According to a disclosure by the Hong Kong Stock Exchange on April 27, GEM Co., Ltd. (referred to as GEM, 002340.SZ) has submitted its listing application for the Main Board of the Hong Kong Stock Exchange again, with JPMorgan, CITIC Securities, and CICC International acting as joint sponsors.

According to Zhitong Finance App, GEM Co., Ltd. (shortened as: GEM, 002340.SZ) has submitted its listing application to the Main Board of the Hong Kong Stock Exchange again as disclosed by HKEX on April 27. JPMorgan, CITIC Securities, and CICC International are its joint sponsors.

Company Profile

As per the prospectus, the company is one of the earliest pioneers in the recycling production of critical metal resources and the lithium-ion battery recycling industry, and it holds a leading position in the new energy materials manufacturing sector. The company employs an urban mining business model to eliminate pollution, regenerate resources, curb global greenhouse effects, advance carbon reduction and carbon neutrality, implement green development concepts, and promote global green transformation.

As per the prospectus, the company is one of the earliest pioneers in the recycling production of critical metal resources and the lithium-ion battery recycling industry, and it holds a leading position in the new energy materials manufacturing sector. The company employs an urban mining business model to eliminate pollution, regenerate resources, curb global greenhouse effects, advance carbon reduction and carbon neutrality, implement green development concepts, and promote global green transformation.

Since its establishment in 2001, the company has developed an integrated business operation model covering the following three core businesses:

Critical Metal Resources: Leveraging its technological advantages, the company engages in the recycling of critical metal resources. Its revenue primarily comes from the sales of nickel, cobalt, and tungsten products widely used as raw materials for battery and alloy production. According to Frost & Sullivan, based on 2025 recycling volumes, the company ranks first in China in terms of nickel, cobalt, and tungsten resource recovery. It is one of the earliest pioneers in the industry to develop nickel, cobalt, and tungsten smelting technologies and apply hydrometallurgical techniques to produce mixed hydroxide precipitate (MHP) and other related intermediates. In 2023, the company began producing MHP and other nickel-based metal products and completed the construction of the world’s largest autoclave for laterite nickel ore. In collaboration with industrial partners, the company spearheaded the establishment of a production base in Indonesia, which has an annual MHP production capacity of 150,000 tons. Based on equity production in 2025, the company ranks among the top three globally.

Lithium-Ion Battery and End-of-Life Vehicle Recycling: The company recycles batteries from third parties and end-of-life electric vehicles (EVs), generating revenue through the sale of (i) reused batteries; (ii) metal intermediates for battery production (e.g., black powder, lithium phosphate, lithium iron phosphate, and lithium carbonate). The company also generates revenue by selling metal products recovered from end-of-life vehicles (e.g., steel, aluminum, and copper). To date, the company has established cooperative relationships with over 1,100 automotive enterprises and battery manufacturers worldwide and has set up six lithium-ion battery recycling subsidiaries in China, all of which have been included in the White List of the Ministry of Industry and Information Technology (MIIT). According to Frost & Sullivan, based on 2025 recycling volumes, the company ranks first domestically in the third-party retired lithium-ion battery recycling sector.

New Energy Materials: Revenue from the company’s new energy materials business mainly comes from the production and sale of (i) ternary precursors for lithium battery production; (ii) cobalt tetroxide for 3C battery production; and (iii) cathode materials for lithium battery production. The company has established long-term and stable cooperative relationships with nine of the top ten lithium-ion battery companies globally. According to Frost & Sullivan, based on 2025 shipment volumes, the company ranks third globally in ternary precursor supply and second globally in cobalt tetroxide supply. Additionally, leveraging the refined intermediate production capacity formed by its capabilities in mixed hydroxide precipitate (MHP) production, critical metal resource recycling, and lithium-ion battery recycling, the company has achieved self-sufficiency in some key raw materials required for new energy material production. During the performance record period, the company's revenue mainly came from its new energy materials business.

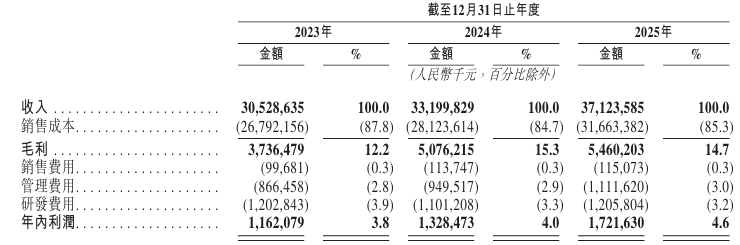

Financial Information

Revenue

In 2023, 2024, and 2025, the company's revenues were approximately RMB 30.529 billion, RMB 33.2 billion, and RMB 37.124 billion, respectively.

Profit

In 2023, 2024, and 2025, the company's annual profits were approximately RMB 1.162 billion, RMB 1.328 billion, and RMB 1.722 billion, respectively.

Gross profit margin

In 2023, 2024, and 2025, the company's gross profit margins were 12.2%, 15.3%, and 14.7%, respectively.

Industry Overview

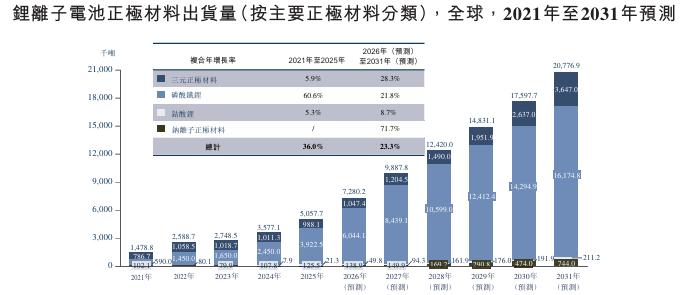

The demand for key new energy metals continues to grow with the expansion of new energy applications. According to Frost & Sullivan, China’s nickel demand is expected to rise from 354,600 tons of metal content in 2026 to 1,296,100 tons of metal content in 2031, with recycled nickel accounting for 32.1% of total demand. China’s cobalt demand is projected to increase from 112,900 tons of metal content in 2026 to 371,700 tons of metal content in 2031, and the share of recycled cobalt in total demand is expected to reach 36.5%. China’s tungsten demand is anticipated to grow from 117,300 tons of metal content in 2026 to 160,100 tons of metal content in 2031, with recycled tungsten expected to account for 42.0% of total supply by 2031. Driven by environmental policies and resource security policies, the recycling of critical metals will become increasingly important.

The rapid development of the electric vehicle and 3C electronics industries has driven the continuous growth in the use of lithium-ion batteries, leading to an increasing number of retired lithium-ion batteries and creating significant opportunities for recycling businesses. According to Frost & Sullivan, the number of retired electric vehicle batteries in China is expected to grow at a compound annual growth rate (CAGR) of 53.6% from 2026 to 2031. By 2031, it is anticipated that approximately 15% of the nickel, cobalt, and lithium required for the production of new electric vehicle batteries will be supplied through recycling.

According to Frost & Sullivan, the cathode materials for lithium-ion batteries are expected to increase from 7.28 million tons in 2026 to 20.78 million tons in 2031, representing a CAGR of 23.3% from 2026 to 2031. In terms of shipment volume, the precursors for ternary materials are projected to grow from 996.2 kilotons in 2026 to 3,472.2 kilotons in 2031, with a CAGR of 28.4% during the same period. Driven by the demand for extended range in electric vehicles, as well as new requirements for high-nickel and high-voltage products from low-altitude aircraft and humanoid robots, the penetration rate of high-nickel ternary precursors is expected to increase significantly in the coming years. The demand for tricobalt tetraoxide is projected to grow steadily, reaching 200.6 kilotons in shipment volume by 2031, with a CAGR of 8.7% from 2026 to 2031. In the future, the development of ternary precursors and tricobalt tetraoxide will be driven by their core downstream industries, including electric vehicles and 3C electronics, as well as emerging applications such as low-altitude aircraft and humanoid robots.

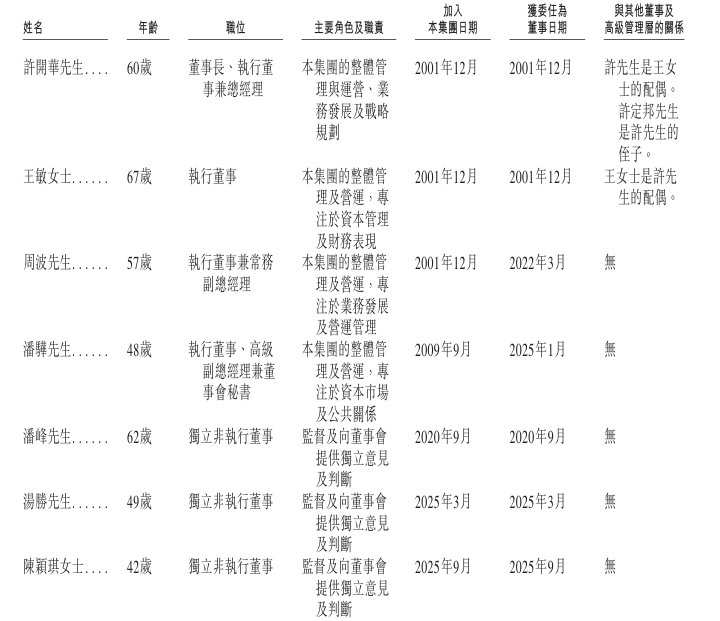

Board of Directors Information

The board of directors consists of seven members, including four executive directors and three independent non-executive directors. All directors are elected by the shareholders' meeting for a term of three years and are eligible for re-election. According to relevant laws and regulations in China, independent non-executive directors may not serve consecutive terms exceeding six years.

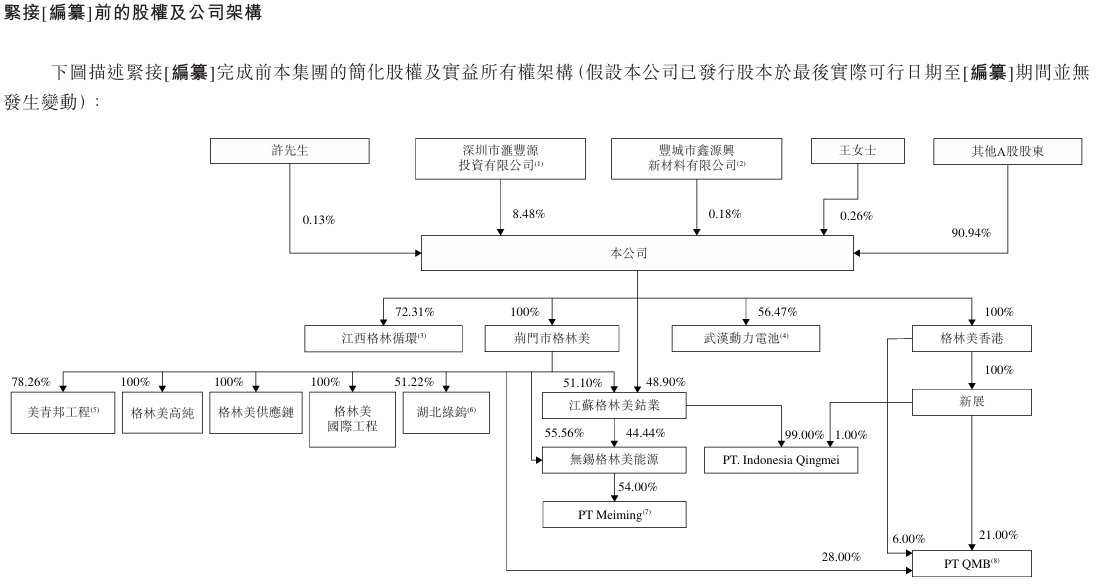

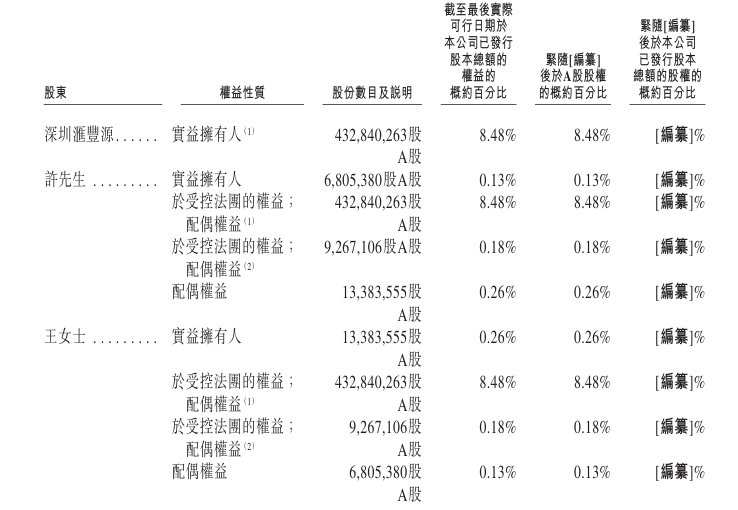

Equity Structure

After the compilation, Mr. Xu, Ms. Wang, Shenzhen Hui Feng Yuan, and Fengcheng Xin Yuan Xing constitute the single largest shareholder group.

Intermediary team

Joint sponsors: J.P. Morgan Securities (Far East) Limited, CITIC Securities (Hong Kong) Co., Ltd., CICC (International) Financing Co., Ltd.;

Legal advisors: Clifford Chance, Guangdong Junxin Jinglun Junhou Law Firm, Santoso, Martinus & Muliawan Advocates, Hogan Lovells;

Joint sponsors and compilation legal advisors: Linklaters, Jingtian & Gongcheng Law Firm;

Independent auditor and reporting accountant: Grant Thornton (Hong Kong) Accountants Limited;

Transfer pricing advisor: Grant Thornton (Beijing) Tax Consultants Co., Ltd. Shenzhen Branch;

Industry Advisor: Frost & Sullivan (Beijing) Consulting Co., Ltd. Shanghai Branch.