U.S. retail sales recorded the largest increase in a year, showing broad-based growth, with consumer spending expansion not limited to gasoline consumption.

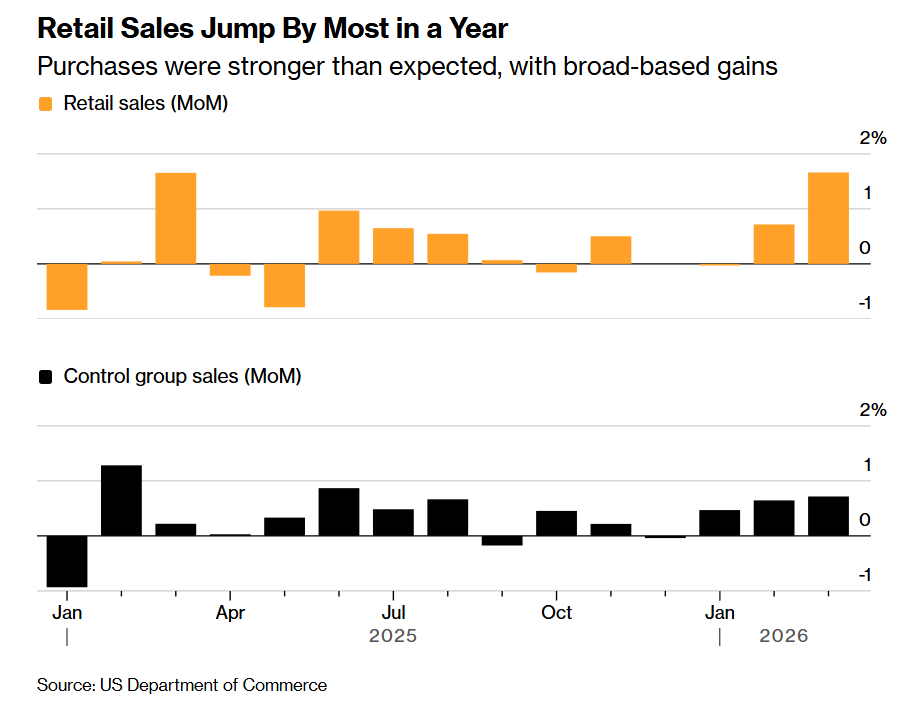

U.S. retail sales in March unexpectedly recorded the largest increase in a year, primarily driven by surging revenues at gas stations amid high oil prices catalyzed by geopolitical tensions in the Middle East, as well as notably stronger consumer spending across other categories than economists had generally anticipated. This highlights that despite gasoline price spikes triggered by the conflict with Iran, consumers continued to exhibit robust spending on various goods. Consumer spending, which accounts for nearly 70% of U.S. GDP, demonstrated significant resilience and ongoing strength. The latest data also showed that the 'control group' retail sales, which directly feed into GDP calculations, rose more than expected on a month-over-month basis, recording the largest increase since August of the previous year.

Thus, following the release of the latest series of retail sales data, interest ratesFutures Tradinghave further weakened market expectations for the Federal Reserve to restart a rate-cutting cycle within the year. The 'CME FedWatch Tool' indicates that the vast majority of traders are betting the Fed will keep rates unchanged for the rest of the year—prior to the release of the retail data, the market was inclined to price in one rate cut.

The retail sales report published by the U.S. Department of Commerce on Tuesday showed that total retail sales in March surged by 1.7% month-over-month—outpacing even the upwardly revised consensus forecast of 1.5%, following a 0.7% growth in February after upward revision. The March retail sales growth was notably stronger than economists’ expectations and the previous month’s figure. This data is not adjusted for inflation.

The retail sales report published by the U.S. Department of Commerce on Tuesday showed that total retail sales in March surged by 1.7% month-over-month—outpacing even the upwardly revised consensus forecast of 1.5%, following a 0.7% growth in February after upward revision. The March retail sales growth was notably stronger than economists’ expectations and the previous month’s figure. This data is not adjusted for inflation.

Detailed data indicates that the March increase was predominantly driven by a 15.5% surge in gas station expenditures, as the Iran war pushed fuel prices to their highest levels since 2022. Excluding gas stations, retail sales increased by 0.6% month-over-month. Overall, the geopolitical conflict in the Middle East—namely, the Iran war—pushed fuel prices to their highest levels since 2022, resulting in a 15.5% spike in gas station consumption during the month, becoming the primary driver of the overall retail sales expansion.

This report suggests that although the spike in gasoline prices was the main force behind the unexpected growth in retail sales, consumer spending remained resilient last month. This strength likely reflects the recent inflow of tax refunds, which have been significantly higher than usual, into more American households’ bank accounts. Some senior economists have begun warning that, with the U.S. tax filing season nearing its end, fuel costs remaining at elevated levels, and hiring continuing to be sluggish, this boost in retail sales may only be temporary.

Almost all of the 13 retail sales categories recorded strong growth, ranging from furniture to electronics to general merchandise. Auto sales grew by 0.5% month-over-month. Restaurant and bar revenue—the sole service category in the report—rose by 0.1% month-over-month after multiple periods of decline.

In contrast to the strong retail sales figures, high-frequency credit card data over recent weeks has shown mixed performance. Analysis reports from PNC Financial Services Group Inc. and Bank of America Institute indicate that discretionary spending categories such as travel services and consumer electronics surprisingly strengthened, while Visa's Consumer Spending Momentum Index showed that—when completely excluding gasoline—spending in discretionary, essential consumption, and dining categories all declined significantly.

High oil prices didn’t first cripple consumption; they shattered the 'preemptive rate cut' fantasy! Control group retail sales unexpectedly strong

Notably, the retail sales report also showed that the so-called control group sales closely watched by economists—which are included in government GDP calculations—unexpectedly rose by 0.7% month-over-month, marking the largest increase since August last year. This indicator excludes food services, auto dealers, building material stores, and gas stations. The Bureau of Economic Analysis will release its initial estimate of Q1 GDP on April 30.

Wall Street financial giant Citigroup views the March retail sales data, particularly the control group retail sales figures, as a critical litmus test for 'Fed rate cut expectations.' According to Citi’s analytical framework, if core consumption weakens significantly after excluding noisy factors like gas stations, it would prove that high oil prices are eroding demand, thereby reopening space for rate cuts.

Citigroup stated that if the Hormuz impact proves to be short-lived, then high oil prices will be difficult to sustain, and inflation spillovers will not form long-term stickiness. Meanwhile, according to Citi's logical framework, the Fed's reverse repo balance is nearing its bottom, financial conditions are marginally tightening, mortgage rates are rising again, and the labor market has not continued to strengthen significantly. All of these indicate that the monetary environment has not eased enough to offset the risks of a future slowdown in growth. However, the unexpectedly strong control group retail sales figures shattered Citi’s rate cut logic framework.

However, the latest data, at least in the short term, does not support Citi's position. U.S. retail sales surged by 1.7% in March, while February’s growth was revised up to 0.7%. More critically, the control group retail sales, which directly factor into GDP calculations, increased by 0.7%, marking the largest rise since August of the previous year. Nominal sales were indeed pushed higher by oil prices—gas station sales jumped and gasoline prices soared amid the war—but even excluding gas stations, retail sales still grew strongly by 0.6%. This indicates that U.S. consumers in March did not show signs of being 'quickly overwhelmed by high oil prices,' as some in the market had anticipated. Tax refunds and resilient demand for certain goods temporarily offset the energy shock. In other words, the key data Citi used to validate its rate-cut logic did not send a sufficiently dovish signal.

The hope for the Federal Reserve to restart rate cuts this year is increasingly slim.

Previously released inflation data showed that the U.S. CPI rose 3.3% year-over-year in March, core CPI increased 2.6% year-over-year, and the overall CPI monthly increase reached 0.9%. Regarding PPI data, final demand rose 0.5% month-over-month and 4.0% year-over-year in March, with final demand energy prices surging 8.5% month-over-month.

Combined with the series of stronger-than-expected retail sales figures, these all mean that the Federal Reserve is facing a typical 'short-term growth remains resilient but inflation is re-emerging' stagflation-like pessimistic combination. In such an environment, the most natural reaction from the Fed is not to cut rates as soon as possible, but to continue waiting for more evidence to confirm whether the oil price shock will spread from energy to broader core prices and inflation expectations. This is also the core logic behind Deutsche Bank’s firm expectation that the Fed will not cut rates throughout 2026. Meanwhile, Goldman Sachs, Bank of America, and Barclays still maintain their forecast of two rate cuts this year but have pushed back the timing of the first cut to September.

Overall, Fed policymakers currently see neither a steady decline in inflation nor a rapid drop in demand, so the most natural policy response is to continue waiting rather than restarting the rate-cut cycle. The combination of economic data from retail sales, CPI, and PPI in March is telling the market that a rate cut around June is becoming increasingly unlikely, and whether one can happen in September or later depends on whether the upward trajectory of prices driven by the oil shock dissipates further and whether employment and core inflation weaken again.

The latest market pricing from the CME FedWatch tool shows that participants in the interest rate futures market no longer factor in any rate cuts this year. Before the recent outbreak of geopolitical conflict in the Middle East, the market had expected the Fed to implement at least two rate cuts this year.

What could truly bring the rate cut expectations envisioned by Citi’s economists back on track is not just a single month’s acceleration in nominal retail sales slowing down, but seeing clear weakening in the control group retail sales, marginal deterioration in employment, and no signs of secondary inflationary pressures from oil prices spreading uncontrollably to more consumer sectors over the next few months. Until then, the Fed appears to be locked in a 'higher-for-longer' hawkish observation mode.

Editor/KOKO