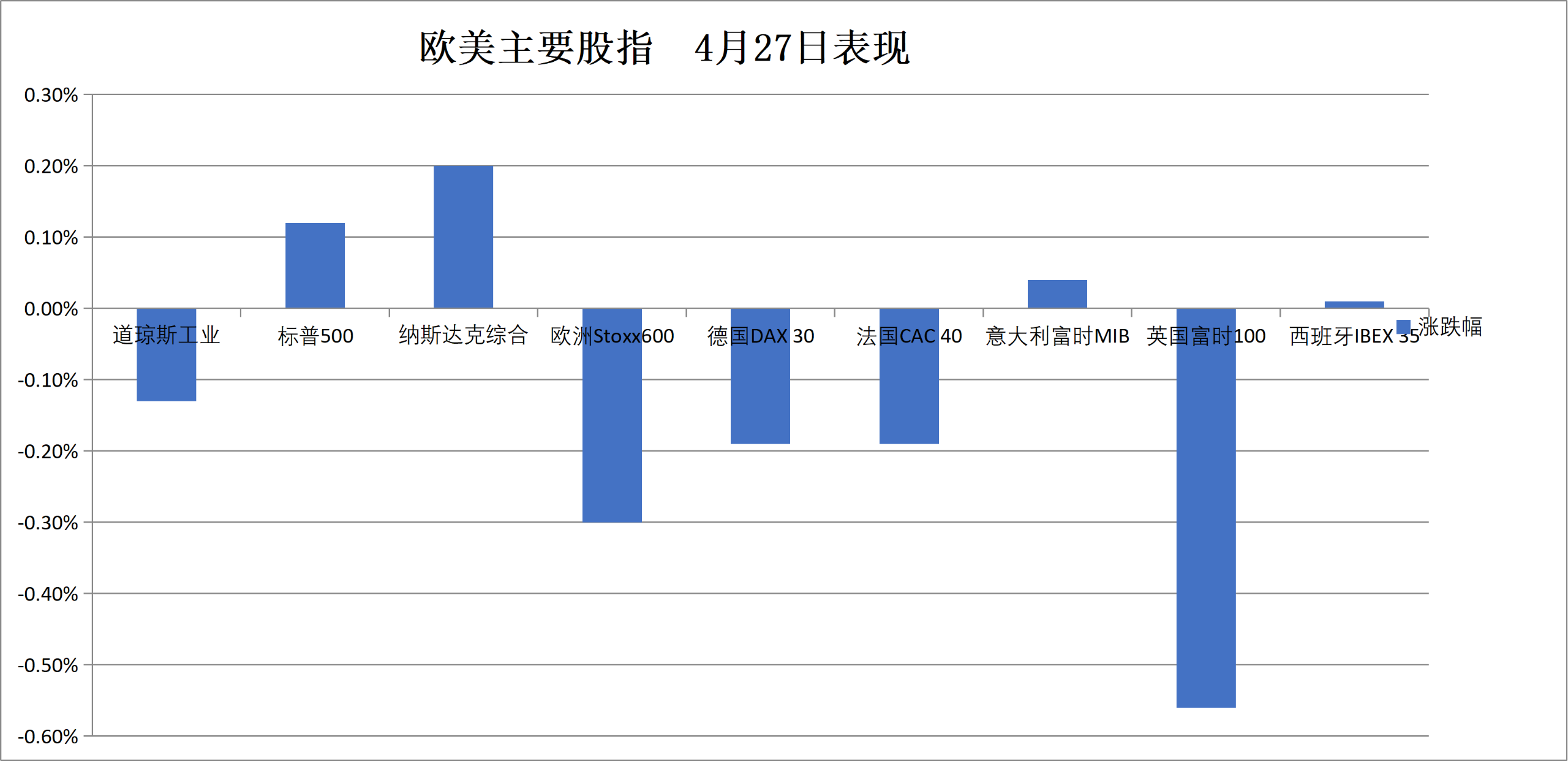

The market sentiment was cautious on Monday, with the S&P 500 edging up 0.1%, the Nasdaq rising 0.2%, and the Dow Jones Industrial Average slipping 0.1%. The semiconductor sector experienced its first decline this month, while the Mag 7 outperformed the broader market. The yield on the 10-year U.S. Treasury note increased by 3 basis points, with longer-dated bonds underperforming shorter-dated ones, showing some correlation with oil price movements. Gold failed to benefit from a softer dollar, closing down 0.6% after trading in a narrow range, at $4,680 per ounce.

U.S. stocks traded narrowly near record highs on Monday as the market remained on hold ahead of a busy week featuring major tech giant earnings reports, the Federal Reserve’s interest rate decision, and the latest developments in the Middle East situation.

Major technology companies are set to release their results this week, with investors closely watching whether artificial intelligence capital expenditures can translate into tangible returns. Meanwhile, the standoff between Iran and the United States over the Strait of Hormuz remains unresolved, keeping oil prices at elevated levels.

On Monday, overall market sentiment leaned toward caution.$S&P 500 Index(.SPX.US)$The index rose slightly by 0.12%, extending its monthly gains and is poised for its best single-month performance since 2020. The Nasdaq and Dow Jones indices underperformed, with the semiconductor sector posting its first decline this month.

On Monday, overall market sentiment leaned toward caution.$S&P 500 Index(.SPX.US)$The index rose slightly by 0.12%, extending its monthly gains and is poised for its best single-month performance since 2020. The Nasdaq and Dow Jones indices underperformed, with the semiconductor sector posting its first decline this month.

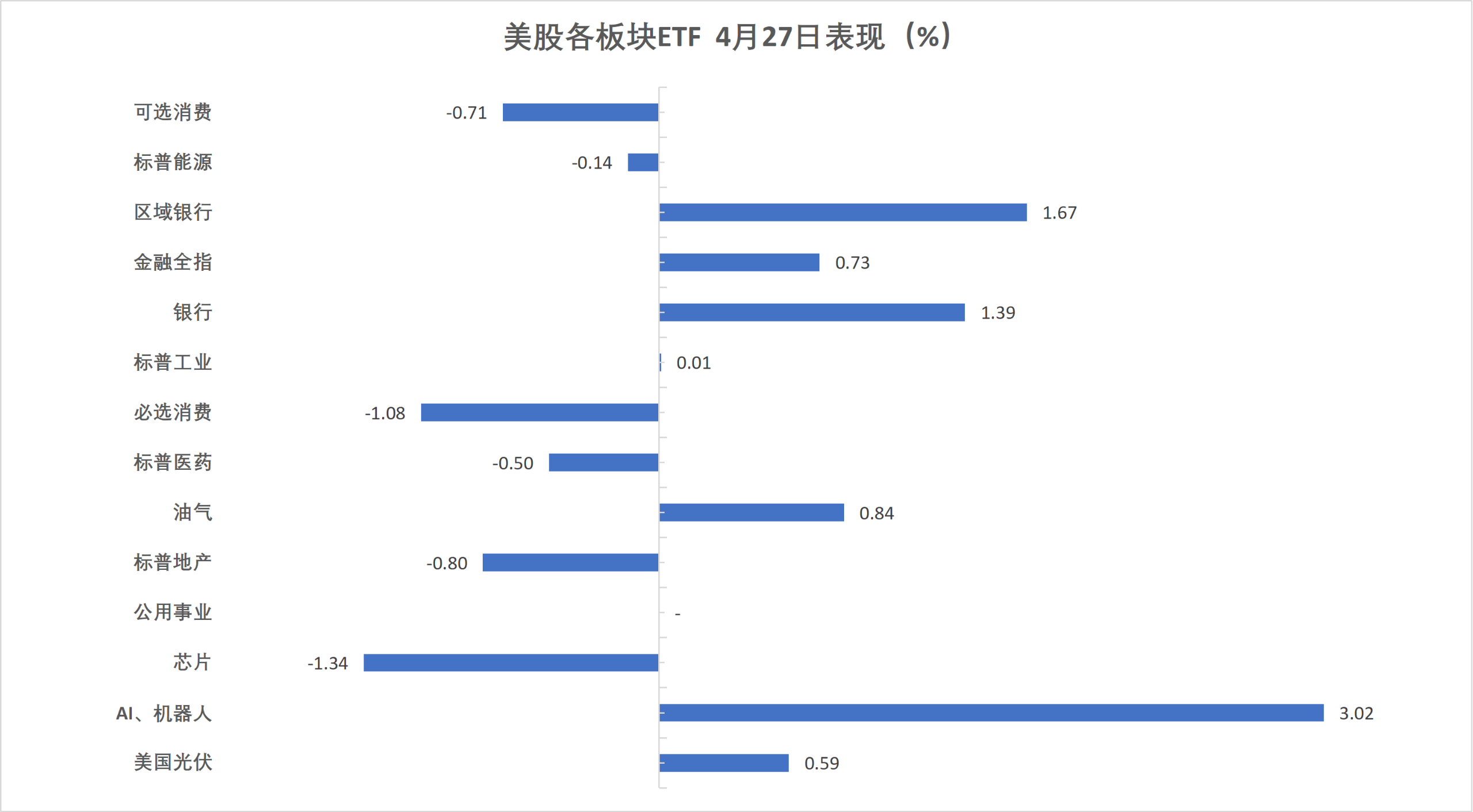

Among the 11 major sectors of the S&P 500 Index, the communication services sector saw the largest increase, while the consumer staples sector recorded the biggest drop. The Mag 7 outperformed the broader S&P 493 Index today.

Options market data showed that a large number of zero-day put options were sold in the late session, suppressing the VIX index. However, analysts noted that this move sharply contrasted with the significant event risks expected later this week.

After the U.S. market closes on Wednesday, Alphabet,Microsoft (MSFT.US)、$Amazon(AMZN.US)$and Meta will release their Q1 earnings reports on the same day, followed by Apple on Thursday. These five companies collectively represent nearly $16 trillion in market value, accounting for approximately 44% of the S&P 500's total market cap, and their financial results will largely determine whether April’s market rally can gain fundamental support.

Senior strategist Louis Navellier stated:

Given the AI-driven market trend, the outlook and capital expenditure plans of the Mag 7 will be crucial to sustaining upward momentum in the market.

Bloomberg macro strategist Kristine Aquino pointed out that the core issue facing investors is whether the substantial AI investments by technology giants have generated quantifiable tangible returns, a key variable that has provided "rather fragile" support for this year's stock market rally.

Goldman Sachs strategist Nelson Armbrust noted that previously high-intensity macro short hedge positions have been significantly unwound, with leverage levels contracting.

Last week, the scale of deleveraging in the U.S. stock market reached its highest level in nearly seven months, and the CTA strategy community has turned net long. However, this also implies that its buying momentum for the S&P 500 has nearly dried up, creating potential resistance for further market gains.

The situation in Iran continues to dominate commodity market movements.

Iran proposed a phased negotiation plan, suggesting the resumption of vessel passage through the Strait of Hormuz on the condition of suspending discussions on nuclear issues. However, subsequent statements from Iranian officials emphasized that their military should retain control over the strait.

U.S. Secretary of State Rubio immediately responded, stating that the United States cannot tolerate Iran normalizing control over the Strait of Hormuz, leading to a further rise in oil prices.

White House Press Secretary Karoline Leavitt stated that Trump has convened national security officials to discuss Iran’s latest proposal but emphasized that the U.S. red line on preventing Iran from acquiring nuclear weapons remains unchanged.

Since early April, the daily average transit volume through the Strait of Hormuz has approached zero, with Brent crude breaking above $108 per barrel and WTI crude rising more than 2%.

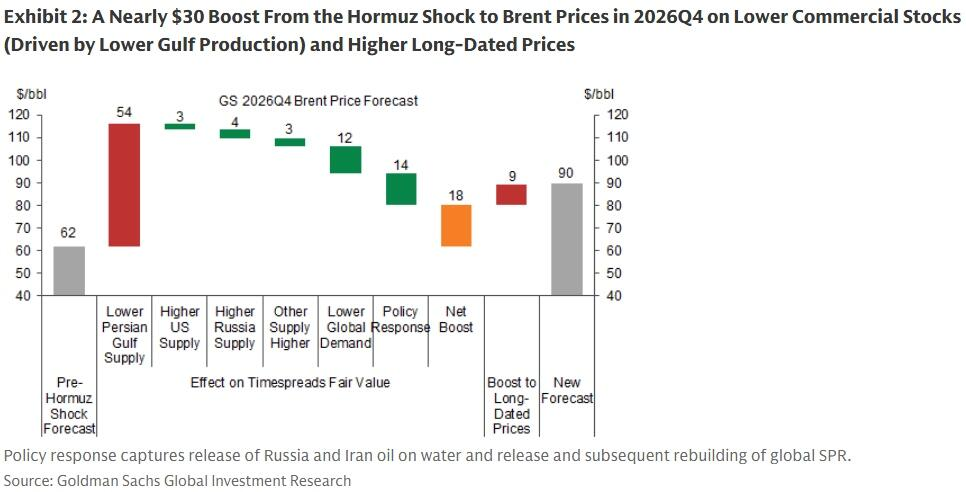

Goldman Sachs commodity analyst Daan Struyven raised the forecast for Brent crude in 2026 to $90 per barrel and projected that global oil demand would decline by 1.7 million barrels per day in the second quarter of 2026 to partially offset an expected production loss of 1.405 million barrels per day from Persian Gulf crude.

Goldman Sachs trader Edoardo Lorenzo Greco additionally warned that the current increase in chemical product costs, both in speed and magnitude, is twice that of the 2022 energy crisis. The frequency of discussions about rising costs and supply chain disruptions in corporate earnings calls has approached the impact levels seen during the 2022 shock, and investors should be alert to second-order effects.

Today, the market's expectation of interest rate cuts in 2026 slightly declined. The yield on 10-year U.S. Treasury bonds increased by 3 basis points, with the long end underperforming the short end, showing some correlation with oil price movements.

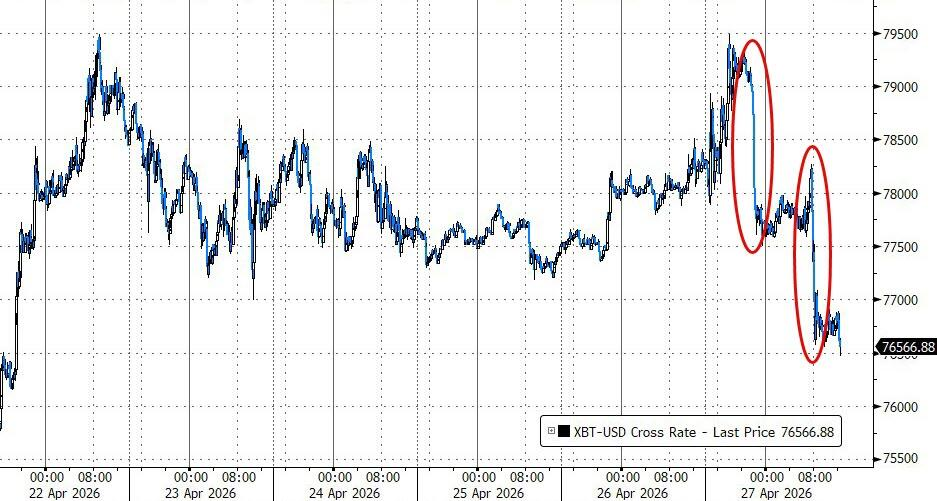

$美元指数(USDindex.FX)$Rebounded after a decline,$Bitcoin (BTC.CC)$The day's decline was the most pronounced, falling from $79,500 to $76,500 at one point, representing a drop of about 1.7%, consistent with the overall rise in risk aversion sentiment.

$黄金/美元(XAUUSD.CFD)$ Failed to benefit from the weakening of the U.S. dollar, closing down 0.6% after narrow-range fluctuations, at $4,680 per ounce.

Market sentiment remained cautious on Monday, with the S&P 500 edging up 0.1%, Nasdaq rising 0.2%, and the Dow Jones Industrial Average slipping 0.1%. The semiconductor sector recorded its first decline this month, while the Mag 7 outperformed the broader market.$NVIDIA(NVDA.US)$Share prices rose by 4.0%.

U.S. benchmark indices:

The S&P 500 Index closed up 8.83 points, or 0.12%, at 6,173.91 points, setting another record high for closing prices.

The Dow Jones Industrial Average fell 62.92 points, or 0.13%, to close at 49,167.79 points.

The Nasdaq Composite Index closed up 50.502 points, or 0.20%, at 24,887.10 points, marking a record high for closing prices for two consecutive trading days.

the Nasdaq 100 Index (.NDX.US)Closed up 2.012 points, or 0.01%, at 27,305.679 points, hitting a record high for closing prices for two consecutive days.

Russell 2000 Index (.RUT.US)Closed up 0.04% at 2788.19 points.

The VIX volatility index closed down 3.63% at 18.03.

U.S. sector ETFs:

U.S. sector ETFs showed mixed performance, with the global airline industry ETF down 1.81%, the consumer staples ETF down 1.07%, the consumer discretionary ETF down 0.72%, and the semiconductor ETF down 0.04%.

Mag 7:

The Wind US Magnificent 7 Index rose 0.97% to 68523.06 points.

NVIDIA surged 4%, and Alphabet A shares climbed 1.72%,$Tesla(TSLA.US)$up 0.6%. Meta gained 0.53%, Microsoft edged up 0.05%, Amazon fell 1.11%, and Apple dropped 1.27%.

Chip Stocks:

Philadelphia Semiconductor Index (.SOX.US)Closing down 1.01%, ending a streak of 18 consecutive daily gains (the longest in history), at 10408.038 points.

Taiwan Semiconductor (TSM.US)ADR rose 0.62%, while AMD declined 3.83%.

Chinese Concept Stocks:

The Nasdaq Golden Dragon China Index closed down 1.20% at 6,868.78 points.

Among popular Chinese stocks,Atour Group (ATAT.US)Closing down 5.4%,$21Vianet (VNET.US)$Dropping 4.2%,Zai Lab (ZLAB.US)、Huazhu Group (HTHT.US)、$Daquan New Energy (DQ.US)$Falling at least 3.5%,$GDS Holdings(GDS.US)$, Bilibili, and Alibaba fell more than 2%.

Other individual stocks:

$Circle(CRCL.US)$Decreasing by 4.21%.

Domino's Pizza shares fell 8.8% after the delivery chain reported first-quarter sales that missed expectations.

Following better-than-expected user growth, the telecommunications company$Verizon(VZ.US)$raised its annual earnings forecast, boosting Verizon's stock price by 1.5%.

Rare-earth concept stocks rally,$Critical Metals(CRML.US)$ Surged over 25%.

The optical communication sector saw a pullback, $POET Technologies(POET.US)$ with a decline of approximately 50%.

The blue-chip index for the Eurozone closed down about 0.4%, led by Siemens Energy which fell more than 5.4%, $ASML Holding(ASML.US)$ while other components dropped nearly 3%. The Dutch stock market closed down over 1.1%, whereas Italy's banking sector rose more than 0.6%, and the UK defense ETF gained 1%.

Pan-European Index:

The European STOXX 600 Index closed down 0.30% at 608.84 points.

The Eurozone STOXX 50 Index closed down 0.39% at 5860.32 points, experiencing an overall rally followed by a pullback, having risen to 5932.33 points at 19:35 Beijing time to refresh its intraday high.

Major Stock Indexes Around the World:

The German DAX 30 Index closed down 0.19% at 24083.53 points.

The French CAC 40 Index closed down 0.19% at 8141.92 points.

$FTSE 100 Index (.FTSE.GB)$closed down 0.56% at 10321.09 points.

Sector and Stock Performance:

Among the blue-chip stocks in the Eurozone, Siemens Energy closed down 5.44%, ASML Holding fell 2.96%, Deutsche Telekom dropped 2.68%, Munich Re declined 1.99%, and Prosus fell 1.84%, ranking fifth in terms of losses.

Among all constituents of the European STOXX 600 Index, Verisure closed down 5.88%, Entain fell 5.44%, tied with Siemens Energy for the second-largest decline, while Aixtron SE dropped 5.15% closely following.

$US 10-Year Treasury Yield (US10Y.BD)$Up by approximately 3.7 basis points. Sovereign bond yields across the Eurozone generally increased.

U.S. Treasuries:

At the New York close, the U.S. 10-year Treasury yield rose 3.69 basis points to 4.3375%.

The two-year Treasury yield climbed 2.10 basis points to 3.7993%; the 30-year Treasury yield increased 3.59 basis points to 4.9420%.

European debt:

At the European market close,$German 10-Year Government Bond Yield (DE10Y.BD)$rose 3.9 basis points to 3.033%, trading within a range of 2.998%-3.040% during the day.

The yield on the UK 10-year government bond (GB10Y.BD)rose by 6.0 basis points to 4.972%.

The average yield on 10-year government bonds in France, Italy, Spain, and Greece increased by 5.0 basis points.

Brent crude oil closed up more than 2.7%.

Crude Oil:

WTI June crude oil futures rose by $1.97, or 2.09%, to close at $96.37 per barrel.

Brent June crude oil futures rose by $2.90, or 2.75%, to close at $108.23 per barrel.

Middle East Abu Dhabi Murban crude oil futures increased by 0.29% to $103.89 per barrel.

Natural Gas:

NYMEX May natural gas futures closed at $2.55 per million British thermal units.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/Liam