Government spending to stabilize public sentiment comes at a cost to the bond market: Rising term premiums are driving global long-term bonds into a 'steepening storm.' Funds that successfully avoided the March bond market rout have warned that 'populist' policies will hit bonds, as governments implement fiscal stimulus measures to counter economic downturns, thereby pushing up yields on long-term government bonds.

A bond fund that achieved strong positive returns during last month’s record sell-off in the global government bond market, driven by 'stagflation' expectations catalyzed by the Iran war, is betting that the yield curves of global government bonds will steepen as countries implement populist-oriented expansionary fiscal policies to cushion the impact of energy shocks. In other words, as 'developed country governments spend to stabilize public sentiment,' the bond market may soon begin to demand a price — particularly through an increase in the 'term premium' metric, which could drive global long-term bonds into a 'steepening storm,' triggering a sustained rise in yields for 10-year and longer-dated government bonds.

The core strategy of this 3 billion euro (approximately 3.5 billion US dollars) bond fund, named Carmignac Portfolio Flexible Bond, focuses on purchasing short-dated government bonds, based on the expectation that yields will fall as aggressive bets on central bank rate hikes are unwound amid multiple favorable factors in the market.

However, the senior fund manager who successfully avoided the sharp downturn in the bond market in March warned that 'populist' policies would significantly impact bond prices, with governments adopting populist fiscal stimulus measures to combat economic recession, thereby driving up long-term sovereign yields.

However, the senior fund manager who successfully avoided the sharp downturn in the bond market in March warned that 'populist' policies would significantly impact bond prices, with governments adopting populist fiscal stimulus measures to combat economic recession, thereby driving up long-term sovereign yields.

Guillaume Rigeade, Co-Head of Fixed Income at Carmignac, the French asset management firm managing the fund, stated in a recent media interview that as economies absorb the shock to growth, governments are likely to respond with more aggressive fiscal stimulus measures — which will undoubtedly push the term premium significantly higher, thereby substantially increasing yields on sovereign bonds with maturities of 10 years or longer. The 10-year U.S. Treasury yield, often referred to as the 'global benchmark for asset pricing,' if driven higher by fiscal stimulus-induced term premiums, will inevitably lead to a new wave of valuation collapses across high-yield corporate bonds, tech stocks, and cryptocurrencies, among other highly sought-after risky assets globally.

According to performance comparison data compiled by institutions, the above-mentioned bond fund issued by Carmignac returned 0.5% in March, while the global government bond index plummeted by 3.4%. This performance ranked it second among 282 flexible bond funds in Morningstar Direct's euro category. The fund benefited from a negative duration strategy stance adopted in most markets during March, allowing it to profit inversely as yields rose.

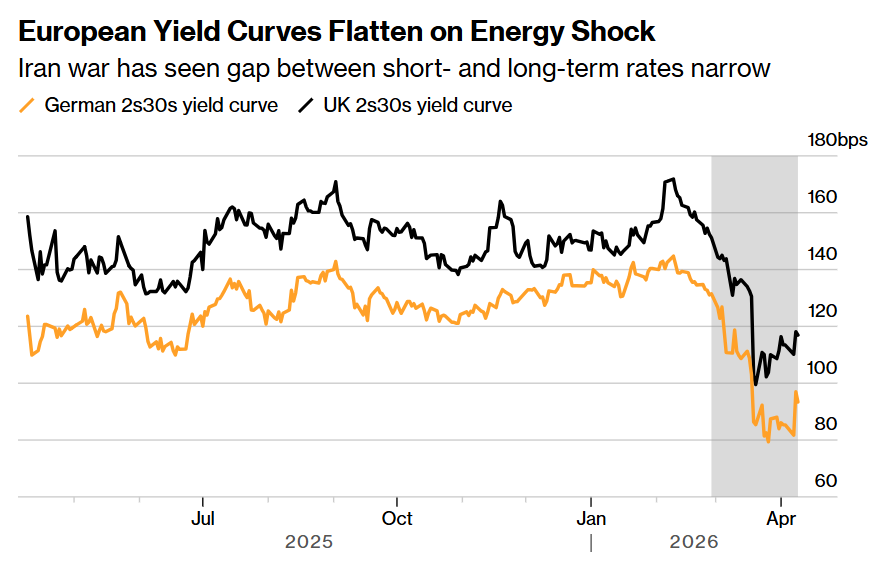

Policies with a 'populist' tone will weigh on bond assets.

In a recent interview, he stated that the economic consequences of the Iran conflict will prompt governments worldwide to introduce 'measures with a degree of populism to assist households and businesses.' 'Governments will face significant pressure to spend more to help households.'

Rigeade said in a media interview on Wednesday that even after a one-day rally driven by a two-week ceasefire agreement between the United States and Iran, his investment team still sees value in such short-dated securities. Following a decline in market optimism over the ceasefire deal, the yield on France’s two-year government bonds rose by about 6 basis points to 2.71% on Thursday, with noticeable increases also seen in German and Italian two-year yields. Rising government bond yields mean falling bond prices.

Many developed country governments, which have been hit relatively hard by the surge in energy prices, have begun extending or newly introducing fiscal support. Italian officials approved temporary reductions in fuel excise taxes, the British government is exploring ways to ease the burden of energy bills, and the South Korean government unveiled a supplementary budget of approximately 17 billion US dollars to bolster its economy. As geopolitical tensions continue to escalate, global defense-related government spending is also likely to rise.

Although the two-week temporary truce curbed the surge in energy prices, compared with pre-conflict levels, global traditional energy prices, including oil and natural gas, remain elevated and prone to sharp volatility in the short term. On Thursday, oil prices rebounded again as Israel's continued attacks on Lebanon and the de facto blockade or closure of the Strait of Hormuz dampened investor optimism about a lasting ceasefire.

Monetary policy authorities have already expressed concerns about excessive stimulus. Last month, European Central Bank President Christine Lagarde warned European policymakers to exercise prudence when funding consumer spending, appearing to caution against repeating the large-scale stimulus policies implemented during the 2022 energy crisis that contributed to rising inflation.

Rigeade stated: 'Certain populist stimulus policies will be costly for governments, especially when they are already facing substantial budget deficits.'

Populist policies may lead to the return of a 'term premium hurricane'.

The term premium refers to the additional yield compensation investors demand for holding long-term bonds. A 2025 IMF policy study has clearly found that following significant fiscal deterioration, the link between deficits and debt and higher long-term interest rates and higher term premiums has notably strengthened.

In the view of some economists, the term premium indicators for government bonds in developed countries globally will be much higher during 2026 to 2027. Particularly, U.S. Treasury yields and budget deficits in the Trump 2.0 era will likely exceed official forecasts significantly. This is mainly due to the new administration under Trump adopting a growth-promoting and protectionist framework centered on 'domestic tax cuts + foreign tariff hikes,' compounded by escalating budget deficits and U.S. Treasury interest payments driven by Middle Eastern geopolitical conflicts, alongside increased military and defense expenditures. The scale of U.S. Treasury issuance might be forced to expand even further during the 'Trump 2.0 era' compared to the already free-spending Biden administration, resulting in a term premium that will inevitably rise much higher than historical data.

Short-term Treasury yields may trend downward as markets unwind rate hike bets or even price in rate cuts. However, longer-term yields face another set of forces—after energy shocks weigh on growth, governments often roll out more aggressive fiscal support to bolster households and businesses. Combined with higher Treasury supply, potential military spending expansion, and concerns over deteriorating fiscal discipline, this pushes up long-term Treasury yields of 10 years or more.

In other words, radical fiscal stimulus with a strong 'populist' hue will likely increase term premiums and long-bond supply pressures, exerting upward pressure on 10-year and longer-term Treasury yields. However, if the energy shock ultimately proves to be a strong but temporary growth shock rather than a persistent inflation shock, or if risk aversion surges sharply, long-term bonds may temporarily benefit from safe-haven demand.

It is worth noting that the 10-year U.S. Treasury yield is known as the 'global asset pricing anchor.' If this yield continues to rise driven by term premiums from fiscal stimulus, it will undoubtedly lead to a new round of valuation collapses for the world's hottest risk assets, including high-yield corporate bonds, tech stocks, and cryptocurrencies. Should the yields of 10-year and longer-term Treasuries continue to climb, it would equate to a simultaneous occurrence of 'significantly higher cost of capital, weaker liquidity expectations, and expanded macro denominator' for key risk assets such as the stock market, cryptocurrencies, and high-yield corporate bonds.

From a theoretical perspective, the yield on 10-year US Treasuries corresponds to the risk-free interest rate indicator r in the denominator of the important valuation model in the stock market—the DCF valuation model. If other indicators (especially cash flow expectations in the numerator) do not show significant changes—for instance, during earnings season when the numerator remains in a vacuum period due to a lack of positive catalysts—then if the denominator level is higher or continues to operate at historical highs, valuations of those risk assets closely tied to AI, such as tech stocks at historically high valuations, high-yield corporate bonds, and cryptocurrencies, face a potential collapse.

Editor/Lee