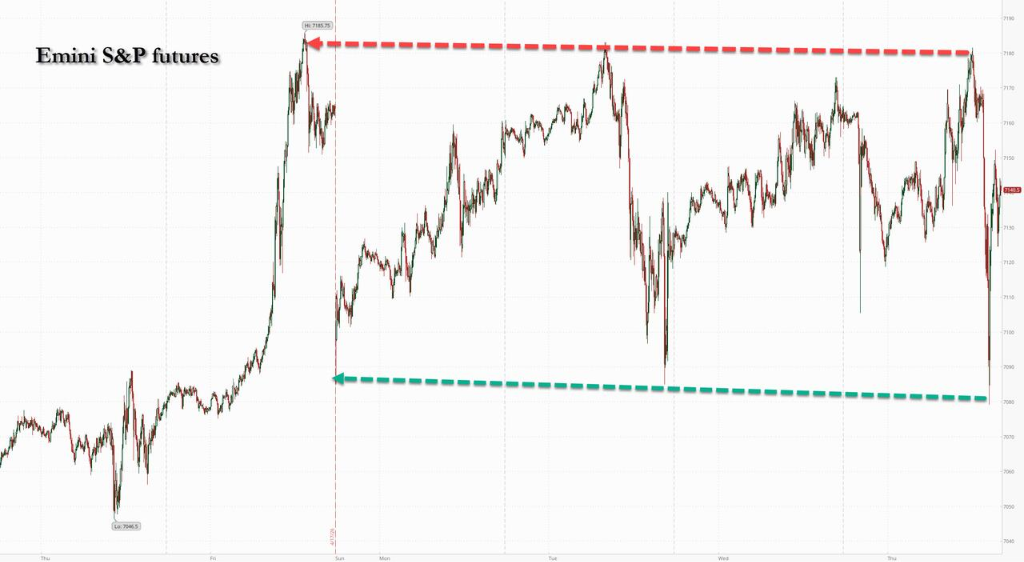

On Thursday, the three major U.S. stock indexes closed lower, while the semiconductor index rose for the seventeenth consecutive trading day. Salesforce closed down 8.8%, leading the decline among Dow components alongside IBM, American Express, Microsoft, and Honeywell. Caterpillar, however, rose 3.2%. The yield on the 10-year Treasury note increased by 2 basis points, while the 2-year yield rose 4.4 basis points to 3.834%. Brent crude oil broke through $105, and WTI crude oil surged 3.7%, reaching a two-week high.

The escalation of tensions in Iran drove oil prices to surge temporarily, while U.S. stocks ended lower amid volatility. Software stocks suffered heavy losses, but the semiconductor sector bucked the trend, setting a historic record of 17 consecutive days of gains for the Philadelphia Semiconductor Index.

The situation in the Strait of Hormuz continued to be the market's focal point:

Before the U.S. stock market opened, Trump ordered the U.S. Navy to take sinking actions against any vessels attempting to lay mines in the strait. The U.S. military also reported intercepting two supertankers trying to evade the blockade.

During the mid-session of the U.S. stock market, Xinhua News Agency cited Iranian media reports stating that explosions were heard over Tehran, the capital of Iran, on the evening of the 23rd local time. The air defense system was activated, firing at 'hostile targets.' Iranian Islamic Parliament Speaker Karibaf withdrew from the negotiation delegation.

A series of Iran-related headlines emerged intensively, causing market sentiment to tighten abruptly. The three major U.S. equity indexes accelerated their declines, with the Nasdaq falling more than 1% during the session. International crude oil futures expanded their gains, hitting fresh intraday highs, with both WTI and Brent crude rising over 5% at one point.

During the U.S. stock trading session, subsequent clarifications indicated that the earlier reports were either misinterpretations or part of system tests. U.S. stocks subsequently recovered most of their losses but still closed lower. Brent crude broke through $105, while WTI crude settled at $96.42, up 3.7%, marking its highest level in nearly two weeks.

Forex.com analyst Fawad Razaqzada stated:

There is considerable uncertainty in the diplomatic relations between the two countries, and there is no clarity on when the Strait of Hormuz will reopen, which continues to weigh on the market.

Infrastructure Capital Advisors CEO Jay Hatfield also noted:

We are toggling between earnings season and war-related headlines. Recent gains have been quite significant, and many investors are using geopolitical risks as a reason to reduce positions.

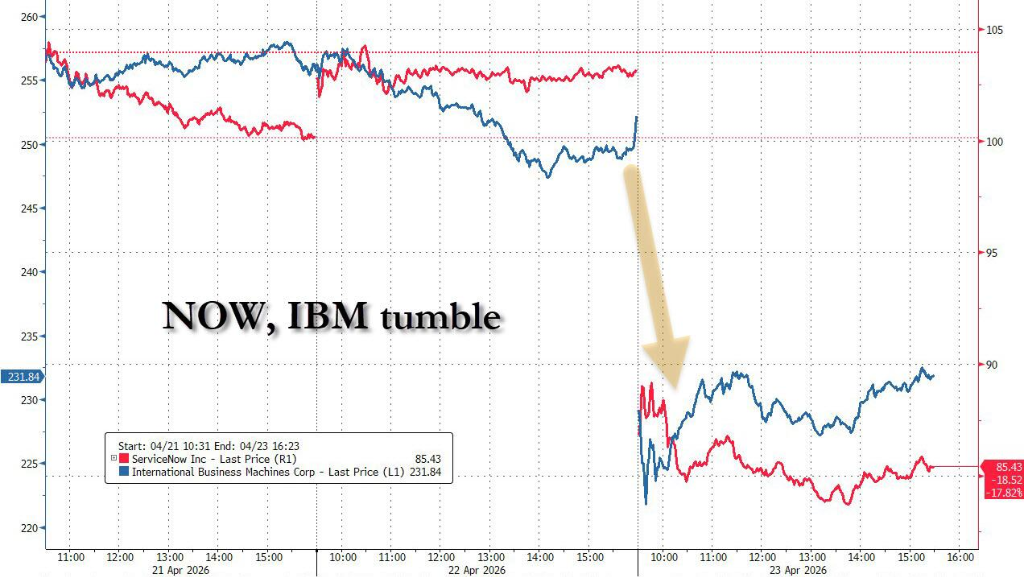

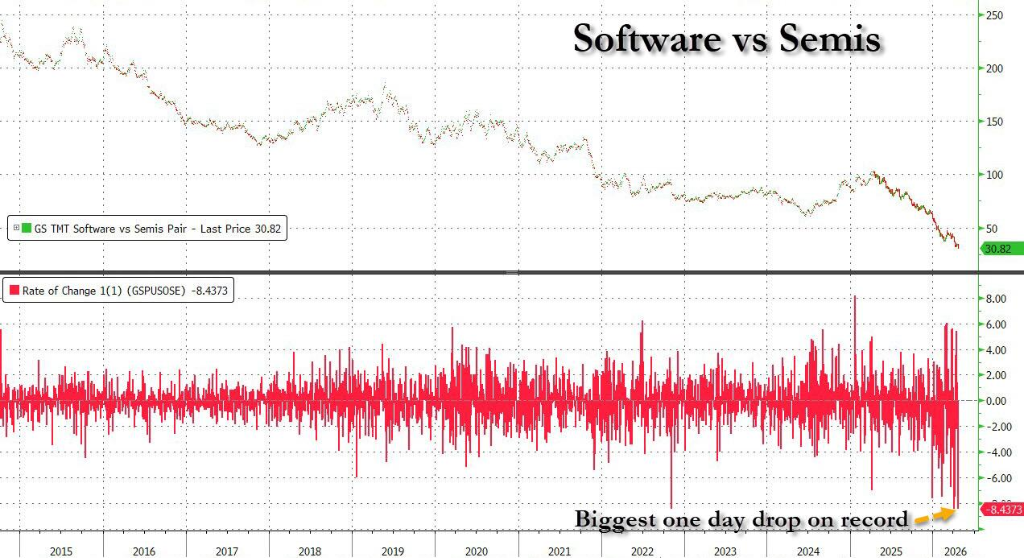

Among the S&P industry sectors, the software sector stood out with a sharp decline of 6%, ending eight consecutive quarters of growth.

$IBM Corp (IBM.US)$ Revenue growth slowed during the quarter, with weak performance in the software business leading to a significant drop in stock prices. $ServiceNow (NOW.US)$ This was due to delays in signing government projects in the Middle East, resulting in revenue growth below expectations and a subsequent plunge in stock prices.

Goldman Sachs' trading desk noted in an intraday report that ServiceNow's decline this time saw almost no buy-side inquiries, evoking a strong sense of "déjà vu"—recalling the lessons from last quarter’s earnings report. Some investors tend to "sell on good news," especially amid lingering concerns about AI disrupting the software industry over the long term.

On the same day that software stocks plummeted, the semiconductor sector strengthened again, with the Philadelphia Semiconductor Index rising by 1.7%, marking a record 17 consecutive trading days of gains.

$Texas Instruments (TXN.US)$ The company was the core driver of this rally, issuing Q2 revenue and profit guidance that exceeded Wall Street expectations. Its stock surged approximately 20% in a single day, marking the best daily performance since the bursting of the internet bubble.

According to LSEG data, as of Thursday morning, 82.1% of the 123 S&P 500 companies that had reported earnings exceeded analyst expectations, with overall profit growth reaching 15.6%, higher than the initial forecast of 14.4%. Bloomberg data shows that nearly 80% of S&P 500 companies beat expectations in Q1.

However, Goldman Sachs warned that end-of-month pension rebalancing is expected to generate approximately $25 billion in net selling pressure on U.S. equities, marking the largest non-quarter-end rebalancing in history. The corresponding figures for November and April 2020 were around $20 billion.

Meanwhile, the buying momentum of Commodity Trading Advisor (CTA) strategy funds, which had significantly driven the recent rebound, has notably weakened. Goldman Sachs’ model indicates that under flat market conditions, CTA’s expected buying volume for U.S. equities is only about $680 million, sharply reduced from the cumulative net purchase of $42.8 billion over the past month.

Thursday's PMI data showed that the U.S. manufacturing PMI in April rose to its highest level in nearly 47 months, while the composite PMI also rebounded. However, S&P Global noted that the improvement was mainly due to companies stockpiling in anticipation of supply disruptions and price increases, rather than a substantial strengthening of end-user demand.

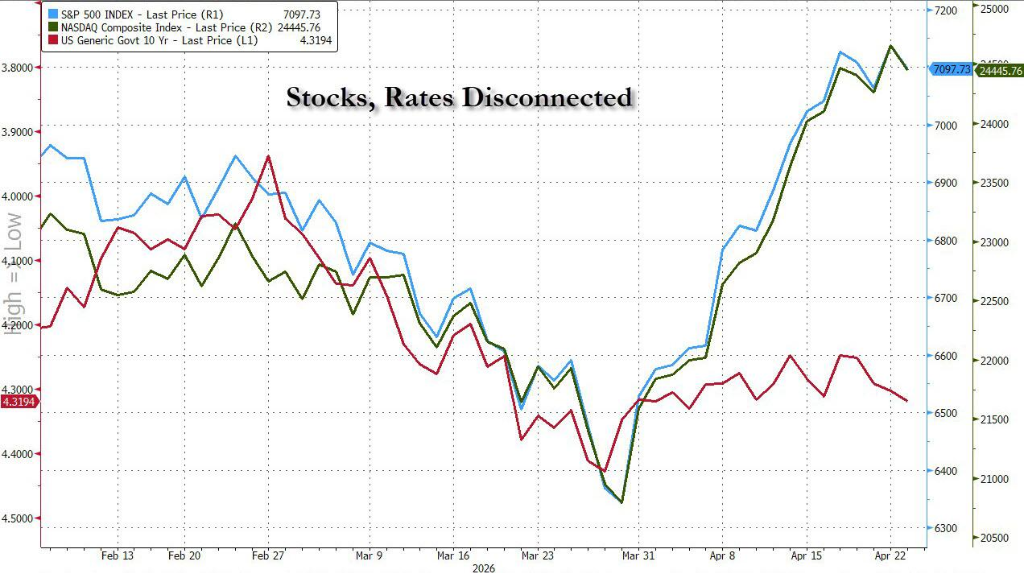

The yield on U.S. Treasuries rose to its highest level in several weeks, continuing to decouple from the trend of the U.S. stock market since April. The 10-year yield increased by 2 basis points, while the 2-year yield rose by 4.4 basis points to 3.834%.

The three major U.S. stock indexes closed lower on Thursday, while the semiconductor index posted gains for the seventeenth consecutive trading day. Salesforce fell 8.8%, leading declines among Dow components alongside American Express, IBM, Microsoft, and Honeywell, while Caterpillar rose 3.2%.

U.S. benchmark indices:

The S&P 500 Index fell 29.50 points, or 0.41%, to close at 7,108.40 points.

The Dow Jones Industrial Average fell 179.71 points, or 0.36%, to close at 49,310.32 points.

The Nasdaq Composite Index fell 219.07 points, or 0.89%, to close at 24,438.50 points.

The Russell 2000 Index fell 0.37% to close at 2,775.10 points.

The VIX volatility index, also known as the 'fear gauge,' rose 2.06% to close at 19.31.

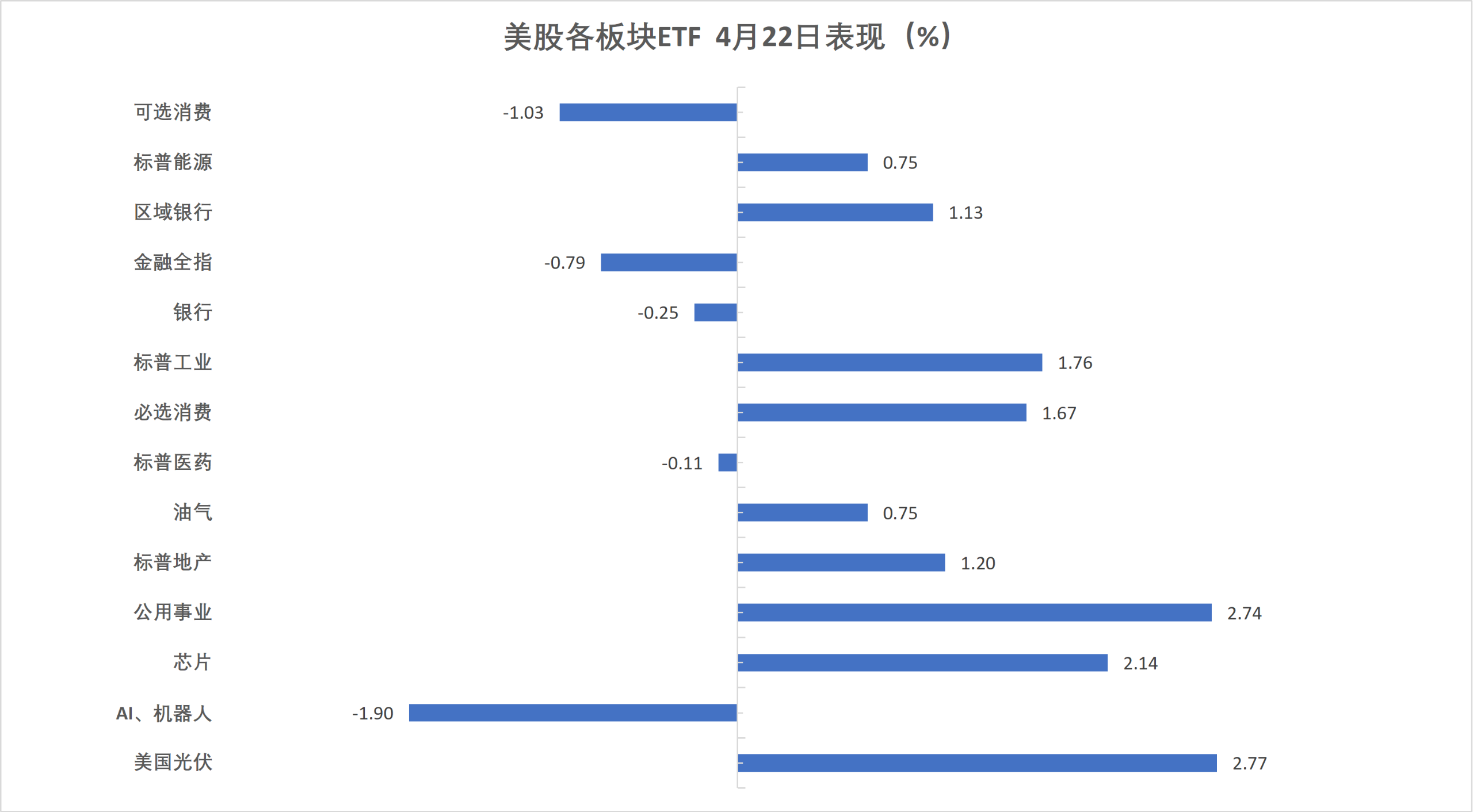

U.S. sector ETFs:

The U.S. solar energy sector rose 2.77%, utilities gained 2.74%, and the chip sector remained strong with a 2.14% increase. AI robotics fell by 1.90%.

Mag 7:

The Wind US Magnificent 7 Tech Stocks Index fell by 1.30%.

$Microsoft (MSFT.US)$Down 3.97%,$Tesla (TSLA.US)$Tesla fell by 3.97%, ServiceNow fell by 3.56%, Meta fell by 2.31%, NVIDIA fell by 1.41%, Alphabet A fell by 0.13%, Amazon fell by 0.11%, and Apple rose by 0.10%.

Chip Stocks:

The Philadelphia Semiconductor Index closed up 1.71% at 10,078.57 points.

Taiwan Semiconductor's ADR fell by 1.25%, while AMD rose by 0.62%.

Chinese Concept Stocks:

The Nasdaq Golden Dragon China Index closed down 2.4%.

Among popular Chinese stocks, TAL Education Group closed down 9.3%, XPeng fell by 6.4%, New Oriental fell by 5.8%, Pony AI fell by 5%, WeRide and Zai Lab fell by 4.3%, and Alibaba fell by 3.5%.

Other individual stocks:

$Circle (CRCL.US)$Down 4.07%.

$Salesforce (CRM.US)$ServiceNow closed down 8.8%, leading the decline among Dow components alongside IBM, American Express, Microsoft, and Honeywell, while Caterpillar rose by 3.2%.

European stock markets closed slightly higher, with Kongsberg's newly listed spin-off business soaring on its first day of trading. The French stock market closed up approximately 0.9%, while Italy's banking sector fell more than 1.1%.

Pan-European stocks:

The European STOXX 600 Index closed up 0.05% at 614.20 points.

The Eurozone STOXX 50 Index fell 0.19% to close at 5894.73 points, showing an overall V-shaped trend.

Major Stock Indexes Around the World:

Germany's DAX 30 Index dropped 0.16% to close at 24155.45 points.

France's CAC 40 Index rose 0.87% to close at 8227.32 points.

The UK FTSE 100 Index declined 0.19% to close at 10457.01 points.

Sector and Stock Performance:

Among the blue chips in the Eurozone, Germany's SAP SE fell 6.09%, EssilorLuxottica dropped 4.81%, Adyen declined 4.10%, ranking as the third-largest drop, Siemens Energy gained 2.45% for the third-best performance, Infineon Technologies surged 8.02%, and L'Oréal jumped 8.97%.

Among all components of the European STOXX 600 Index, Kongsberg Maritime SA soared 64599900.11% on its first day of trading in Oslo, STMicroelectronics rose 14.10%, and Sunbelt Rentals Holdings Inc. climbed 11.25%.

The yield on the US 10-year Treasury note increased, with a short-term spike occurring at 00:58 Beijing time, briefly rising from around 4.29% to 4.35%.

U.S. Treasuries:

At the New York close, the yield on the 10-year U.S. Treasury bond increased by 1.99 basis points to 4.3200%.

The yield on the two-year U.S. Treasury bond rose by 2.52 basis points to 3.8231%, while the yield on the 30-year U.S. Treasury bond climbed by 1.53 basis points to 4.9193%.

European debt:

At the European session close, the yield on the 10-year German government bond increased by 0.1 basis points to 3.009%, trading within a range of 3.047%-2.999% during the day, showing an overall trend of opening higher and closing lower.

The yield on the 10-year UK government bond rose by 2.9 basis points to 4.939%. The yield on the two-year UK government bond increased by 3.4 basis points to 4.369%.

The yields on the 10-year government bonds of France, Italy, Spain, and Greece rose by up to 1.3 basis points.

Abu Dhabi Murban crude oil futures in the Middle East rose by 1.13% to $104.29 per barrel, reaching $107.12 at 15:40 Beijing time.

Crude Oil:

WTI June crude oil futures settled at $95.85 per barrel.

Brent June crude oil futures settled at $105.07 per barrel.

Abu Dhabi Murban crude oil futures in the Middle East rose by 1.13% to $104.29 per barrel, reaching $107.12 at 15:40 Beijing time.

Natural Gas:

NYMEX May natural gas futures settled at $2.6140 per million British thermal units.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/Stephen