The Middle East conflict has triggered the largest energy supply disruption in history, prompting global capital to reassess the strategic value of renewable energy. CATL's stock price hit a new all-time high, with strong performances across photovoltaic, lithium battery, wind power, and electric vehicle sectors. Dongwu Securities maintained its "Buy" rating for CATL, projecting that electric vehicle exports will grow by over 70% for the year and global energy storage installations will increase by more than 60%. Huaxin Securities pointed out that "energy independence and controllability" will become a core investment theme in the coming years, with renewable energy generation, energy storage, and grid equipment presenting strategic opportunities.

The fires of war in the Middle East are reshaping the global energy landscape, with China's new energy industrial chain emerging as one of the biggest beneficiaries of this crisis.$CATL (03750.HK)$Stock prices hit record highs as sectors related to photovoltaics, wind power, lithium batteries, and electric vehicles took turns strengthening. Behind the collective surge in A-share new energy stocks lies a clear energy security logic that is being repriced by global capital.

On April 13, the new energy sector in A-shares strengthened again, with lithium mining concept stocks surging. CATL rose more than 4% intraday, hitting a record high, while the photovoltaic sector gained momentum in the afternoon.$Tongwei Co.,Ltd (600438.SH)$and others hit the upper limit.

Meanwhile, Ningbo Deyi Technology expects its first-quarter profits to grow by up to 70% year-on-year, directly attributed to a surge in overseas energy storage orders. In March, China-manufactured electric vehicles and hybrid models saw their exports double from the previous year, reaching a record 3.49 million units.

Meanwhile, Ningbo Deyi Technology expects its first-quarter profits to grow by up to 70% year-on-year, directly attributed to a surge in overseas energy storage orders. In March, China-manufactured electric vehicles and hybrid models saw their exports double from the previous year, reaching a record 3.49 million units.

Behind all this lies the near-total closure of the Strait of Hormuz, which has triggered the largest energy supply disruption in history. According to the International Energy Agency, the energy supply shock caused by this conflict is unprecedented. Consumers and governments worldwide are shifting to solar, wind, energy storage, and electric vehicles at an unprecedented pace—most of these technologies originate from China. China accounts for approximately four-fifths of global photovoltaic manufacturing capacity and over 70% of global electric vehicle production.

CATL Hits New High as Energy Security Logic Is Repriced

CATL's stock price hitting a new historical high is the most emblematic signal of this market trend.

Since the escalation of the conflict in the Middle East at the end of February, according to Huaxin Securities, the gains of leading battery companies such as CATL$BYD Company Limited (002594.SZ)$have comprehensively surpassed those of international oil giants, highlighting the market’s long-term bet on the energy transition. In its weekly industry tracking report, Dongwu Securities maintained a 'Buy' rating for CATL, listing it as the top recommendation due to its status as a 'global leader in power and energy storage batteries with strong growth prospects and low valuation.'

The revaluation of energy security logic is systematically elevating the strategic premium of the new energy sector. Huaxin Securities believes that 'energy autonomy and controllability' will become a core investment theme spanning several years, with new energy generation, energy storage, and grid equipment representing three directions entering a strategic opportunity window. Amid external energy shocks compounded by carbon neutrality goals, the demand center for relevant sectors is expected to shift upward systematically, significantly increasing their strategic priority.

Lithium Batteries: Rising Oil Prices Open Demand Ceiling

The surge in oil prices is the most direct catalyst driving this round of gains in the lithium battery sector.

Dongwu Securities explicitly pointed out in its weekly tracking report on the power equipment industry that high oil prices will directly benefit lithium battery demand and projected that electric vehicle exports for the year are expected to achieve growth of over 70%. Production scheduling data also confirms an upward trend: after a 20% month-on-month increase in March, April is expected to grow by 5%, and May is projected to increase by approximately 10%, indicating sustained upward momentum.

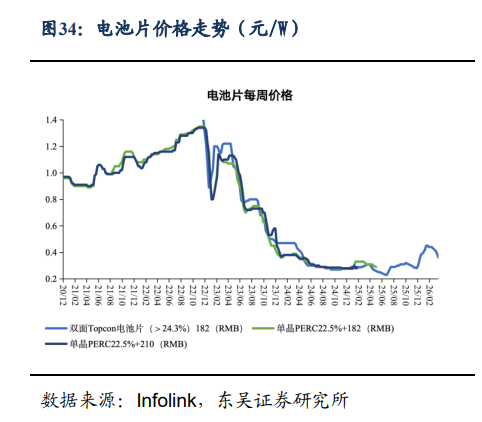

On the price front, the resumption of lithium ore exports from Zimbabwe still requires time. Lithium carbonate prices remain at a high level, and the transmission of battery price increases has been smooth. Spot prices have been adjusted to CNY 0.38 per Wh. Price hikes for small and medium-sized customers in the materials segment have already been implemented, while large customers are expected to gradually follow suit in April. Dongwu Securities noted that profitability inflection points for the battery and separator segments are approaching, with prices of low-price orders beginning to recover.

Energy storage demand remains robust. Ningbo Deyi Technology attributed the substantial profit growth in the first quarter directly to surging demand for battery energy storage from households and businesses in Europe and Southeast Asia. Domestically, the cumulative tendered/awarded capacity for large-scale energy storage in January-March 2026 reached 93.8/83.7 GWh, representing year-on-year growth of 92%/286%. Dongwu Securities forecasts that global energy storage installations will achieve growth of over 60% by 2026.

Wind Power: European Energy Security Drives New Overseas Growth

The Middle East conflict is driving up oil and gas prices, accelerating Europe's policy pace toward reducing dependence on fossil fuels. Offshore wind power is entering an upward cycle driven by three factors: intensified policy support, strengthened energy security, and supply chain restructuring.

Huaxin Securities provided a detailed breakdown of the rapid implementation of European policies in its weekly report on the power equipment sector: Germany plans to restart offshore wind auctions in 2027; the UK has moved the AR8 auction forward to July 2026 and eliminated import tariffs on 33 offshore wind-related products, including blades and cables; the Netherlands intends to launch subsidized offshore wind project tenders in September 2026; France has merged the AO9 and AO10 bidding rounds, planning to award approximately 10 GW of installed capacity. At the EU level, the Hamburg Declaration sets a target of 300 GW of offshore wind power by 2050, and the Clean Energy Investment Strategy plans annual investments of EUR 660 billion from 2026 to 2030.

In terms of the supply chain, Europe’s domestic production capacity remains constrained by high costs and insufficient output. Chinese companies have established significant competitive advantages in key areas such as submarine cables, pipe piles, and towers. Huaxin Securities predicts that over the next two to three years, Europe's offshore wind power industry chain will adopt a division of labor characterized by 'local complete systems + globally sourced components,' with growing demand for equipment imports. The UK’s elimination of import tariffs essentially represents a 'systematic opening' to external supply chains, which will directly lower the cost barriers for Chinese companies entering the European market.

Domestically, Dongwu Securities highlighted that China’s offshore wind power sector is expected to regain high growth momentum in 2026, entering a new upward cycle. It recommends focusing on subsectors such as offshore piles, complete turbines, and submarine cables.

Electric Vehicles: Soaring Oil Prices Accelerate Global Penetration

Surging oil prices are unexpectedly boosting China’s electric vehicle exports.

According to Bloomberg, the export volume of electric vehicles (EVs) and hybrid models manufactured in China more than doubled year-over-year in March, reaching a record high of 349,000 units. Rising oil prices have reignited consumer demand for alternatives to traditional fuel-powered vehicles. The Wall Street Journal reported that China's EV exports in March more than doubled compared to the same period last year, with higher oil prices significantly enhancing the appeal of plug-in models.

$BYD COMPANY (01211.HK)$and$GEELY AUTO (00175.HK)$Automakers such as BYD and Leapmotor are benefiting from this trend. Industry observers have drawn parallels to the oil crisis of the 1970s — when Japan gained global market share amid ongoing turmoil thanks to fuel-efficient models. In February, Chinese brands represented by BYD and Leapmotor increased their overall share in the European passenger vehicle market to 8%, nearly doubling from 4.2% in the same period last year. In the pure electric vehicle segment, the share of Chinese brands rose to 14%.

Data from Soochow Securities shows that sales of EVs in nine major European countries reached 220,000 units in February, up 27% year-over-year and 6% month-over-month. Full-year growth is expected to remain above 30%. In March, BYD sold 300,000 units domestically and 120,000 units overseas, raising its full-year export target to 1.5 million units, reflecting a potential year-over-year growth rate exceeding 40%.

Soochow Securities pointed out that the EV industry is currently expected to grow at a rate of over 30%. A turning point in profitability is approaching. Strong recommendations are made for leading battery manufacturers and structural component suppliers with stable profit structures. Material suppliers with strong profit elasticity are also viewed favorably.

Editor/Rocky