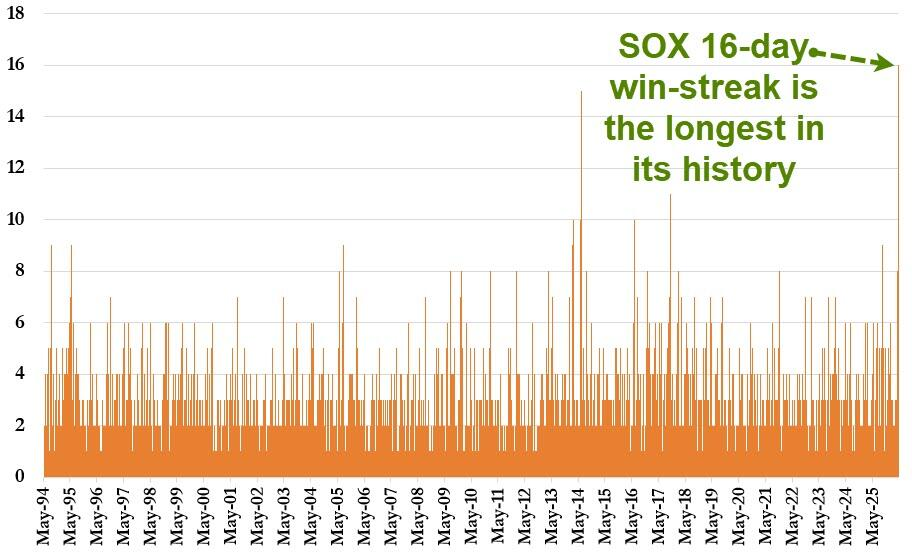

The Nasdaq Composite Index closed up more than 1.6%, reaching a new all-time high along with the S&P 500. The semiconductor sector extended its longest streak of consecutive gains on record, with the Philadelphia Semiconductor Index preliminarily closing up approximately 2.7%, marking its sixteenth consecutive day of gains, the longest such streak since data recording began in 1994. After the market close, Tesla surged 4% and Texas Instruments soared 10% following their earnings reports. The US Dollar Index rebounded for the second consecutive trading day, while Bitcoin rose 4.2%, briefly breaking above $79,000 during the session.

Trump announced on Wednesday an extension of the U.S.-Iran ceasefire agreement by three to five days, combined with robust corporate earnings in the first quarter. The U.S. stock market quickly rebounded from two consecutive days of declines, led by gains in technology stocks. However, a divergence emerged between surging oil prices and market optimism.

Trump announced the extension of the ceasefire at the request of Pakistan's mediation team, stating that U.S.-Iran peace talks might resume as early as Friday. However, Iran later denied the possibility of negotiations taking place on Friday.

The Iranian president expressed 'welcome for dialogue and agreements' but criticized Trump for 'contradictions between words and actions.' Mohammad Baqer Qalibaf, the speaker of Iran’s parliament and chief negotiator, stated that a comprehensive ceasefire cannot be achieved unless the blockade is lifted.

The Iranian president expressed 'welcome for dialogue and agreements' but criticized Trump for 'contradictions between words and actions.' Mohammad Baqer Qalibaf, the speaker of Iran’s parliament and chief negotiator, stated that a comprehensive ceasefire cannot be achieved unless the blockade is lifted.

Crude oil prices surged on Wednesday, marking the third consecutive daily increase this week. WTI crude oil futures rebounded to pre-negotiation breakdown levels, while Brent crude approached $102.

Elon Gu, an analyst at Ultima Markets, stated:

The U.S. stock market indicates that investors have downplayed short-term geopolitical disruptions. Meanwhile, the crude oil market continues to be driven by fundamentals of ongoing supply contraction, providing independent support for oil prices.

All three major U.S. stock indices closed higher on Wednesday, with the S&P 500 hitting a new record high and the Nasdaq Composite reaching an all-time high. Technology stocks spearheaded this rally. The S&P 500 technology sector rose approximately 2%, outperforming the other 11 sectors.

Chip stocks recorded their longest winning streak in history, with the Philadelphia Semiconductor Index preliminarily closing up about 2.7% for the sixteenth consecutive trading day, marking the longest streak since data recording began in 1994.

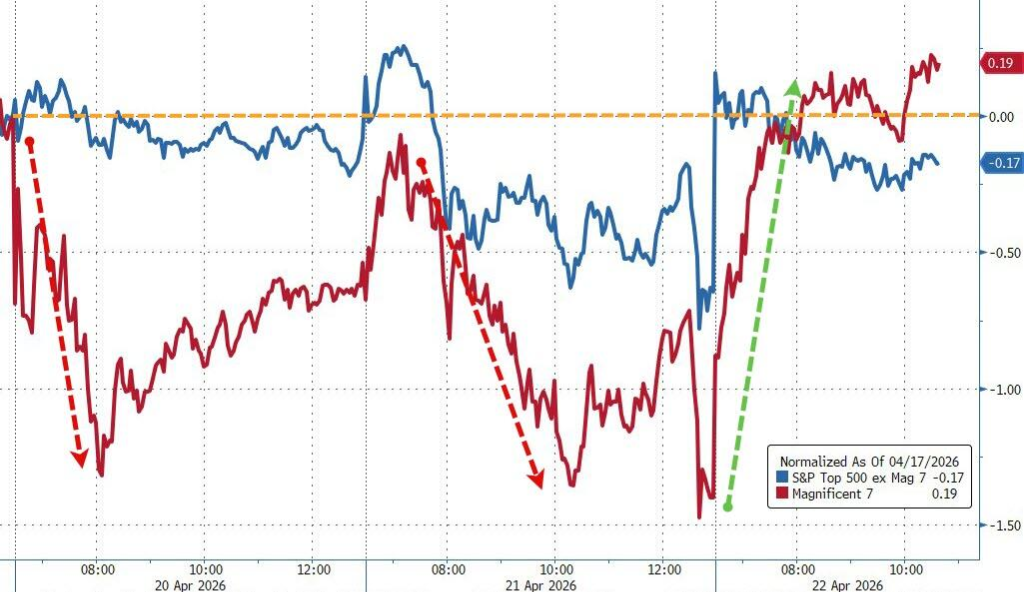

The Mag 7 significantly outperformed the remaining 493 components of the S&P 500 today.

Software stocks continued to rebound, recording gains for the eighth consecutive trading day, rallying nearly 20% from their April lows.

However, Goldman Sachs warned that the uncertainty facing the software sector is unlikely to dissipate in the short term. JPMorgan trader Brian Heavey maintained a cautious assessment:

This is largely still a tactical move. Essentially, no one is truly holding significant positions in the software sector, but investors do not want to maintain short positions ahead of ServiceNow's earnings release. We are transitioning from 'SaaS is dead' to 'perhaps it can coexist with AI.'

The first-quarter earnings season has so far performed strongly, providing important fundamental support for the market.

According to Bloomberg data, approximately 81% of S&P 500 companies that have reported first-quarter results exceeded analyst expectations for earnings per share; LSEG data indicates an overall earnings growth rate of about 14% for the quarter.

Goldman Sachs data shows that since late January this year, the earnings per share forecasts for the S&P 500 in 2026 and 2027 have been revised upward by 4%, respectively.

After-hours, $Tesla (TSLA.US)$ announced better-than-expected first-quarter results, causing its stock price to jump 4% initially before reversing into a decline; $Texas Instruments (TXN.US)$ also issued a stronger-than-expected earnings outlook, surging 10% after-hours.

In the bond market, despite a robust auction for 20-year U.S. Treasury bonds, Treasury yields overall rose alongside oil prices, with the 2-year yield climbing 1.5 basis points and the 30-year yield remaining largely unchanged.

The interest rate futures market currently reflects pricing for only an 8-basis-point rate cut in 2026, signaling that market expectations for monetary policy have turned more hawkish.

The US Dollar Index rebounded for two consecutive trading days, with Bitcoin surging 4.2%, breaking through $79,000 intraday and hitting a new high since February 2.

The Nasdaq Composite closed up over 1.6% on Wednesday, reaching a record closing high alongside the S&P 500, while the Philadelphia Semiconductor Index marked its longest streak of consecutive gains in history. After-hours earnings saw Tesla jump 4% and Texas Instruments soar 10%.

U.S. benchmark indices:

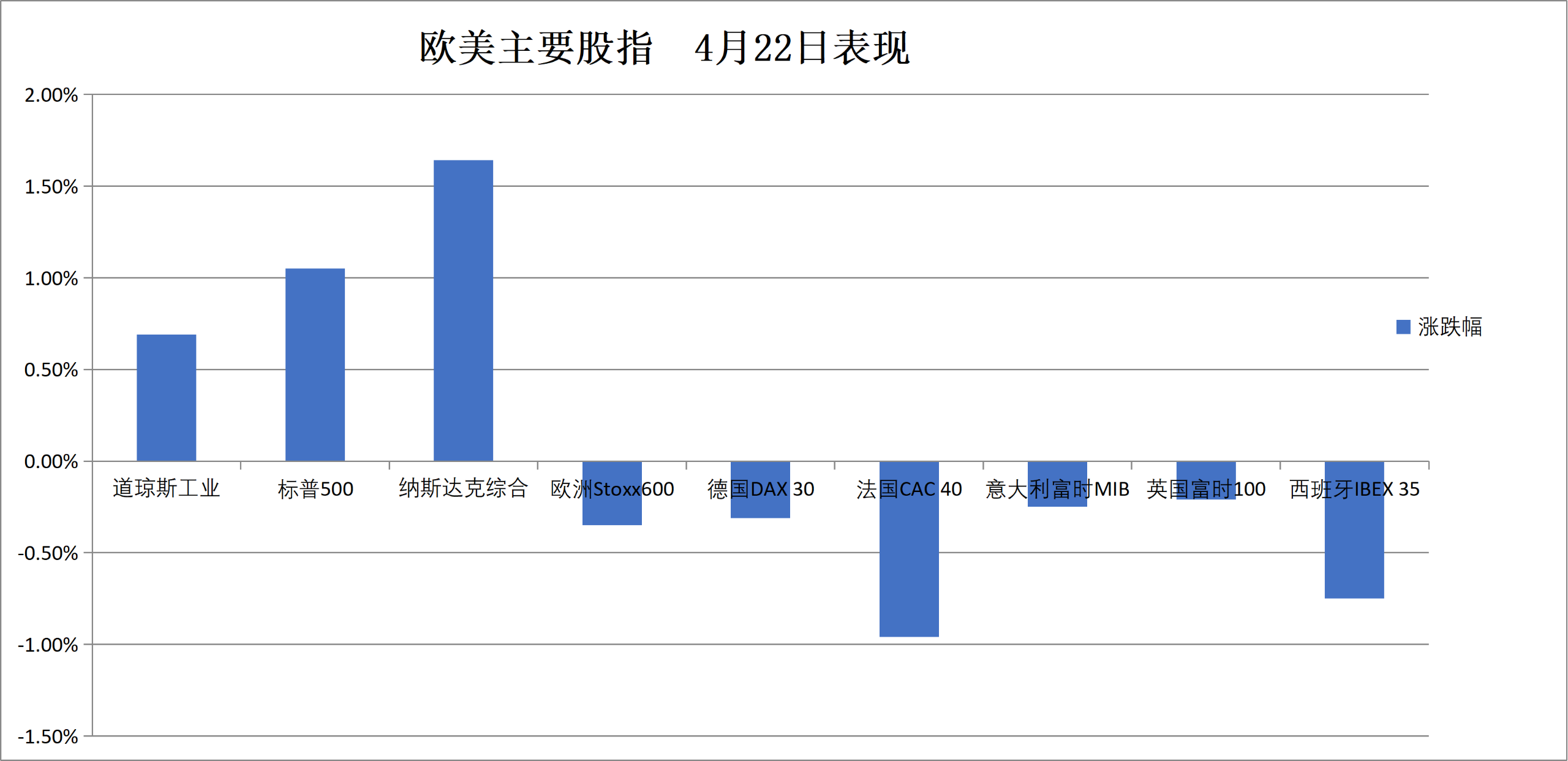

The S&P 500 Index rose 73.89 points, or 1.05%, to close at 7,137.90 points, setting another record closing high after a two-day hiatus.

The Dow Jones Industrial Average gained 340.65 points, or 0.69%, to close at 49,490.03 points.

The Nasdaq Composite surged 397.603 points, or 1.64%, to close at 24,657.567 points, marking another record closing high after a two-day gap. The Nasdaq 100 Index climbed 457.804 points, or 1.73%.

The Russell 2000 Index advanced 0.74% to close at 2,785.377 points, hitting a new record closing high after a one-day pause and nearing its all-time intraday high of 2,817.955 points set on April 21.

The VIX volatility index, also known as the 'fear gauge,' declined 3.03% to close at 18.91.

U.S. sector ETFs:

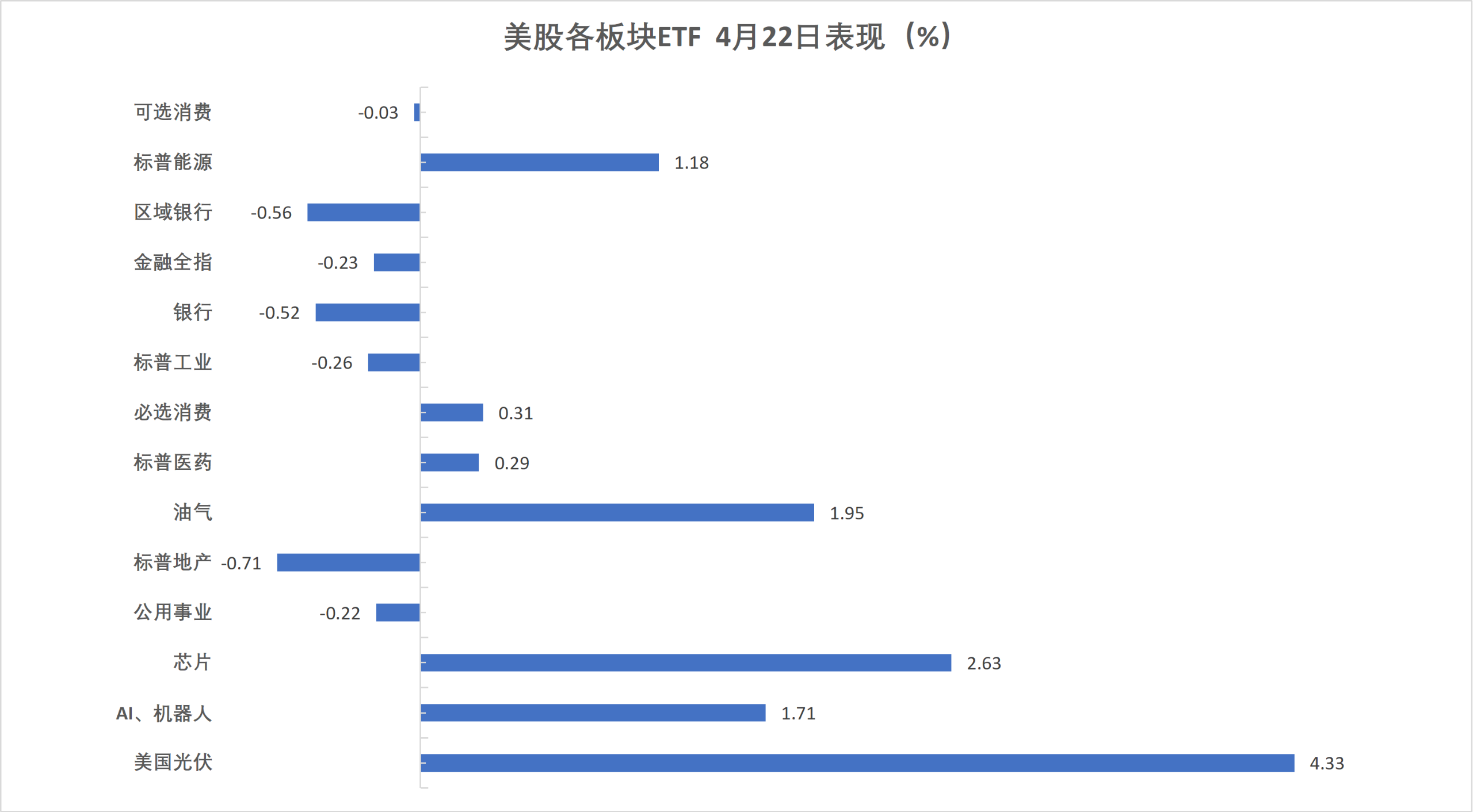

Most U.S. sector ETFs closed higher, with the semiconductor ETF rising 2.62%, global technology stock index ETF and technology sector ETF gaining at least 2.20%, energy sector ETF increasing by 1.20%, banking ETF dropping 0.59%, and global airline industry ETF falling 3.25%.

Mag 7:

The Wind US Magnificent 7 Tech Index rose by 2.04%.

$Apple (AAPL.US)$ Amazon rose by 2.63%, Alphabet A rose by 2.18%, Google A rose by 2.12%, Microsoft rose by 2.07%, NVIDIA rose by 1.31%, Meta rose by 0.88%, and Tesla rose by 0.28%.

Chip Stocks:

The Philadelphia Semiconductor Index closed up 2.72%, marking its 16th consecutive trading day of gains, finishing at 9,909.266 points, the first time in history that it has closed above 9,900 points.

Arm Holdings closed up 11.3%, $SanDisk (SNDK.US)$ Advanced Micro Devices rose by 8.5%, $Micron Technology (MU.US)$ Micron Technology rose by 8.4%, $Advanced Micro Devices (AMD.US)$ Texas Instruments rose by 6.9%.

Chinese Concept Stocks:

The Nasdaq Golden Dragon China Index closed nearly flat.

Among popular Chinese stocks, Daqo New Energy closed up 16.5%, JinkoSolar rose by 11.2%, Canadian Solar rose by 8.8%, Atour rose by 5%, Kingsoft Cloud fell by 2.1%, and New Oriental Education fell by 3.1%.

Other individual stocks:

$Circle (CRCL.US)$ ServiceNow rose by 8.7%.

The French stock index closed down more than 0.9%, the Italian banking sector fell approximately 1.3%, and the Norwegian stock market rose over 0.2%.

Pan-European Index:

The European STOXX 600 Index closed down 0.35% at 613.88 points, continuing its overall downward trend.

The Eurozone STOXX 50 Index closed down 0.41% at 5906.22 points.

Major Stock Indexes Around the World:

The German DAX 30 Index closed down 0.31% at 24194.90 points.

The French CAC 40 Index closed down 0.96% at 8156.43 points.

The UK FTSE 100 Index closed down 0.21% at 10476.46 points.

Sector and Stock Performance:

Among the Eurozone blue-chip stocks, Deutsche Telekom closed down 4.76%, Safran fell 3.51%, EssilorLuxottica EL dropped 2.52%, and Airbus fell 2.51%, ranking as the fourth-largest decline.

Among all the components of the European STOXX 600 Index, Bureau Veritas closed down 10.59%, European Top Tech Company fell 9.69%, and Frontline dropped 8.29%, ranking as the third-largest decline.

The 10-year U.S. Treasury yield reversed its course, falling to 4.2619% at 20:22 Beijing time to hit a fresh intraday low before rebounding to turn positive. The German two-year government bond yield rose by more than 3 basis points.

U.S. Treasuries:

In late New York trading, the 10-year U.S. Treasury yield was unchanged at 4.2916%.

The two-year U.S. Treasury yield increased by 1.25 basis points to 3.7916%, while the 30-year U.S. Treasury yield rose by 0.20 basis points to 4.9020%.

European debt:

At the close of European trading, the 10-year German government bond yield climbed by 0.5 basis points to 3.008%, trading within a range of 2.986%-3.016% during the day.

The 10-year U.K. government bond yield rose by 2.5 basis points to 4.909%. The two-year U.K. government bond yield increased by 6.4 basis points to 4.335%.

The 10-year French government bond yield edged up by 0.2 basis points. The 10-year Greek government bond yield rose by 1.2 basis points.

Abu Dhabi Murban crude oil futures in the Middle East surged by 4.88% to $100.99 per barrel.

Crude Oil:

WTI crude oil futures for May delivery closed up $3.29, or 3.67%, at $92.96 per barrel.

Brent crude oil futures for June delivery settled up $3.43, or 3.48%, at $101.91 per barrel.

Abu Dhabi Murban crude oil futures in the Middle East surged by 4.88% to $100.99 per barrel.

Natural Gas:

The May natural gas futures contract on NYMEX closed at $2.7220 per million British thermal units.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/Stephen