Tesla's total revenue and automotive business income both increased by 16% year-over-year in Q1, citing a rebound in vehicle demand in Europe and North America; energy business revenue declined by 12% after previous growth; service revenue accelerated by 42%, with paid Robotaxi mileage nearly doubling quarter-over-quarter; gross margin rose to 21% instead of falling, hitting a three-year high; capital expenditure was 40% lower than expected, and a $20 billion equity investment was made in SpaceX.

Tesla stated that its collaboration with SpaceX aims to build the largest chip factory; Cortex 2 has been launched, and development of the Dojo 3 custom chip is progressing; preparations for the Optimus factory will begin in Q2, with the first-generation production line targeting an annual output of 1 million units, and the second-generation line aiming for 10 million units annually.

After the earnings report, Tesla's stock price rose over 4% in after-hours trading but reversed quickly following Elon Musk’s statement about a significant increase in capital expenditures; after the CFO announced capital spending would exceed $25 billion this year, shares turned negative, dropping more than 2%.

$Tesla (TSLA.US)$ The quarterly report significantly outperformed Wall Street expectations, temporarily easing market concerns about slowing sales, pressured margins, and tight cash flow for the electric vehicle giant. However, management’s indication of substantial future investments reignited worries about the impact of rising expenditures.

$Tesla (TSLA.US)$ The quarterly report significantly outperformed Wall Street expectations, temporarily easing market concerns about slowing sales, pressured margins, and tight cash flow for the electric vehicle giant. However, management’s indication of substantial future investments reignited worries about the impact of rising expenditures.

After the U.S. stock market closed on Wednesday, the 22nd Eastern Time, Tesla announced that its revenue for the first quarter of 2026 increased by double digits year-on-year, marking the strongest growth in nearly three years and reversing the decline seen in the fourth quarter. The earnings per share (EPS) for the quarter exceeded the consensus analyst expectations by more than 20%. Contrary to expectations of a decline, the gross margin rose further to its highest level in over three years after returning to above 20% in the fourth quarter of last year. Operating cash flow also showed improvement.Free cash flowAll metrics performed better than the market's previously pessimistic forecasts.

Tesla highlighted in its financial report that one-time gains related to warranties and tariffs contributed to the automotive segment, while higher-margin businesses like services improved. Combined with declining raw material costs and favorable currency effects, these factors collectively boosted profitability. Tesla noted sustained demand growth in the Asia-Pacific and South American markets, alongside a rebound in demand in Europe, the Middle East, Africa, and North America.

Cash flow was the biggest 'surprise' of this earnings report. Wall Street had anticipated Tesla’s free cash flow to turn negative in Q1, but actual cash flow more than doubled year-over-year, with capital expenditure being 40% lower than analysts’ expectations. Although Tesla continues to invest heavily in Cortex computing power, Dojo chips, the Robotaxi autonomous ride-hailing service, the Optimus humanoid robot production line, and vertically integrated projects such as battery materials, at least from the Q1 results, these investments did not weigh on cash flow as reflected in the books.

Following the earnings announcement, Tesla's stock, which had risen only slightly by nearly 0.3% during regular trading hours on Wednesday, surged in after-hours trading, with gains exceeding 4%. Analysts believe the core driver behind the post-market strength was better-than-expected profitability and cash flow, along with narrative reinforcement stemming from advancements in Robotaxi and the Full Self-Driving (FSD) software.

During the earnings call, Tesla CEO Elon Musk stated that the company plans to 'significantly increase' investments, predicting a notable rise in capital expenditures. The new Optimus factory in Texas is expected to commence operations in 2027. Following Musk’s comments about increased capital spending, Tesla shares accelerated their retracement of after-hours gains.

During the conference call, Tesla CFO Vaibhav Taneja stated that the company's capital expenditure this year will exceed $25 billion, surpassing the forecast disclosed during the Q4 earnings release, which was over $20 billion. Tesla shares erased all post-market gains and turned negative, with losses once expanding beyond 2%, currently down nearly 1%.

Analysis suggests that, based on the financial reports themselves, Tesla is using higher gross margins and increased service-based revenue to support investments across multiple fronts, including Robotaxi, AI computing power, chips, robotics, and battery materials. However, in the short term, the stock market is more concerned with the question of when these investments will translate into verifiable profits and cash flow.

Haris Khurshid, Chief Investment Officer of Karobaar Capital, commented on Tesla's after-hours reversal, stating that higher capital expenditures would delay the payback period, to which the market often reacts negatively in the short term. Investors like Tesla’s narrative, but when they realize there is still much work to be done, they continually adjust their strategies.

Revenue slightly exceeded expectations, gross margin increased instead of declining, and expenses continued to rise.

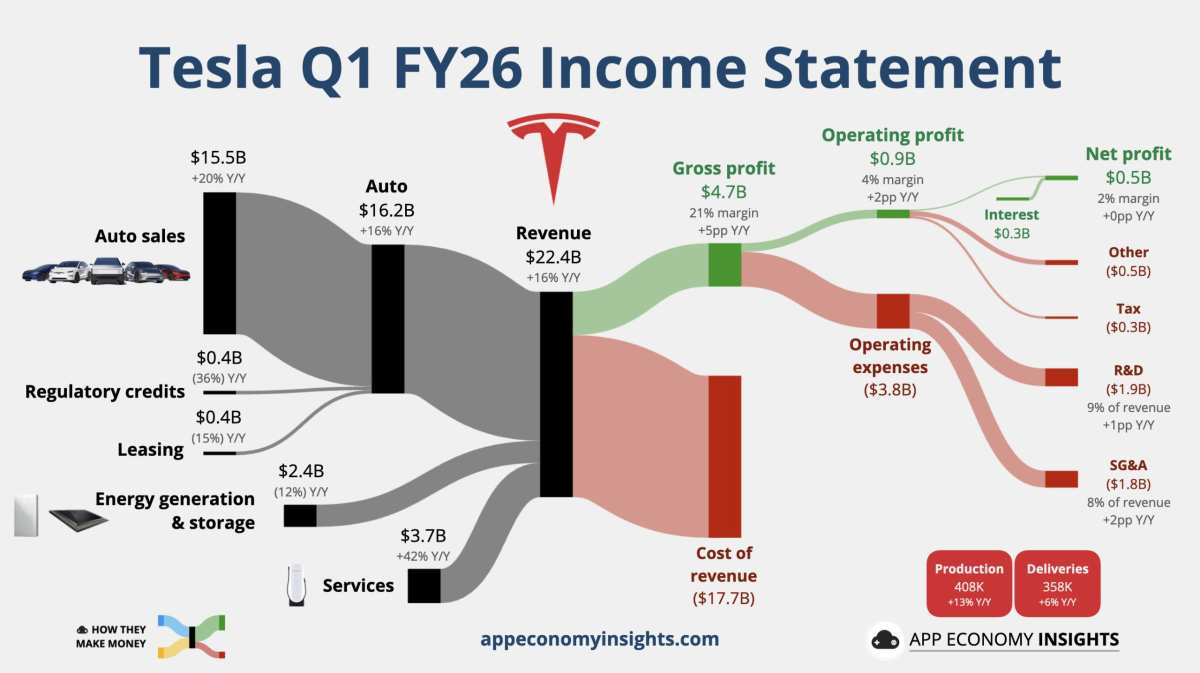

Tesla's total revenue for the first quarter of this year was $22.387 billion, a year-on-year increase of 16%, marking the highest year-on-year growth rate since the second quarter of 2023, while fourth-quarter revenue fell by 3% year-on-year. Adjusted EPS under non-GAAP terms grew by 52% year-on-year to $0.41 in the first quarter, surpassing analyst expectations of $0.34 by 20.6%, whereas fourth-quarter EPS fell by 17% year-on-year.

By business segment:

Automotive business revenue reached $16.234 billion, a year-on-year increase of 16%, remaining the core contributor, while fourth-quarter revenue fell by 10% year-on-year.

Energy generation and storage revenue amounted to $2.408 billion, a year-on-year decrease of 12%, becoming the main drag, while fourth-quarter revenue grew by 25% year-on-year.

Services and other revenue totaled $3.745 billion, a year-on-year increase of 42%, becoming the largest incremental contributor this quarter, while fourth-quarter revenue grew by 18% year-on-year.

The improvement at the gross profit level was even more prominent:

Total gross profit in the first quarter was $4.720 billion, a year-on-year increase of 50%, more than double the growth rate of 20% recorded in the fourth quarter.

Gross margin under GAAP terms in the first quarter rose to 21.1% from 20.1% in the fourth quarter, hitting a new quarterly high since the fourth quarter of 2022. It increased by 478 basis points year-on-year, whereas analysts had projected a gross margin of 17.7% for the quarter, an increase of only about 14 basis points year-on-year and a decline of 24 basis points quarter-on-quarter.

Operating profit in the first quarter was $9.41 billion, with an operating margin of 4.2%, up 214 basis points year-over-year but down from 5.7% in the fourth quarter, mainly due to cost expansion.

In terms of expenses, operating costs in the first quarter were $37.79 billion, a 37% increase year-over-year, including $19.46 billion for R&D and $18.33 billion for sales and administration, both showing significant increases.

Tesla also highlighted in its earnings report that AI and other R&D projects, equity incentives related to CEO compensation (SBC), and selling, general, and administrative expenses (SG&A) were key drivers of cost growth. This indicates that short-term profit improvements need to be assessed alongside medium- and long-term investment intensity.

Automotive business deliveries rebounded year-over-year, but inventory days increased alongside a 'regionalization' strategy.

In terms of operational data, Tesla delivered 358,000 vehicles in the first quarter, a 6% year-over-year increase, with production reaching 408,400 units, up 13% year-over-year. According to Tesla, demand continued to grow in the Asia-Pacific (APAC) and South American markets, while demand rebounded in Europe, the Middle East, Africa (EMEA), and North America.

However, two structural signals should be noted:

Rising inventory pressure: Global vehicle inventory 'supply days' rose to 27 days in the first quarter, up from 22 days in the same period last year and 15 days in the fourth quarter. An increase in inventory days despite higher year-over-year deliveries typically indicates ongoing adjustments in supply-demand matching, with subsequent reliance likely on promotions, financing options, product mix changes, or regional reallocation to clear stock.

Product mix tilting toward an 'autonomous driving future': Tesla emphasized optimizing its model lineup, continuing to advance various global versions of the Model 3/Y, including more affordable variants of both models and the launch of the Model YL outside China, while disclosing that Cybertruck deliveries have begun in the UAE.

Tesla also reiterated that the Cybercab, a dedicated Robotaxi product, and the Semi truck are expected to enter mass production this year, meaning they are currently in trial production/preparation phases. This further suggests that the automotive business narrative is transitioning from 'sales scale' to 'fleet-based, service-oriented' operations.

Energy business revenue declined, but Megapack 3 and capacity expansion remain in progress.

Tesla's energy generation and storage business reported revenue of $2.408 billion in the first quarter, a year-over-year decrease of 12%. Energy storage deployment capacity fell by 15% year-over-year to 8.8 gigawatt-hours (GWh), marking a significant sequential decline of 38% from the record level achieved in the fourth quarter.

In Tesla's operational cadence, the energy segment is more susceptible to fluctuations due to the timing of project confirmations and deliveries, making quarterly volatility not uncommon.

Of greater importance is the mid-term groundwork being laid for production capacity and product iteration.

Tesla disclosed that its new Megafactory near Houston continues to make progress. This facility will produce Megapack 3 energy storage units for the Megablock energy storage system, with production expected to commence later this year.

Meanwhile, Tesla has begun large-scale deployment and delivery to customers of solar panels manufactured at its New York Gigafactory, which were independently designed by the company.

Tesla stated that this new type of solar panel features 18 independent power-generating zones, three times the number of traditional household panels, enabling it to maintain stable and efficient power output even in partially shaded conditions. The product also incorporates innovations in other areas, such as a more aesthetically pleasing design and a simpler, faster installation process.

Commentators noted that this underscores Tesla's emphasis on zonal power generation capabilities and installation efficiency. If energy storage shipments rebound, the energy business still holds potential to contribute to gross margin elasticity.

Services and Software: FSD Subscriptions and Robotaxi Mileage Drive Growth; Non-Vehicle Revenue Accelerates

The most notable structural change this quarter came from service and software-related revenue: Services and Other revenue reached $3.745 billion, surging 42% year-over-year. From an income statement breakdown, the gross profit of the services segment also showed significant improvement, with cost increases lagging behind revenue growth, making it one of the key drivers of overall gross margin expansion in the first quarter.

In terms of operational metrics, Tesla disclosed:

The number of FSD subscriptions reached 1.28 million, representing a year-on-year increase of 51% and a quarter-on-quarter growth of approximately 16%.

The supervised version of FSD (Supervised) received approval in the Netherlands this April, paving the way for further regulatory approvals across more EU countries.

Tesla has begun transitioning FSD (Supervised) to a subscription-only model, aiming to boost recurring revenue and market penetration.

Regarding Robotaxi, Tesla reported that the mileage of paid Robotaxi services nearly doubled in the first quarter. In April, the company expanded its unsupervised Robotaxi service to Dallas and Houston, while continuing to broaden the scope of unsupervised operations in Austin. Additionally, Tesla disclosed that more U.S. cities are in the preparation phase.

For the capital markets, such progress often has a greater impact on valuation than short-term delivery figures. Once Robotaxi transitions from 'limited operations' to 'scalable replication,' Tesla's profit model will shift from 'hardware gross margins' to a compound structure driven by 'fleet + software.'

Q2 Kicks Off Preparations for Optimus Factory with Second-Generation Production Line Targeting Annual Output of 10 Million Units

In terms of robotics, Tesla disclosed that preparations for its first large-scale Optimus factory will officially commence in the second quarter. The first-generation production line, designed for an annual output of 1 million robots, will replace the existing Model S and Model X production lines at the Fremont plant in California.

Additionally, Tesla is preparing a second-generation production line at its Texas Gigafactory, with a design goal of achieving a long-term annual capacity of 10 million robots.

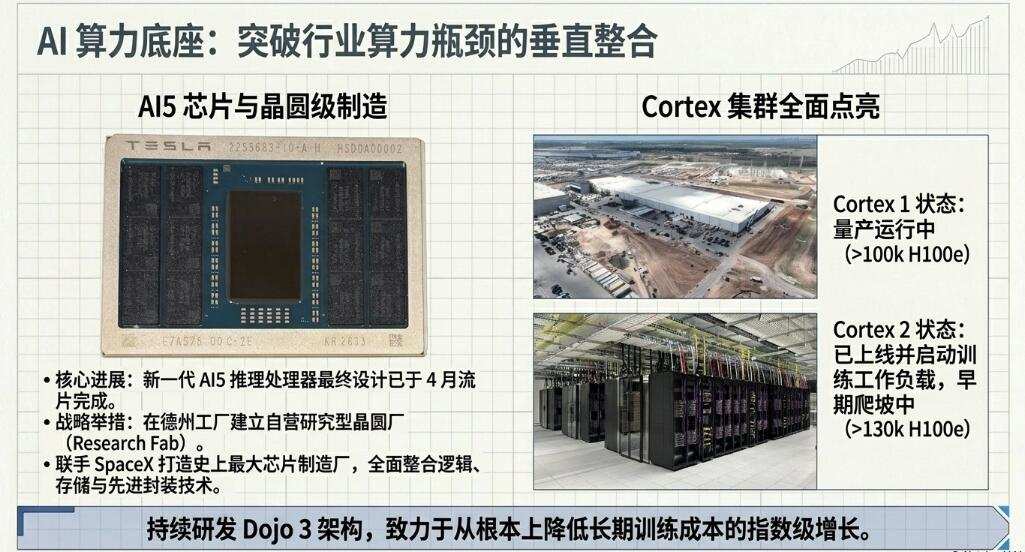

AI and Vertical Integration: Cortex 2 Goes Live, Dojo 3 Advances Amid Coexistence of Self-Developed Chips and Capacity Bottlenecks

In AI infrastructure, Tesla announced that Cortex 2, the second-generation AI training supercomputer cluster located at the Texas Gigafactory, has gone live and started handling training workloads. The company is continuously expanding its on-site training infrastructure to ensure sufficient computing resources for the development of its AI products and services.

Meanwhile, Tesla continues to advance the development of custom chips based on the Dojo 3 supercomputing project, aiming to gradually reduce training costs over time.

More aggressively, Tesla has proposed expanding into semiconductor manufacturing. Tesla stated that its collaboration with SpaceX aims to build the largest chip factory in history, starting with a research-oriented wafer fab within the Texas factory complex. Tesla also announced that it completed the tape-out of its next-generation AI inference processor in April.

On the battery and materials front, Tesla’s LFP cell production line in Nevada has begun ramping up, while cathode material and lithium refining are being advanced in Texas. The company emphasized that 'battery pack production capacity remains a limiting factor for vehicle ramp-up.' Such statements typically imply that short-term deliveries are more determined by supply chain and manufacturing rhythms rather than simply 'whether there are orders.'

Free Cash Flow Far Exceeds Expectations; Lower Capital Expenditure May Reflect Timing Rather Than Intensity Changes

Tesla Q1 Results:

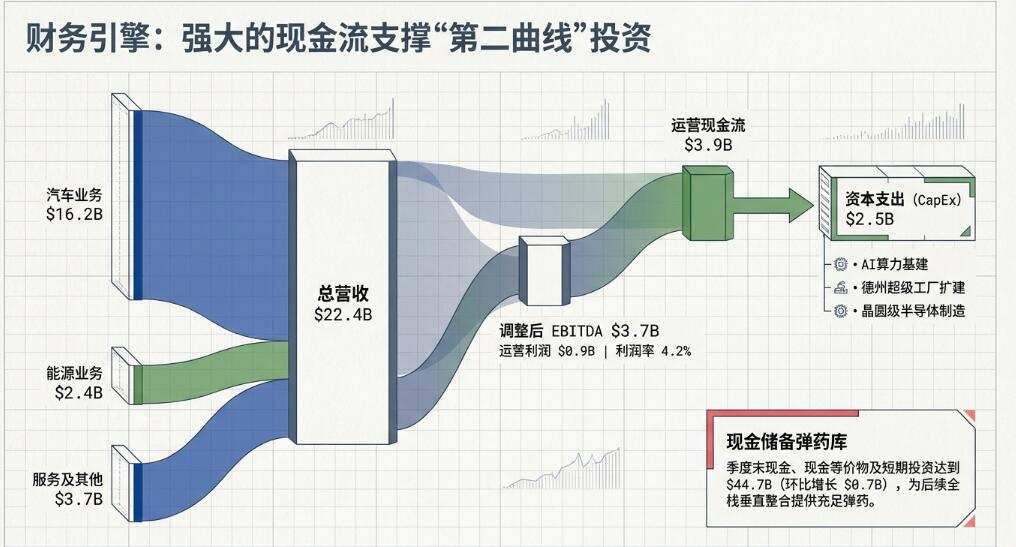

Operating cash flow was $3.937 billion, an 83% year-over-year increase.

Capital expenditure amounted to $2.493 billion, a 67% year-over-year increase, but was approximately 40.4% lower than the analyst consensus of $4.18 billion.

Free cash flow reached $1.444 billion, marking a 117% year-over-year increase. Analysts had expected -$1.86 billion, compared to a 30% year-over-year decline in Q4 to $1.42 billion.

Tesla's lower-than-expected capital expenditure was one of the key reasons for the significant outperformance in Q1 cash flow, but this should not be simplistically interpreted as a reduction in investment.

Tesla repeatedly emphasized in its earnings report that it is advancing multiple multi-year infrastructure projects (computing power, solar energy, battery materials, semiconductor manufacturing, Cybercab/Semi/Megapack 3, Optimus factories, etc.). From this perspective, expenditures appear to fluctuate between quarters, but the overall growth trajectory remains unchanged.

In terms of the balance sheet, Tesla held $44.743 billion in cash and short-term investments at the end of the first quarter, marking an increase of approximately $700 million from the previous quarter. The company disclosed that alongside the increase in cash, it also made a $2.002 billion equity investment in SpaceX, indicating its continued strong liquidity position as well as its willingness to deepen ties within the 'AI ecosystem/alliance chain.'

AI-powered earnings insights in three steps to establish an options strategy! Open Futubull > Stock Page > Click [Company] >Earnings Express

AI-powered earnings insights in three steps to establish an options strategy! Open Futubull > Stock Page > Click [Company] >Earnings Express

Editor/Jayden