Barclays believes that investors are increasingly inclined to reward segments of the value chain that are closer to monetizing profits, including uranium mining and processing, engineering and construction companies, and power producers with existing generation capacity, while developers of small modular reactors (SMRs) that have yet to generate revenue face higher valuation uncertainty.

Nuclear energy is transitioning from policy consensus to the substantive construction phase, with the market increasingly rewarding companies that can demonstrate actual delivery capabilities—whether in the operation and expansion of existing units or in credible pathways for advanced reactors from licensing to commencement.

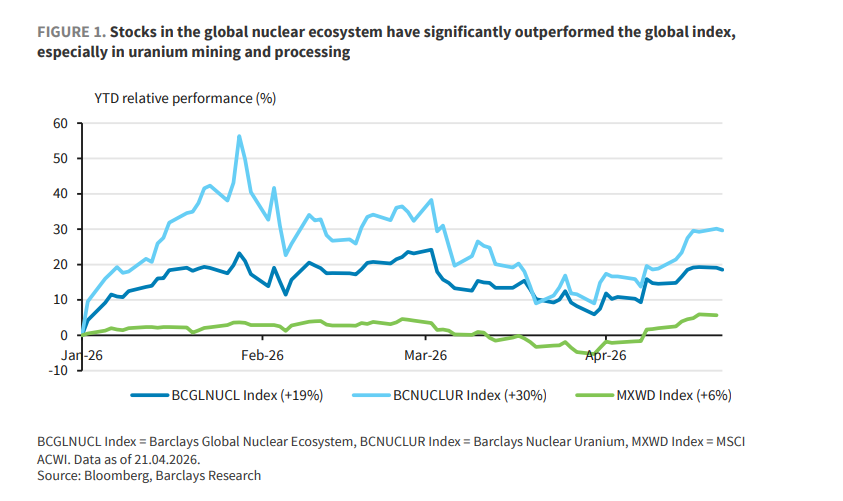

According to the Wind Chase trading platform, the latest research report by Barclays shows that since 2026, the three driving forces of energy security, decarbonization, and AI computing power demand have continued to strengthen. Global nuclear energy ecosystem stocks have risen cumulatively by 19% year-to-date, with the uranium mining and processing sector surging by as much as 30%, significantly outperforming the 6% gain of the global benchmark index.

The escalation of the situation in the Middle East has become a significant catalyst for the acceleration of nuclear energy policies in this round. The Trump administration in the United States announced an investment of $2.7 billion into domestic uranium enrichment capacity, and the Nuclear Regulatory Commission (NRC) subsequently issued construction permits for advanced reactor projects by TerraPower and Holtec; in Asia, Unit 6 of Tokyo Electric Power's Kashiwazaki-Kariwa nuclear power plant resumed commercial operations; in Europe, both Sweden and Switzerland have advanced legislative processes to repeal bans on nuclear power. Meanwhile,$Meta Platforms (META.US)$and$Vistra Energy (VST.US)$, TerraPower,$Oklo Inc (OKLO.US)$signed a comprehensive agreement with potential support reaching up to 6.6 GW of nuclear capacity, marking an evolution in demand from hyperscalers for nuclear energy, transitioning from single-asset support to portfolio-based procurement.

The escalation of the situation in the Middle East has become a significant catalyst for the acceleration of nuclear energy policies in this round. The Trump administration in the United States announced an investment of $2.7 billion into domestic uranium enrichment capacity, and the Nuclear Regulatory Commission (NRC) subsequently issued construction permits for advanced reactor projects by TerraPower and Holtec; in Asia, Unit 6 of Tokyo Electric Power's Kashiwazaki-Kariwa nuclear power plant resumed commercial operations; in Europe, both Sweden and Switzerland have advanced legislative processes to repeal bans on nuclear power. Meanwhile,$Meta Platforms (META.US)$and$Vistra Energy (VST.US)$, TerraPower,$Oklo Inc (OKLO.US)$signed a comprehensive agreement with potential support reaching up to 6.6 GW of nuclear capacity, marking an evolution in demand from hyperscalers for nuclear energy, transitioning from single-asset support to portfolio-based procurement.

Barclays maintained its bullish stance on the nuclear energy sector in the report but noted that the market is becoming more selective—investors are increasingly inclined to reward those segments of the value chain closer to profit realization, including uranium mining and processing, engineering and construction firms, and power producers with existing generation capacity. Developers of small modular reactors (SMRs), which have yet to generate revenue, face higher valuation uncertainties.

Market Repricing: Rewarding Execution Over Narrative

Barclays data shows that as of April 21, 2026, the Barclays Global Nuclear Ecosystem Index (BCGLNUCL) has risen by 19% year-to-date, while the Barclays Nuclear Uranium Index (BCNUCLUR) surged by 30%, both significantly outperforming the 6% gain of the MSCI World Index (MXWD).

However, Jordan Isvy and Maggie O’Neal, analysts at Barclays, emphasized in the report that the market gains were not evenly distributed.

Construction companies demonstrated the strongest performance, with Hyundai Engineering & Construction (Hyundai E&C) seeing an annual increase of 142%; power companies that own existing nuclear capacity and can benefit from power upgrades or license extensions also performed well, with Engie SA rising 26% year-to-date. In contrast, the stock prices of advanced reactor companies such as NuScale and Oklo exhibited higher volatility, reflecting growing investor caution regarding timelines, permitting risks, and the gap between technology validation and contractual projects.

Barclays concluded that the next phase of the nuclear energy theme will increasingly reward “enablers” and “existing operators.” Investors are no longer willing to pay solely based on narratives but are instead gravitating toward rewarding tangible megawatt deliveries, visible licensing progress, or at least credible pathways from concept to contracted projects.

Policy Acceleration: From Endorsement to Empowerment

By 2026, global nuclear energy policy has transitioned from principled support to the implementation of specific industrial policies, with substantial progress observed in North America, Europe, and Asia.

In the United States, the Trump administration viewed nuclear energy as a geostrategic tool to win the global AI competition, introducing a series of aggressive industrial policies. The U.S. Department of Energy (DOE) allocated approximately $900 million each to three companies—Centrus, Orano, and General Matter—to expand domestic uranium enrichment capacity, covering both high-assay low-enriched uranium (HALEU) for advanced reactors and low-enriched uranium (LEU) for conventional light-water reactors. The NRC also issued a construction permit for TerraPower’s 345 MW Natrium project in Kemmerer and accepted a phased construction permit application for Holtec SMR-300 at Palisades.

In Asia, the Middle East crisis has made energy security even more urgent. Unit 6 of Tokyo Electric Power's Kashiwazaki-Kariwa plant resumed commercial operations for the first time since the Fukushima accident. The South Korean government approved its 11th Basic Plan, committing to add 2.8 GW of large reactors and 700 MW of SMR capacity by 2038. Meanwhile, India passed legislation to break state monopolies and open its civilian nuclear energy market to private capital, aiming to achieve 100 GW of nuclear power capacity by 2047.

In Europe, the issue of energy sovereignty continues to strengthen the strategic position of nuclear energy. European Commission President von der Leyen emphasized the role of nuclear energy in a statement earlier this month. Sweden’s parliament repealed the uranium mining ban on January 1, 2026, reclassifying uranium as a permitted mineral, while Switzerland’s Senate Committee advanced legislation to lift the moratorium on new nuclear power plant permits. Barclays noted that public attitudes toward nuclear energy in Europe have increasingly shifted to acceptance since the 2022 energy crisis, providing a popular mandate for policy advancement.

Hyperscale Technology Enterprises: Providing Revenue Assurance for Nuclear Energy Development

The explosive growth in AI computing demand has made electricity supply the biggest bottleneck for data center expansion. Hyperscale technology enterprises are providing critical revenue certainty for nuclear projects through long-term power purchase agreements (PPAs) and prepayment mechanisms.

The most significant business development in 2026 is Meta’s modular nuclear procurement strategy. In January, Meta announced agreements with Vistra, TerraPower, and Oklo, potentially supporting up to 6.6 GW of new and existing clean energy capacity. Combined with its earlier PPA with Constellation for the Clinton Clean Energy Center, Meta has established a diversified nuclear procurement portfolio covering operating units, power upgrades, and advanced reactor pipelines.

Notably, Meta’s 20-year PPA with Vistra is particularly noteworthy, covering over 2,600 MW of capacity across three nuclear plants within the PJM grid, including 2,176 MW of existing generation and an additional 433 MW of power upgrades at Perry, Davis-Besse, and Beaver Valley. Vistra stated that this agreement provides certainty for initiating license renewal planning for these three plants.

Meta’s agreement with TerraPower supports the development of up to eight Natrium advanced reactors with a base capacity of 2.8 GW, extendable to 4 GW with energy storage systems, targeting the first units to come online by 2032. TerraPower positions this agreement as a multi-unit deployment pathway rather than a single demonstration project, which Barclays views as crucial for addressing the long-standing challenge of scaling nuclear energy efficiently beyond the first unit. Meta’s agreement with Oklo employs a prepayment mechanism to support the development of a 1.2 GW advanced nuclear energy park in Pike County, Ohio, driving Oklo’s stock price up by 20% on the announcement day.

Additionally, previously signed agreements have begun to translate into actual construction activities. The Hermes 2 project, a collaboration between Kairos Power and Google, broke ground in April at Oak Ridge. This marks the first fourth-generation commercial-scale reactor in the United States to receive a construction permit and will supply up to 50 MW of clean electricity to the Tennessee Valley Authority (TVA) grid. Last week, TerraPower also announced the official commencement of its flagship Natrium project, Kemmerer Unit 1, less than two months after receiving the construction permit from the NRC.

Bottlenecks are easing, but labor issues are becoming increasingly prominent.

Barclays believes the key difference between the current nuclear cycle and previous short-lived booms lies in the fact that some substantive bottlenecks are beginning to be concretely addressed.

Progress in the fuel cycle sector is the most evident. The U.S. Department of Energy's $2.7 billion uranium enrichment support program, combined with the phased implementation of a ban on Russian uranium imports starting in 2028, is driving physical supply growth. Uranium Energy Corp has commenced production at Burke Hollow in Texas, marking the first new in-situ recovery (ISR) uranium mine in the U.S. in over a decade. Canada’s NexGen Rook I project, after receiving final approval in 2026, is also advancing towards commissioning within this decade.

In terms of permitting and project delivery capacity, advanced reactor developers are entering formal permitting queues and commencing construction. Kairos Power’s Hermes 2 equipment modules will be prefabricated at its Albuquerque manufacturing base before being transported to Oak Ridge for modular assembly—a model demonstrating the industry’s efforts to bridge the gap between design ambition and practical delivery.

However, labor is emerging as an increasingly prominent bottleneck. Barclays noted in its report that, compared with advancements in the fuel cycle and permitting areas, labor constraints exhibit deep structural characteristics that are difficult to alleviate in the short term. The core issue does not lie in overall employment levels but rather in the scarcity, geographic concentration, and temporal mismatch of specialized skills—nuclear power, data centers, and power development projects often compete for the same pool of electrical engineers, nuclear specialists, and experienced construction workers.

This issue is most apparent in the United Kingdom. In February this year, EDF announced that the commissioning of the first unit of Hinkley Point C would be delayed by another year to 2030 due to lower-than-expected productivity in electromechanical installation works. Barclays believes that labor shortages are driving up costs, extending construction timelines, and increasing execution risks, potentially becoming the most significant remaining obstacle to determining the pace of the nuclear renaissance.

Editor/Deng