NVIDIA's cash flow for 2026-2027 is close to the sum of Apple and Microsoft, yet its valuation is excessively discounted, with a PEG ratio of approximately 0.36 times, significantly lower than the Mag7 average of 2.61 times. Bank of America Securities attributes this to the market's failure to price in 'growth durability and capital allocation,' and recommends increasing the dividend yield to 0.5%-1% to leverage more predictable cash returns for a revaluation.

$NVIDIA (NVDA.US)$The valuation appears increasingly like a 'cash distribution' issue rather than just a matter of AI-driven prosperity. Bank of America Securities shifts its perspective from computational power demand and product iteration back to a more fundamental question: once the peak of ecosystem investment has passed, can NVIDIA return its ever-growingFree cash flowto shareholders in a more predictable manner, thereby triggering a revaluation of its worth?

According to HardAI, Bank of America Securities analyst Vivek Arya highlighted the core driver of NVIDIA's valuation in his latest report—'enhancing returns can broaden the shareholder base and signal enduring value.' He maintained a buy rating for NVIDIA with a target price of $300, not because the market underestimates how much NVIDIA can earn, but because investors remain uncertain about 'how this money will ultimately be used and whether it can be sustained.'

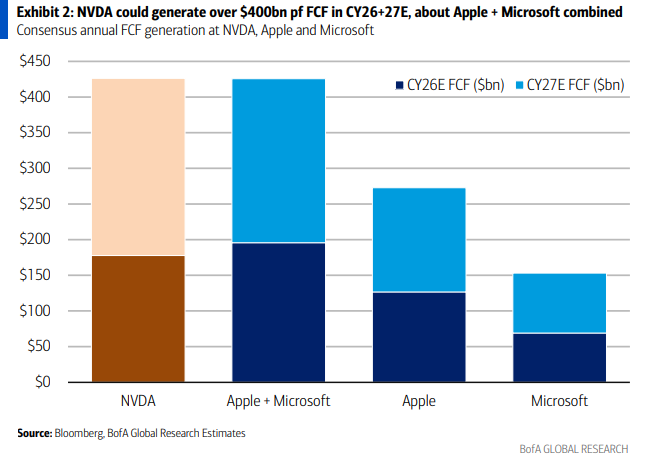

NVIDIA is projected to generate over $400 billion in free cash flow cumulatively between 2026 and 2027, a figure close to the combined total of Apple and Microsoft, yet its valuation remains significantly discounted.$Microsoft (MSFT.US)$The report argues that if the company enhances its cash returns to shareholders through dividends or share repurchases, making it more akin to 'mature large-cap technology stocks,' some concerns regarding the durability of growth and capital allocation would be mitigated, and the valuation discount would have a better chance of narrowing.

NVIDIA is projected to generate over $400 billion in free cash flow cumulatively between 2026 and 2027, a figure close to the combined total of Apple and Microsoft, yet its valuation remains significantly discounted.$Microsoft (MSFT.US)$The report argues that if the company enhances its cash returns to shareholders through dividends or share repurchases, making it more akin to 'mature large-cap technology stocks,' some concerns regarding the durability of growth and capital allocation would be mitigated, and the valuation discount would have a better chance of narrowing.

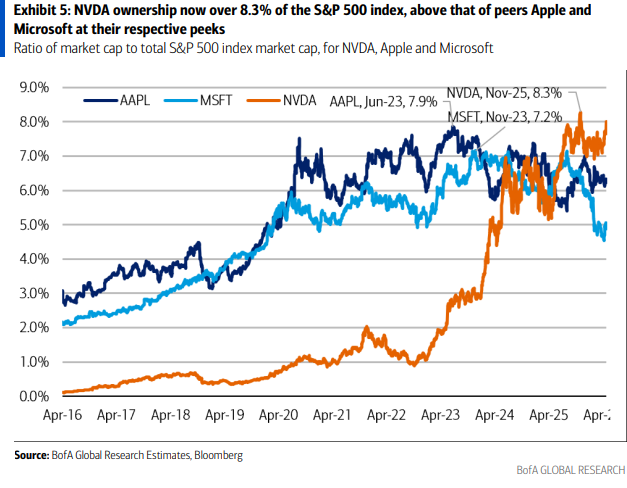

However, dividend payouts and buybacks are not the only headwinds. The report also highlights two constraining factors: first, NVIDIA’s weighting in the S&P 500 has reached approximately 8.3%, leaving limited room for further increases by passive or benchmark-tracking funds; second, competition from general-purpose GPUs offered by AMD and ASIC-based solutions from companies such as Google and AWS is intensifying.$Broadcom (AVGO.US)$Google, AWS, and others, is intensifying.

The crux of the valuation discount lies not in insufficient earnings but rather in the lack of pricing for 'durability + capital allocation.'

The starting point of the report is 'excessive discount.' Based on consensus estimates, NVIDIA currently trades at approximately 26x/19x CY26/27E P/E, while the 'Magnificent Seven' average is around 49x/42x; the discount is even larger when measured by EV/FCF (NVIDIA at about 28x/20x versus higher averages for the same group).PEG indicatorIn terms of another metric, NVIDIA stands at approximately 0.36x, significantly lower than the group average of 2.61x.

The implication behind this comparison is that the market does not doubt NVIDIA’s short-term profit surge but is more sensitive to two issues – whether growth can span multiple cycles and whether management will reinvest cash flow into directions that create 'uncertainty' for shareholders (such as unexpected large-scaleM&Aor noisier supplier financing arrangements). Under this sentiment, even though the scale of cash flow is already close to that of Apple and Microsoft combined, the valuation may continue to be suppressed.

Cash returns serve as a 'catalyst': they can lead to a new shareholder composition.

NVIDIA’s current dividend yield is only about 0.02%, resulting in significantly low coverage within dividend/income-focused funds. According to Lipper/EPFR data, NVIDIA is held by approximately 16% of equity income funds, compared to an average of about 32% for technology peers, whose average dividend yield is around 0.89%.

In other words, NVIDIA’s shares are naturally concentrated among growth/momentum/benchmark-driven funds. Once the market begins to worry about marginal changes in growth, such shareholders tend to be more 'discerning.' Higher and more predictable cash returns would unlock additional pools of capital, making the shareholder base stickier, more diversified, and closer to the path taken by Apple and Microsoft in accumulating a 'long-term shareholder foundation' through their return policies.

"Enhanced" return plan: Increasing dividend payout from a symbolic level to 0.5%-1%.

NVIDIA does not need to aggressively increase leverage or sacrifice investments; instead, it is recommended to first raise the most visible aspect—dividends. The proposal suggests increasing the dividend yield from 0.02% to 0.5%-1%, aligning with Apple’s approximately 0.4% and Microsoft’s roughly 0.8% range.

This provides an estimation of a "sufficient but not excessive" amount of funds: Achieving the aforementioned dividend yield target would require approximately $26 billion to $51 billion, accounting for about 15%-30% of CY26E free cash flow and 11%-21% of CY27E free cash flow. This implies that even with a significant increase in dividends, there would still be room for share repurchases and ecosystem investments.

Over the past three years (CY22-25), NVIDIA's free cash flow return rate (dividends + buybacks/FCF) averaged approximately 47%, lower than the industry average of around 80% and also below its earlier stage (CY13-22) average of approximately 82%. The relatively low return itself constitutes room for adjustment.

Two issues that dividends alone cannot resolve: oversized index positions and more complex competitive dynamics.

Regarding valuation suppression: NVIDIA accounts for approximately 8.3% of the S&P 500, surpassing the historical peaks of Apple and Microsoft at 7.9% and 7.2%, respectively. As the semiconductor sector now represents about 17% of the index, many funds “closely tracking the benchmark” objectively face greater difficulty in continuing to increase their holdings. With large private AI companies expected to go public in the future, the index structure may undergo some “rebalancing,” which could alleviate this constraint—but it will not disappear immediately just because NVIDIA increases its dividends.

The same applies to competition. NVIDIA currently faces two types of pressure: market share competition from general-purpose chipmakers like AMD and alternative solutions from ASIC/self-developed routes by companies such as Broadcom, Google, and AWS. It is still projected that NVIDIA can maintain over 70% of the AI value share due to factors including a more comprehensive product portfolio, third-party validated tokens/watt metrics, over $95 billion in strategic prepayments securing the supply chain, ecosystem investments, and more than 100 workload-optimized software libraries alongside enterprise/developer adoption rates. However, these advantages primarily determine whether NVIDIA can “maintain high profitability,” rather than directly deciding “when the valuation discount will disappear.”

Putting all of this together, the research report’s stance is actually quite clear: NVIDIA’s biggest challenge is not “proving the AI story again,” but using more predictable cash returns to create some initial relief on market concerns regarding growth durability and capital allocation efficiency. How much leeway it can create depends on whether it can defend its competitive moat while distributing its earnings more like a tech giant.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/joryn