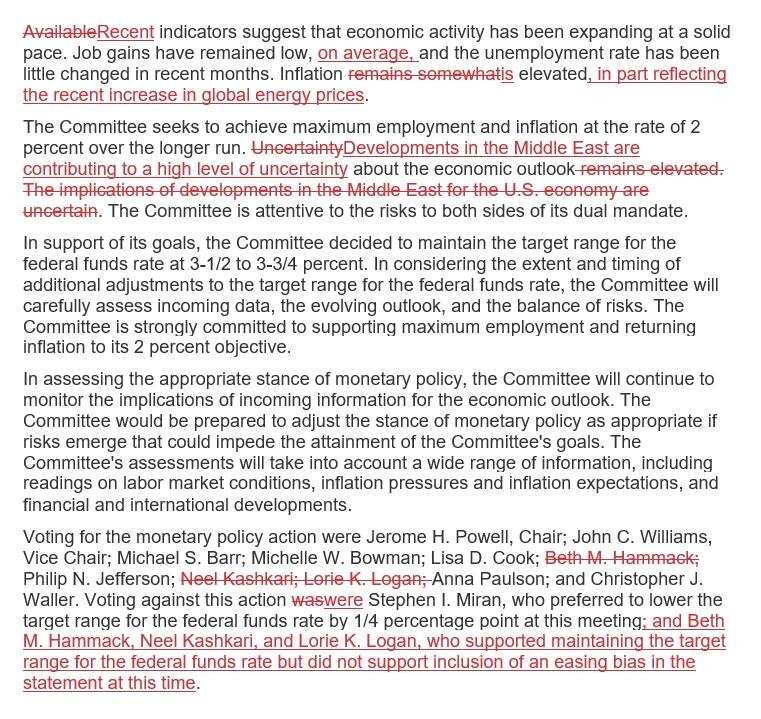

Among the dissenters, Governor Milan insisted on a 25-basis-point rate cut this year, while three regional Federal Reserve presidents supported no rate cut but opposed retaining the easing bias in the statement. The statement reiterated readiness to adjust the stance of monetary policy when appropriate, revised to say that the situation in the Middle East has heightened significant uncertainty about the economic outlook, and added that part of the high inflation stems from recent global energy price increases. 'The New Fedwire': There is serious division within the Fed over whether it should signal the possibility of further rate cuts in the future.

Key Points:

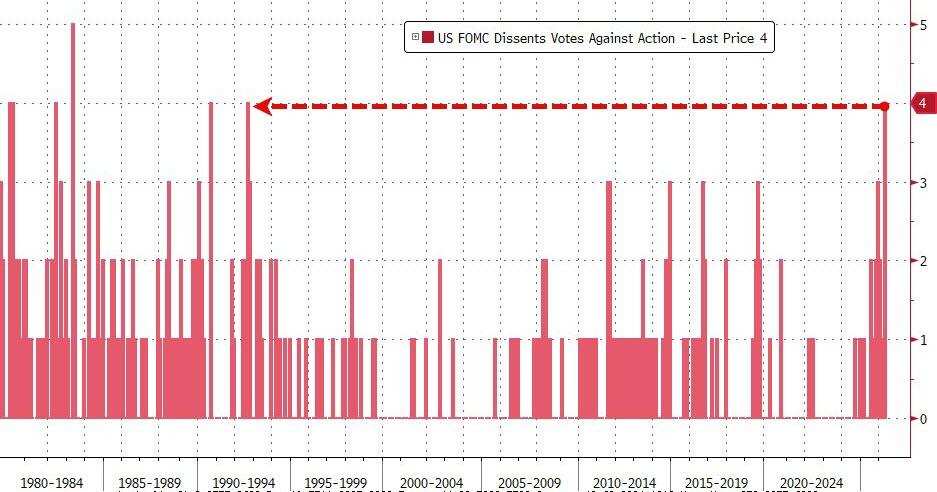

As expected by the market, the Federal Reserve paused rate cuts for the third consecutive meeting, with dissenters increasing from one at the previous meeting to four.

Among the dissenters, Governor Milan insisted on a 25-basis-point rate cut this year, while three regional Federal Reserve presidents supported no rate cut but opposed retaining the easing bias in the statement. The statement continued to emphasize readiness to adjust the stance of monetary policy when appropriate.

The statement removed the phrase 'the impact of the Middle East situation on the U.S. economy is uncertain' and instead stated that the situation in the Middle East has exacerbated significant uncertainty about the economic outlook.

The statement added that part of the high inflation is due to recent global energy price increases.

'The New Fedwire': There is serious division within the Fed over whether it should signal the possibility of further rate cuts in the future.

At Powell’s last monetary policy meeting as Federal Reserve Chair, the Fed, as expected by the market, remained on hold but revealed growing divisions within the policymaking body over whether to continue cutting rates, with some officials questioning whether to keep signaling that the likelihood of rate cuts outweighs that of hikes.

On Wednesday, April 29, Eastern Time, the Federal Reserve announced that the Federal Open Market Committee (FOMC) decided after its meeting to keep the target range for the federal funds rate unchanged at 3.50% to 3.75%. Thus, following three consecutive rate cuts through the end of last year, the FOMC has paused action at all three monetary policy meetings so far in 2026.

This Federal Reserve decision was entirely in line with market expectations. As of Tuesday's close, tools from the Chicago Mercantile Exchange (CME) showed that the futures market priced in a 100% probability of no rate cut this week, approximately a 97% chance of no action at the June meeting, and only slightly over a 20% probability of a rate cut by the end of December, at 21.9%.

As with the previous FOMC meeting more than a month ago, at this meeting, Miran, the Fed governor 'handpicked' by former U.S. President Trump last year, continued to support interest rate cuts. Unlike the previous meeting, in addition to Miran, three other FOMC members with voting rights opposed the statement due to its dovish stance.

The above result means that among the 12 FOMC voting members, including Powell himself, eight supported the statement, and four opposed it.

Nick Timiraos, a veteran Fed reporter known as the 'new Fedwire,' pointed out that this decision revealed a more serious division within the Fed regarding whether it should signal the possibility of further rate cuts in the future. The fact that four out of the 12 voting members dissented is the highest number of dissenters at a Fed monetary policy meeting since 1992.

Timiraos commented that the dissenting outcome might foreshadow what Kevin Warsh, the nominee for the next Fed Chair, expressed during last week's confirmation hearing. Warsh anticipated scenes of 'chaotic meetings' and 'internal debates.' This division highlights the potential decision-making challenges Warsh may face as the Fed attempts to respond to new inflation risks triggered by energy shocks.

Governor Miran insisted on a 25-basis-point rate cut this year, while three regional Fed presidents did not support retaining a dovish bias.

Compared with the statement from the March meeting, the biggest difference in this meeting's statement was that a total of four FOMC voting members did not support the resolution, whereas only one dissented at the previous meeting.

The voting results disclosed this Wednesday showed that among the four 'dissenters,' Fed Governor Miran (Stephen Miran) cast his opposing vote again because he supported a 25-basis-point rate cut, as he did at the previous meeting.

White House economic advisor Miran has consistently voted against the Fed’s interest rate decisions since he concurrently became a governor in September last year. He advocated for a 50-basis-point rate cut at the September, October, and December meetings last year and has consistently pushed for a 25-basis-point rate cut at this year's three meetings.

The other three individuals are regional Fed presidents with voting rights at this year’s FOMC meetings: Beth Hammack, president of the Cleveland Fed, Neel Kashkari, president of the Minneapolis Fed, and Lorie Logan, president of the Dallas Fed.

Their positions differ somewhat from Miran's. The statement revealed that they 'supported maintaining the federal funds rate target range unchanged but opposed reflecting a dovish bias in the statement.'

Media commentary noted that the voting results of this meeting revealed a significant divergence within the Federal Reserve, with Milan still advocating for interest rate cuts while three other voting members opposed retaining the so-called 'easing bias,' which refers to the Fed's consistent signaling over the past two years that the likelihood of rate cuts was higher than that of rate hikes.

The commentary pointed out that the wording of the statement from this meeting did not explicitly reveal an easing bias and did not directly mention rate cuts. The statement reiterated:

"If risks emerge that could impede the Committee’s achievement of its goals, the Committee will be prepared to adjust the stance of monetary policy as appropriate."

However, three regional Federal Reserve presidents labeled this phrasing as indicative of an easing bias.

Revised to state that escalating tensions in the Middle East have heightened significant uncertainty about the economic outlook.

Compared to the previous meeting, the main change in the economic assessment in this meeting's statement reflected the impact of the conflict in Iran.

In the previous resolution statement, there was an additional sentence regarding the situation in the Middle East: "The impact of developments in the Middle East on the U.S. economy remains uncertain." This statement removed that sentence and revised the phrasing concerning the notion that "uncertainty about the U.S. economic outlook remains high," now stating:

"Developments in the Middle East have exacerbated the already high level of uncertainty surrounding the economic outlook."

Prior to the aforementioned sentence, the statement reiterated that the FOMC is committed to achieving maximum employment and a 2% inflation target over the long term. Following that sentence, the statement again emphasized that the FOMC is closely monitoring risks related to both employment and inflation.

Added a section attributing high inflation partly to rising global energy prices.

In terms of other commentary on the economic situation, this statement made only minor adjustments. Unlike the previous statement, which reiterated that the inflation rate remained slightly elevated, this one emphasized the impact of the Middle East conflict, stating:

"The inflation level remains high, partly due to the recent rise in global energy prices."

The previous statement reiterated that employment growth remained low. This time, a modifier was added, changing it to "On average, employment growth remains low." The previous statement noted that "current" indicators suggested economic activity "has been steadily expanding," whereas this time, "current" was changed to "recent."

This statement repeated verbatim from the last one, saying that "the unemployment rate has remained largely unchanged in recent months."

This statement did not mention any balance sheet-related changes such as Treasury bond purchases, indicating that the Reserve Management Purchases (RMP) operations by the New York Fed are proceeding according to the latest plan.

At the December FOMC meeting last year, the initiation of so-called reserve management was announced. The statement at that time said that the FOMC believed "reserve balances had fallen to an adequate level and would begin purchasing short-term Treasury securities as needed to continuously maintain an ample supply of reserves." At that time, the New York Fed announced plans to purchase $40 billion worth of short-term Treasury securities over the next 30 days starting from December 11.

The plan published earlier this month by the New York Fed showed that during the monthly cycle ending May 13, RMP operations with a purchase scale of $25 billion will be conducted, representing a nearly 40% reduction compared to the purchase level in December last year.

The red text below highlights the deletions and additions in this policy statement compared to the previous one.

Editor/Rocky