On Wednesday, amid repeated activity in lithium mining stocks, UBS Group significantly raised its lithium price forecast, stating that this cycle is entirely different from previous ones.

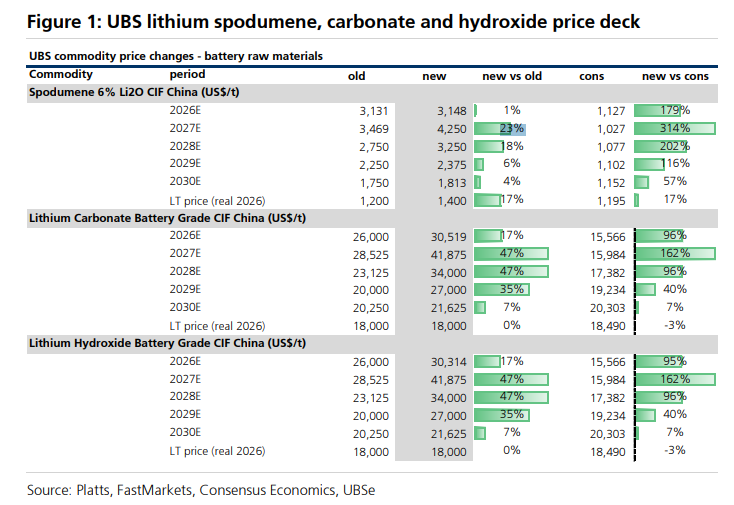

According to Wind Information, UBS Securities analyst Lachlan Shaw wrote in a research report: "This cycle features three key demand-side drivers — stronger energy storage, improved economics for electric vehicles, and accelerated penetration of electric trucks in China. On the supply side, there will be responses, but not at the same pace." In terms of pricing, the near-term forecast for 6% Li2O spodumene concentrate was raised by up to 23%, while the long-term price was increased by 17% to USD 1,400 per ton. Mid-term forecasts for battery-grade lithium carbonate and lithium hydroxide were raised by 17%-47%, with no change to the long-term price.

What is noteworthy is not individual price figures but the reassessment of the supply-demand slope for 2026-2027. The model predicts that global lithium demand will increase from 1.702 million tons LCE in 2025 to 1.974 million tons in 2026 and 2.324 million tons in 2027, adding approximately 623,000 tons LCE in new demand over two years; during the same period, risk-weighted supply is expected to increase by about 596,000 tons LCE, with demand slightly outpacing supply.

The report does not assume a disappearance of supply. On the contrary, it acknowledges that past cycles have shown lithium supply can ramp up relatively quickly. However, this time, the absolute scale of new demand is larger, and new projects face more policy, geological, and commercial constraints. In other words, the lithium market is not without supply response, but the response time may not be short enough.

The report does not assume a disappearance of supply. On the contrary, it acknowledges that past cycles have shown lithium supply can ramp up relatively quickly. However, this time, the absolute scale of new demand is larger, and new projects face more policy, geological, and commercial constraints. In other words, the lithium market is not without supply response, but the response time may not be short enough.

Energy storage has raised the baseline for lithium demand.

A significant starting point for this lithium price increase is the Battery Energy Storage System (BESS).

Geopolitical shocks, rising oil and gas prices, and increased electricity demand from data centers driven by AI, combined with an expected 30% drop in BESS system costs, have prompted upward revisions in global energy storage demand. By 2030, global BESS demand is projected to reach approximately 1.6 TWh, a 6% increase from previous forecasts, with larger upward adjustments in the United States and other regions.

The project pipeline also provides confidence. According to Benchmark Mineral Intelligence and available data, the global BESS project pipeline for 2026-2030 totals over 2.1 TWh, or 2,131 GWh. Regionally, China accounts for 46%, North America 18%, Europe 12%, Oceania 12%, Asia excluding China 4%, the Middle East 3%, South and Central America 4%, and Africa 1%.

There is a caveat: the project pipeline includes all stages such as proposed, announced, EPC tendering, technology awarding, under construction, operational, canceled, and expanded projects, which does not guarantee that these projects will be implemented on schedule. However, even with adjustments, energy storage is no longer a marginal component of lithium demand.

Europe is accelerating, the United States remains weak, and China determines the total volume.

The electric vehicle (EV) sector is experiencing a divergence.

As of March, EV sales in Germany, France, and the UK have grown year-over-year by 34%, 40%, and 22%, respectively, since the beginning of the year. The US market remains under pressure. China presents a more complex scenario: it accounts for approximately 60% of global EV sales, but its performance in March was weaker, with a year-over-year decline of 18%. However, EV sales in China typically pick up in the second half of the year, so a rebound in the second half is still anticipated.

The assumptions regarding global EV sales are also more optimistic than those in the original model. Previously, the model assumed a compound annual growth rate (CAGR) of 12% over the next two years, but this forecast was made prior to the current US-Iran conflict. In the lithium supply-demand model, a more constructive assumption of a 15% CAGR over the next two years has been adopted.

March data from China's battery supply chain provided some support. According to the China Automotive Battery Innovation Alliance (CABIA):

In March, EV registrations totaled 798,000 units, representing an 86% month-over-month increase and an 18% year-over-year decline, which is better than the combined January-February performance showing a 27% year-over-year decline.

In March, automobile exports reached 690,000 units, marking a 76% year-over-year increase, with EVs accounting for 50.6% of total exports.

In March, EV battery sales amounted to 114.5GWh, reflecting a 54% month-over-month increase and a 31% year-over-year rise.

In March, energy storage battery sales reached 60.3GWh, showing a 56% month-over-month increase and a 115% year-over-year surge.

Based on these figures, global battery demand is expected to grow from 1.476TWh in 2025 to 1.811TWh in 2026 and 2.353TWh in 2027.

Supply will catch up, but this time it may not match the steep slope of demand.

The judgment on supply is not an aggressive bearish view; the issue is not whether supply can catch up, but when it will catch up.

From 2025 to 2027, the primary new supply in the model will come from Australia, China, and Africa.

Australia is expected to contribute approximately 23% of the incremental supply, sourced from Kathleen Valley, Pilgangoora, and Greenbushes. However, Greenbushes has been revised downward due to IGO's reduced production guidance.

China is projected to contribute around 28%, including significant new supply from Qinghai salt lakes and the restart of CATL's Jianxiawo mine. Research reports predict that starting mid-2026, Jianxiawo will account for approximately 44% of China's supply.

In Africa, ongoing attention is being paid to Goulamina in Mali, as well as Kamativi and Arcadia in Zimbabwe. Among these, Arcadia faces policy-related challenges, as Zimbabwe mandates domestic midstream processing, adding complexity to the project.

There is a risk of supply exceeding expectations, especially in regions with low transparency, such as Nigeria's DSO. However, it is also believed that in an environment of heightened macroeconomic uncertainty, disruptions in diesel and input costs, and significant lithium price volatility, listed producers will prioritize higher certainty before restarting, expanding, or initiating new projects, which will suppress the speed of potential supply responses.

Inventories have left little room for market buffering.

Inventory signals from China also support the view of a tightening market.

SMM data shows that recent weekly lithium carbonate inventories in China have increased, but measured in inventory months, they remain near historical lows, indicating that the overall supply chain remains tight.

Monthly lithium carbonate inventories are at relatively low levels year-on-year. If seasonal patterns in orders and restocking continue, processing-side inventories may rise in the coming months.

Lithium hydroxide inventories will continue to decline in the first few months of 2026. In February, due to the shorter month and seasonal factors, inventory levels rose slightly, but absolute inventory remains tight before entering the regular order and restocking season.

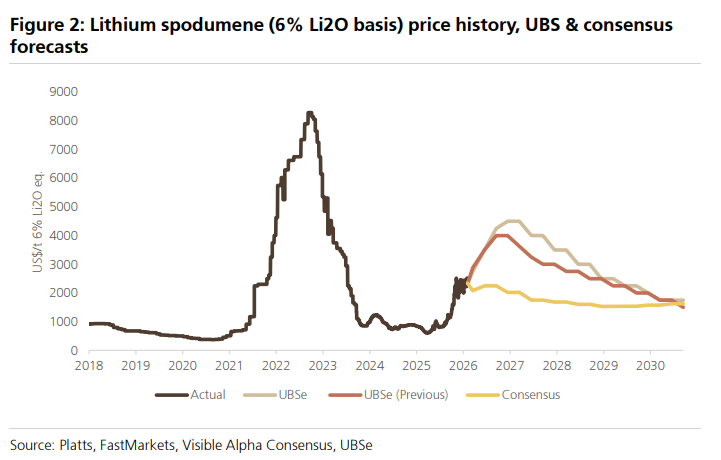

The most aggressive price forecast is for 2027, but there has been no upward revision in long-term chemical lithium prices.

In the new price forecast, 2027 stands out as the most notable year.

Price forecast for 6% Li2O spodumene concentrate:

2026: USD 3,148 per ton, up 1% from the previous forecast;

2027: USD 4,250 per ton, up 23%;

2028: USD 3,250 per ton, up 18%;

2029: USD 2,375 per ton, up 6%;

2030: USD 1,813 per ton, up 4%;

Long-term price: USD 1,400 per ton, up 17%.

Price forecast for battery-grade lithium carbonate:

2026: USD 30,519/ton, up 17%;

2027: USD 41,875/ton, up 47%;

2028: USD 34,000/ton, up 47%;

2029: USD 27,000/ton, up 35%;

2030: USD 21,625/ton, up 7%;

Long-term price: USD 18,000/ton, unchanged.

The forecast for battery-grade lithium hydroxide is largely consistent with that of lithium carbonate: USD 30,314/ton in 2026, USD 41,875/ton in 2027, USD 34,000/ton in 2028, USD 27,000/ton in 2029, USD 21,625/ton in 2030, and the long-term price remains at USD 18,000/ton.

The long-term price of spodumene has been revised upwards due to ongoing capital expenditure and operational cost inflation in key mining regions such as Canada and Australia. The long-term price for chemical lithium has not been adjusted upwards, which is attributed to compressed profit margins in China's conversion process.

The real unresolved issue lies beyond 2030.

The lithium market is expected to face a deficit of 6,000 tons of LCE in 2025, expanding to 84,000 tons in 2026. By 2027, the market will approach balance but remain slightly undersupplied, followed by continued deficits from 2028 to 2031.

Its outlook for beyond 2030 is more cautious: to address the anticipated structural deficits, new greenfield projects will become increasingly critical, though significant uncertainty remains regarding which projects will ultimately fill these gaps.

This is the implication of the research report: it does not suggest that lithium supply will not recover, but rather that after demand accelerates again, the market will require higher prices sustained over a longer period to incentivize the next wave of sufficiently large supply.

Editor/joryn