Morgan Stanley warned of a turning point for the technology sector in 2026: the first half of the year will continue to benefit from AI capital expenditure and rising commodity prices, but in the second half, cost inflation will begin to 'crowd out' demand. Global semiconductor revenue this year is projected to reach $1.6 trillion, while the adequacy rate of HBM supply will be compressed to 2%. The next bottleneck may shift to more upstream sectors such as EUV. Agent AI will redefine CPU valuations, with segments like memory and ABF substrates facing repricing; however, consumer electronics will come under pressure, and the rollout of edge AI may be delayed.

AI has not 'lost momentum,' but the tech rally in 2026 is unlikely to remain smooth sailing.

Morgan Stanley's annual outlook breaks the rhythm into two phases: the first half will continue benefiting from AI capital expenditures and rising commodity prices; the real challenge will come in the second half, when rising costs will begin to test demand, and 'price elasticity' will push some end markets back.

Morgan Stanley research analyst Shawn Kim wrote in the latest report that the first half will continue the main theme of AI infrastructure investment seen in 2025, with memory prices remaining strong. In the second half, the pass-through of foundry, packaging and testing, and memory costs will compress profit margins for consumer electronics and IC design companies, while the proliferation of edge AI in smartphones and PCs will be delayed due to skyrocketing BOM costs.

Morgan Stanley research analyst Shawn Kim wrote in the latest report that the first half will continue the main theme of AI infrastructure investment seen in 2025, with memory prices remaining strong. In the second half, the pass-through of foundry, packaging and testing, and memory costs will compress profit margins for consumer electronics and IC design companies, while the proliferation of edge AI in smartphones and PCs will be delayed due to skyrocketing BOM costs.

For semiconductors, the report’s forecast is quite aggressive: global semiconductor revenue is expected to reach $1.6 trillion in 2026, with a projected year-on-year growth rate of approximately 96%. If this narrative holds, capital will favor sectors that can 'outperform consensus' while being at critical bottlenecks—memory, advanced foundries, front-end equipment, packaging and testing, and key materials will all be repriced.

Another underlying theme is Agentic AI (intelligent agents). As AI moves from 'generation' to 'autonomous action,' system bottlenecks will shift from simply stacking GPUs to longer chains involving CPU orchestration, memory, and packaging/substrates. Stock selection will no longer rely solely on 'the hottest AI' but resemble a barbell strategy: one side focuses on pricing power and bottleneck assets, while the other allocates space for overlooked companies with strong cash flow and reasonable valuations to hedge against potential volatility.

$1.6 Trillion Semiconductor Market: This Cycle Goes Beyond GPUs, Extending Leadership to Memory, Foundries, and Equipment

The leadership of AI-related stocks is continuing to expand from logic chips, commodity memory, and semiconductor equipment to a broader industrial chain. The logic here is: as the AI investment cycle is perceived to be 'longer and more structural,' pullbacks present a window to reassess entry points—provided you are buying into bottlenecks rather than hype.

At the same time, it maintains a neutral overall stance: valuations in the AI chain are high, so selections must be more stringent; by comparison, non-AI sectors may offer greater room for valuation recovery—but only if leading AI companies do not have 'undiscovered new drivers.'

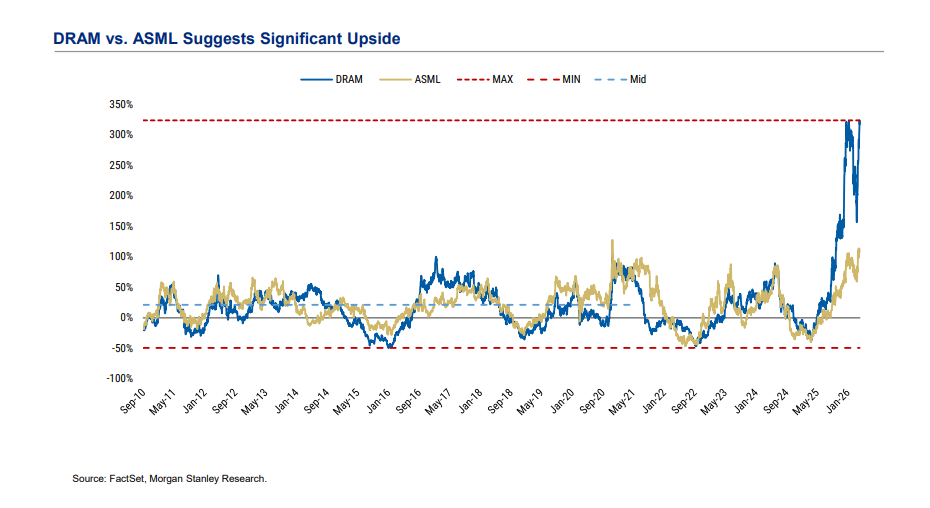

Memory Returns to Center Stage: Record High Prices + Supply Constraints, HBM Remains the Hardest Bottleneck

In terms of memory, DRAM prices are expected to break historical highs, and 'record-high prices' often correspond to 'record-high stock prices,' with stronger profitability support this time around. It also highlights an unusual phenomenon: a significant mismatch between contract and spot prices, reflecting extraordinary supply-demand tensions.

HBM represents a more direct bottleneck. Based on supply chain estimates: the HBM market size will grow from approximately $3 billion in 2023 to about $51 billion in 2026 and $72 billion in 2027; meanwhile, under assumptions of capacity, yield, and utilization, HBM supply 'adequacy' will be compressed to extremely low levels, approximately 2%, by 2026. The conclusion is clear: as long as AI inference demand persists, the 'supply-driven cycle' for memory will accelerate aggressively, with both prices and capital expenditures becoming more aggressive.

It further extends its vision: if this tight constraint persists, an "unprecedented" capex may emerge around 2028, potentially pushing the next bottleneck to even more upstream segments such as EUV, benefiting the semiconductor equipment chain once again.

Shifting bottlenecks: advanced foundry, front-end equipment, and packaging/testing will benefit from the "second wave."

As AI continues to scale up and constraints in memory and packaging deepen, the beneficiaries will shift from "single-point explosions" to "rotating bottlenecks." It focuses on several key areas within the semiconductor sector:

Advanced process foundry: AI demand supports TSMC in maintaining a compound annual revenue growth rate of approximately 20% over the next five years, with potential incremental opportunities arising from AI GPU foundry services in China.

Front-end equipment (SPE): The strength in back-end AI-related equipment remains, but front-end equipment will accelerate again by the second half of 2026, driven by demand for advanced logic and DRAM. Companies with high DRAM exposure and those benefiting from advanced node expansion are preferred.

Packaging and testing (OSAT): AI demand is further tightening packaging and testing capacity. While Taiwan-based back-end manufacturers benefit, it also implies that "supply bottlenecks" will become more normalized.

Agentic AI: CPU becomes the new bottleneck, transforming the "hardware war" into a "collaborative war."

Agentic AI represents a transition from "generation" to "autonomous action": the critical factor is not just stronger computing power, but how systems coordinate and allocate resources. Using architectural diagrams, it highlights the orchestrating role of CPUs and provides estimates: by 2030, Agentic AI could create a CPU incremental opportunity worth $32.5 billion to $60 billion, along with 15-45 EB of additional DRAM demand.

This will change the way markets monitor performance: while GPUs remain important, the ceiling may be determined by any weak link in the "collaborative chain," including CPUs, memory, substrates, equipment, and foundries—weak links will rotate.

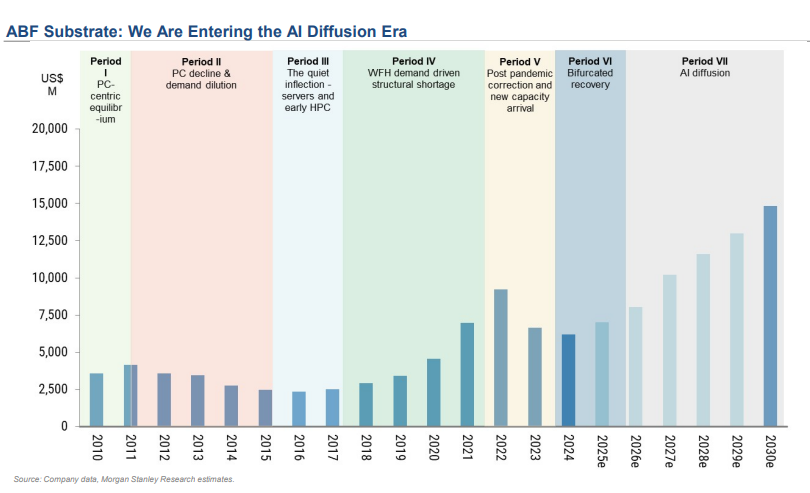

The supply-demand inflection point for ABF substrates is imminent—with a persistent shortage expected to begin in 2027. The tight supply of T-glass substrates may even extend to 2028. The share of ABF demand from AI GPUs/ASICs and networking boards is projected to rise from approximately 18% in 2020 to over 75% by 2030.

The logic for MLCC is more straightforward: the MLCC content per AI server is more than 20 times that of a regular server—approximately USD 230 for HGX Hopper, while for the GB200 NVL72 rack system, it reaches as high as USD 4,635. Current MLCC inventories are at historically low levels, and demand is accelerating. Regarding thermal management, Q2 2026 is projected to set a new quarterly shipment record for thermal management companies, with liquid cooling penetration rates continuously rising; AVC is considered the preferred choice.

2026’s turning point lies in the second half of the year: cost-driven inflation will force 'demand destruction.'

The report directly points to 'technology inflation' as the risk factor for the second half of the year. Rising costs in wafer fabrication, outsourced semiconductor assembly and testing (OSAT), and memory will cascade pressure down to original equipment manufacturers and chip design firms. End-users may not be able to fully pass on price increases, leading to squeezed demand and thinner profit margins.

Its outlook for 'edge AI' is relatively cautious: Edge AI computing upgrades for smartphones and PCs may be significantly delayed due to higher input costs. For segments heavily reliant on consumer electronics shipments and with weaker pricing power, the second half of 2026 presents a more challenging environment.

Even under bearish scenarios, the situation remains clear: the initial phase often involves overinvestment and overconsumption, followed by a more rational period. Spending without a clear objective will repeatedly raise doubts about return on investment. Additionally, nearing the 'power wall' and financial constraints will slow deployment. Combined with the counterbalancing forces of 'pricing power from rising costs' and 'compressed downstream profits,' industry divergence will become more pronounced.

On the hardware side, regarding AI server demand, NVIDIA's GPU server rack shipments are expected to increase to approximately 75,000 units in 2026, significantly higher than around 29,000 units in 2025. Correspondingly, the logic of 'increased component content' for ABF substrates, MLCCs, and thermal solutions remains valid, and it is believed that ABF substrates may re-enter a tight supply state after 2027.

However, the keywords for smartphones and PCs have shifted to 'cost.' The smartphone industry in 2026 will be weighed down by rising component costs, putting pressure on profit margins. PC OEM/ODM manufacturers may also experience several quarters of margin compression due to rising memory prices. In other words, although both fall under the category of 'hardware,' the beneficiaries have changed: the closer to data centers, the smoother the path; the closer to consumer electronics, the tougher the environment.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/joryn