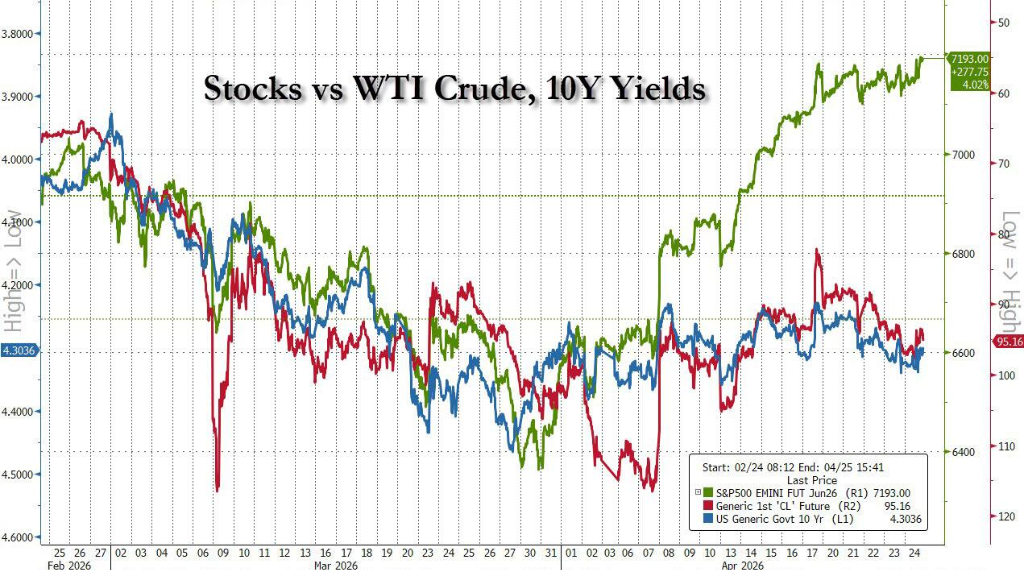

The US stock market showed a mixed performance on Friday, with the Dow closing lower while the S&P 500 gained 0.8% and the Nasdaq rose 1.6%, both reaching new all-time highs. The semiconductor sector extended its record-breaking streak to 18 consecutive days of gains. Intel surged to a record high, rising as much as 28% during the session, while AMD soared 14%. The yield on two-year US Treasury bonds fell more than 5 basis points on Friday as the Trump administration's decision to 'suspend' legal investigations bolstered investor expectations for a more accommodative monetary policy outlook.

Expectations for renewed negotiations between the US and Iran are rising, Intel's earnings exceeded expectations triggering a stock price surge, and the US Department of Justice dropped its criminal investigation into Powell. The major US stock indexes diverged, with the Dow closing lower while the S&P 500 and Nasdaq hit new highs.

Prospects for US-Iran talks are emerging. Iran’s official media confirmed that Alaghchi departed for Pakistan on Friday to hold talks focused on 'bilateral consultations.'

On the US side, American media cited informed officials stating that President Trump would dispatch Presidential Envoy Witkof and his son-in-law Kushner to Pakistan to participate in talks with Araghchi over the weekend.

On the US side, American media cited informed officials stating that President Trump would dispatch Presidential Envoy Witkof and his son-in-law Kushner to Pakistan to participate in talks with Araghchi over the weekend.

This diplomatic progress pushed crude oil prices down, with the S&P 500 rising approximately 0.8%, closing out a four-week winning streak—the longest since September 2024.

Meanwhile, the US Department of Justice dropped its criminal investigation into Powell, which the market interpreted as a clearer path for monetary policy. Traders immediately increased bets on rate cuts, with the two-year Treasury yield falling by 4.5 basis points.

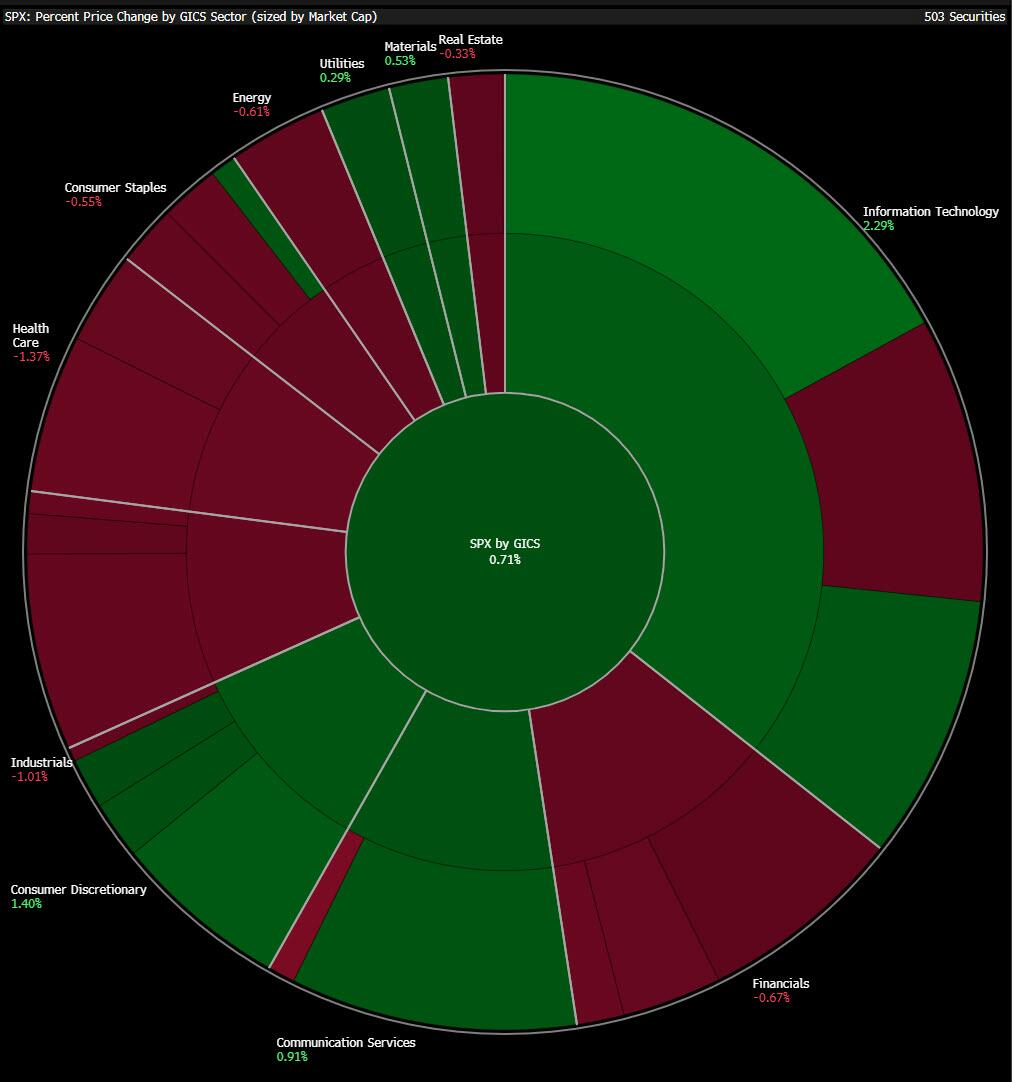

However, behind the record highs, the internal structure of the market remains imbalanced. About 62% of S&P 500 constituents, or more than 320 stocks, closed lower. The strong performance was highly concentrated in technology and semiconductor sectors, while defensive sectors like healthcare faced significant pressure.

The most notable movement in the market this week came from the semiconductor sector. The Philadelphia Semiconductor Index rose for 18 consecutive trading days, setting a record for the longest streak, with technical indicators showing the highest overbought level ever recorded.

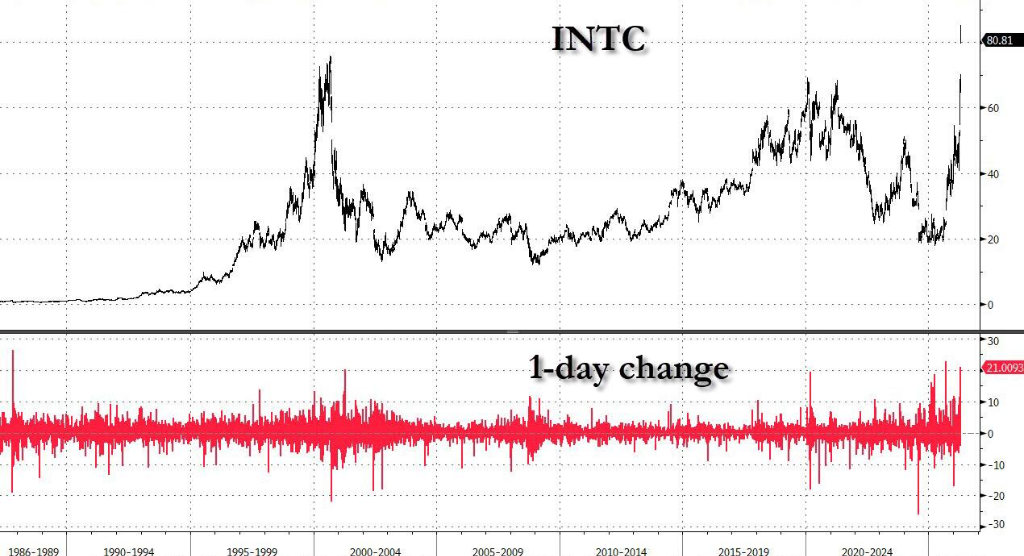

$Intel (INTC.US)$ Intel was the standout performer this week. Following the release of robust earnings and optimistic forward guidance, its shares surged as much as 28% intraday—the largest single-day gain since 'Black Monday' in 1987—ultimately closing up about 21%, surpassing the previous all-time high set during the dot-com bubble peak.

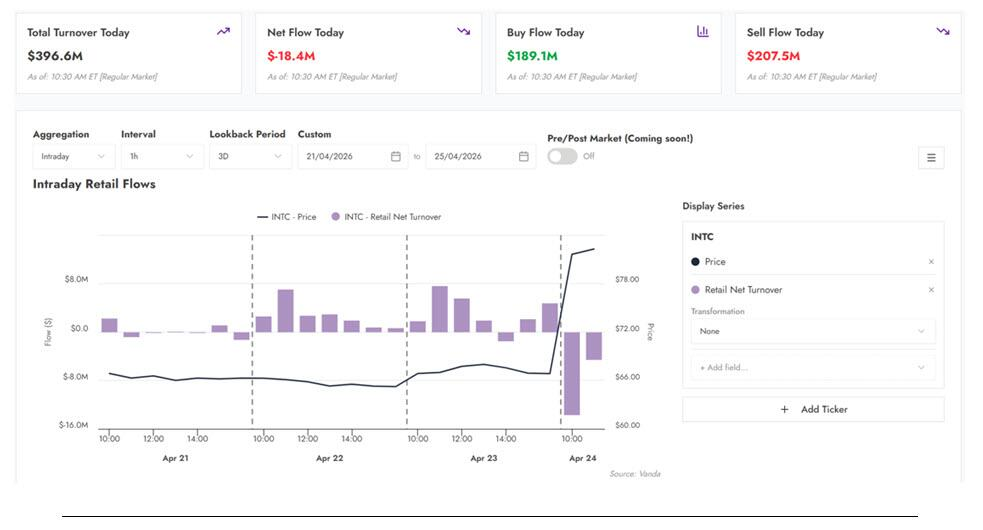

According to Vanda Research data, retail investors performed well on Intel's trade.

Since early September of last year, coinciding with the Trump administration’s announcement of an $89 billion stake in Intel, retail investors have been consistently buying. Since then, net purchases have totaled $26 billion, with two noticeable peaks: one in October 2025 and another at the beginning of this year.

Based on current prices, the average retail investor who has held Intel since September of last year has gained nearly 90%. Early trading data on Friday showed that some retail investors began taking profits, with net selling reaching $18.4 million in the morning session.

The upward momentum in the semiconductor sector extends beyond Intel. SAP SE reported better-than-expected growth in cloud service revenue, while Taiwan Semiconductor surged significantly after Taiwan's financial regulatory authority relaxed restrictions on single-stock fund holdings, further boosting sentiment across the entire sector.

While technology stocks experienced a broad-based rally, the healthcare sector was one of the weakest performers on Friday, declining approximately 1% overall.

$Eli Lilly and Co (LLY.US)$ The stock price fell by about 4%. New prescription data showed weak initial sales for its new weight-loss drug Foundayo, with prescription volumes notably lower than those for Novo-Nordisk A/S's oral Wegovy. According to Goldman Sachs' trading desk:

It currently feels as though the healthcare sector is being used as a source of funding for purchasing technology stocks.

This phenomenon is fairly widespread in the current market. The renewable energy sector also lagged behind, falling by around 2% overall.

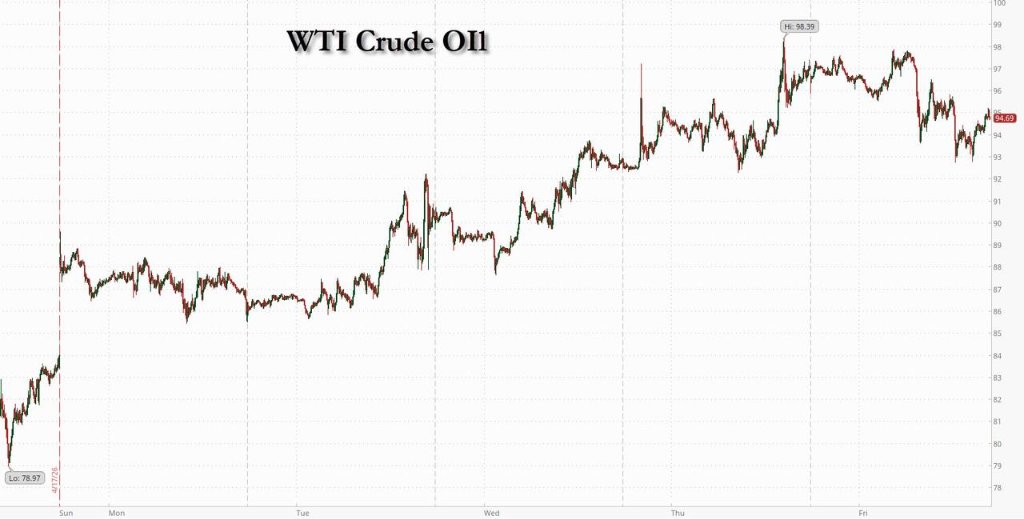

Crude oil prices experienced significant intraday volatility on Friday. Influenced by the mood surrounding US-Iran negotiations, oil prices initially surged over 3%, but reversed course and fell more than 3% following news that Trump had sent an envoy.

Nevertheless, oil prices still recorded substantial gains for the week overall.

On Friday, the US stock market saw divergent performances, with the Dow closing lower, while the S&P 500 rose 0.8% and the Nasdaq climbed 1.6%, both hitting record highs. The semiconductor sector extended its record-breaking streak to 18 consecutive days. Intel soared to a record high, surging as much as 28% during the session, while Advanced Micro Devices jumped 14%.

U.S. benchmark indices:

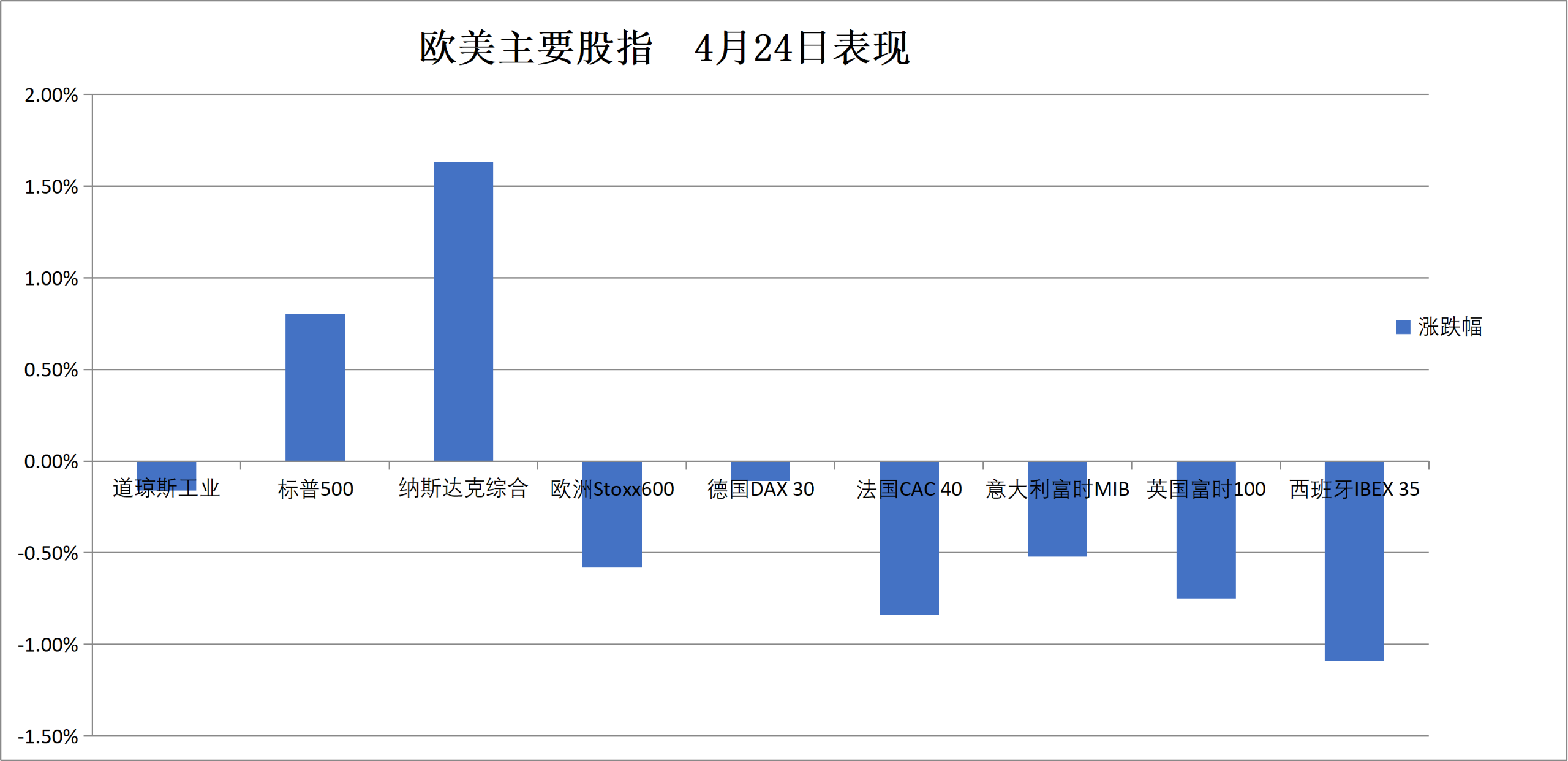

The S&P 500 Index closed up 56.68 points, or 0.80%, at 7,165.08 points, setting a new closing high after a one-day hiatus, with a cumulative weekly gain of 0.55%.

The Dow Jones Industrial Average closed down 79.61 points, or 0.16%, at 49,230.71 points, posting a cumulative weekly decline of 0.44%.

The Nasdaq Composite Index closed up 398.094 points, or 1.63%, at 24,836.599 points, hitting a new closing high after a day, and gaining 1.50% for the week.

The Nasdaq 100 Index closed up 521.042 points, or 1.95%, at 27,303.667 points, reaching a new closing high after a day, and increasing by 2.37% over the week.

The Russell 2000 Index closed up 0.43% at 2,787.001 points, rising 0.36% for the week.

The VIX Volatility Index closed down 3.21% at 18.69, with a weekly increase of 6.92%.

U.S. sector ETFs:

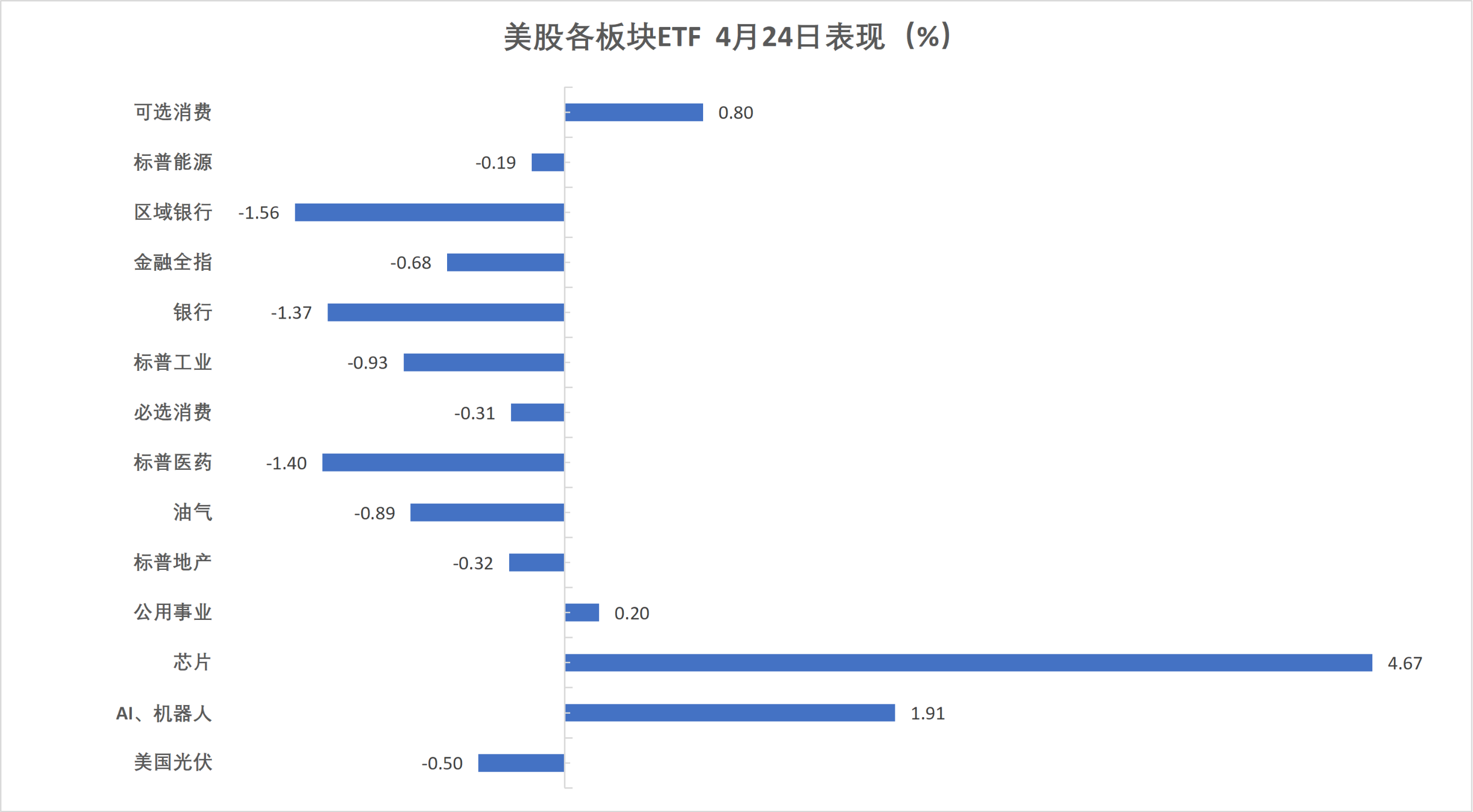

U.S. sector ETFs saw mixed performance, with the semiconductor ETF closing up 5.11%, global technology stock index ETF and tech sector ETF rising more than 2.8%, and the internet index ETF gaining over 1.2%.

Mag 7:

The Mag 7 index rose 2.08% to 213.18 points, with a cumulative weekly gain of 1.19%.

$NVIDIA (NVDA.US)$Up 4.32%,$Amazon (AMZN.US)$Advanced Micro Devices surged 4.32%, NVIDIA gained 3.49%, Meta rose 2.41%, Microsoft increased 2.13%, Alphabet A climbed 1.63%, Tesla advanced 0.69%, while Apple fell 0.87%.

This week, Amazon rose 5.36%, NVIDIA rose 3.26%, Alphabet A rose 0.8%, Microsoft rose 0.43%, Apple rose 0.31%, Meta fell 1.96%, and Tesla fell 6.07%.

Chip Stocks:

The Philadelphia Semiconductor Index closed up 435.092 points, or 4.32%, at 10,513.664 points, rising 10.02% this week.

$Intel (INTC.US)$ Up 24%, marking the best single-day performance since 1987.

Taiwan Semiconductor ADR rose 5.18%, $Advanced Micro Devices (AMD.US)$ up 13.91%.

Chinese Concept Stocks:

The Nasdaq Golden Dragon China Index closed up 1.59% at 6,952.52 points, falling 3.85% cumulatively this week.

Among popular Chinese stocks, Baidu closed up 5.9%, Zai Lab, XPeng, and GDS Holdings rose more than 4%, while 21Vianet, WeRide, and Alibaba rose about 3% each.

Other individual stocks:

Eli Lilly and Co's shares fell about 4%. New prescription data showed weak initial sales of its new weight-loss drug Foundayo.

Advanced nuclear energy company $X-Energy (XE.US)$The stock surged 27% on its first day of trading, as the nuclear energy industry has attracted a new wave of capital interest driven by the AI boom and electrification trend.

The Eurozone blue-chip index fell approximately 2.9% this week. The French stock market closed down over 0.8%, while the Italian banking sector dropped about 7.2% and the German defense ETF fell approximately 9.4% for the week.

Pan-European stocks:

The European STOXX 600 Index closed down 0.58% at 610.65 points, accumulating a weekly decline of 2.54%. It opened with a gap down on Monday and continued to extend losses since Tuesday.

The Eurozone STOXX 50 Index closed down 0.19% at 5883.48 points, with a cumulative weekly decline of 2.88%.

Major Stock Indexes Around the World:

The German DAX 30 Index closed down 0.11% at 24128.98 points, accumulating a weekly decline of 2.32%.

The French CAC 40 Index closed down 0.84% at 8157.82 points, accumulating a weekly decline of 3.17%.

The UK FTSE 100 Index closed down 0.75% at 10379.08 points, accumulating a weekly decline of 2.70%.

Sector and Stock Performance:

Among Eurozone blue chips, Germany’s Rheinmetall RHM fell 6.24%, Bayer dropped 3.85%, Safran shares declined 3.23% as the third-largest drop, while Infineon Technologies rose 1.50%, ranking fifth in performance.

Among all the components of the European STOXX 600 Index, Tomra Recycling Systems fell by 25.56%, Indutrade dropped by 15.26%, and Mondi fell by 11.12%, ranking as the third-largest decline. BE Semiconductor Industries closed up 4.30%, marking the seventh-best performance.

The yield on two-year U.S. Treasury bonds fell more than 5 basis points on Friday, as the Trump administration's 'suspension' of legal investigations improved investors’ expectations for a looser monetary policy outlook. The yield on two-year UK government bonds rose approximately 23 basis points this week.

U.S. Treasuries:

At the New York close, the yield on the benchmark 10-year U.S. Treasury bond fell by 2.37 basis points to 4.3007%.

The yield on two-year U.S. Treasury bonds fell by 5.54 basis points to 3.7783%, with a cumulative increase of 7.01 basis points this week.

European debt:

At the European session close, the yield on 10-year German government bonds fell by 1.5 basis points to 2.994%, with a cumulative increase of 3.4 basis points this week, trading within a range of 2.906%-3.047%.

The yield on 10-year UK government bonds fell by 2.7 basis points to 4.912%, with a cumulative rise of 15.0 basis points this week, maintaining an upward trend and trading in a range of 4.769%-4.993%.

This week, the yield on 10-year French government bonds increased by 5.9 basis points cumulatively, while the yield on two-year French government bonds rose by 13.4 basis points, and the yield on 30-year French government bonds increased by 0.9 basis points.

According to the CFTC positioning report in the United States, during the week ending April 21, speculators reduced their net long positions in NYMEX WTI crude oil by 842 contracts to 143,401 contracts.

Crude Oil:

WTI June crude oil futures closed down $1.45, or 1.51%, at $94.40 per barrel, with a cumulative increase of nearly 14.30% this week.

Brent June crude oil futures closed at $105.33 per barrel.

Middle East Abu Dhabi Murban crude oil futures fell 1.74% to $104.11 per barrel, with a cumulative weekly gain of 13.53%.

Natural Gas:

NYMEX May natural gas futures closed at $2.5230 per million British thermal units.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/Stephen