① As the conflict in the Middle East and Iran's blockade of the Strait of Hormuz triggered a surge in energy prices, US CPI data has undoubtedly once again surpassed non-farm payrolls as the most closely watched US economic indicator at this stage; ② Tonight at 8:30 PM Beijing time, the US Department of Labor will release the highly anticipated March CPI data, which will also be the first US inflation report reflecting the 'war premium' from the Middle East...

Cailian Press, April 10 (Edited by Xiaoxiang) As the conflict in the Middle East and Iran's blockade of the Strait of Hormuz triggered a surge in energy prices, US CPI data has undoubtedly once again surpassed non-farm payrolls as the most closely watched US economic indicator at this stage. Tonight at 8:30 PM Beijing time, the US Department of Labor will release the highly anticipated March CPI data, which will also be the first US inflation report reflecting the 'war premium' from the Middle East...

Market insiders generally expect that due to the war between the US, Israel, and Iran driving up oil prices and the ongoing impact of tariff transmission effects, the US Consumer Price Index for March is likely to record its largest month-on-month increase in nearly four years. This would further diminish hopes for interest rate cuts this year.

Over the past month, the conflict involving the US and Israel against Iran has caused US gasoline prices to soar above $4 per gallon. Therefore, it is almost certain that the trend of slowing oil price growth reflected in US inflation indicators at the beginning of the year will be overturned. Of course, what concerns market observers is not just energy prices: about one-third of global maritime fertilizer shipments pass through the Strait of Hormuz, which could ultimately exacerbate already high food prices.

Over the past month, the conflict involving the US and Israel against Iran has caused US gasoline prices to soar above $4 per gallon. Therefore, it is almost certain that the trend of slowing oil price growth reflected in US inflation indicators at the beginning of the year will be overturned. Of course, what concerns market observers is not just energy prices: about one-third of global maritime fertilizer shipments pass through the Strait of Hormuz, which could ultimately exacerbate already high food prices.

Therefore, many industry insiders are focusing tonight on the performance of overall CPI data, particularly the month-on-month indicator.

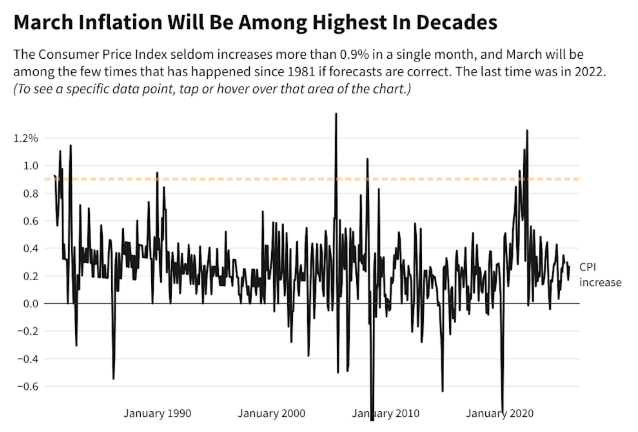

According to a survey of economists by the media, economists expect that the US CPI report, scheduled for release on Friday, will show that the US inflation rate rose by 0.9% month-on-month in March.

This expected month-on-month increase of 0.9% is itself a rather striking figure. Notably, since 1981, there have only been 16 instances where the US monthly CPI increased by 0.9% or more month-on-month, making this potentially the largest month-on-month rise since June 2022 – a period when the US CPI annual increase exceeded 9%.

In terms of year-on-year figures, economists predict that this month-on-month increase will push the March CPI up by 3.3% year-on-year, reaching the highest level since April 2024. In February, the US CPI was up 2.4% year-on-year – indicating a difference of nearly one percentage point between the previous value and current market expectations...

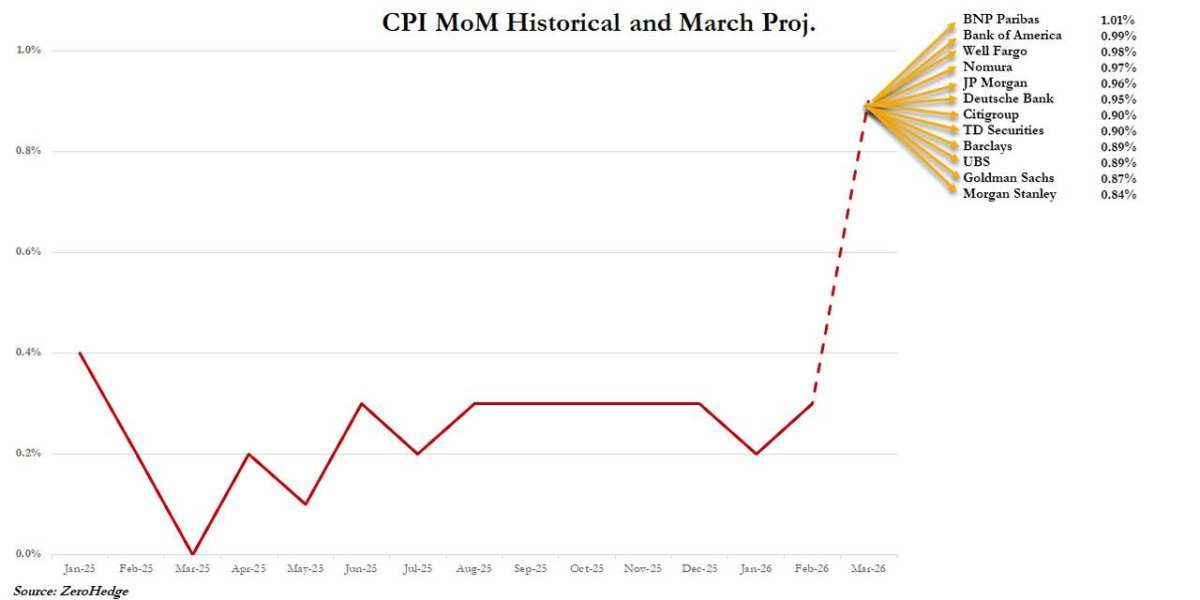

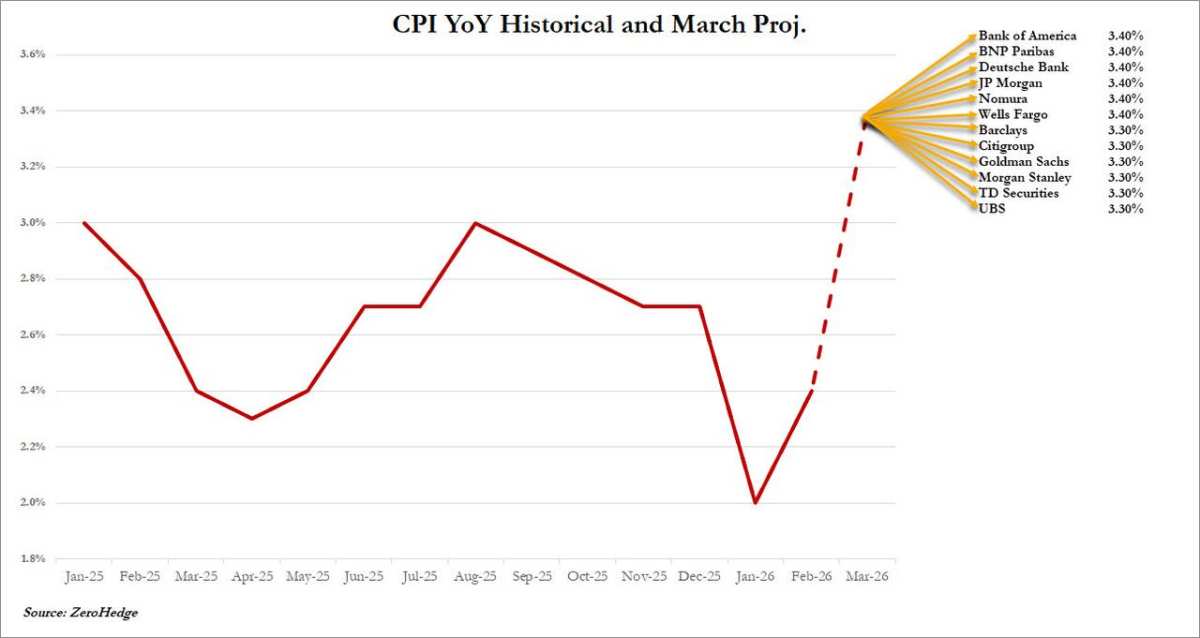

Overview of Wall Street Investment Bank Estimates

The chart below shows specific forecasts by Wall Street investment banks for the month-on-month March CPI data. It can be observed that most bank estimates are above 0.8%, with some institutions predicting a possible month-on-month increase exceeding 1%.

The chart below shows the forecast distribution of the year-over-year increase in the March CPI, broken down by major investment banks. Based on the forecasts from these banks, it is almost certain that the year-over-year increase in the March CPI will exceed 3%.

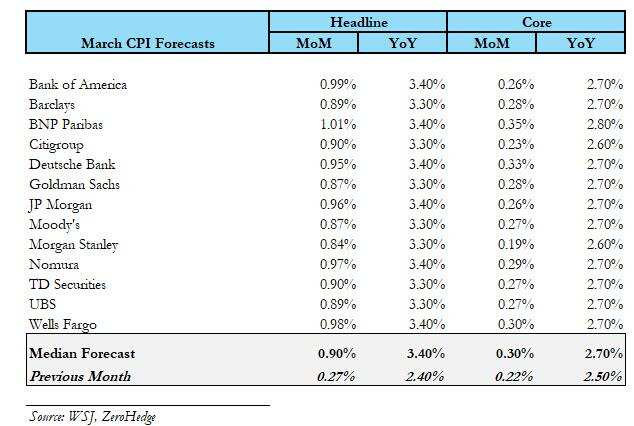

Below is a complete summary of the forecasts from major investment banks:

Jim Reid, head of macro research at Deutsche Bank, wrote in a commentary, 'The impact of the energy price shock will be fully reflected in the March CPI report.'

Brian Bethune, professor of economics at Boston College, also predicted that 'tonight’s overall CPI data will be quite unattractive, and the next wave of shocks may also be approaching; fuel surcharges will begin to show up and pass through to other goods, especially food prices, which will be impacted.'

Of course, since this is still only the first inflation report reflecting the impact of the Middle East conflict, the fluctuations in core CPI for March, excluding energy and food prices, may remain relatively moderate for now – economists surveyed by the media expect that core inflation in the U.S. will rise by 0.3% month-over-month and 2.7% year-over-year in March, compared with previous values of 0.2% and 2.5%, respectively.

Stephen Juneau, an economist at Bank of America, stated in a report this week, 'Although it may still be difficult to discern the impact of the Iran war on core inflation, we will closely monitor airfares and logistics services to see if there are any early signs that rising oil prices are permeating into a broader basket of goods.'

Additionally, the impact of tariffs may continue to put pressure on prices. Goldman Sachs economists Jessica Rindels and Ronnie Walker pointed out in a report this week that tariffs are expected to 'continue to moderately push up monthly inflation in the coming months,' affecting categories such as leisure and entertainment, home furnishings, and more.

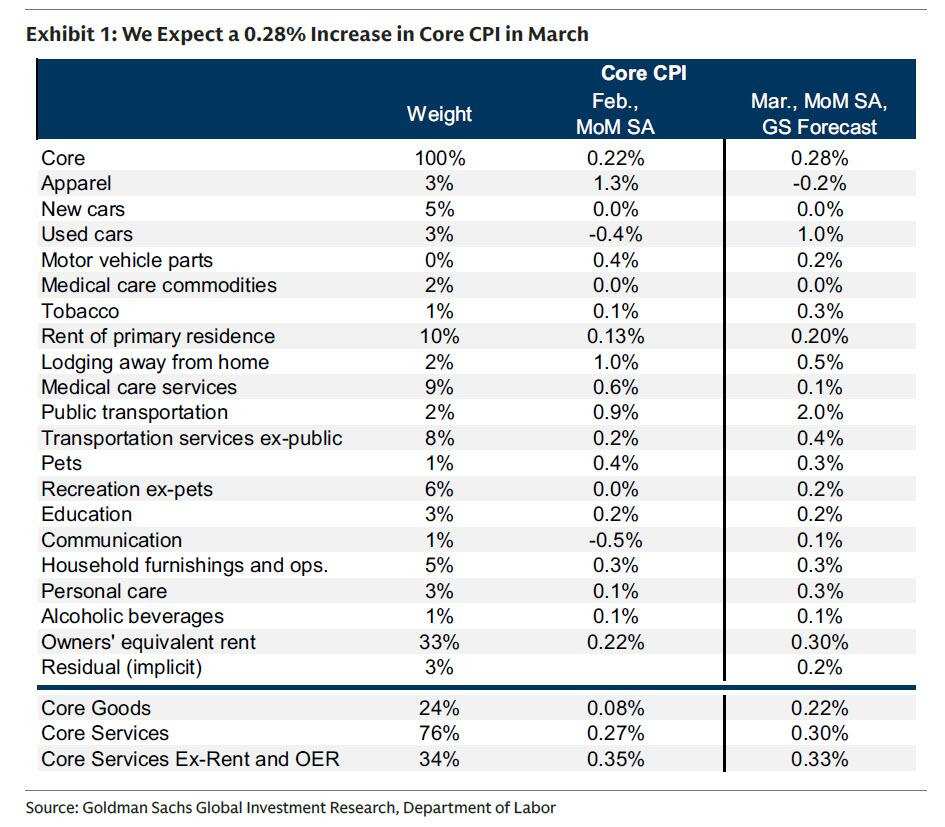

Goldman Sachs’ specific outlook

Regarding tonight’s performance of the U.S. March CPI, Goldman Sachs expects the year-over-year increase in overall CPI to be 3.28%, with a month-over-month increase of 0.87% – both consistent with current mainstream market expectations. Goldman Sachs noted that overall CPI was mainly driven by rising food prices (up 0.3% month-over-month) and a significant jump in energy prices (up 9.4%), which itself reflects the rise in oil and retail gasoline prices since the outbreak of the Iran war.

Upon closer inspection of Goldman Sachs' forecast report, the bank highlighted trends in four key components of inflation expected to be seen in this week’s report:

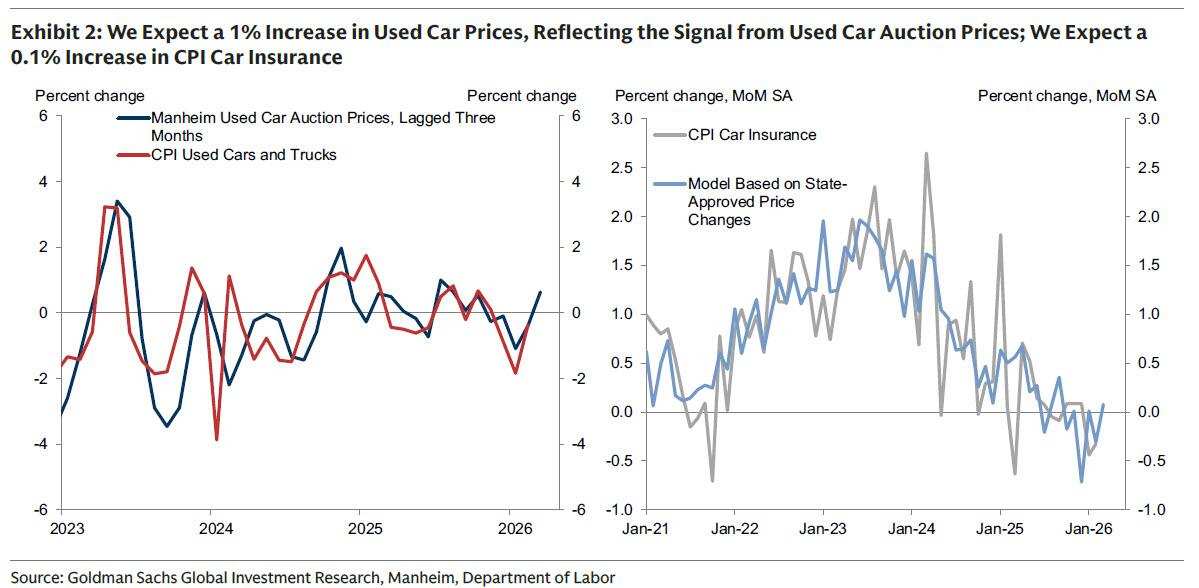

① Automobiles. Goldman Sachs believes that automobile inflation is expected to be uneven, reflecting a 1% increase in used car prices based on signals from used car auction prices; stable new car prices, reflecting largely unchanged incentives for new car sales; and a 0.1% rise in auto insurance premiums, reflecting premium increases indicated by Goldman Sachs' online datasets.

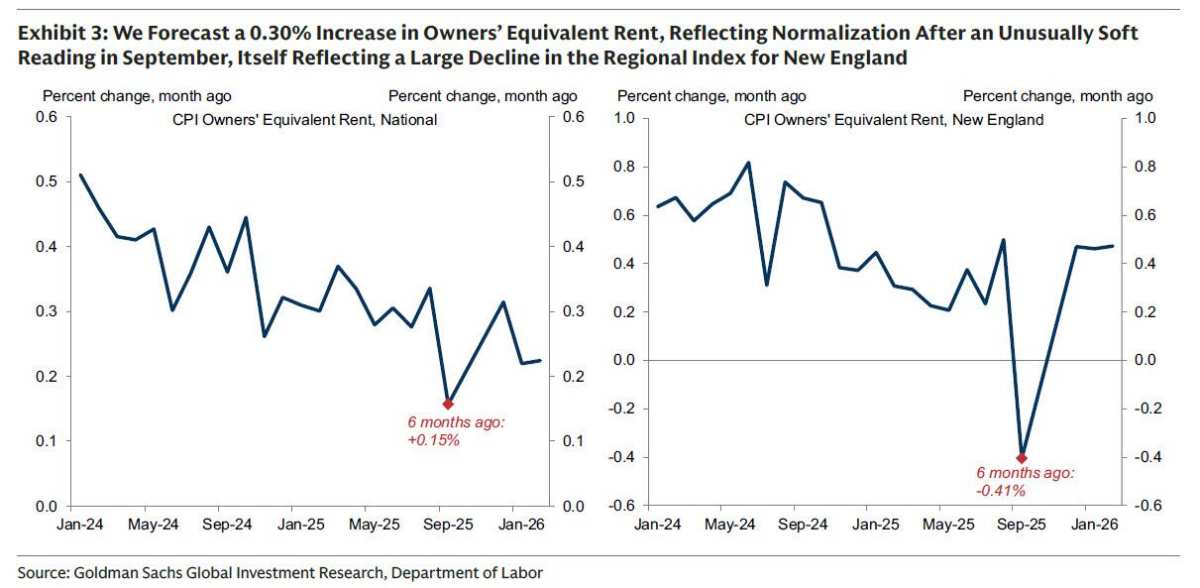

② Housing. Goldman Sachs forecasts a mild month-on-month growth of 0.20% in the rent category, reflecting the continued slowdown in its underlying trend. The firm also predicts that the Owners' Equivalent Rent (OER) category will accelerate to 0.30%, reflecting upward pressure from the rebound of an unusually weak reading in September, which itself was driven by a larger decline in the OER index in the New England region.

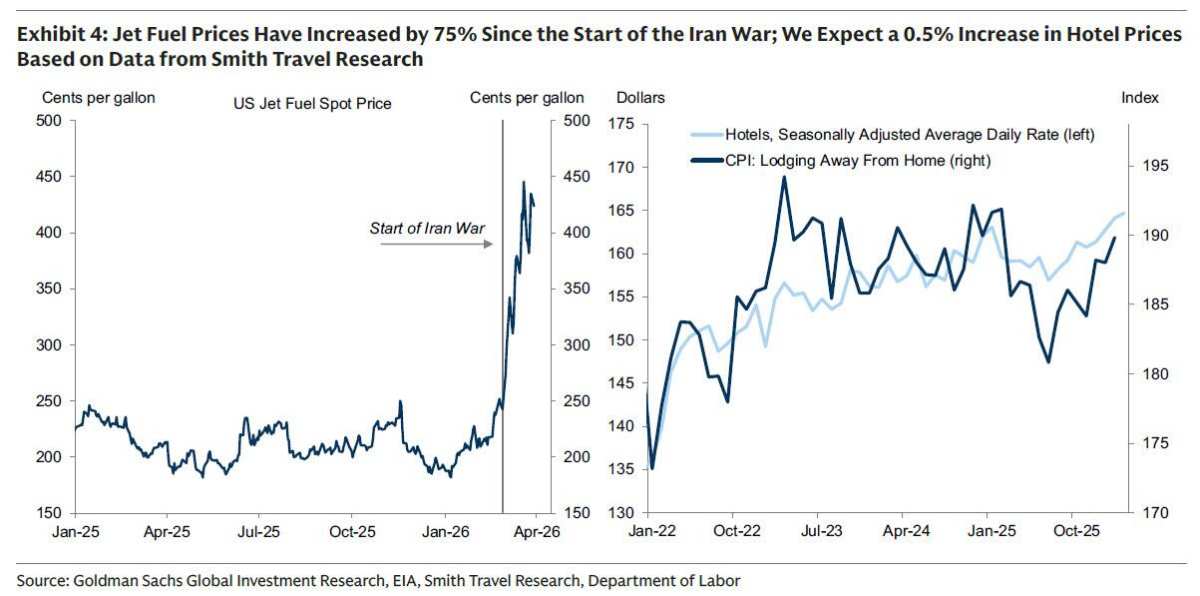

③ Travel services. Goldman Sachs anticipates robust travel service inflation in March, partly reflecting the transmission effects of rising oil prices since the start of the Iran conflict. The firm forecasts a 4% month-on-month increase in airfare, partly reflecting a significant rise in aviation fuel prices, and a 0.5% month-on-month rise in hotel prices in March, reflecting upward signals from alternative price data.

④ Tariffs. Goldman Sachs expects tariffs to exert upward pressure on highly exposed categories, contributing +0.03 percentage points to core inflation in March. The firm believes tariffs may drive price increases in entertainment (+0.2%), education (+0.2%), home furnishings (+0.3%), communications (+0.1%), and personal care (+0.3%).

It is particularly noteworthy that Goldman Sachs believes that after the year-on-year increase in the March Consumer Price Index (CPI) “breaks 3,” energy prices may surge again in April, pushing the overall year-on-year CPI increase in April to around 4%.

To put this into perspective, the last time U.S. inflation exhibited such a “successive upward breach of integer thresholds” was in 2022. At that time, the post-pandemic supply chain crisis coupled with the energy price spike triggered by the Russia-Ukraine conflict led to a year-on-year CPI increase exceeding 9% in June 2022.

The 'key battle' determining the direction of the Federal Reserve’s interest rate policy

Minutes from the Federal Reserve’s March meeting released earlier this week showed that “the vast majority” of officials believed that the process of U.S. inflation easing could be slower than expected due to three interrelated concerns: the impact of tariffs on goods prices might take longer to fade; oil prices were seeping into core inflation metrics; and years of above-target inflation might make consumers and businesses more accepting of further price increases.

At present, the energy price shock brought about by the U.S.-Iran conflict undoubtedly has made the Federal Reserve increasingly cautious.

Recent remarks by Federal Reserve officials have generally leaned toward maintaining unchanged interest rates while assessing the impact of the energy shock until inflation shows clearer directional progress. Policymakers indicated that rate cuts would require labor market weakness, while rate hikes are not the baseline scenario but cannot be ruled out if inflation surges. Geopolitical events in the Middle East could push up inflation via energy and supply chains while harming growth, so brief shocks might be overlooked, but any prolonged shock could delay the timing of rate cuts.

In fact, compared to the CPI report for March, what is more concerning is the performance of U.S. prices in the coming months. Some economists predict that the Middle East conflict will push up core prices through expensive aviation fuel (which will raise airfare) and diesel (which will increase the cost of road freight transportation). Prices of commodities such as fertilizers and plastics are also expected to rise.

"The price increases we are observing are already in the transmission process, and we will continue to see rising inflation," said Dan North, senior economist at Allianz Trade Americas. The duration of the geopolitical conflict will determine how long the inflationary impact persists.

The rising inflation has led some economists to believe that the Federal Reserve will not cut interest rates this year, a view further reinforced after the release of the minutes from the Fed's policy meeting on March 17-18.

Gregory Daco, chief economist at EY Parthenon, stated, "When we look ahead, say to the fourth quarter and the end of 2026, there may be factors prompting the Federal Reserve to ease monetary policy, but it will be for unfortunate reasons (such as a recession). Meanwhile, we must now confront a very real possibility: the Fed’s next move might be a rate hike."

Nick Timiraos, a well-known journalist often referred to as the 'new Fedwire,' recently noted that the Fed's recent cautious stance echoes a framework proposed over two decades ago by then-Chairman Ben Bernanke. Bernanke argued that the central bank’s response to oil price shocks should depend on the prevailing level of inflation at the time of the shock. When inflation is already low and inflation expectations are firmly anchored, policymakers can 'look through' or disregard inflationary impacts caused by rising energy prices.

However, when inflation is already above the target level, supply shocks may further destabilize inflation expectations, which would require tighter policies—some officials believe this may be closer to the situation currently faced by the Fed.

Stay ahead with key financial updates and discover investment opportunities early! Open Futubull > Market > US Stocks >Economic Calendar/Selected macroeconomic data, seize the investment opportunity!

Stay ahead with key financial updates and discover investment opportunities early! Open Futubull > Market > US Stocks >Economic Calendar/Selected macroeconomic data, seize the investment opportunity!

Editor /rice