At 20:30 on Friday, the United States will release its Consumer Price Index (CPI) report for March. The market broadly anticipates a significant rise in inflation, primarily driven by soaring energy prices and trade policy factors.

Although the two-week ceasefire announced on Tuesday once eased the pressure on rising oil prices, overall, inflation in the United States may remain at a relatively high level in the first half of the year.

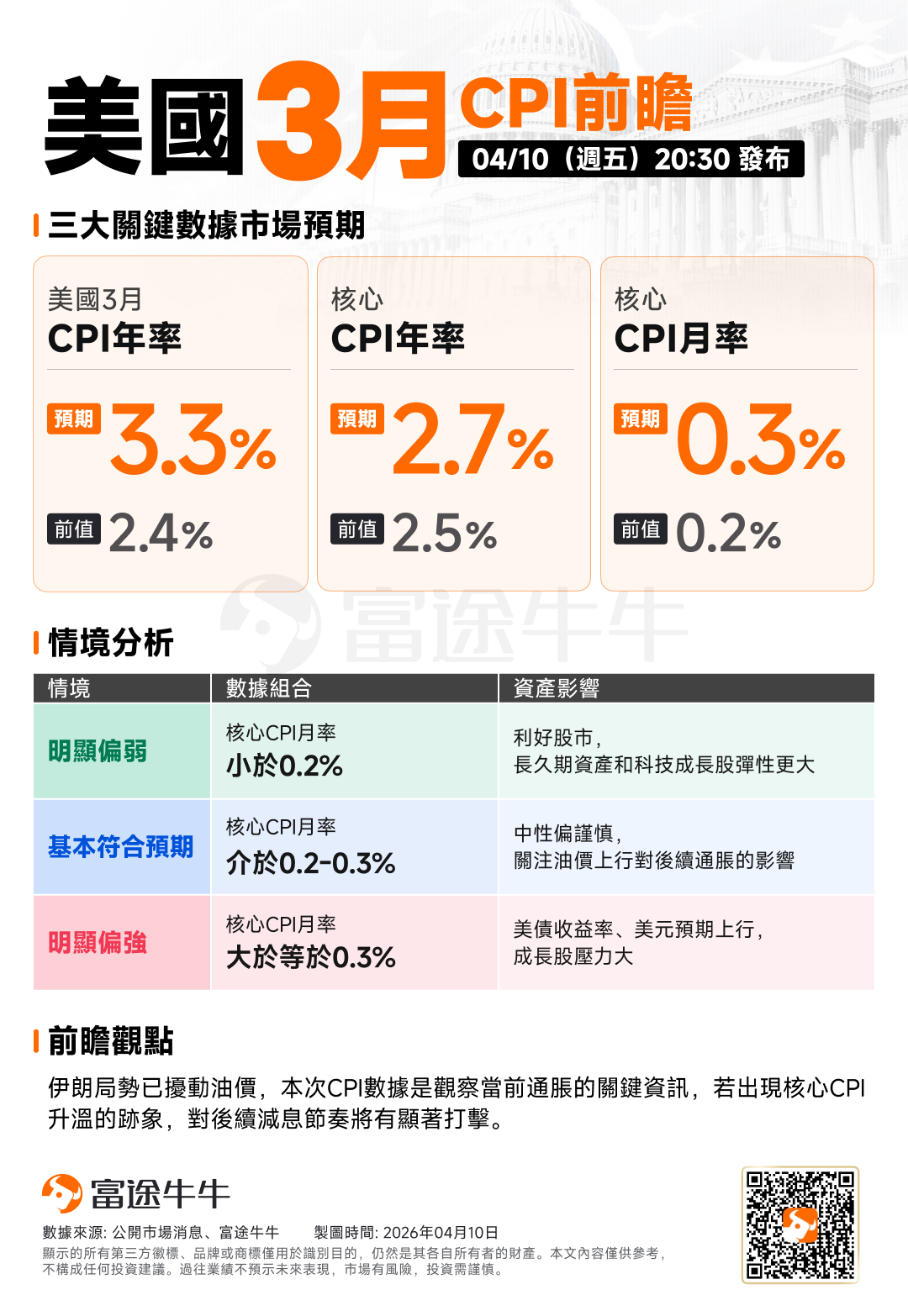

According to market expectations, overall inflation in March is projected to rise by 0.9% month-over-month, marking the largest single-month increase since June 2022 and the 17th instance of surpassing a 0.9% increase since 1981. On an annual basis, inflation is expected to rise by 3.3%, accelerating notably from 2.4% in January and February, reaching the highest level since April 2024. Excluding food and energy, core inflation is anticipated to increase by 0.3% month-over-month and 2.7% year-over-year, reflecting a slight uptick from the previous month.

Among the factors, analysts at Bank of America pointed out that energy prices in March are expected to surge by 10.6%, becoming a key driver of rising inflation.

Among the factors, analysts at Bank of America pointed out that energy prices in March are expected to surge by 10.6%, becoming a key driver of rising inflation.

From a broader industrial chain perspective, the energy shock is spreading across various sectors. Bloomberg Economics research shows that under similar oil market disruptions, commodity prices such as aviation fuel, steel, aluminum, natural gas, fertilizers, and plastics are most susceptible to increases. This cost pressure has gradually transmitted to multiple industries.

Automobile manufacturing, which relies heavily on steel, aluminum, and plastics, has seen new car prices pushed higher, further impacting the used car market. Data from Cox Automotive indicates that used car prices have risen to their highest level in nearly three years. The aviation industry has also been affected, with several airlines beginning to cut flights and raise checked baggage fees to offset rising fuel costs. In agriculture, rising fertilizer costs are expected to further drive up food prices, extending inflationary pressures from gas stations to supermarkets.

At the same time, trade policy is also intensifying price pressures. Goldman Sachs analysts Jessica Rindels and Ronnie Walker forecast that core goods inflation in March will rise to 0.22% month-over-month, significantly higher than 0.08% in February. In their April report, they noted that tariffs over the coming months will “moderately push up” inflation, affecting areas such as entertainment, education, household goods, communications, and personal care.

Analysts at JPMorgan also believe that as trade costs are passed on to end consumers, food prices will remain under pressure. Even without considering the spillover effects of energy, tariffs alone will drive up the CPI. They stated, "Regardless of where oil prices eventually stabilize, if prices stop changing, their contribution to inflation will diminish, but the drag on household spending power will correspondingly increase as price levels rise."

LPL Financial Chief Economist Jeffrey Roach similarly emphasized that tariffs will continue to provide sustained support to the CPI.

"Despite the announcement of a ceasefire and some pullback in oil prices, the pressure from trade policy has not disappeared."

As the conflict persists over several weeks, market attention has shifted from short-term oil price fluctuations to longer-term ripple effects. JPMorgan's CEO referred to inflation as the "skunk at the party," suggesting it could undermine stock market performance in 2026.

Ken Rogoff, a professor at Harvard University and former head of the International Monetary Fund, pointed out that the continuous increase in military spending may further expand the fiscal deficit, push up bond yields, thereby exerting pressure on the stock market and overall economic resilience. He also noted that the current disturbances caused by the conflict alone are sufficient to keep oil prices high over the next year.

Despite evident short-term pressures, some analysts remain relatively optimistic about the mid-term outlook. Roach indicated that the Middle East conflict has placed significant upward pressure on wholesale energy prices, an effect that may persist into the first half of 2026, driving further increases in healthcare, housing, and vehicle prices.

However, he anticipates that as the housing and durable goods markets gradually ease, overall inflation will decline in the second half of the year, creating space for policy adjustments.

“Inflation remains elevated, with challenges still present in the short term, but there is hope for a slowdown in the second half of this year, requiring investors to exercise patience.”

At the monetary policy level, the market is almost unanimous in believing that the Federal Reserve will not adjust interest rates in the short term. The CME FedWatch tool shows that 98.4% of respondents expect the Federal Reserve to maintain interest rates in the range of 3.50% to 3.75% at the meeting scheduled for the end of April. Roach stated that while the economy is slowing, it has not yet entered a recessionary phase, “Inflation remains very high, so the Federal Reserve needs to continue observing.”

Looking ahead to future policy paths, as inflation gradually eases later in the year, the market still anticipates room for rate cuts. According to data from the CME FedWatch tool as of midday Wednesday, approximately 15.4% of market participants expect a 25-basis-point rate cut at the September meeting.

The ultimate response of the Federal Reserve will largely depend on the CPI data released on Friday. If inflation turns out to be significantly higher than expected, calls for another rate hike may resurface in the market. However, against the backdrop of a weakening labor market, the policy stance will face more complex trade-offs. This dilemma represents one of the most prominent challenges in the current macroeconomic environment.

Stay ahead with key financial updates and discover investment opportunities early! Open Futubull > Market > US Stocks >Economic Calendar/Selected macroeconomic data, seize the investment opportunity!

Stay ahead with key financial updates and discover investment opportunities early! Open Futubull > Market > US Stocks >Economic Calendar/Selected macroeconomic data, seize the investment opportunity!

Editor/KOKO