The core issue in the market is not the strength of demand—demand is clearly robust—but whether capital expenditure can increase further. If capital expenditure remains flat amid rising input costs, this would effectively amount to a slowdown, directly challenging the prevailing narrative around the AI market.

One of the most intensive earnings report weeks in history has arrived, and the narrative surrounding AI capital expenditure is facing a critical stress test.

This Wednesday, $Alphabet-A (GOOGL.US)$ 、$Microsoft (MSFT.US)$、$Amazon (AMZN.US)$、 $Meta Platforms (META.US)$ will simultaneously release their Q1 earnings reports, $Apple (AAPL.US)$ followed by disclosures on Thursday. Current consensus expectations have already fully priced in a combined capital expenditure exceeding $600 billion for these four companies in 2026.

Rich Privorotsky, head of Goldman Sachs' Delta One, pointed out that the core issue for the market is not the strength or weakness of demand—demand is evidently robust—but whether capital expenditure can be further increased. If capital expenditure remains flat amid persistently rising input costs, this would essentially equate to a slowdown, directly challenging the prevailing AI market narrative.

Rich Privorotsky, head of Goldman Sachs' Delta One, pointed out that the core issue for the market is not the strength or weakness of demand—demand is evidently robust—but whether capital expenditure can be further increased. If capital expenditure remains flat amid persistently rising input costs, this would essentially equate to a slowdown, directly challenging the prevailing AI market narrative.

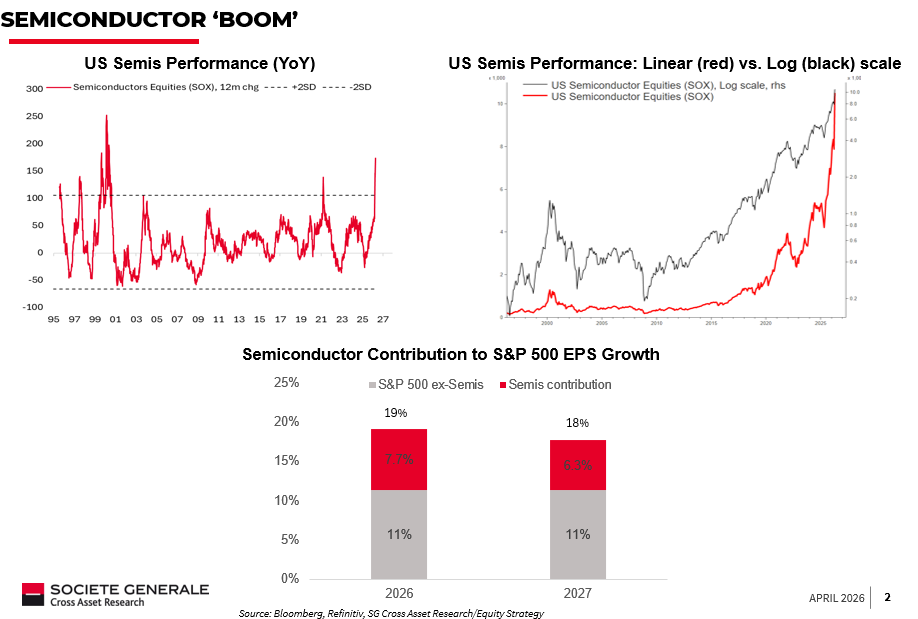

In this market structure dominated by AI capital expenditure logic, semiconductors have become the most direct beneficiaries, with the sector surging 42% year-to-date, far outpacing the approximately 2% increase of the Mag 7 as a whole; excluding $NVIDIA (NVDA.US)$, the Mag 7's year-to-date increase is only about 0.2%. However, Goldman Sachs has also cautioned that the upside surprises brought by AI spending are "almost the entire game," and the semiconductor sector's valuation has risen to a price-to-earnings ratio of 60x, with the risk-reward ratio deteriorating and technical indicators shifting from tailwinds to headwinds.

Capital Expenditure Expectations: Consensus Fully Priced In

The tech industry’s current race for computing power is giving rise to what Goldman Sachs calls the "Token Maxing" effect: engineering teams across major companies are competing to consume as much computing power as possible, fostering a distorted incentive where "under-spending equals career risk," driving firms to aggressively spend even if inefficiently.

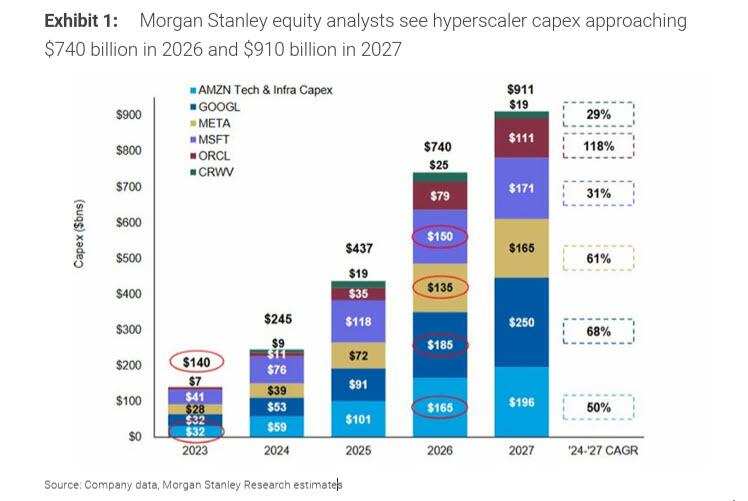

Leading tech stocks have committed to a combined AI capital expenditure exceeding $740 billion by 2026. The current consensus forecast has already incorporated over $600 billion in capital expenditure by Amazon, Microsoft, Meta, and Alphabet into models by 2026. Meanwhile, constraints have spread across multiple areas: shortages in electricity, CPUs, GPUs, copper materials, and even engineering talent have emerged.

Goldman Sachs noted that it is hard to argue against the fundamentals at present: "Supply constraints across multiple verticals, accelerating earnings per share growth, and the market narrative (whether right or wrong) is that we are on the cusp of the most significant technological breakthrough in decades." However, the market is indefinitely extrapolating upside potential—more computing power, higher intelligence, until the eventual realization of Artificial General Intelligence (AGI)—and this week's earnings reports will provide crucial insight into these expectations.

Semiconductors: Rally Reaches Critical Zone

The rally in the semiconductor sector has evolved into a self-reinforcing cycle: expectations and prices drive each other, shifting the market dynamic from "fundamentally supported" to "self-fulfilling." The sector's price-to-earnings ratio has surged to 60x, with panic-driven buying sentiment continuously building. Goldman Sachs believes this is the zone where "convexity risks are beginning to emerge"—parabolic rallies always have an endpoint.

Within the sector, the leading force has quietly shifted. CPUs and analog chips have become the main drivers, while GPUs, which usually lead the rally, will lag relatively. Goldman Sachs judges that the current breakout "appears to be an upward breakout, but the trading characteristics resemble a short squeeze"—positions, capital flows, and forced buying are collectively pushing the market to chase right-tail risks.

From the perspective of earnings contributions, $Micron Technology (MU.US)$ one company alone accounted for more than half of the total upward revision in S&P 500 earnings per share recently. Its quarterly results and guidance far exceeded consensus expectations, and market expectations of "unbounded demand" for AI memory chips have nearly doubled consensus valuations. The breadth of upward revisions in S&P 500 earnings is narrowing, with little change in consensus expectations for median firms, making the extreme concentration of earnings momentum an undeniable fact.

Hyperscale cloud vendors: Shareholder logic shows divergence

Semiconductor stocks and hyperscale cloud vendor stocks are showing starkly different market reactions to the same wave of capital expenditure. A misalignment of interests between the two types of investors is coming to light. Rich Privorotsky stated bluntly that semiconductor stocks exhibit strong enthusiasm for capital expenditure growth—after all, these expenditures flow directly into their pockets; however, shareholders of hyperscale cloud vendors have historically not benefited from increased capital spending.

"Last week, we heard from suppliers (semiconductor companies), and this week it’s the spenders’ turn (hyperscale cloud vendors). The latter’s narrative is much more complex," Rich Privorotsky remarked.

This divergence has already been clearly reflected in the year-to-date market performance: The overall gain of Mag 7 was only about 2%, nearly flat when excluding NVIDIA, forming a striking contrast with the 42% rise in the semiconductor sector. Hyperscale cloud vendors are undertaking substantial capital investments in the AI era, but significant uncertainty remains regarding when and how these investments will translate into shareholder returns.

Corporate buybacks: Structural demand provides bottom support

Amidst a challenging market sentiment, U.S. corporate stock buybacks are providing a layer of structural cushioning for the stock market. The scale of buyback authorizations has reached record highs, quiet periods are ending successively, and total corporate buyback demand this year is expected to exceed $1 trillion.

This buying is price-insensitive and represents pure structural demand—companies are aggressively repurchasing shares at historical highs, continuously reducing outstanding shares, and mechanically boosting earnings per share. For the currently high-flying stock market, this is a passive support force that cannot be ignored.

Market landscape: Non-AI supply chains are outsiders

Rich Privorotsky's assessment of the overall market risk-reward has become increasingly cautious: "It is hard not to respect the strength of AI-driven capital, but the speed of this rally has been extreme. Almost all of the anticipated upside surprises are entirely attributed to AI spending — that is the entire game."

Beyond the AI narrative, crude oil and refined product prices are capturing market attention, with European equities lagging behind, and market divergence reaching an extreme. Goldman Sachs summarized: "You are either part of the AI supply chain, or you are not participating in this rally. From the current position, the risk-reward has deteriorated, and technical factors are shifting from tailwinds to headwinds."

This concentration trend also extends to emerging markets: semiconductor-driven profit growth is reshaping the structure of the entire emerging market landscape, making EM more concentrated rather than diversified. For global investors, regardless of the market they operate in, the distinction between being inside or outside the AI supply chain is increasingly becoming the most critical determinant of returns.

Editor/joryn