Müller-Glissmann still questions whether this rally can sustain itself without the support of monetary policy. He pointed out that, to maintain this upward momentum in the U.S. stock market, the Federal Reserve would need to shift back to a rate-cutting stance.

The situation in the Middle East has further eased, with Iran announcing that the Strait of Hormuz is now 'completely open' to commercial shipping. Prior to this, U.S. stocks had already experienced a significant rebound. Amid the retreat of geopolitical risks, Goldman Sachs believes that for U.S. equities to sustain this rally, the Federal Reserve needs to pivot back to a rate-cutting stance.

Christian Mueller-Glissmann, head of asset allocation research at Goldman Sachs Group, described the recent strong rebound in U.S. stocks as a 'rapid and intense recovery phase,' noting that part of the rebound was driven by technical factors—including hedge funds that previously sold stocks to reduce risk now being forced to rebuild positions.

Despite the S&P 500 Index appearing to be on track for a third consecutive week of gains exceeding 3%, Mueller-Glissmann still questioned whether this rally could be sustained without monetary policy support. He pointed out that for U.S. equities to maintain this upward momentum, the Federal Reserve would need to pivot back to a rate-cutting stance.

Despite the S&P 500 Index appearing to be on track for a third consecutive week of gains exceeding 3%, Mueller-Glissmann still questioned whether this rally could be sustained without monetary policy support. He pointed out that for U.S. equities to maintain this upward momentum, the Federal Reserve would need to pivot back to a rate-cutting stance.

Mueller-Glissmann said in an interview, 'To sustain this recovery and keep the rally going, I believe we need the Fed to return somewhat to its previous policy stance. We need to see a relief in interest rate pressures.'

He also noted that despite the substantial rise in stock markets, oil prices remain high, and credit markets are lagging behind equities. He attributed part of the equity market's outperformance to higher exposure to technology stocks, which continue to 'deliver solid results.'

The Federal Reserve Faces Policy Dilemma

Although investors have recently chosen to treat Middle East war-related headlines as trading noise and have embraced U.S. stocks, led by technology shares, amid better-than-expected corporate earnings in the latest earnings season, the negative impact of this conflict on U.S. economic growth and inflation cannot be ignored.

Williams, the 'third-in-command' of the Federal Reserve and president of the New York Fed, stated on Thursday that the Middle East conflict has begun to have a material impact on the U.S. economy, manifested by increased upward price pressures and slowing economic momentum. In a speech to banking professionals in his district, he pointed out that this conflict has further heightened uncertainty about the U.S. economic outlook. While he still expects the economy to grow this year and inflation to gradually decline, he acknowledged that the Fed is currently facing dual risks of rising inflation and economic slowdown.

Williams said that if energy supply disruptions can be quickly alleviated, energy prices should fall, and some of the related impacts may partially reverse later this year. However, he warned that if the conflict escalates into a larger-scale supply shock, it could further raise inflation and suppress economic activity by pushing up intermediate input costs and commodity prices—a trend that 'has already started to emerge.'

Mussallem, president of the St. Louis Fed, similarly stated, 'Supply shocks are threatening the Fed's dual mandate on inflation and employment,' and pointed out, 'The current interest rate range may remain appropriate for some time.' He also said, 'The oil price shock may be transmitting to core inflation, meaning that core inflation could remain close to 3% by the end of this year.'

Even Milan, a Federal Reserve governor who has consistently supported larger and more frequent interest rate cuts, has slightly changed his stance recently. On Thursday, Milan stated that his position on interest rate cuts had become more restrained because inflation appears to be more stubborn. He now believes that the rationale for adopting an accommodative monetary policy is less compelling than before. While he originally anticipated four interest rate cuts this year, he now favors three cuts.

Milan noted that the inflation situation has worsened since December of last year, but this was not entirely due to the Middle East conflict. In fact, he had observed this trend in the months leading up to the outbreak of the war. Milan pointed out that the fundamental composition of inflation has become more challenging, with contributions from other sectors starting to increase, making the situation more complex than at the beginning of the year.

Milan currently believes that the Federal Reserve should move towards a neutral interest rate, which is estimated to be as low as 2.5%. He expects the inflation rate to reach the Federal Reserve's 2% target level in about a year. Regarding the labor market, Milan sees no reason why the cooling trend in the labor market would not continue. Therefore, given the weakening labor market, he advocates for interest rate cuts now.

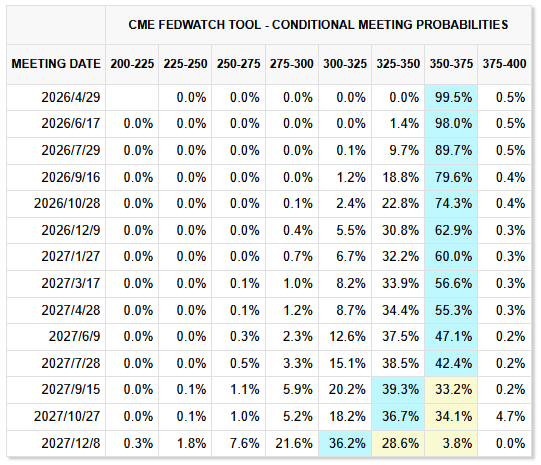

Overall, the dual risks of rising inflation and slowing economic growth brought about by the Middle East conflict are placing the Federal Reserve in a policy dilemma. As of this writing, the CME Group’s 'FedWatch' tool shows that markets expect a 62.9% probability of the Federal Reserve maintaining the benchmark interest rate unchanged through the end of 2026.

At the monetary policy meeting held on March 17-18, the Federal Reserve announced that it would maintain the target range for the federal funds rate between 3.5% and 3.75%, keeping rates unchanged for the second consecutive time. Although projections released after the meeting indicate that most officials still anticipate at least one rate cut this year, the minutes from the March meeting reveal growing concerns.

Many policymakers emphasized that upside risks to inflation may ultimately necessitate rate hikes. The likelihood of inflation remaining above the 2% target for an extended period has significantly increased. The minutes from the March meeting show that the majority of participants judged progress toward the 2% inflation target to be slower than previously expected, with risks of prolonged inflation above the target level having risen.

Meanwhile, most officials are concerned that if the conflict persists over the long term, it could impact the labor market, thereby justifying rate cuts. Many officials cautioned that the current environment, characterized by low net job creation, makes the labor market vulnerable to negative shocks. A protracted conflict in the Middle East could dampen business sentiment and lead to further contraction in hiring.

In fact, even before the outbreak of the Middle East conflict, the Federal Reserve's room for rate cuts had already narrowed – the labor market had stabilized, alleviating fears of a recession, while progress in bringing inflation back to the Federal Reserve's 2% target had stalled.

Considering the information conveyed in the Federal Reserve's meeting minutes alongside current market conditions, the probability of the Fed maintaining interest rates unchanged in the short term is highest, with both immediate rate hikes or cuts being unlikely. Regarding the threshold for a rate hike, although a few officials are open to the idea, most believe it is 'too early' to assess the economic impact of the Middle East situation, preferring to maintain a cautious wait-and-see approach.

Concerning the conditions for rate cuts, the meeting minutes clarified the scenarios that would trigger further reductions: if the prolonged Middle East conflict leads to further deterioration in labor market conditions, faster rate cuts may be warranted. However, stronger-than-expected U.S. nonfarm payroll data for March does not align with this scenario, temporarily easing the urgency for the Federal Reserve to cut rates in the near term.

Some analysts have indicated that the direction of the Federal Reserve's monetary policy will largely depend on external variables beyond its control, namely the duration and intensity of the conflict in the Middle East. Under these circumstances, the Fed’s policy trajectory is likely to exhibit characteristics of 'wait-and-see—awaiting data—making decisions as circumstances warrant.'

The Federal Reserve will announce its interest rate decision on April 29. This decision will be a critical test for the outlook of the Fed's monetary policy. The market widely expects the Fed to maintain the current interest rate at that time. Therefore, any changes in wording in the policy statement and comments from Federal Reserve Chair Powell during the press conference will serve as important indicators for the market to assess the path of the Fed's monetary policy.

If the Transition of the Fed Chair Does Not Go Smoothly, Trump's Wish for Rate Cuts May Be Hard to Fulfill

Meanwhile, the ongoing transition process for the chairmanship of the Federal Reserve has not been proceeding smoothly, which could become a variable influencing the path of the Fed's monetary policy.

The Senate Banking Committee is expected to hold a confirmation hearing next week for Warsh, whom Trump has nominated to serve as the next Federal Reserve Chair. This hearing will provide a platform for bipartisan senators to scrutinize Warsh’s positions on economic and monetary policy. Warsh previously served as a Fed governor and acted as an economic policy advisor to Trump. Investors are particularly focused on how Warsh will strike a balance between two competing forces: pressure from Trump to significantly lower borrowing costs, and economic conditions that do not yet justify rate cuts, at least in the short term.

Given repeated attacks on the Federal Reserve by the Trump administration and inflation having remained above the central bank's target for over five years, any inappropriate responses regarding interest rates could undermine the credibility of the Federal Reserve under Warsh’s leadership.

However, even if Warsh performs impeccably during the committee hearings, uncertainty remains regarding his path to Senate confirmation as long as the Department of Justice continues its investigation into Powell. Senator Tillis, a Republican from North Carolina, has stated that he will not support any nominee until the criminal investigation is resolved, as he believes it poses a threat to the independence of the Federal Reserve.

Trump reiterated this week that he would take action to remove Powell from the Federal Reserve if Powell does not step down on schedule. Although Powell’s term as Fed Chair is set to expire on May 15, his tenure as a member of the Board of Governors extends until January 2028. It is customary for outgoing Fed chairs to resign entirely upon the conclusion of their leadership role; however, Powell stated in March that he intends to remain until the Department of Justice investigation is resolved “in a transparent and conclusive manner.”

Trump stated that he does not intend to drop the Department of Justice investigation into Powell and reiterated the necessity of probing issues related to the Federal Reserve building project. This week’s raid by U.S. prosecutors on the construction site of the Federal Reserve headquarters also indicates that the DOJ has not abandoned its investigation into Powell. Earlier this month, U.S. District Court Judge Boasberg upheld the ruling to dismiss the subpoena against Powell.

If Warsh fails to secure confirmation by May 15, Powell has stated his intention to serve as interim chair and may continue in his other key role as chair of the Federal Open Market Committee (FOMC), which sets interest rates. This means that continued investigations by the Trump administration could not only delay Warsh’s confirmation but also allow Powell to retain significant control over monetary policy.

Corporate Earnings Resilience Is a Key Pillar! Wall Street Strongly Bullish on U.S. Stocks

Despite the Federal Reserve's policy remaining shrouded in uncertainty, recent calls from multiple Wall Street firms for a positive outlook on U.S. stocks, supported by resilient corporate earnings, have sparked market hopes for a new bull market led by technology stocks.

Tom Lee, a seasoned stock market strategist and co-founder of Fundstrat, who is known as the 'Oracle of Wall Street,' believes that the current position of the U.S. stock market—and even the global equity markets—is stronger than when it reached its previous historical peak earlier this year. Tom Lee agrees with a typical assessment by JPMorgan, the Wall Street financial giant, which posits that the technology sector centered on AI computational infrastructure will lead the main theme of the next super bull market phase.

Citi has upgraded its rating on U.S. equities from 'Neutral' to 'Overweight' and forecasts that the S&P 500 index will reach 7,700 points by the end of the year. The bank’s latest research report indicates that the technology sector, previously weighed down by geopolitical conflicts, valuation concerns, and overly optimistic expectations, is now experiencing a shift from restored risk appetite toward fundamental revaluation. Following a marginal easing of tensions in the Middle East, the market swiftly pivoted back to risk assets, with both the S&P 500 and Nasdaq strengthening in tandem, suggesting capital has begun re-trading on the 'future overall earnings growth trajectory driven by AI' rather than 'current panic.' Within this framework, tech stocks—particularly large technology platforms—are no longer merely liquidity-driven safe havens but have become the core anchor of U.S. stock risk appetite and earnings expectations once again.

Blackrock’s equity strategists have shifted back to an 'Overweight' stance on U.S. stocks. Blackrock emphasized the upcoming U.S. earnings season, heralding strong earnings growth as the engine that could sustain the main theme of a bull market. The strategists wrote: 'Even amid geopolitical conflicts, corporate earnings expectations continue to rise, largely due to robust demand for AI-related computational power investments.'

In summary, the narrative of a new bull market in U.S. stocks is fundamentally supported by three key pillars: the resilience of corporate earnings demonstrated in the latest earnings season, the renewed risk appetite driven by technology stocks and AI computational themes, and the market's belief that the Middle East shock will not evolve into prolonged inflation akin to that seen in 2022. As long as these three pillars remain intact and tensions in the Middle East ease, U.S. stocks are likely to continue strengthening.

Editor/Doris