JPMorgan has warned that the supply and demand accounts are now “unbalanced,” with idle capacity completely failing. If the market is to eventually clear, it will trigger an oil price storm far exceeding expectations, driving extreme high prices to force significant consumption cuts in Europe and the United States!

The strangest aspect of the oil market now is that the accounts don't add up: a significant portion of supply has been removed, inventories are rapidly shrinking, and demand is also declining, yet the price reaction does not resemble a market being forced to liquidate. JPMorgan's conclusion is straightforward—there is something wrong with this global crude oil supply and demand equation.

Natasha Kaneva, JPMorgan’s commodity strategist, wrote in her latest research report: "From a practical operational perspective, oil prices must rise much higher." Her reasoning is that physical commodity markets will eventually be forced back into equilibrium: when idle capacity cannot compensate and inventories continue to thin out, the only recourse is higher prices to suppress consumption and allow the market to clear.

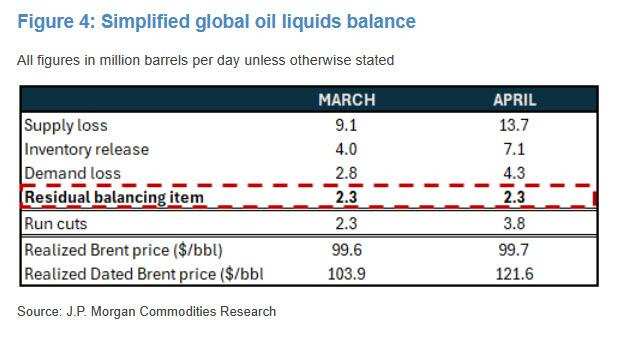

The research report highlights several key figures: global supply disruptions amounted to 9.1 million barrels per day (mbd) in March, expanding to 13.7 mbd in April; observable commercial and strategic inventories were drawn down at average daily rates of 4.0 mbd and 7.1 mbd, respectively; global oil demand fell by an average of 2.8 mbd per day in March and so far tracked a 4.3 mbd reduction in April. The issue lies in the fact that Brent futures’ average price remains below $100 per barrel, making this pace of demand decline look more like 'forced conservation,' rendering the price-suppressing-demand logic untenable here.

The research report highlights several key figures: global supply disruptions amounted to 9.1 million barrels per day (mbd) in March, expanding to 13.7 mbd in April; observable commercial and strategic inventories were drawn down at average daily rates of 4.0 mbd and 7.1 mbd, respectively; global oil demand fell by an average of 2.8 mbd per day in March and so far tracked a 4.3 mbd reduction in April. The issue lies in the fact that Brent futures’ average price remains below $100 per barrel, making this pace of demand decline look more like 'forced conservation,' rendering the price-suppressing-demand logic untenable here.

The inference follows: the gap cannot be closed solely by relying on the Middle East, peripheral economies in Asia, and Africa. JPMorgan believes that higher oil prices must also pull Europe and the US into this rebalancing. Cracks have already emerged on the product side: petrochemical feedstock and jet fuel contractions are leading the way, while gasoline appears more resilient, though this buffer may not last through the peak season.

The gap is too large to be cleared at current prices.

The starting point of the research report is physical constraints: crude oil accounts must balance every day. When supply falls short, the market first looks to idle capacity to fill the gap; if that fails, inventories must be drawn upon; as inventories tighten, prices must rise until demand is suppressed to the level where 'available oil can still be purchased.'

What Kaneva refers to as 'arithmetic imbalance' centers on this: the magnitude of supply removal is so large that the currently observable inventory drawdowns and demand declines combined are still insufficient to fully close the gap. As long as the gap persists, prices will only be pushed to a level that allows the market to clear.

The buffer of idle capacity has failed.

Under normal circumstances, idle capacity serves as the largest cushion for the oil market. This time, its failure is specific: almost all idle capacity is concentrated in Saudi Arabia and the UAE, and under the current shock, this capacity's ability to supply the global market has effectively been severed.

The United States, as the marginal supplier, cannot provide immediate relief either. Even if oil prices rise significantly, a meaningful increase in shale oil production typically takes three to six months to materialize, contributing only about 0.3 to 0.7 million barrels per day (mbd) within this window; larger increments often require six to twelve months. Russia still has approximately 300,000 barrels per day (kbd) of idle capacity, but recent attacks on energy infrastructure have led to a supply reduction of 350 kbd, making repairs even more difficult.

The corrective mechanism on the supply side is stuck, leaving the market with no choice but to rely earlier and more heavily on inventory drawdowns and demand compression.

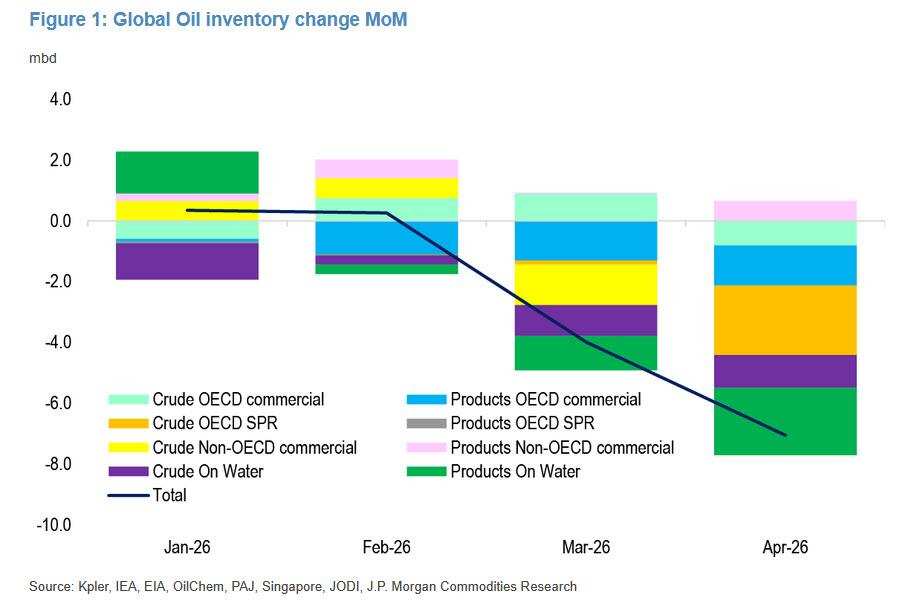

Inventories are being drawn down at an accelerating pace, and visibility remains incomplete.

After idle capacity proved insufficient, inventories were forced into action. JPMorgan estimates that observable inventories were drawn down by an average of 4.0 million barrels per day (mbd) in March, accelerating to 7.1 mbd in April — the intensity of relying on inventories to bridge the gap is rising significantly.

More troubling is the issue of visibility. Research reports warn that the market does not have full visibility into all inventories, especially refined product stocks, which have lower transparency. The actual destocking magnitude may be greater than reported figures. As inventories approach operational lows, the task for prices becomes singular: rising high enough to force consumption cuts.

Demand is falling, but not necessarily because it has become unaffordable.

The research report benchmarks the decline in demand to the financial crisis: In January 2009, global peak demand fell by about 2.5 mbd, whereas this March saw a drop of 2.8 mbd, expanding further to 4.3 mbd so far in April. The anomaly lies in the price: Brent futures averaged less than $100 per barrel in both March and April, spot crude averaged about $107 in March and $123 in April, while refined product prices nearly doubled from pre-war levels. Price alone struggles to explain such a steep drop in demand over such a short period.

The research report offers a starker explanation: A significant portion of what appears to be 'demand destruction' is actually the reflection of supply shortages on the demand side — scarcity constrained actual consumption, leaving consumers unable to purchase fuel and thus forced to reduce usage.

Emerging economies in the Middle East, Asia, and Africa bore 87% of the burden.

If demand contraction primarily stems from 'unavailability,' then the focus shifts to who will be the first unable to secure supplies. Adjustments to date have mainly concentrated in peripheral economies in the Middle East and Asia, followed by Africa: the former is at the epicenter of the shock, while the latter heavily relies on Gulf crude and refined products, with thin inventories and weak fiscal buffers. When cargo flows are rerouted to higher-paying markets, some buyers are directly squeezed out.

JPMorgan estimates that these regions collectively accounted for 87% of the 4.3 million barrels per day (mbd) demand decline in April. Rebalancing cannot rely solely on reductions from these areas over the long term; the shortfall will inevitably shift to larger consumption zones.

To fill the gap, Europe and the U.S. must also participate.

The research report brings the issue back to arithmetic: approximately 14 mbd of supply has been removed. Even under the aggressive assumption of "daily inventory drawdowns of 8 mbd," the market still requires an additional demand reduction of around 2 mbd to clear the surplus.

This magnitude is far beyond what emerging markets can absorb alone; Europe and the U.S. must also engage in rebalancing. To achieve sufficient demand compression in these two major consumption zones, prices need to rise further. Europe is already tightening, with diesel and jet fuel already constrained, and supply disruptions are further squeezing the availability of middle distillates. The Americas, in the short term, remain more "isolated" due to better domestic supply elasticity and inventory buffers, but higher retail gasoline prices have started to suppress discretionary driving demand, while rising airfares are softening jet fuel demand.

The first cracks are appearing at the product level: petrochemicals and jet fuel are being forced into shutdowns, and the buffer for gasoline is disappearing.

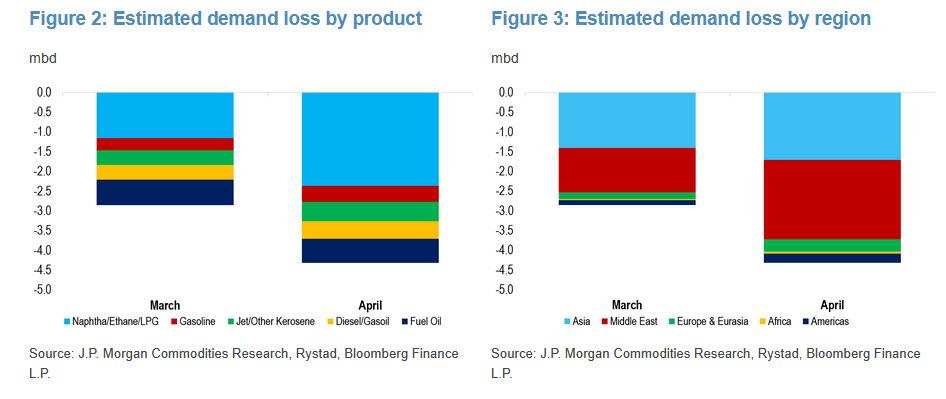

The first sectors to be hit are those with thin margins and high price sensitivity. Shortages of LPG, ethane, and naphtha in the Gulf region have forced many PDH and steam cracking facilities in Asia to reduce operations or even shut down. LPG is also a key household fuel in India, where LPG consumption fell by 13% year-on-year in March.

JPMorgan estimates that weakness in petrochemical feedstock accounts for about 55% of the 4.3 mbd demand loss in April; jet fuel accounts for 11%, mainly reflecting evaporating demand due to flight suspensions in the Middle East. Further contraction in aviation activity across Asia and Europe in May will weaken jet fuel demand further. For gasoline, dependence on Gulf supplies is relatively lower, so price increases have been less pronounced compared to middle distillates thus far. However, this isolation may not last long: refinery constraints are tightening, broader refined product balances are becoming strained, and seasonal demand from the U.S. summer driving season will eventually drag gasoline into the same tight net.

This article is reprinted from Wall Street News; Author: Pan Lingfei; Zhitong Finance Editor: Wang Qiujia.

Editor/Lee