On Thursday, Google, Amazon, Meta, and Microsoft will release their earnings reports on the same day, a rare occurrence. The combined market value of these four companies has exceeded 11.6 trillion US dollars. This time, the market is no longer seeking promises of 'willingness to spend,' but rather concrete answers regarding accelerated cloud revenue growth, order fulfillment, and controlled profit margins. Microsoft, which has experienced a significant drop in its stock price this year, is considered to be under the most pressure among the four. Meanwhile, the Federal Reserve will announce its interest rate decision, and Powell will preside over his last press conference during his term.

Within a single day, Wall Street must digest earnings reports from four tech giants alongside multiple interest rate decisions — a day the market has dubbed 'one of the most important earnings days in recent years.'

On April 29 Eastern Time (early morning to early hours on April 30 Beijing Time), Alphabet (Google), Amazon, Meta, and Microsoft will release their quarterly results after the market close on the same trading day. Concurrently, the Federal Reserve's FOMC will conclude its two-day meeting, announcing its interest rate decision, with Fed Chair Powell also hosting his last press conference during his term. The Bank of England and the European Central Bank are also set to announce their latest interest rate decisions on the same day.

Matt Stucky, Chief Portfolio Manager at Northwestern Mutual, characterized this day as 'one of the most important earnings days in recent years.' The combined market capitalization of the four companies is approximately $11.6 trillion, accounting for over 19% of the S&P 500 Index; any volatility in one company’s performance could significantly impact the broader market.

Matt Stucky, Chief Portfolio Manager at Northwestern Mutual, characterized this day as 'one of the most important earnings days in recent years.' The combined market capitalization of the four companies is approximately $11.6 trillion, accounting for over 19% of the S&P 500 Index; any volatility in one company’s performance could significantly impact the broader market.

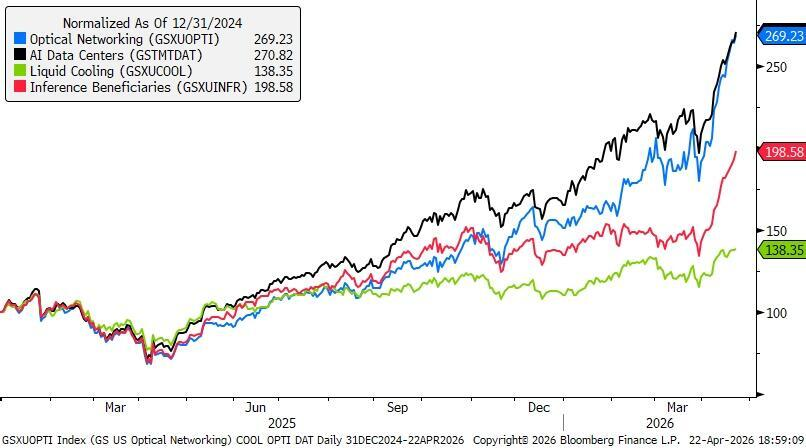

The S&P 500 Index and Nasdaq Index have rebounded approximately 11% and 18%, respectively, from recent lows, with funds flowing back into technology and data center-related sectors. The core narrative behind this rally is the ongoing expansion of AI investments. This earnings season will be a key test of whether this narrative can continue.

A $650 billion AI bill, the market wants to see returns.

The combined capital expenditure budget for the four companies this year totals $650 billion: Google’s guidance is $175 billion to $185 billion, Meta’s is $115 billion to $135 billion, Amazon’s is about $200 billion, and Microsoft spent $37.5 billion on capital expenditures in the previous quarter alone.

Money continues to pour in, but market patience is dwindling.

Bernstein analyst Mark Shmulik wrote in a research note last week that the four hyperscale cloud providers need to achieve three things simultaneously: deliver AI-driven revenue that exceeds expectations, maintain their capital expenditure budgets without reduction, and demonstrate cost control through layoffs or pricing power. 'Overall, the landscape entering the earnings season is quite clear and consistent.'

Citizens analyst Andrew Boone told MarketWatch, 'The entire AI ecosystem is currently constrained by supply' — insufficient infrastructure and energy to meet computational demands. Therefore, the four companies need to prove they can bring data center capacity online fast enough to address the backlog of orders. 'Part of the issue is who can execute well enough to put capital expenditures into practice effectively.'

Demand-side signals remain robust. Boone pointed out that computing power demand has surged rapidly since 2026: Anthropic signed a series of new agreements to expand access to AI infrastructure; Amazon announced the provision of tens of millions of customized Graviton chips to Meta; Google disclosed at last week’s Google Cloud Next conference that the number of tokens processed daily by its models had increased from 1 billion in the previous quarter to 1.6 billion.

Each company faces different pressures, with Microsoft in the most delicate position.

Google's main pressure lies on the cost side. The company had previously indicated that depreciation growth would accelerate in the first quarter and rise significantly throughout the year. The market is not concerned about whether Google will continue to invest but rather whether cloud business and AI-related revenues can absorb this expenditure more quickly.

Meta’s challenge is the most straightforward. It possesses the strongest advertising cash flow and also the most aggressive infrastructure investment. The company has clearly stated that capital expenditures will rise to between $115 billion and $135 billion in 2026, but its annual operating profit will still be higher than in 2025. After the earnings report, the market will quickly assess whether the profitability of the advertising business can continue to cover the expansion pace of AI investments.

Amazon’s issue is not just about heavy investment but also about delayed returns on spending. In his shareholder letter, CEO Andy Jassy explicitly stated that most of the cloud business’s capital expenditures in 2026 will materialize gradually between 2027 and 2028. AWS added 3.9 gigawatts of power capacity in 2025, with total capacity expected to double by the end of 2027, but the company still acknowledged capacity constraints and unmet demand. This time, the market will pay special attention to how management discusses customer commitments, capacity ramp-up, and the timeline for realization.

Microsoft is in the most delicate situation. Matt Stucky believes that among the four companies, Microsoft carries the highest risk. Last quarter, Azure’s cloud growth disappointed the market, and Copilot’s enterprise adoption rate was lower than expected. Its stock price has fallen by 12% year-to-date, making it the worst performer among the four. Guggenheim analyst John DiFucci estimates that Wall Street expects Azure’s growth this quarter to be around 38%, but he wrote in a research note last week: "This expectation implies a significant jump in new business growth, which seems unlikely."

Stucky noted that the adoption trend of Microsoft Copilot will influence market sentiment for the entire software sector this quarter.

Powell’s 'last dance' – interest rate expectations have already been priced in.

On the same day, the Federal Reserve’s FOMC will conclude its two-day meeting and announce the interest rate decision. The market has fully priced in the expectation that rates will remain unchanged in the range of 3.50% to 3.75%.

Following the interest rate cut in the second half of 2025, the Federal Reserve promptly paused. Rising oil prices have complicated the inflation outlook, further delaying the timing for additional rate cuts.

This will also be Powell’s last press conference as Chairman of the Federal Reserve. His term as chairman will expire on May 15, and Trump's nominee, Warsh, is expected to be confirmed by the Senate before the Fed’s mid-June meeting. The biggest suspense now is whether Powell will announce his intention to remain on the Federal Reserve Board after stepping down as chairman.

Geopolitical Risks: The Strait of Hormuz Impacts AI Supply Chains

Geopolitical dynamics added an extra variable to the day. The blockade of the Strait of Hormuz has directly impacted global energy flows and supply chains, with data center supply chains also being affected.

Moody's analyst Terrence Dennehy highlighted in a research note last week that the Middle East conflict poses a 'supply risk' to the helium market. 'Helium is critical in multiple stages of semiconductor manufacturing—including cooling, carrier gas usage, and leak detection—and has no effective substitutes,' Dennehy wrote.

Stucky from Northwestern Mutual also noted that the possibility of the four companies further raising their capital expenditure forecasts cannot be ruled out, which could trigger a new round of market concerns about overinvestment in AI.

How the Market Prices After Earnings Reports

This earnings report is more like a screening point rather than an overall switch.

Wall Street Insight mentioned that there are currently no signs of the AI-driven trend coming to an end, with funds still flowing in. However, the market’s pricing logic is diverging: Companies delivering faster results, firmer orders, and steadier profits will continue to receive premium valuations; companies making significant investments but with unclear return paths will experience more pronounced stock price volatility.

The industrial chain encompassing semiconductors, servers, networking equipment, and data center infrastructure continues to closely follow the investments of major firms. Recent divergence in software and chips indicates the market is beginning to consolidate around areas closer to orders and infrastructure within this main theme. If the upcoming earnings reports from the four companies reaffirm demand and capital expenditure intensity, such divergence will only become more pronounced.

On the day of the earnings report, the market's most pressing specific questions are: whether the full-year capital expenditure forecast will be revised upward again, whether the growth rate of the cloud business can continue to rise, whether there is clearer disclosure regarding AI-related revenue, and whether there has been more noticeable pressure on profit margins and cash flow.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/joryn