The three major U.S. stock indexes closed lower on Tuesday.Philadelphia Semiconductor Index (.SOX.US)The decline was approximately 3.6%, marking the second consecutive day of retreat from record closing highs.$Oracle(ORCL.US)$Stock prices fell by 4.1%,CoreWeave (CRWV.US)while yields on two-year U.S. Treasury bonds rose by 5.6 basis points. Gold prices plummeted by 1.8%, breaching the $4,600 level. WTI crude oil futures surged 3.69%, reaching their highest level since April 13.

The narrative around AI investment is undergoing a stress test, with U.S. technology stocks leading the declines. Oil prices climbed to wartime highs amid renewed inflation concerns, driving up U.S. Treasury yields.

Sources familiar with the matter revealed that Sarah Friar, Chief Financial Officer of OpenAI, has expressed concerns to other senior executives about the company's ability to cover future data center contract costs if revenue growth does not accelerate sufficiently.

Dennis Follmer, Chief Investment Officer at Montis Financial, stated that any issues involving AI-related demand or capital expenditure budgets could prompt the market to reassess gains made over the past month, adding, "The critical question for investors is whether the AI-driven momentum can continue to propel the market forward."

OpenAI has fallen short of internal targets in terms of weekly active users and revenue. Market participants are concerned that this may undermine the rationale supporting large-scale spending on AI infrastructure by tech giants.

U.S. stocks retreated from record highs on Tuesday, with technology shares experiencing significant declines. Chipmakers and AI-related concept stocks were hit hardest, as the Nasdaq Composite Index dropped 0.9% and the semiconductor index plunged 3.6%.

OpenAI subsequently issued a statement asserting that its consumer and enterprise businesses are "fully operational," but the market reaction remains difficult to quell. Oracle’s stock price fell by 4.1%, while CoreWeave declined by 5.8%. Both companies are deeply integrated into OpenAI's cloud computing initiatives.

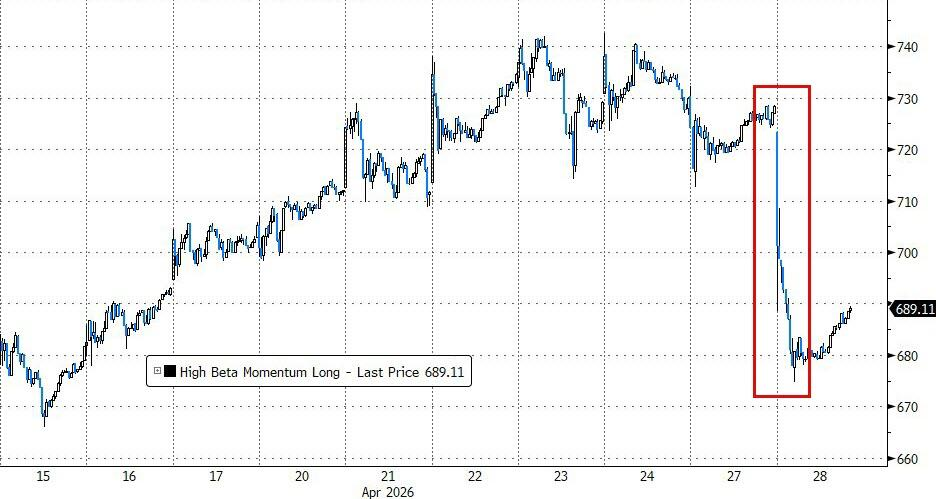

According to data from Goldman Sachs' trading division, this was the second-worst trading day for momentum factors so far this year. High-beta momentum portfolios, primarily exposed to AI-related stocks, suffered a significant setback, marking the second-worst performance day of the year.

Chuck Carlson, CEO of Horizon Investment Services, stated:

The situation with OpenAI has prompted investors to reassess whether growth is slowing and what that implies for capital expenditures.

Dennis Follmer of Montis Financial also pointed out:

The most critical question for investors is whether the AI-driven momentum can continue to propel the market forward.

Notably, Alphabet,Microsoft (MSFT.US)、$Amazon(AMZN.US)$Meta, and Apple are set to release their earnings reports in the next two days. The combined market capitalization of these companies accounts for approximately 44% of the S&P 500. Any commentary on the scale of AI spending and return on investment is expected to directly influence current market sentiment.

On the geopolitical front, Trump mentioned on social media that Iran had requested the U.S. to lift its naval blockade of this key shipping channel and reopen it as soon as possible. According to reports, Pakistani mediators anticipate Tehran will submit a revised proposal within days.

However, Trump subsequently expressed dissatisfaction with Iran's latest peace proposal, citing delays in nuclear negotiations, which significantly dampened expectations for a short-term resolution to the conflict. Iranian officials claimed they could 'outlast Trump,' suggesting the situation might escalate into a prolonged stalemate.

On Tuesday, WTI crude oil futures closed 3.69% higher at $99.93 per barrel, reaching the highest level since April 13. Brent crude oil futures rose by 2.80%, settling at $111.26 per barrel.

Notably, the UAE announced its withdrawal from OPEC and OPEC+ effective May 1, with plans to gradually increase oil production. The statement briefly caused oil prices to retreat before quickly recovering their losses.

Analysts warn that as OPEC's ability to adjust supply imbalances diminishes, volatility in the oil market is expected to intensify further. However, Salih Yilmaz, senior analyst at Bloomberg Intelligence, noted:

In the short term, the focus of the paper market will remain on tensions in the Strait of Hormuz and tight physical flows. Only after the channel reopens will market attention shift back to fundamentals.

The surge in energy prices has also pressured the bond market, with a poor tail performance in the 7-year U.S. Treasury auction exacerbating the trend.

Short-term U.S. Treasury yields rose, while the 10-year yield remained largely unchanged at 4.34%. In a research note, Ian Lyngen, head of U.S. rates strategy at BMO Capital Markets, wrote:

Persistently rising energy prices are dominating the direction of U.S. interest rates, with crude oil prices approaching the threshold for triggering inflation concerns.

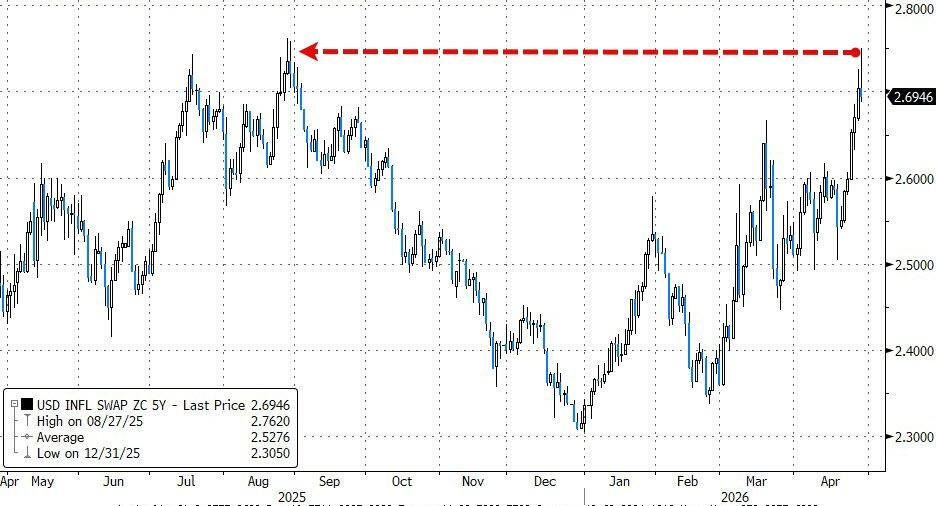

The U.S. five-year inflation swap rate, which typically represents the expected average CPI rate over that period, exceeded 2.7% for the first time since August 2025.

Meanwhile, market pricing for a 2026 rate cut has been significantly compressed, with investors seeing only a one-in-six chance of a 25-basis-point reduction.

This week’s monetary policy meeting is likely Powell’s last as chair, with rates expected to remain unchanged. The focus will be on the wording of the policy statement and Powell’s characterization of energy-driven inflation during the press conference.

Oliver Pursche, senior vice president at Wealthspire Advisors, stated:

The key question the market needs to consider is whether persistently high oil prices will lead to inflation being viewed as non-transitory, thereby forcing the Federal Reserve to raise interest rates.

At the asset correlation level, the US dollar closed slightly higher amid fluctuations, with the Bloomberg Dollar Spot Index rising by 0.2%.

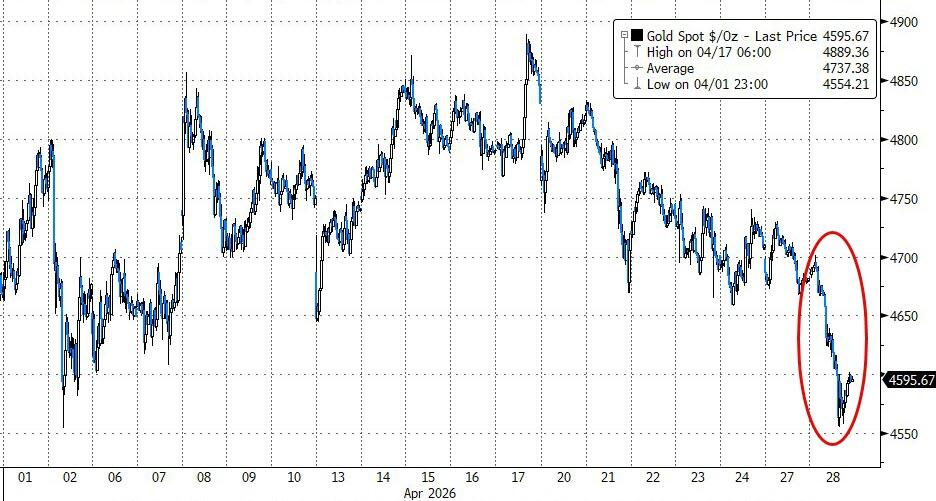

Gold prices fell by 1.8%, breaking below the $4,600 mark. Rich Privorotsky of Goldman Sachs previously commented that gold now acts like an 'ATM machine for energy companies.'

On Tuesday, the three major U.S. stock indexes closed lower, with the Philadelphia Semiconductor Index falling approximately 3.6%, retreating from its all-time closing high for two consecutive days. The Nasdaq Technology Index dropped more than 1.3%. The China Concept Index fell about 0.5%, and CQQQ declined over 1.7%.

U.S. benchmark indices:

$S&P 500 Index(.SPX.US)$Closed down 35.11 points, or 0.49%, at 7,138.80 points.

The Dow Jones Industrial Average closed down 25.86 points, or 0.05%, at 49,141.93 points.

The Nasdaq Composite closed down 223.301 points, or 0.90%, marking its largest single-day decline since March 27, at 24,663.799 points.the Nasdaq 100 Index (.NDX.US)Closed down 276.667 points, or 1.01%, at 27,029.012 points.

Russell 2000 Index (.RUT.US)Closed down 1.15% at 2,756.051 points.

The VIX volatility index, often referred to as the 'fear gauge,' closed down 1.05% at 17.83. It hit an intraday high of 19.43 at 20:31 Beijing time before declining steadily.

U.S. sector ETFs:

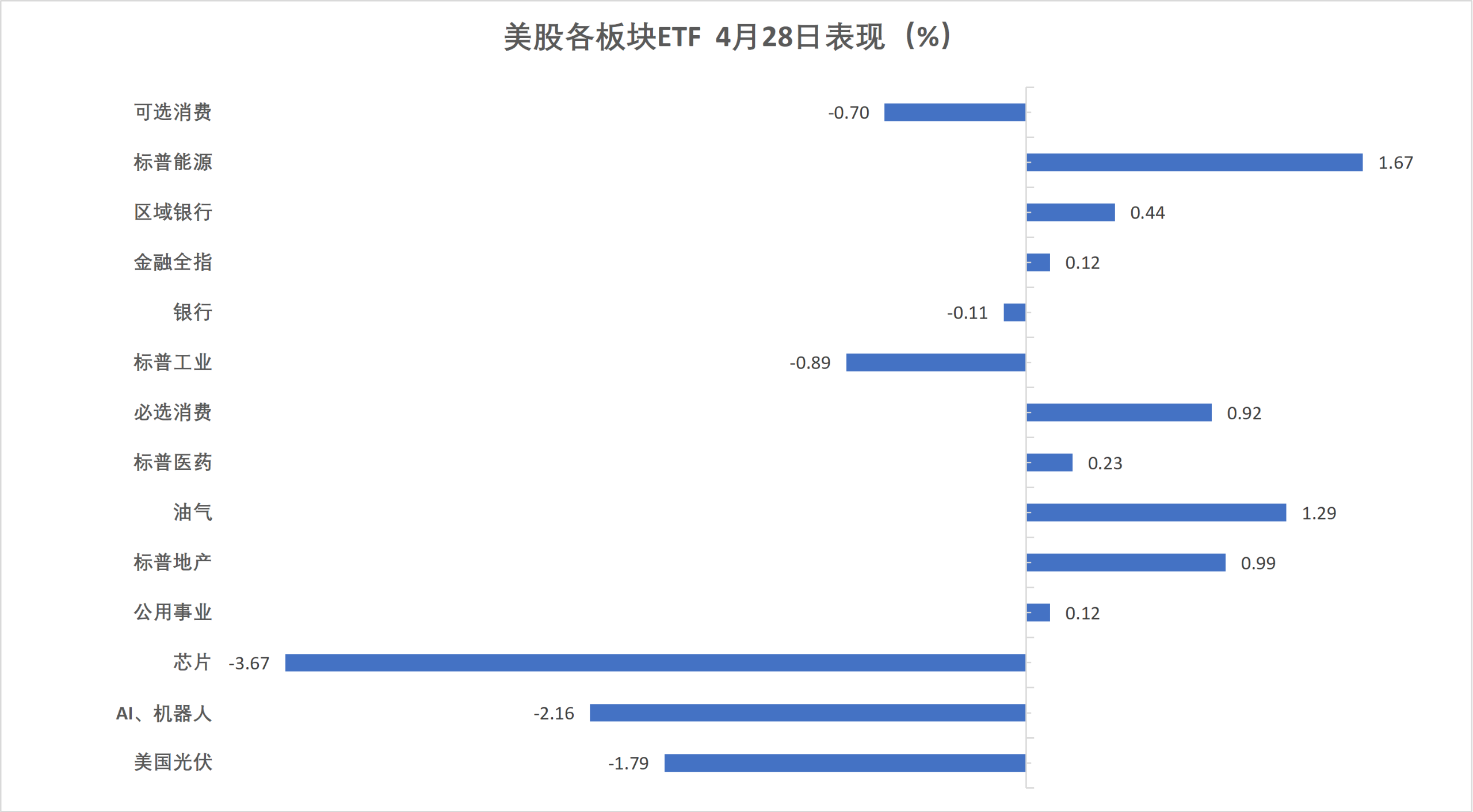

The U.S. sector ETFs showed mixed performance, with the semiconductor ETF closing down 2.97%, and the global technology stock index ETF, technology sector ETF, and internet stock index ETF declining between 1.81% and 0.98%.

Mag 7:

The Wind U.S. Magnificent 7 Index fell by 0.27%.

$NVIDIA(NVDA.US)$Declined by 1.63%, Meta fell by 1.07%,$Tesla(TSLA.US)$Dropped by 0.7%, Amazon declined by 0.54%, Google A fell by 0.15%, Microsoft rose by 1.04%, and Apple increased by 1.16%.

Chip Stocks:

The Philadelphia Semiconductor Index closed down 3.58% at 10,035.578 points.

Taiwan Semiconductor (TSM.US)ADR dropped by 3.16%, and AMD fell by 3.41%.

Chinese Concept Stocks:

The Nasdaq Golden Dragon China Index closed down 0.49% at 6,835.31 points, gradually recovering losses after a gap-down opening.

Among popular Chinese ADRs, Kingsoft Cloud (KC.US)Closed down 6.4%,$GDS Holdings(GDS.US)$Dropped by 4.8%,$21Vianet (VNET.US)$Dropped by 3.7%, Xiaomi fell by 3.3%, and XPeng dropped by 2.6%, $BYD (ADR) (BYDDY.US)$ Fell by 2.3%, Alibaba,$PDD Holdings (PDD.US)$Dropped by 1.2%.

Other individual stocks:

$Circle(CRCL.US)$Fell by 1.14%.

Corning (GLW.US) Corning (an Apple supplier) closed down 8.9%, marking its largest single-day drop since April 2025.

Precious metals, semiconductor equipment and materials, and memory-related stocks led the declines, with Arm falling nearly 8%,$SanDisk (SNDK.US)$dropping over 6%,$Coeur Mining (CDE.US)$、$Pan American Silver (PAAS.US)$Fell more than 5%,$Dell Technologies (DELL.US)$dropped by more than 4%,$ASML Holding(ASML.US)$、$Micron Technology(MU.US)$And AMD fell more than 3%. Oil and gas, as well as coal sectors, performed strongly.$Chevron(CVX.US)$、$Exxon Mobil(XOM.US)$rose over 1%,Occidental Petroleum (OXY.US)Surged over 2%.

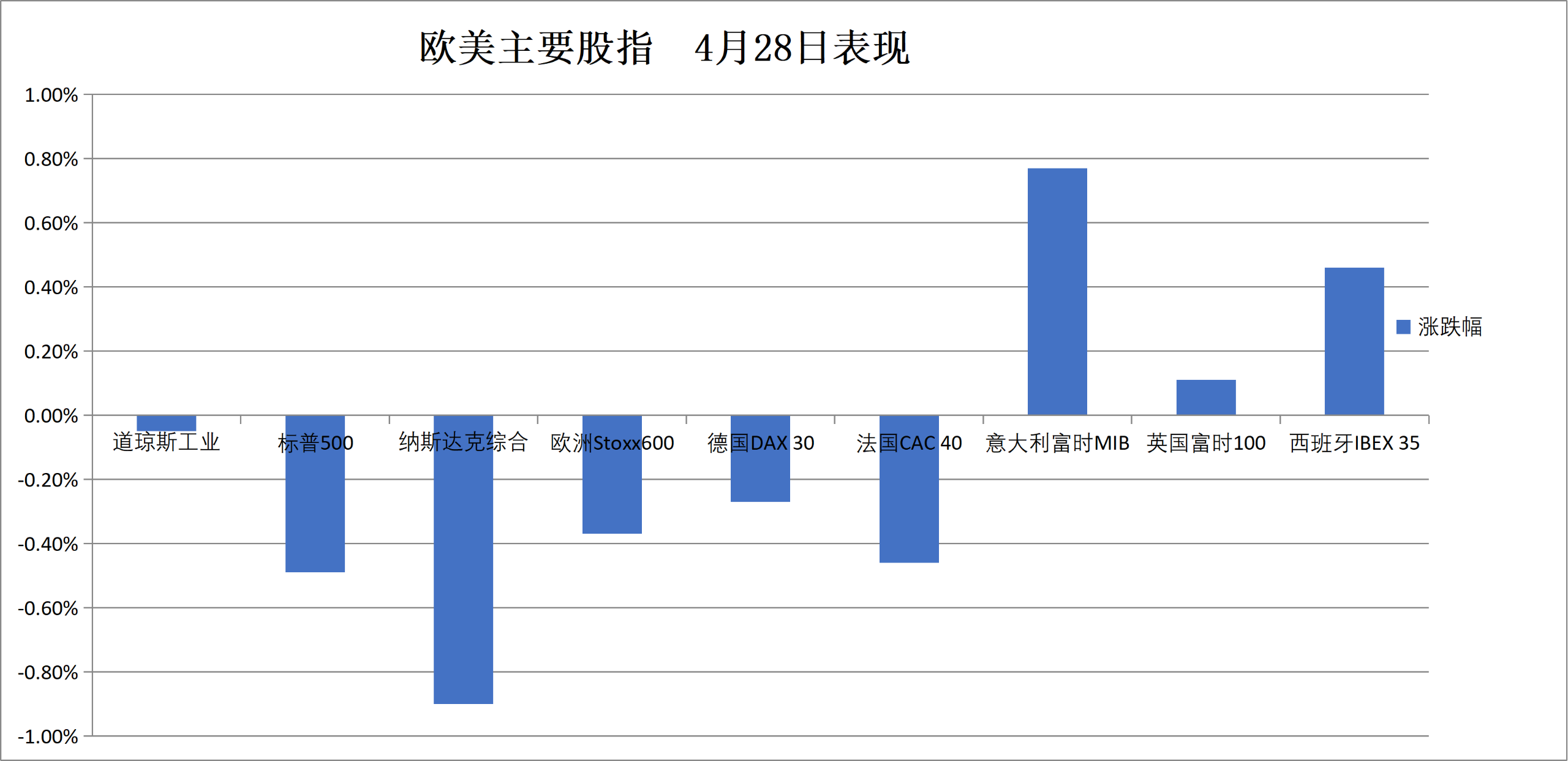

European stock markets closed down approximately 0.4%, with Bayer falling about 4.6% and ASML Holding declining over 3.3%. The Dutch stock market closed nearly 0.8% lower, while Italy's banking sector rose more than 1.7%.

Pan-European stocks:

The European STOXX 600 Index closed down 0.37% at 606.58 points.

The Eurozone STOXX 50 Index closed down 0.41% at 5836.10 points.

Major Stock Indexes Around the World:

The German DAX 30 Index closed down 0.27% at 24018.26 points.

The French CAC 40 Index closed down 0.46% at 8104.09 points.

$FTSE 100 Index (.FTSE.GB)$It closed up 0.11% at 10332.79 points.

Sector and Stock Performance:

Among the blue-chip stocks in the Eurozone, Bayer closed down 4.59%, ASML Holding fell 3.36%, Air Liquide dropped 3.20%, LVMH Group declined 2.72% as the fourth-largest drop, and Hermès fell 2.14%.

Among all the components of the European STOXX 600 Index, Germany's Qiagen closed down 10.76%, Valmet Corporation fell 8.53%, and FDJ United dropped 7.81% as the third-largest decline.

The yield on the two-year U.S. Treasury note rose by approximately 4.3 basis points. The yield on the two-year German government bond increased by about 8 basis points.

U.S. Treasuries:

In late New York trading,$US 10-Year Treasury Yield (US10Y.BD)$rose by 1.20 basis points to 4.3515%.

The yield on the two-year U.S. Treasury note rose by 4.29 basis points to 3.8401%, while the yield on the 30-year U.S. Treasury bond fell by 0.41 basis points to 4.9420%.

European debt:

At the European market close,$German 10-Year Government Bond Yield (DE10Y.BD)$rose by 3.4 basis points to 3.067%, trading within a range of 3.048%-3.086% during the session, remaining in an upward trend throughout the day.

The yield on the UK 10-year government bond (GB10Y.BD)rose by 3.4 basis points, while the yield on the two-year British government bond increased by 5.5 basis points.

$The yield on the 10-year French government bond (FR10Y.BD)$rose by 3.8 basis points, while the yield on the two-year French government bond climbed by 8.0 basis points.

The Abu Dhabi Murban crude oil futures in the Middle East rose by 2.91% to $107.22 per barrel.

Crude Oil:

WTI crude oil futures for June delivery closed up $3.56, or 3.69%, at $99.93 per barrel.

Brent crude oil futures for June closed up $3.03, or 2.80%, at $111.26 per barrel.

The Abu Dhabi Murban crude oil futures in the Middle East rose by 2.91% to $107.22 per barrel.

Natural Gas:

NYMEX natural gas futures for May settled at $2.5590 per million British thermal units.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/Liam