The two strongest-performing IPO stocks in the Hong Kong stock market — Zhilv and MiniMax — would have reduced the year-to-date loss of the Hang Seng Tech Index by 5 percentage points if they had been included since their listing. Both are expected to be added to the index on June 8, with a combined weight of 5%-7%, bringing approximately $1.25 billion to $1.75 billion in passive fund inflows. The Stock Connect program for Hong Kong stocks will also gradually open. However, the real stress test will come in July during the lock-up expiration period: Zhilv faces a 5.83% lock-up expiration, while MiniMax has nearly 50% of its shares unlocked, putting liquidity premiums to the test.

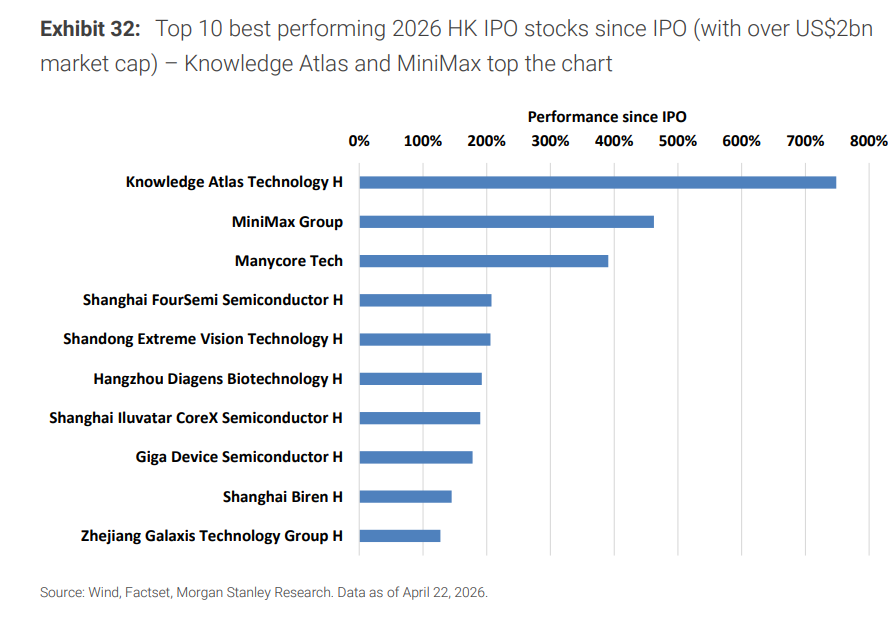

Since the beginning of this year, the Hang Seng Tech Index has fallen more than 10% year-to-date, showing sluggish performance. However, coincidentally, the two best-performing new stocks in Hong Kong's market this year are two large AI model companies —— $KNOWLEDGE ATLAS (02513.HK)$and$MINIMAX-W (00100.HK)$ , with their gains since listing ranking among the top two IPO stocks in Hong Kong in 2026.

The issue, however, is that these two companies are not yet included in the Hang Seng Tech Index. The reason is simple: their listing period is too short to meet the inclusion criteria. Currently, it is expected that both Zhipu and MiniMax will pass the $Hang Seng TECH Index (800700.HK)$ June review and be officially included on June 8, 2026, with a combined weight of approximately 5%-7%.

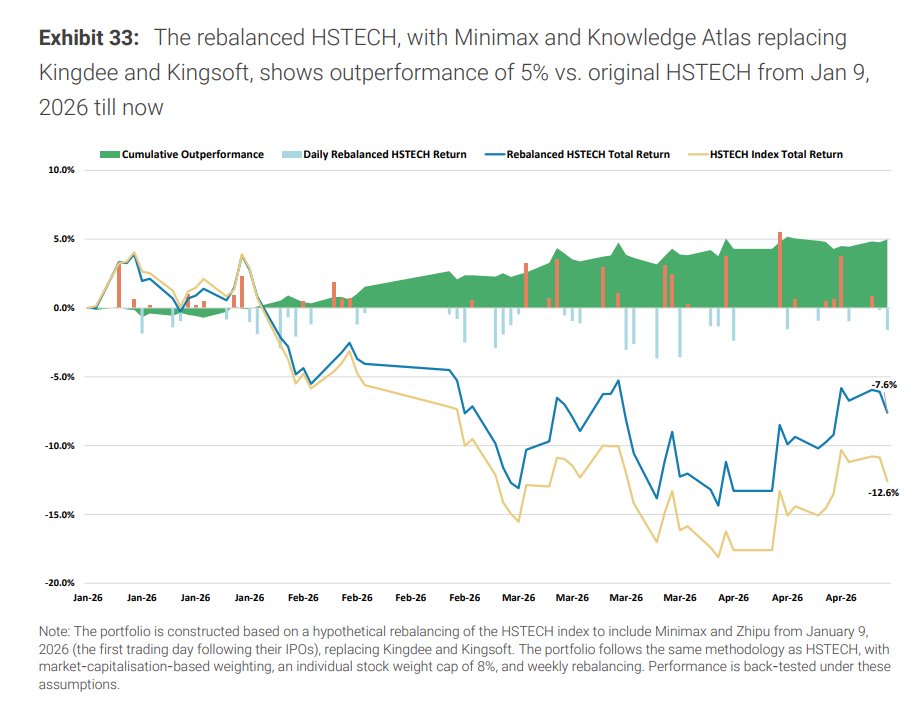

According to information from the Wind Trading Platform, Morgan Stanley analysts estimated in their latest research that if Knowledge Atlas and MiniMax had been included in the Hang Seng Tech Index on their listing day, the index’s year-to-date decline would have narrowed from -12.6% to -7.6%.

According to information from the Wind Trading Platform, Morgan Stanley analysts estimated in their latest research that if Knowledge Atlas and MiniMax had been included in the Hang Seng Tech Index on their listing day, the index’s year-to-date decline would have narrowed from -12.6% to -7.6%.

However, the real stress test will be the wave of share lock-up expirations starting in July: 5.83% of Knowledge Atlas’s cornerstone investors’ shares will be unlocked, while nearly 50% of MiniMax’s shares will be released, leading to a sudden multiple-fold increase in tradable shares, which will put significant pressure on the premium attributed to stock scarcity.

Has the Hang Seng Tech Index 'gone off track'?

Year-to-date, the Hang Seng Tech Index has fallen by double digits. On the surface, this is related to geopolitical tensions in the Middle East and the contraction of global risk appetite.

Analysts pointed out that the current structure of the Hang Seng Tech Index shows that the e-commerce sector ( $BABA-W (09988.HK)$ 、 $MEITUAN-W (03690.HK)$ 、 $JD-SW (09618.HK)$ 、 $TRIP.COM-S (09961.HK)$ 、 $TONGCHENGTRAVEL (00780.HK)$ ) accounts for 25.4% of the index weight, while the automobile/new energy vehicle sector ( $BYD COMPANY (01211.HK)$ 、 $XIAOMI-W (01810.HK)$ 、 $NIO-SW (09866.HK)$ 、 $XPENG-W (09868.HK)$ 、 $LI AUTO-W (02015.HK)$ 、 $LEAPMOTOR (09863.HK)$ ) accounts for 25.1%, with the two sectors combined exceeding 50%.

In other words, half of the index’s weight is actually tied to consumption and travel. Meanwhile, the 'absence effect' of ByteDance continues to ferment.

If Knowledge Atlas and MiniMax had entered the index earlier, this year’s loss would have been reduced by 5 percentage points

Analysts conducted a hypothetical calculation: If Knowledge Atlas and MiniMax had been included in the Hang Seng Tech Index on January 9 (the first trading day after listing), replacing the two smallest-weighted constituents—Kingdee International and Kingsoft Software—the index’s year-to-date total return would have improved from -12.6% to -7.6%, an increase of approximately 5 percentage points.

These five percentage points are sufficient to offset the pullback triggered by ByteDance’s DouBao and JiMeng gaining significant popularity around the Chinese New Year period (mid-to-late February).

The significance of this estimation goes beyond the hypothetical—it directly points to an imminent reality: these two companies are about to enter the market.

June 8: Zhipu and MiniMax both included in the Hang Seng Tech Index

Currently, it is expected that both Zhipu and MiniMax will pass the June review of the Hang Seng Tech Index and be officially included on June 8, 2026, with a combined weight of approximately 5%-7%.

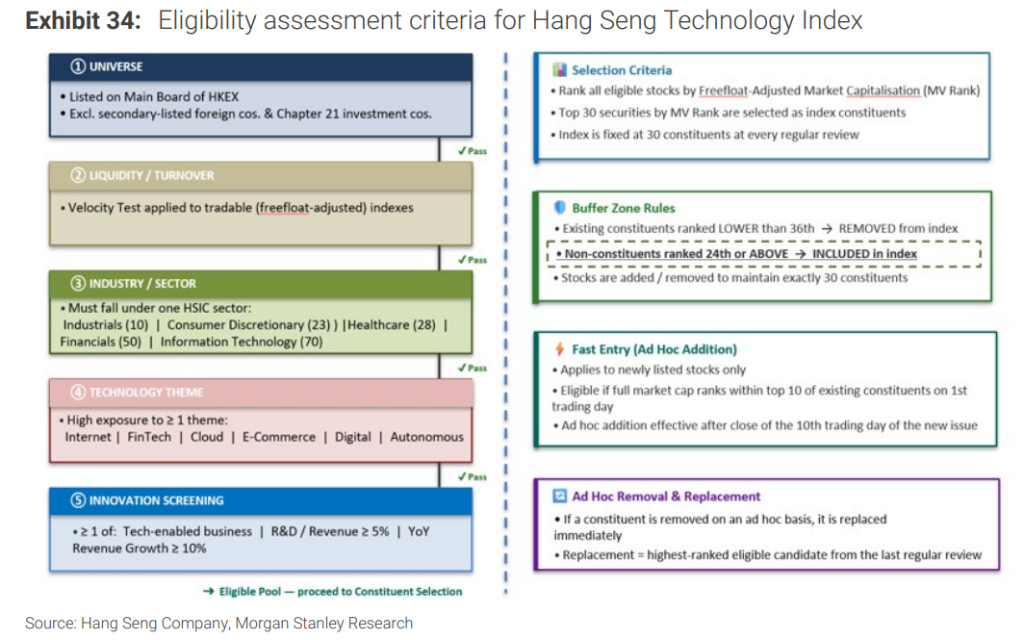

The Hang Seng Tech Index maintains a fixed composition of 30 stocks, with an upper limit of 8% weight per stock. When new members enter, it means some existing ones must exit. According to the rules, non-component stocks must rank 24th or higher to be included. The stock currently with the smallest weight, $KINGDEE INT'L (00268.HK)$and$KINGSOFT (03888.HK)$ , will most likely be replaced.

The direct impact of being included in the index is mandatory buying by passive funds. Data shows that the scale of ETFs and passive products tracking the Hang Seng Tech Index is approximately $25 billion.

Based on a weight of 5%-7%, Zhipu and MiniMax are expected to receive an inflow of approximately $1.25 billion to $1.75 billion from passive funds.

H-share Connect opening: Zhipu in June, MiniMax to wait until August

Beyond inclusion in the Hang Seng Tech Index, another major source of capital inflow is the H-share Connect (southbound funds).

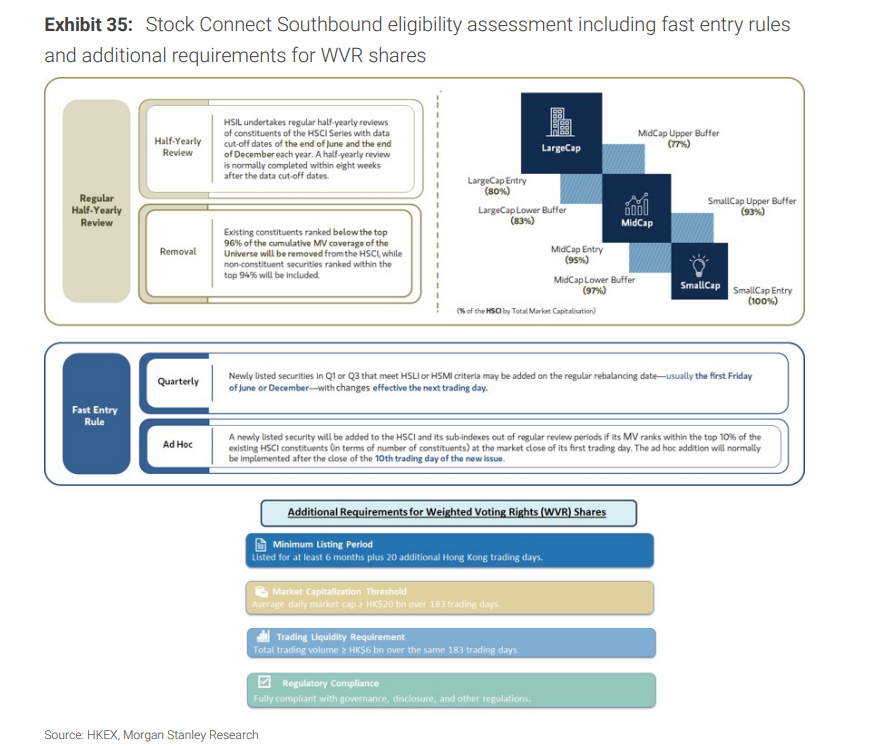

Morgan Stanley expects that Zhipu will be simultaneously included in the H-share Connect on June 8, 2026; MiniMax, due to its adoption of the WVR (weighted voting rights) structure, must meet additional requirements—being listed for at least six months and 20 trading days, with an average daily market capitalization of no less than HKD 20 billion over the past 183 trading days and a total trading volume of no less than HKD 6 billion during the same period—and is expected to become eligible earliest on August 6, 2026.

The time difference between the two reflects the Hong Kong Stock Exchange's stricter governance review of companies with dual-class share structures.

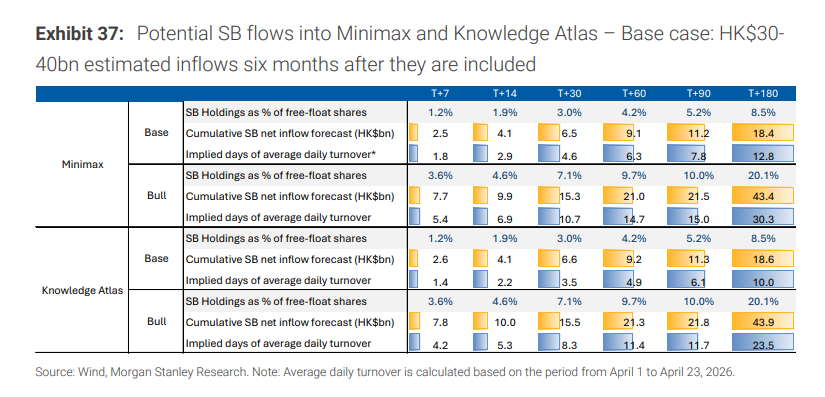

How much capital can southbound trading bring?

The report systematically reviews changes in southbound holdings after major historical internet and technology companies were included in the Stock Connect program. Data shows that, on average, six months after inclusion, southbound holdings rose to approximately 9% of the free float of the relevant companies; for companies with smaller free floats, this percentage tends to be higher.

Based on this, forecasts for two scenarios are provided:

Base scenario (southbound holdings reach 8%-9% of the free float):

MiniMax: Cumulative southbound net inflows of approximately HKD 18.4 billion within 180 days after inclusion, equivalent to about 12.8 days of its average daily trading volume as of April 2026.

Zhipu: Cumulative southbound net inflows of approximately HKD 18.6 billion, equivalent to about 10 days of average daily trading volume.

Optimistic scenario (referring to small free-float new stocks like Horizonrobot, with southbound holdings rising to approximately 20%):

MiniMax: Cumulative southbound net inflows of approximately HKD 43.4 billion, equivalent to about 30 days of average daily trading volume.

Zhipu: Cumulative southbound net inflows of approximately HKD 43.9 billion, equivalent to about 23.5 days of average daily trading volume.

Under the base scenario, Southbound funds for the two stocks are estimated to reach approximately HKD 37 billion, while under the optimistic scenario, they approach nearly HKD 88 billion.

Given the extreme scarcity of similar investment targets in the current Hong Kong and A-share markets, the inflow of capital following the inclusion of these two stocks will provide support for their share prices and valuations, while also boosting broader market sentiment and participation from both institutional and retail investors.

The real pressure test lies in the lifting of lock-up restrictions.

While expectations of capital inflows are optimistic, the other side of the coin cannot be ignored.

Currently, the free float of the two companies is extremely small: Zhipu’s actual free float rate is only about 2.67%, while MiniMax’s is approximately 5.44%. Over 90% of their shares remain locked up. This means that the current share price is formed on a very limited number of tradable shares, reflecting a noticeable liquidity premium.

There are two key time nodes:

First hurdle: July 7/8, 2026 (approximately six months after listing) – 5.83% of Zhipu’s cornerstone investor-held shares will be unlocked; for MiniMax, around 44.29% of existing shareholders (with a six-month lock-up period) and 5.34% of cornerstone shares will be released, totaling nearly 50% of the company’s shares. At that point, the number of tradable shares in the market will suddenly increase several-fold, marking the first reversal in supply and demand dynamics.

Second hurdle: January 2027 (approximately 12 months after listing) – Primarily impacting Zhipu, over 60% of shares held by non-controlling shareholders will be unlocked, leading to a concentrated release of monetization needs from early investors and employees.

At that time, the market pricing logic will shift from “scarcity premium” back to fundamentals: revenue growth rate, the pace of narrowing losses, and the effectiveness of commercial implementation will all become critical benchmarks.

Based on current financial data, the pressure on the two companies is significant. Zhipu’s revenue for the first half of 2025 was RMB 191 million, with R&D expenditures reaching RMB 1.594 billion, implying an R&D investment of approximately RMB 8 for every RMB 1 of revenue. For MiniMax, revenue for the first nine months of 2025 was USD 53.44 million, with R&D expenditures at USD 180 million, indicating an R&D investment of roughly USD 3.37 for every USD 1 of revenue.

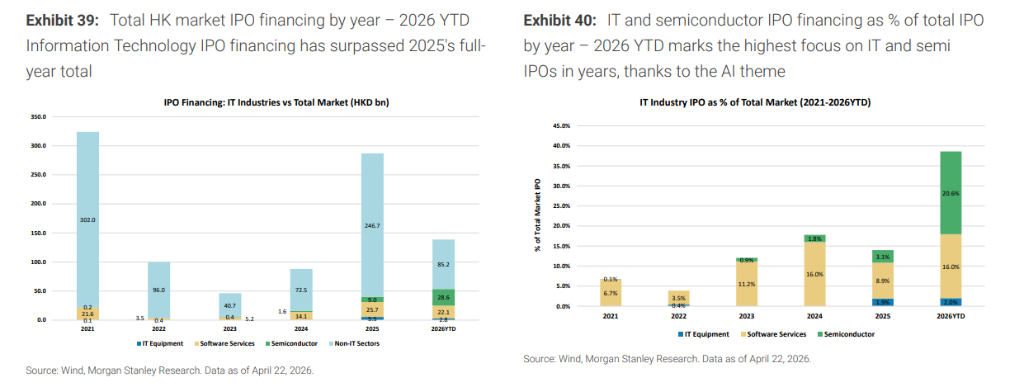

The Hong Kong stock IPO market is being reshaped by AI.

The listings of Zhipu and MiniMax are not isolated events but epitomize a larger structural shift.

As of 2026, the total amount raised through IPOs on the Hong Kong stock market has reached HKD 139 billion, approximately 50% of the total for the whole of 2025. Of this, the IT sector accounted for HKD 54 billion in IPO proceeds, representing 39% of the total, surpassing the HKD 40 billion for the entire IT sector in 2025 and seeing its share rise sharply from 14% in 2025. The semiconductor sector was particularly prominent, with its share of total proceeds rising from 3% in 2025 to 21%.

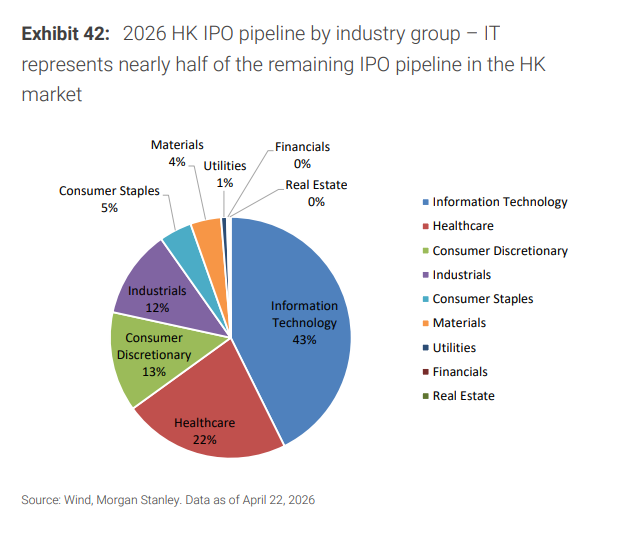

In terms of the IPO pipeline, information technology accounts for about 43% of the approximately 390 companies currently queued for listing in Hong Kong stocks, healthcare represents 22%, and consumer goods account for 13%.

Behind this shift is clear policy impetus. In September 2024, the Hong Kong Stock Exchange (HKEX) and the Securities and Futures Commission (SFC) lowered the minimum market capitalization threshold under Chapter 18C (for specialized technology companies)—from HKD 6 billion to HKD 4 billion for commercialized companies and from HKD 10 billion to HKD 8 billion for non-commercialized companies, with a three-year validity period. Simultaneously, HKEX and SFC jointly launched the "Technology Enterprise Channel" (TECH), providing an exclusive fast-track listing channel and confidential filing options for AI and large model companies.

At the policy level, the 2025-26 fiscal budget allocated HKD 10 billion to establish an innovation and technology industry-oriented fund and set aside HKD 1 billion to create the Hong Kong Artificial Intelligence Research Institute. The 2026-27 budget further established the "AI+ and Industrial Development Strategy Committee," designating AI as a core industry.

Hong Kong has become the world's first market to welcome the IPOs of large-scale model companies, and this pipeline continues to expand.

Looking to pick stocks or diagnose stock performance? Want to know the opportunities and risks in your portfolio? For all investment-related questions,just ask Futubull AI!

Looking to pick stocks or diagnose stock performance? Want to know the opportunities and risks in your portfolio? For all investment-related questions,just ask Futubull AI!

Editor/KOKO