Driven by the surge in oil prices amid the Iran conflict, the US CPI recorded its largest month-over-month increase in nearly four years in March. However, core indicators suggest inflation is stabilizing, leading markets to slightly raise their bets on a single rate cut by the Federal Reserve later this year.

The US inflation rate in March recorded the largest month-over-month increase in nearly four years due to a surge in gasoline prices caused by the war with Iran.

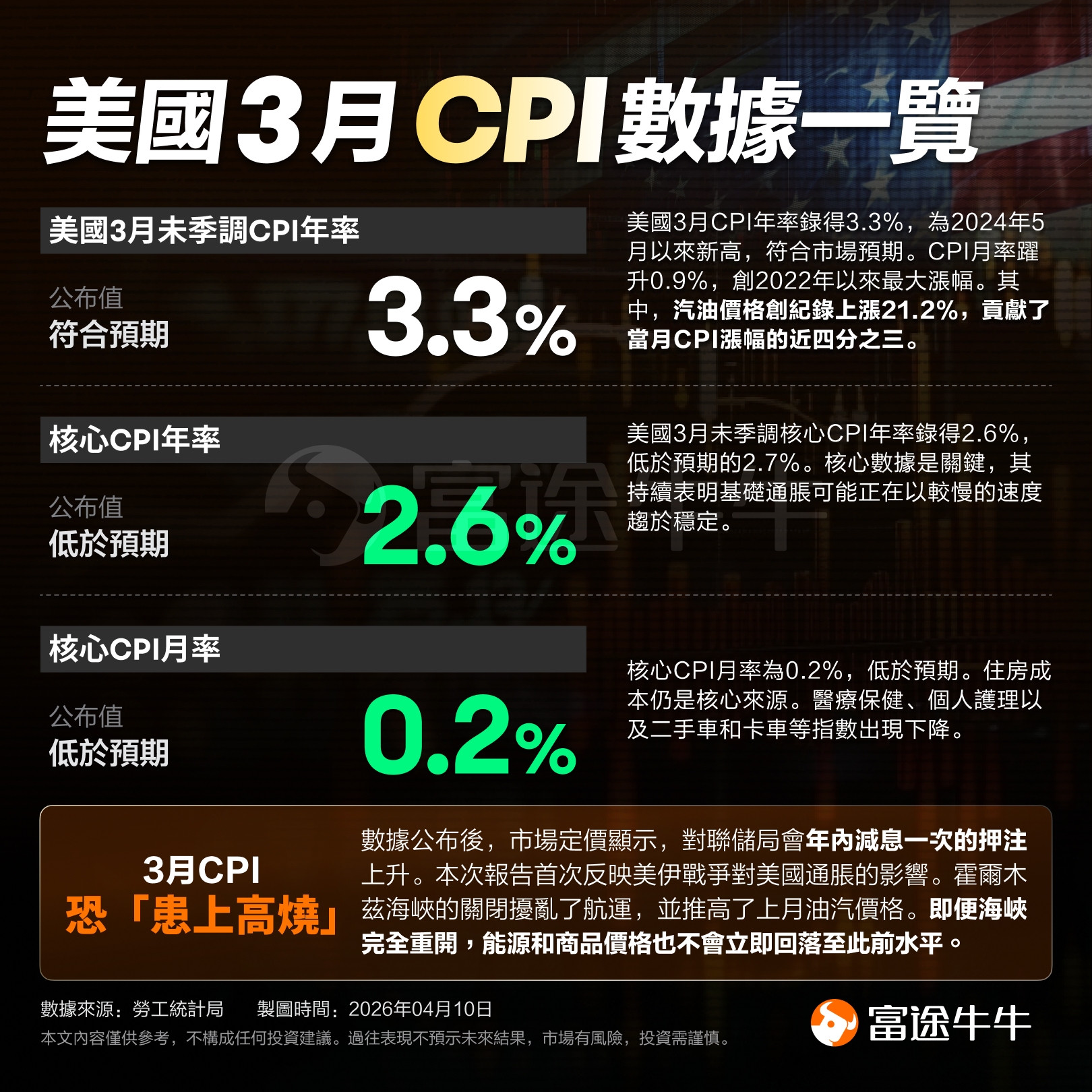

The unadjusted year-over-year CPI for the US in March reached 3.3%, the highest since May 2024, meeting market expectations and surpassing the previous reading of 2.4%; the seasonally adjusted month-over-month CPI for March hit 0.9%, the highest since June 2022, in line with market forecasts, compared to the prior value of 0.3%. The unadjusted core CPI year-over-year rate for March was 2.6%, below the expected 2.7% and down from the prior reading of 2.50%; the seasonally adjusted core CPI month-over-month rate for March stood at 0.2%, below the anticipated 0.3% and unchanged from the previous value of 0.2%.

Following the release of the CPI data, spot gold surged more than $10 in a short period, currently trading at $4,775 per ounce. Market pricing indicates that bets on one interest rate cut by the Federal Reserve this year have increased.

Following the release of the CPI data, spot gold surged more than $10 in a short period, currently trading at $4,775 per ounce. Market pricing indicates that bets on one interest rate cut by the Federal Reserve this year have increased.

Notably, the rise in gasoline prices within the US CPI marked the highest record since 1967, with gasoline price increases accounting for nearly three-quarters of the overall CPI increase. The US Bureau of Labor Statistics reported that the unadjusted energy inflation for March rose 10.9% month-over-month and 12.5% year-over-year.

Market analyst Chris Anstey noted that the headline figures met expectations. However, the core data remains critical, as it continues to indicate that underlying inflation may be stabilizing at a slower pace.

Market analyst Enda Curran remarked that if there were any lingering questions about how the war with Iran would impact inflation, the March CPI data has largely dispelled uncertainty. Energy prices experienced a significant jump within a single month and will clearly transmit into other areas of the economy. The key question is whether this shock is 'temporary' or more persistent.

Just before the release of the CPI data, San Francisco Federal Reserve President Mary Daly had prepared the market with a 'warning.' Daly stated that even before the oil price shock, the US had work to do in addressing inflation, and now it simply requires more time.

Daly noted that if the conflict with Iran is resolved quickly and oil prices retreat, a rate cut is 'not out of the question'; however, if inflation remains higher than expected for an extended period, the Fed will remain on hold until it is confident that the inflation issue has been addressed. She believes the likelihood of a rate hike is lower than that of a rate cut or maintaining current rates.

Daly pointed out that persistently high oil prices would imply rising inflation but would also impact economic growth. She has already observed higher prices being passed through to the economy, with people reducing travel due to concerns over rising costs. However, she emphasized that this is not a fundamental price increase. She noted that it is necessary to observe how the conflict unfolds and how companies pass on price increases. She highlighted that the real question is whether the ceasefire can hold; if it does, then the CPI data becomes irrelevant; the high inflation figures themselves would not surprise anyone.

Daly stressed that bringing inflation down to 2% is crucial, but doing so at the expense of employment would place households in dire straits. Currently, the risks to the Federal Reserve achieving its dual mandate of full employment and inflation targets are broadly balanced.

"Fed's Voice": The surge in fuel prices was anticipated; the key lies in its ripple effects.

As Nick Timiraos, often referred to as the "Fed's voice," stated after the release of the CPI data, Fed officials had long prepared for a significant increase in fuel prices. The CPI report released on Friday further explained why they decided to pause interest rate adjustments at last month’s meeting. At that time, Fed Chair Powell indicated they were ready to overlook the spike in energy prices, treating it as a supply shock that pushed up prices while tightening household budgets.

Timiraos noted that typically, a one-off energy shock would not trigger a policy response. However, this is the fourth such shock in six years, and Powell has warned that a series of one-off disruptions could erode public confidence in inflation returning to normal levels. This implies that officials will closely monitor whether cost increases driven by fuel, tariffs, or other factors (such as AI investments) are transmitted more broadly, and whether consumers begin to view larger price hikes as the norm.

Before the outbreak of the war, there were indeed some signs of improvement in the CPI, thanks to the continued slowdown in housing costs. Additionally, core inflation—excluding volatile food and energy categories—performed well again in March.

However, Timiraos pointed out that the Personal Consumption Expenditures Price Index (PCE), which the Fed prefers to focus on, has risen slightly in recent months. According to the minutes of the Fed’s March meeting released on Wednesday, the vast majority of officials believed that progress toward bringing inflation down to target levels this year might be slower than previously expected. This is mainly due to three overlapping factors: the impact of tariffs on goods prices, the transmission of rising energy costs to other goods and services, and persistently above-target inflation rates over the years, making consumers and businesses more prone to accepting further price increases.

Although a ceasefire reduces the risk of further sharp price increases and the resulting demand contraction weakening the economy, paradoxically, it increases the likelihood of interest rates remaining unchanged for a longer period. This is because the elimination of the worst impacts of the conflict on economic growth outweighs any easing of inflationary pressures, especially if shipping bottlenecks in the Strait of Hormuz prove harder to resolve or introduce new costs.

Timiraos mentioned that several Fed officials have indicated they may not support interest rate cuts for most of the year. The rationale for resuming rate cuts without a recession hinges entirely on sustained downward pressure on inflation. However, the Iran conflict has interrupted this process for at least several months, and even if a fragile ceasefire holds, conditions cannot revert to their pre-war state.

Stay ahead with key financial updates and discover investment opportunities early! Open Futubull > Market > US Stocks >Economic Calendar/Selected macroeconomic data, seize the investment opportunity!

Stay ahead with key financial updates and discover investment opportunities early! Open Futubull > Market > US Stocks >Economic Calendar/Selected macroeconomic data, seize the investment opportunity!

Editor/Lambor