 3.8 million to 4 million units this year.

Citi: Xiaomi's stock price is still supported by robust core profits and profits from new energy vehicles, with a target price of 22.7 Hong Kong dollars.

Citigroup's report states that Xiaomi's SU7 announced that it delivered more than 0.01 million vehicles in August this year, marking the third consecutive month that it has exceeded 0.01 million vehicles. It maintains its expectation of achieving a full-year delivery target of 0.1 million vehicles in November. Citigroup believes that Xiaomi has already achieved more than 50% of its target of 0.1 million vehicles this year, or approximately 45% of its target of 0.12 million vehicles. The stock price of Xiaomi is expected to be supported by its solid core profit prospects and improving gross margin for electric vehicles. Currently, the price-earnings ratio is about 15 times for its smartphone, internet of things, and internet services business, and about 2 times for its smart electric vehicle business. The target price is set at HKD 22.7, and Citigroup believes that the valuation level is reasonable, recommending a "buy" rating. $XIAOMI-W (01810.HK)$

Editor/Feynman