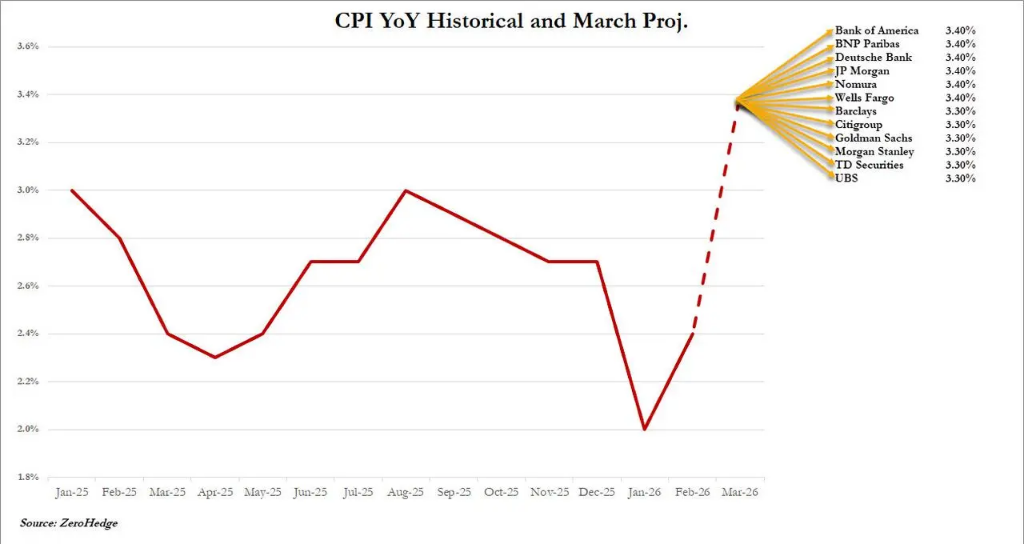

Due to the energy price shock triggered by the U.S.-Iran conflict, the U.S. CPI for March is expected to increase by 0.9% month-over-month, potentially marking the largest monthly rise since June 2022; the year-over-year increase may climb to 3.4%, the highest in two years. The energy component may surge by more than 10%, transmitting a "second wave" of pressure into sectors such as transportation and food. This data performance could force the Federal Reserve to abandon its plan to cut interest rates this year, or even restart discussions on rate hikes.

At 20:30 Beijing time, the U.S. March Consumer Price Index (CPI) report will be released, with the market widely expecting it to show the largest monthly inflation increase in nearly four years. The energy price shock caused by the Iran war is the core driver, while the secondary transmission effects have yet to fully materialize, which will further compress the Federal Reserve's room for interest rate cuts this year.

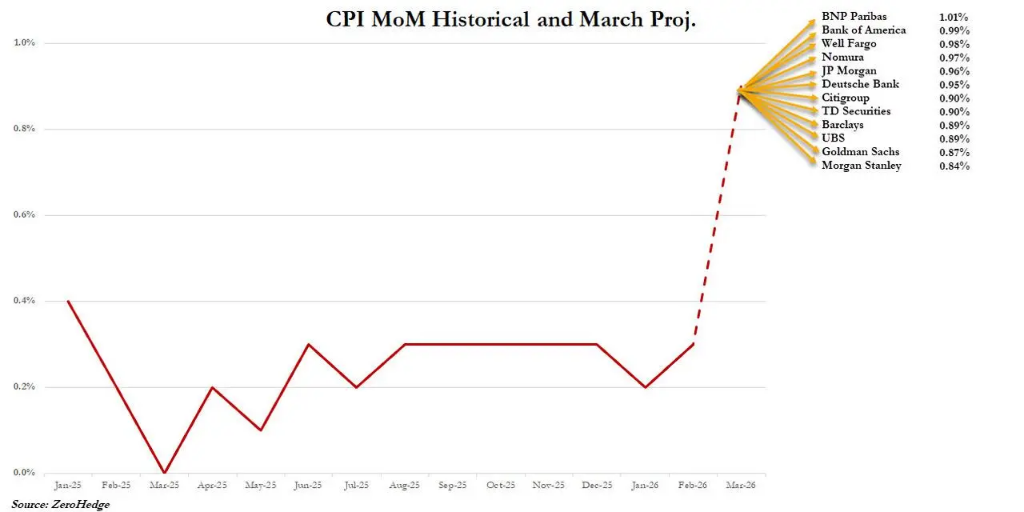

According to a survey of economists by the media, the CPI for March is expected to rise by 0.9% month-over-month, with the annual increase forecasted to jump from 2.4% in February to 3.3%, marking the largest yearly increase since May 2024; if the 0.9% monthly increase is realized, it would represent the largest monthly increase since the Russia-Ukraine conflict in June 2022. Some Wall Street institutions predict an even more aggressive scenario, with a median expectation for an annual increase of 3.4%. The Cleveland Fed’s real-time forecast points to an annual increase of approximately 3.25%. Impacted by the U.S.-Iran war, global crude oil prices have soared by over 30%, and the national average retail gasoline price has surpassed $4 per gallon for the first time in more than three years.

The timing of this data release is particularly sensitive. Minutes from the Federal Reserve’s March policy meeting released this week indicate that an increasing number of officials believe rate hikes may become necessary; the federal funds rate currently stands at a range of 3.50% to 3.75%. Several economists argue that if the impact of high oil prices continues to transmit to core inflation, the window for the Federal Reserve to cut interest rates this year will significantly narrow, and the possibility of a rate hike cannot be ruled out.

The timing of this data release is particularly sensitive. Minutes from the Federal Reserve’s March policy meeting released this week indicate that an increasing number of officials believe rate hikes may become necessary; the federal funds rate currently stands at a range of 3.50% to 3.75%. Several economists argue that if the impact of high oil prices continues to transmit to core inflation, the window for the Federal Reserve to cut interest rates this year will significantly narrow, and the possibility of a rate hike cannot be ruled out.

It is worth noting that the current CPI data does not fully reflect all the effects of the energy shock. Several economists warn that as jet fuel costs push up airfare, rising diesel prices drive up land transportation costs, and prices for commodities like fertilizers and plastics increase, the "second wave" effect of the energy shock being transmitted to core inflation will gradually emerge in the coming months.

The energy component may soar by more than 10%, driving the overall CPI spike.

The core driver behind the March CPI jump is the energy shock caused by the Iran conflict. According to a research report published by JPMorgan on the 9th, energy prices in March are expected to increase by about 11% month-over-month, making it the primary factor behind the significant rise in overall CPI. Goldman Sachs forecasts a 9.4% month-over-month increase in the energy component, with food prices also expected to rise by 0.3%.

Goldman Sachs predicts an overall CPI increase of 0.87% month-over-month, corresponding to an annual increase of 3.28%; JPMorgan forecasts a 0.96% month-over-month jump in overall CPI, with an annual increase reaching 3.4%. A Reuters survey shows wide-ranging estimates from various institutions, ranging from 0.4% to 1.7%, reflecting significant market divergence regarding the magnitude of the oil price shock.

"The overall CPI data will look quite ugly," said Brian Bethune, a professor of economics at Boston College.

"There is a second wave of shocks brewing – fuel surcharges will begin to appear and transmit to other commodities, with food being the most vulnerable."

Despite Trump's announcement on Tuesday of a two-week ceasefire agreement with Iran, contingent upon Tehran reopening the Strait of Hormuz, the ceasefire is widely considered fragile. Dan North, Chief Economist for the Americas at Allianz Trade, stated, "Even though oil prices have retreated somewhat recently, the effect of higher prices has already entered the transmission pipeline, and inflationary pressures will persist." He added that the duration of the conflict would be the key variable determining the length of the inflationary impact.

Core inflation remains relatively moderate, but secondary transmission pressures cannot be ignored.

Compared to the significant jump in overall CPI, the core CPI, which excludes food and energy, is expected to rise more moderately. According to media surveys, the core CPI is projected to increase by 0.3% month-on-month, with annual growth rising slightly from 2.5% in February to 2.7%. Goldman Sachs forecasts a 0.28% monthly increase in core CPI, with an annual rate of 2.69%, while JPMorgan predicts a 0.26% monthly increase, both slightly below market consensus.

Goldman Sachs outlined four key components of core inflation trends in its report: First, automobiles, with used car prices expected to rise by about 1%, new car prices remaining largely flat, and auto insurance rates increasing slightly by 0.1%; second, housing costs, with rental components projected to rise moderately by 0.2%, and owner's equivalent rent (OER) expected to rebound to 0.3% due to technical corrections following weaker data; third, travel services, with jet fuel costs surging, leading to an anticipated 4% increase in airfare and a 0.5% rise in hotel prices; fourth, tariff effects, contributing approximately 0.03 percentage points to core inflation across categories such as entertainment, education, home goods, communications, and personal care.

Economists have also warned that rising producer prices and factory raw material input costs indicate pipeline pressures may keep core inflation elevated. Gregory Daco, Chief Economist at EY Parthenon, noted, "Looking toward the end of this year, there may be factors prompting the Federal Reserve to ease policy, but it would likely stem from negative reasons. We must seriously consider the realistic possibility that the next move by the Fed could be a rate hike."

The Federal Reserve faces a dilemma as the window for rate cuts continues to narrow.

Inflation data will make the Fed's policy position increasingly challenging. Minutes from the March policy meeting released this week revealed that an increasing number of Fed officials have begun discussing the need for rate hikes, with the benchmark interest rate currently remaining in the range of 3.50% to 3.75%.

Recent public statements by Fed officials have generally leaned toward maintaining interest rates unchanged until inflation shows clearer signs of easing, while assessing the ongoing impact of the energy shock. Officials indicated that rate cuts would require a significant weakening in the labor market, and while a rate hike is not the baseline scenario, it remains a possibility if inflation rebounds sharply. Officials also noted that inflation expectations remain well-anchored.

March employment data showed the labor market remains robust, but economists are concerned that prolonged Middle East conflicts and high oil prices could gradually erode consumer purchasing power, weighing on employment. Some economists pointed out that reduced consumer spending amid high oil prices would also make it difficult for businesses to fully pass on energy costs, creating a reverse drag on demand.

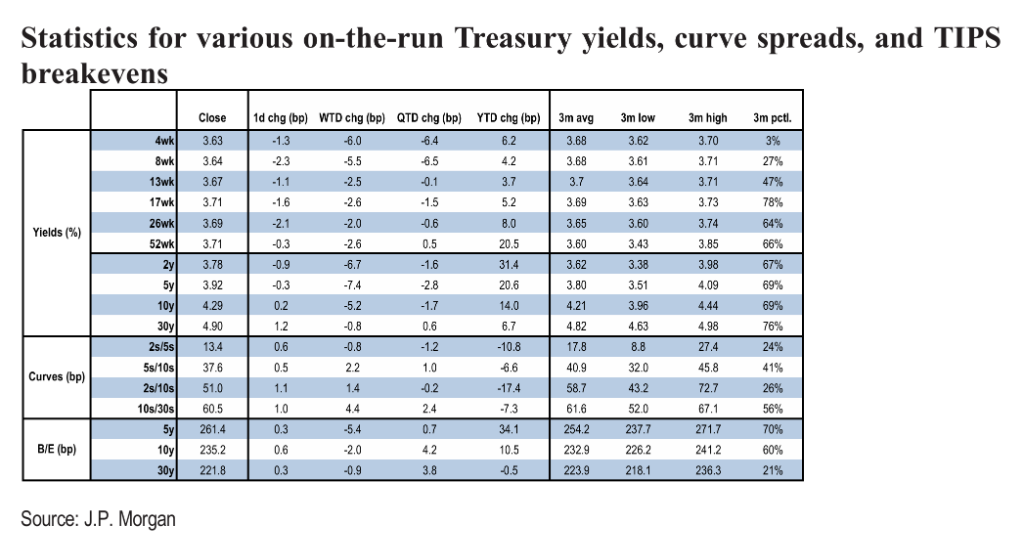

TIPS holdings are expected to yield returns at their highest levels since the Russia-Ukraine conflict.

The impact of this CPI data on the fixed-income market is also significant. According to JPMorgan's fixed-income strategy report, if the March CPI aligns closely with forecasts, the May holding returns for 5-year TIPS and breakeven positions will surge to their highest levels since the Russia-Ukraine conflict in 2022.

JPMorgan forecasts that the unadjusted CPI-U index for March will rise to 330.613, surpassing both the Bloomberg consensus (330.535) and the market pricing level (330.380). The bank believes that the valuation of breakeven inflation rates remains relatively low, and the current fixing market’s expectations for inflation this year are below its internal forecasts, indicating room for further widening of breakeven inflation rates. However, given the high degree of uncertainty in geopolitical conditions and elevated market volatility, JPMorgan maintains a neutral stance on breakeven inflation rates ahead of the data release.

The U.S. Treasury market has recently experienced significant fluctuations due to conflicting geopolitical signals, fully reflecting the market's dilemma between high inflation and economic downside risks. Tonight’s CPI data will provide key pricing guidance for this dynamic.

Stay ahead with key financial updates and discover investment opportunities early! Open Futubull > Market > US Stocks >Economic Calendar/Selected macroeconomic data, seize the investment opportunity!

Stay ahead with key financial updates and discover investment opportunities early! Open Futubull > Market > US Stocks >Economic Calendar/Selected macroeconomic data, seize the investment opportunity!

Editor/joryn