Authors: McKinsey & QED Investors

Compiled by: Yuliya, PANews

Editor's Note: Over the past few years, success in fintech was largely about storytelling and customer acquisition through heavy spending, which attracted significant investment. However, times have changed.

According to the latest report by McKinsey and QED, the fintech industry has moved past its phase of unbridled growth and officially entered the 'fifth era,' characterized by competition on profitability and compliance. Although fintech currently accounts for only 4% of the global financial market (generating $650 billion annually), its revenue growth rate is 3.5 times that of traditional banks. In the coming years, this sector will remain a fertile ground for nurturing giants with valuations exceeding $100 billion.

According to the latest report by McKinsey and QED, the fintech industry has moved past its phase of unbridled growth and officially entered the 'fifth era,' characterized by competition on profitability and compliance. Although fintech currently accounts for only 4% of the global financial market (generating $650 billion annually), its revenue growth rate is 3.5 times that of traditional banks. In the coming years, this sector will remain a fertile ground for nurturing giants with valuations exceeding $100 billion.

(This report was jointly written by Jon Steitz, Max Flötotto, Uzayr Jeenah, Vikram Iyer, and Edward Allanson from McKinsey's Financial Services Practice, along with Nigel Morris, Nick Gasbarro, Amias Gerety, and Adams Conrad from QED Investors.)

Key Data Highlights

Market Size and Forecast: Fintech total revenue is expected to reach $650 billion by 2025 (accounting for 4% of total financial services revenue). If recent growth rates persist, the market size is projected to hit $2 trillion by 2030 (with a share of 9%).

Since 2023, capital invested annually in fintech has increased by more than 40%.

Top Valuations: Five companies are now valued near 'decacorn' status ($100 billion).

Over 50% of fintech acquisitions are initiated by fintech companies rather than traditional institutions or sponsors.

Digital Assets: The total value of stablecoin transactions is projected to reach $35 trillion by 2025, but only 1% ($390 billion) is associated with 'real payments.'

In 2025, the United States received 21 applications for banking licenses, surpassing the total number of the previous four years.

Business model evolution: 13% of fintech revenue comes from 'horizontal' software companies that empower traditional institutions, helping them achieve digital transformation from within to outwards. These companies are growing 25% faster than direct competitors.

I. Industry Status: High Growth with Regional and Sectoral Differentiation

In 2025, the global fintech market generated approximately USD 650 billion in revenue, representing a year-on-year increase of about 21% compared to 2024 (with an average annual growth rate of 23% over the past four years). This growth significantly outpaced the traditional financial services industry, which is valued at USD 15 trillion and grows at an average annual rate of 6%. Nevertheless, fintech companies account for only about 4% of total financial services revenue, indicating substantial room for market expansion.

Regional differentiation, with Latin America experiencing the fastest growth

North America: The largest market, generating USD 310 billion in revenue. Operations are extending deeper into capital markets (accounting for 21%) and insurance (accounting for 15%).

Latin America: The fastest-growing region, with revenue reaching USD 60 billion (penetration rate of 8%). Over the past five years, the average annual growth rate was 40%, and loan operations have surged by an average of 50% annually since 2021. The market is highly concentrated, with the top three giants (Mercado Pago, Nubank, PagBank) accounting for 48% of the region's total revenue.

Asia-Pacific: Revenue reached USD 1.5 trillion (penetration rate of 3%). Due to regulatory impacts, the growth rate slowed from 23% to 15%. The revenue focus has shifted, decreasing in loans (to 29%) and increasing in payments (to 40%).

Europe: Revenue amounted to USD 1.1 trillion (penetration rate of 2.6%). The market is the most fragmented, with the top three companies (Adyen, Klarna, Revolut) accounting for less than 20%.

Vertical sector differentiation

Payments: The largest vertical, generating $250 billion in revenue (18% year-over-year growth from 2024 to 2025, with a penetration rate of 19%). Companies like PayPal and Stripe are capturing the fastest-growing global transaction flows, spanning digital, embedded, cross-border, and platform-based commerce payments.

Lending: Total revenue of approximately $120 billion (19% year-over-year growth), concentrated in underbanked markets such as Latin America, Asia-Pacific, and Africa. Global players like Nubank and WeBank are scaling by embedding credit into digital platforms. This sector has the lowest concentration, with the top three companies accounting for only 16% of total revenue.

Insurance and capital markets: Each contributing around $80 billion, experiencing rapid growth but from a low base. Insurtech is growing the fastest (up 37% since 2021), but overall penetration remains below 1%.

Customer Structure and Sub-Sectors: B2C accounts for 47%, and B2B accounts for 41%. In the wealth technology sub-sector, the leading effect is significant, with the three major cryptocurrency platforms$Bakkt (BKKT.US)$, Binance, and $Coinbase (COIN.US)$ collectively accounting for approximately 30% of the total revenue in this sector.

Capital markets: Presenting a 'barbell-shaped' investment profile.

IPO Recovery: In 2025, there were 31 new listings, raising nearly $14 billion (four times that of 2024), accounting for 12% of the total market value of the world's top 100 IPOs. Notable cases include: Klarna (raised $1.3 billion/valued at $11 billion), $Circle (CRCL.US)$ (raised $1 billion/valued at $20 billion), Chime (raised $800 million/valued at $11 billion). The total market capitalization of listed fintech companies reached a record high of $850 billion (across 202 companies).

Polarized investments: Capital is concentrated at both ends. Late-stage scaling deals grew by 22% annually, while early-stage venture capital accounted for 37%; the share of mid-stage growth equity capital plummeted from 45% in 2019 to 25%.

Giant expansion: Companies like Revolut, Robinhood, and Stripe are approaching valuations of $100 billion, with Stripe making a strong entry into the digital asset space through acquisitions of Bridge and Privy.

Customer trust surpasses traditional finance.

McKinsey’s 2025 Retail Banking Survey reveals that customers, for the first time, trust fintech companies more than traditional banks. Customers generally perceive fintech firms as more innovative, transparent in fees, and offering better overall value. Overall, fintech companies achieve a Net Promoter Score (NPSSM) 2.5 times higher than their traditional counterparts (often exceeding 50 or even 70 points).

II. Four Core Trends Shaping the Future

Trend 1: AI is Driving Fintech Transformation

AI is reshaping industry economics in four significant ways: commoditization (product development cycles shortened from years to weeks), democratization (e.g., April Tax Solutions embedding tax logic, Midas providing affordable wealth advice), unbundling, and disintermediation.

Counter-Moves by Giants: Notably, companies such as Coinbase, Nubank, Revolut, and $Robinhood (HOOD.US)$ are leveraging AI to move in the opposite direction (by aggregating products and leveraging scale advantages to become intermediaries for horizontal fintech firms).

Predictions for Winners:

Pioneering traditional institutions: Traditional institutions that adopt AI early both internally and client-facing could see their tangible equity return on equity (ROE) increase by up to four percentage points.

“AI Second” disruptors: Companies with deep domain expertise, proprietary data, or distribution channels will gain a significant advantage by accelerating product development through AI.

Current applications: Fintech companies are boldly deploying AI customer service agents like Decagon, Lorikeet, and Sierra. Traditional institutions that act slowly and scaled enterprises relying solely on outdated technological moats face the risk of obsolescence.

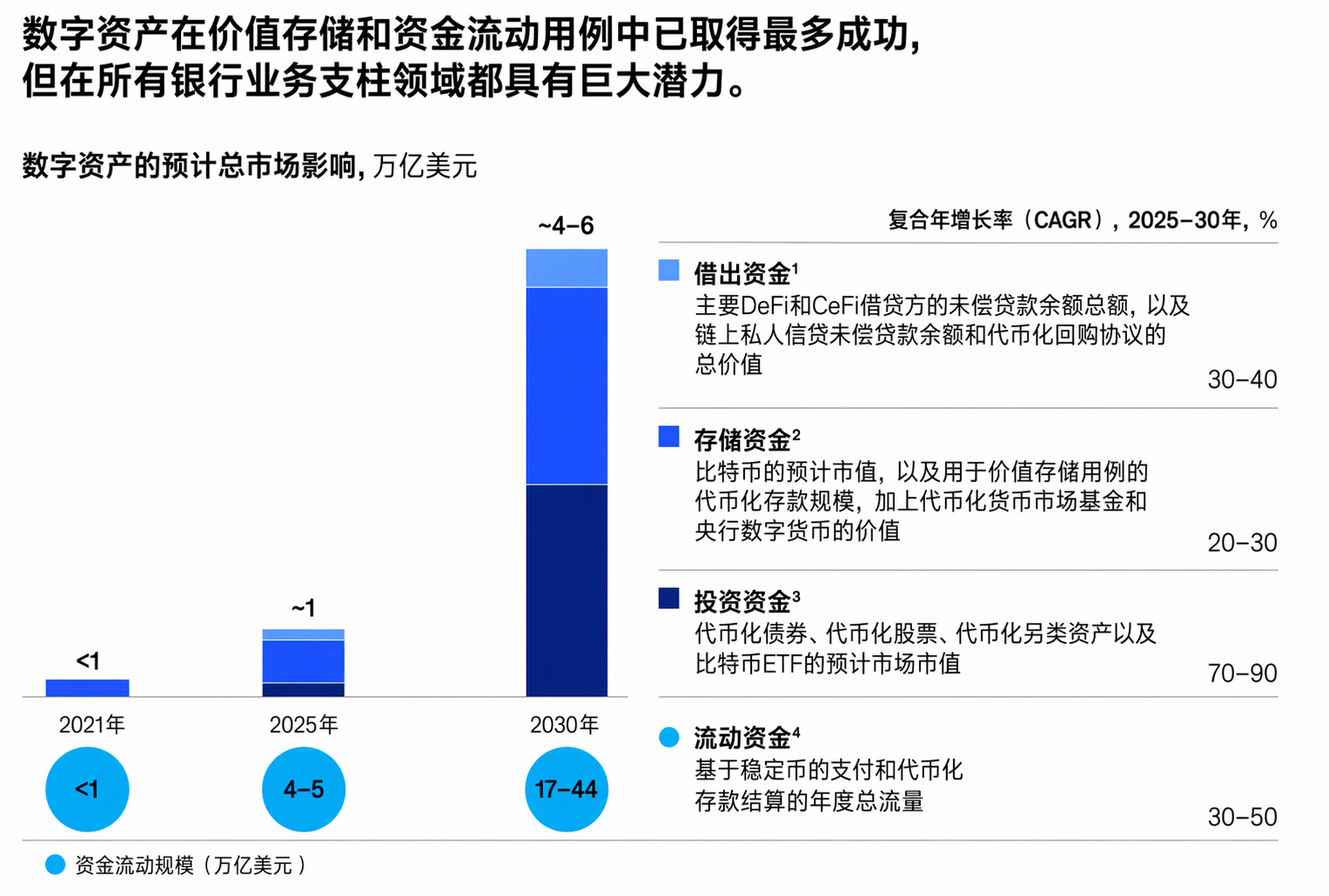

Trend 2: The Rising Tide of Digital Assets

After a decade of experimentation, digital assets have shed their speculative image and become investable infrastructure for traditional financial institutions. The irrational exuberance of 2020–2022 has ended, with market focus shifting to stablecoins and tokenized deposits, which are reshaping how funds are transferred, stored, lent, and invested. High double-digit growth is projected across all sectors by 2030.

Bitcoin: Considered an alternative to fiat currency and gold. As of the first quarter of 2026, over 60% of $Bitcoin (BTC.CC)$ has been held in wallets for more than one year, with its penetration rate accounting for approximately 3% of the globally investable gold value.

Stablecoins: The current total issuance stands at $300 billion, with a circulation value of $40 trillion, and the market capitalization is expected to reach between $2 trillion and $4 trillion by 2030 (with an annual compound growth of 40%). Despite an annual total transaction volume of $35 trillion, only 1% ($390 billion) represents real end-user payments, with the remainder largely attributed to trading and arbitrage. Real-world application scenarios include: global remittances ($90 billion, accounting for less than 1% of the global $100 trillion), B2B payments ($226 billion), and capital market settlements ($80 billion, representing 0.01% of the global $200 trillion). Additionally, emerging markets seeking to mitigate local currency volatility (such as Argentina, Nigeria, etc.) have also generated significant demand.

Tokenized deposits: Effectively address the 'cash leg' bottleneck in institutional settlements. JPMorgan's JPMD and Kinexys (processing $2-3 billion daily), as well as Citi Token Services (projected to support $100-140 trillion in traffic by 2030), are leading this trend.

Tokenization of RWA (Real-World Assets): Expected to reach a scale of $2 trillion by 2030.$Bank of New York Mellon (BK.US)$、 $Goldman Sachs (GS.US)$ is integrating digital asset custody into its core platform.

Ecosystem Convergence: Klarna, $PayPal (PYPL.US)$ has developed various payment stablecoins; Stripe (Bridge) is rolling out stablecoin cards in over 100 countries;$Visa (V.US)$、$MasterCard (MA.US)$direct settlement $USDCoin (USDC.CC)$ ; AI agents have even begun utilizing micropayments based on stablecoins to autonomously procure computing resources, heralding the advent of a programmable money-driven era of machine commerce.

Trend Three: The Race for Licenses (Embracing Compliance Moats)

Fintech companies are no longer seeking regulatory arbitrage but are proactively applying for banking licenses, leveraging them as strategic tools to unlock low-cost funding, expand product portfolios, enhance customer trust, and solidify their moats.

Data: In 2025, there were 21 new charter applications in the United States, with approval times shortened by 40% (Paycom took 421 days, while Erebor Bank required only 125 days).

Participants: Include Nubank, Circle (First National Digital Currency Bank), Stripe (Bridge), Fidelity, PayPal, Monzo, Zilch (acquired AB Fjord Bank), Revolut, Flutterwave, KakaoBank, Airwallex, and others.

Potential risks: Licensed entities will face direct regulatory pressures, and their valuation logic may undergo a reset—from high-premium tech multiples to traditional bank price-to-book ratios.

Trend Four: The Rise of 'To B' FinTech

Horizontal FinTech companies (enablers that do not directly serve end consumers but provide digital software/infrastructure to traditional institutions) are attracting a disproportionate share of investment. Notable examples include Omilia (AI solutions), Vitesse (claims digitization), and Alloy/Footprint (compliance automation).

Data: This model already accounts for 13% of the industry’s total revenue. In the UK InsurTech sector, the proportion of funding captured by horizontal enterprises surged from 25% in 2021 to 91% in 2024.

Section Three: New Secrets to Success and Institutional Response Strategies

Four Characteristics Shaping Future Winners

Economics: Moving away from 'blind growth,' it is essential to balance high growth with reliable unit economics. Raman Bhatia of Starling Bank pointed out, 'Technological barriers are declining, but business model barriers are rising.'

Distribution and Trust: In an era where AI makes products easily replicable, owning customer relationships and long-term accumulated trust becomes the ultimate moat.

Product Quality: Substantial improvements must be achieved in economics, speed, and risk, rather than merely focusing on UI enhancements. Justin Basini of ClearScore emphasized that competitive advantages increasingly depend on fundamental product strengths.

Risk and Resilience: Compliance capabilities have become a core differentiator. Dima Kats of Clear Junction believes, 'The best investment a FinTech company can currently make may well be in compliance.'

Response Strategies for Traditional Institutions

Investment/M&A: Building defenses through capital. JPMorgan's technology investment for 2025 is nearly 18 billion US dollars; Visa has invested in/acquired over 50 companies in the past five years and established partnerships with approximately 90 companies.

Reinventing oneself: Leveraging innovations in AI and horizontal fintech to rapidly modernize core legacy systems.

IV. Forecast: Six major growth drivers for the next wave.

Digital Asset Infrastructure and Networks: With the implementation of regulations such as the Zhi Xin Electronics Act, wallets, on-ramps/off-ramps, compliance tools, and programmable settlement will form the foundational layer.

Agent AI focused on financial services: Targeting pools of contact center, operational, and compliance costs worth hundreds of billions of dollars, providing automated ROI.

Data infrastructure: Leveraging open banking, real-time payments, and alternative data (such as payroll and rent) to reshape credit and risk decision-making.

AI-driven wealth advisory: Serving the mass affluent segment with assets between USD 100,000 and USD 1 million (e.g., Robinhood’s cross-sector positioning), unlocking the largest underserved market.

Horizontal insurtech: Using AI to unlock unstructured data (such as claims notes and satellite imagery) for personalized real-time risk pricing.

Identity and trust infrastructure: Building a universal, portable KYC/KYB/AML compliance layer to address one of the industry’s most expensive redundancies.

*Risk warning: Enterprises relying solely on technological barriers from the past 5-10 years and deposit-based fintech firms dependent on interest rate spreads will face significant survival pressures amid the widespread adoption of AI and heightened competition from high-interest rates.

Editor/Joe