Source: Wall Street News

Author: Bu Shuqing

The U.S. federal debt has surpassed $39 trillion, with interest payments exceeding $1.2 trillion. Coupled with the Federal Reserve's resumption of balance sheet expansion and renewed monetary easing, fiscal and monetary pressures have intensified. At the same time, the yield on 10-year U.S. Treasury bonds has risen, money supply has expanded, and controversies surrounding the Consumer Price Index (CPI) have grown, pushing gold prices to new all-time highs. Eight core indicators collectively point to the same trend: debt-driven growth and excessive money supply are continuously eroding the purchasing power of the dollar, posing systemic challenges to the dollar-based system.

Multiple critical indicators are simultaneously issuing warnings: US federal debt surpassing $39 trillion, annualized interest expenses exceeding $1.2 trillion, and the Federal Reserve restarting the expansion of its balance sheet—indicating systemic pressure on the purchasing power of the dollar.

Multiple critical indicators are simultaneously issuing warnings: US federal debt surpassing $39 trillion, annualized interest expenses exceeding $1.2 trillion, and the Federal Reserve restarting the expansion of its balance sheet—indicating systemic pressure on the purchasing power of the dollar.

From fiscal deficits to money supply, from Treasury bond yields to gold prices, eight core indicators all point in the same direction: more debt, more currency issuance, and continued erosion of the dollar’s purchasing power—a trend presenting long-term challenges for investors holding dollar-denominated assets.

The Federal Reserve recently announced the end of its balance sheet reduction and the resumption of balance sheet expansion, while pivoting toward easing even as inflation remains not fully under control. Meanwhile, gold prices have reached record highs, seen as a direct reflection of waning market confidence in the fiat currency system.

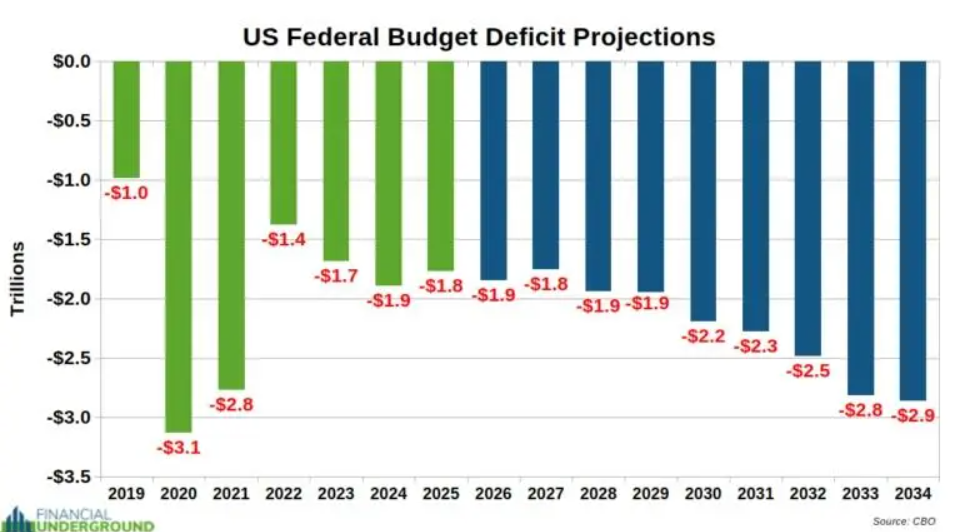

Continued deterioration of fiscal deficits

The trajectory of the US federal budget deficit is alarming.

Even under the optimistic assumption of "no wars and no recessions in the next decade," the US government is still projected to accumulate over $22 trillion in new deficits, all of which will need to be financed through debt issuance.

However, this assumption is becoming increasingly untenable. Reports indicate that the Pentagon has requested an additional $200 billion in funding for potential military actions related to Iran, marking only the beginning of possible supplementary expenditures.

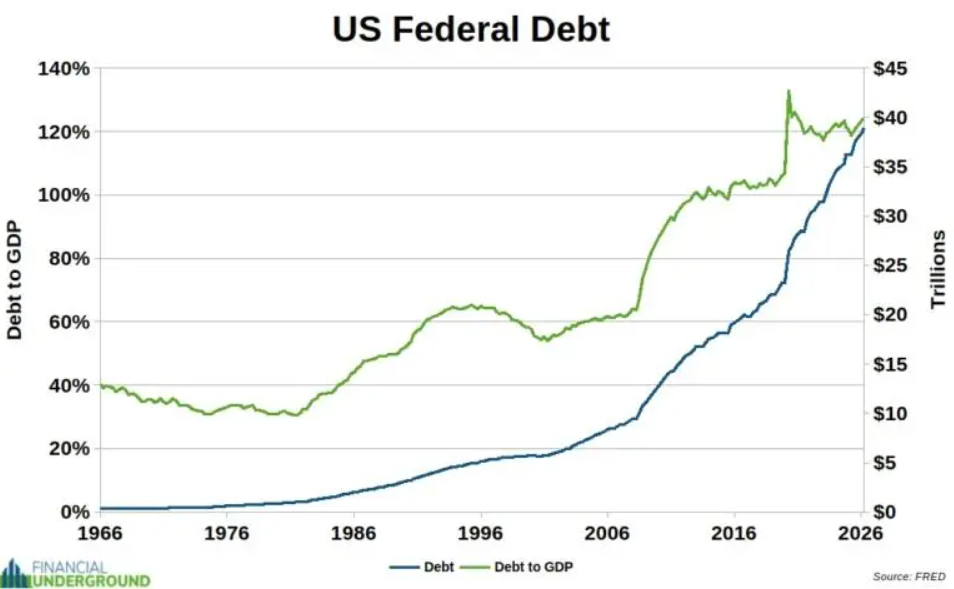

Debt surpasses GDP, placing an unbearable burden on the economy

The total federal debt has now exceeded $39 trillion, representing over 124% of GDP.

Notably, GDP calculations inherently count government spending as a positive contribution, with government expenditure accounting for at least 37% of US GDP. If this factor were excluded, the actual debt relative to the productive economy would far exceed the levels indicated by official statistics.

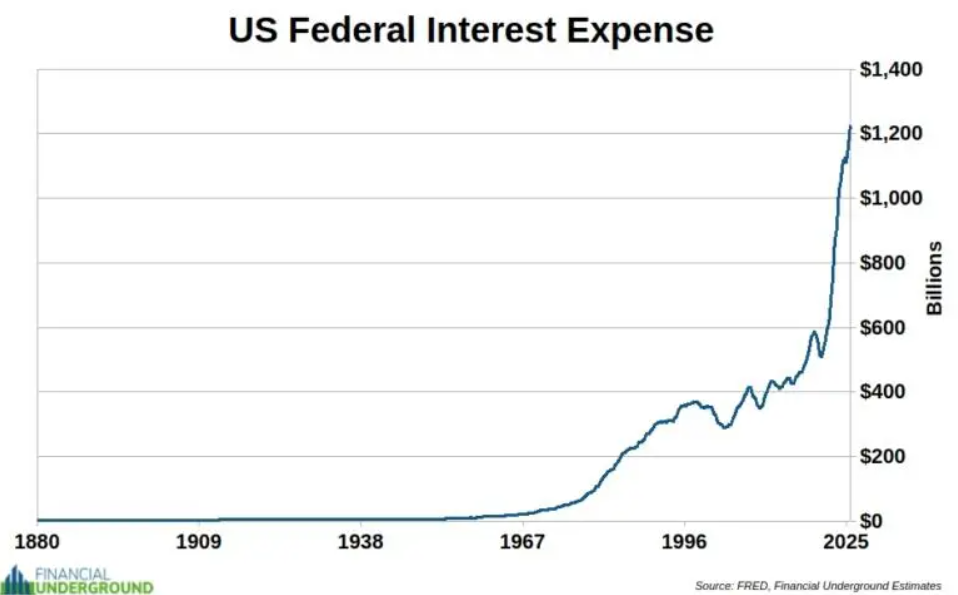

Interest expenditure is set to surpass social security as the largest fiscal burden.

The annualized interest expenditure on federal debt has exceeded $1.2 trillion, accounting for more than 23% of federal tax revenue, and continues to rise rapidly.

Currently, debt interest represents the second-largest spending item for the U.S. government and is projected to surpass social security expenditures within months, becoming the largest single expense for the federal government.

This dynamic creates a self-reinforcing cycle: rising interest payments compel the government to issue more debt, which in turn further increases interest burdens, continually narrowing fiscal space.

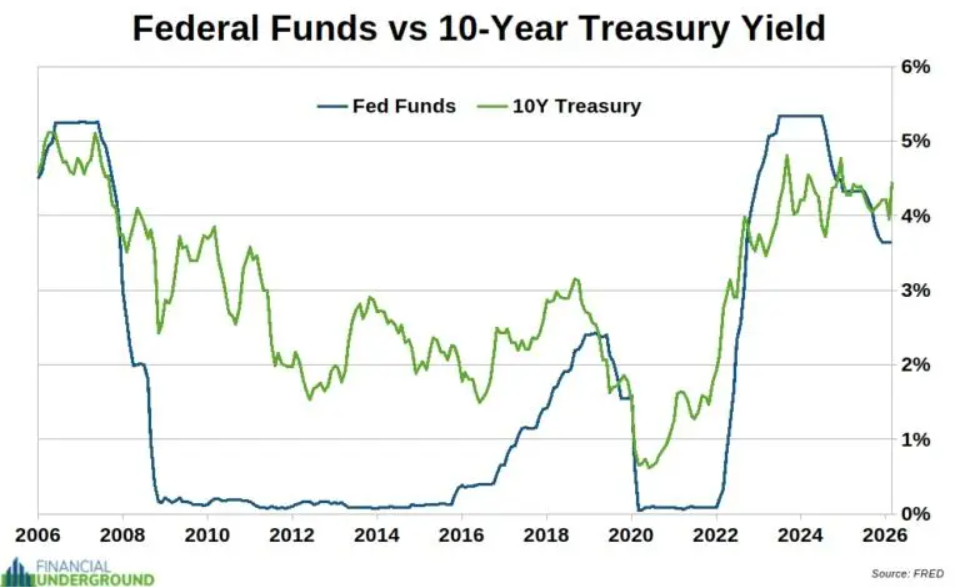

Federal funds rate and 10-year Treasury yield

Central banks, represented by the Federal Reserve, attempting to set interest rates resemble planned economic behavior, which is difficult to sustain in the long term and may lead to distortions and losses.

Historically, following the 2008 financial crisis, the Federal Reserve maintained near-zero interest rates for an extended period; from 2015–2019, it entered a tightening cycle; in 2020, rates were cut back to near zero due to the pandemic; after inflation surged in 2022, rates were aggressively raised above 5% within 18 months. Although a shift toward easing has begun, inflationary pressures persist.

Mechanically, the federal funds rate is a short-term rate directly controlled by the Federal Reserve, whereas the 10-year Treasury yield is determined by broader market forces, influenced by policy but not entirely controllable.

This yield serves as a core benchmark for global asset pricing; its increase typically reflects bond sell-offs, rising financing costs, and potential pressure on the U.S. dollar system.

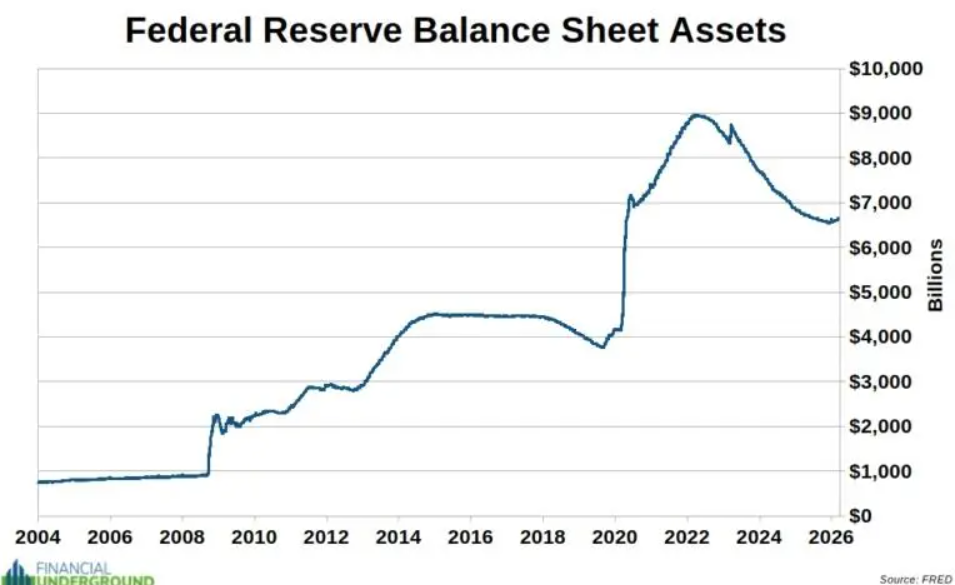

The Federal Reserve’s commitment to balance sheet reduction has once again faltered, ushering in a new phase of expansionary policy.

The trajectory of the Federal Reserve's balance sheet reveals a recurring pattern: every contraction following a period of expansion has been interrupted by cracks emerging somewhere in the financial system, after which the balance sheet resumes expansion at a higher level, never returning to the starting point of the previous cycle.

After the 2008 financial crisis, then-Federal Reserve Chairman Ben Bernanke pledged that the balance sheet would eventually normalize, at which time its size was approximately $2.5 trillion, with the goal of reverting to pre-crisis levels of less than $1 trillion. However, nearly 15 years later, the balance sheet has grown to more than twice the promised level and is entering a new phase of expansion.

During the COVID-19 pandemic, the Federal Reserve's balance sheet swelled from around $4 trillion to nearly $9 trillion. Even after so-called "quantitative tightening," its size remains over 50% higher than pre-pandemic levels. The Fed characterized this latest round of expansion as "reserve management" rather than quantitative easing, but critics argue that regardless of terminology, purchasing government bonds with newly created money essentially constitutes money printing.

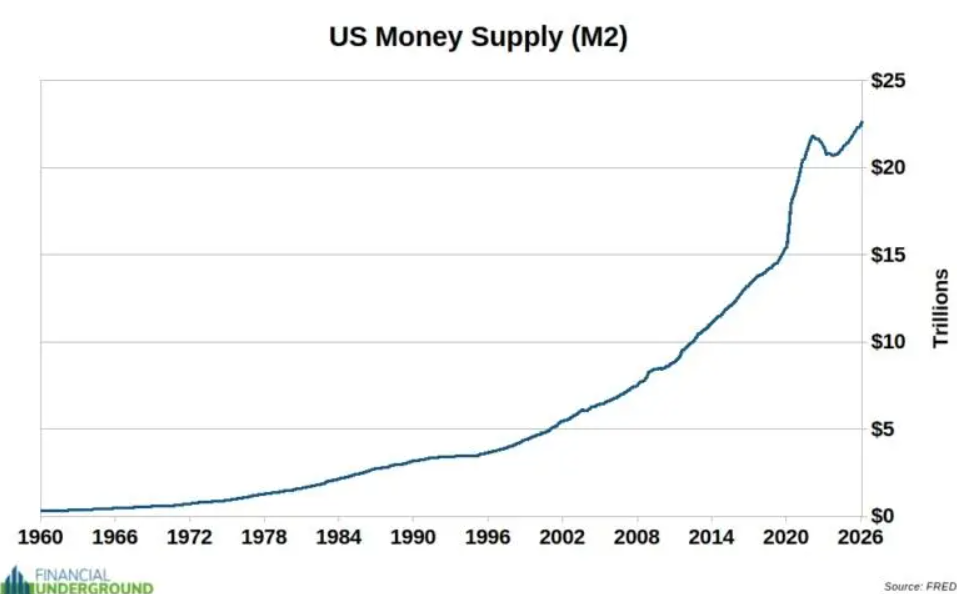

Excessive money creation

The long-term average annual growth rate of the money supply is approximately 6.8%.

During the pandemic, the Federal Reserve and other major central banks around the world injected liquidity, resulting in about 40% of the dollar supply being created in a short period of time, followed by inflation rising to a 40-year high in 2022.

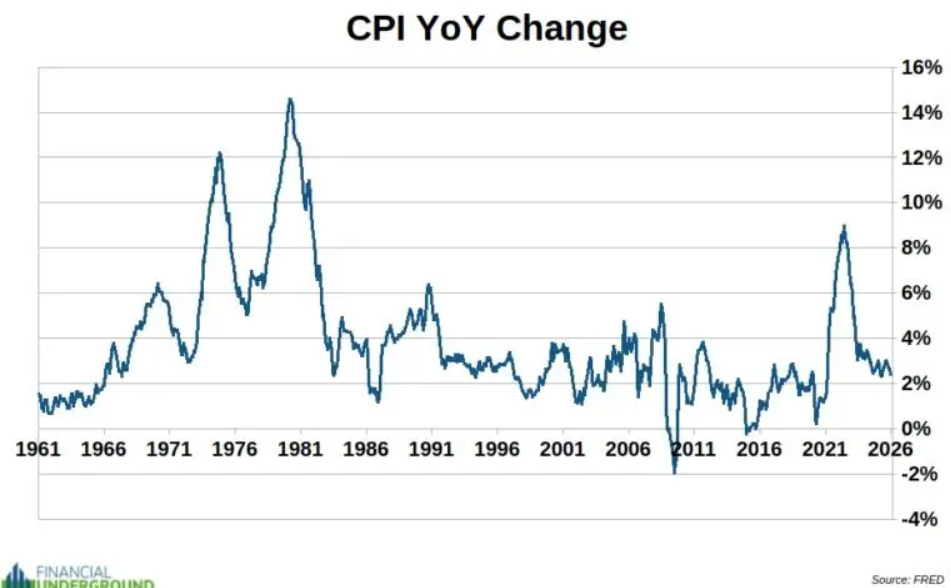

Does CPI obscure excessive money creation?

The Consumer Price Index (CPI) is among the most politically manipulated of all government statistics. This indicator attempts to measure the average price changes for 340 million Americans using a unified basket of goods, but individual consumption patterns vary significantly.

Furthermore, the government retains discretionary control over the composition and weighting of the CPI basket, raising doubts about its objectivity as a measure of inflation. Analysts believe that monitoring CPI serves more to assess the direction of Federal Reserve policy rather than to precisely measure actual inflation levels.

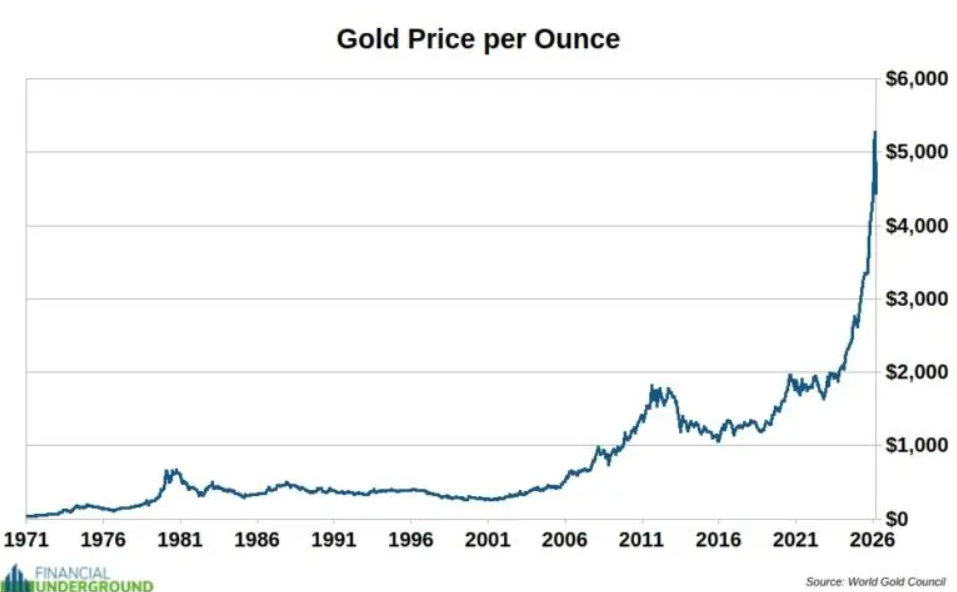

Gold hits record highs: A market reflection of stress on fiat currency systems

Gold prices have reached historical highs, reflecting a combination of the aforementioned pressures. The annual increase in gold supply is only 1% to 2%, and its supply cannot be arbitrarily expanded, giving it an inherent quality to hedge against currency depreciation.

Unlike fiat currency systems, the value of gold does not depend on any government credit or counterparty, providing it with intrinsic internationality and political neutrality. Against the backdrop of the Federal Reserve's balance sheet resuming expansion and fiscal deficits continuing to widen, gold’s appeal as a store of value is rising.

These eight indicators—federal deficits, debt levels, interest expenditures, federal funds rates and 10-year Treasury yields, the Federal Reserve’s balance sheet, money supply, CPI, and gold prices—collectively paint a systemic picture of pressure on the purchasing power of the US dollar, a trend that investors should monitor closely.

Editor/Deng