Qualcomm released its Q2 earnings report for the fiscal year 2026, with revenue of $10.6 billion, a year-over-year increase of 3%, and earnings per share of $2.65, both surpassing expectations. Business segments such as automotive and IoT performed exceptionally well, but smartphone chip revenue declined by 13% year-over-year. Impacted by memory shortages, the guidance for the third quarter fell below market expectations. The CEO stated that the smartphone market is expected to bottom out and recover in the third quarter.

A memory shortage has impacted demand for mobile chips, but $Qualcomm (QCOM.US)$ the CEO announced that the company can "see the bottom," and its data center business is expected to provide new growth momentum.

Boosted by this news, Qualcomm's after-hours trading surged over 13%, following a 4% gain in the previous trading session, with cumulative gains exceeding 21% since April.

On April 29, after the US stock market closed, Qualcomm released its fiscal year 2026 second-quarter earnings report. Both revenue and earnings per share exceeded Wall Street expectations, but the guidance for the third quarter was significantly lower than market estimates.

On April 29, after the US stock market closed, Qualcomm released its fiscal year 2026 second-quarter earnings report. Both revenue and earnings per share exceeded Wall Street expectations, but the guidance for the third quarter was significantly lower than market estimates.

Moreover, the company's chip business has been significantly affected by the shortage of mobile memory, with smartphone business revenue declining 13% year-on-year. CEO Cristiano Amon stated:

We can now announce that we have hit the bottom, and we expect the smartphone market to start recovering after the third quarter.

Meanwhile, Qualcomm revealed that in the second half of this year, it will deliver custom chips to a hyperscale cloud computing company, and plans to host an investor day on June 24, where it will elaborate on its data center and 'physical AI' strategy.

Due to weaker-than-expected guidance for the third fiscal quarter, several analysts downgraded their ratings and target prices for Qualcomm. However, market expectations of the company’s long-term growth potential continue to support its stock price.

Second-quarter results beat expectations, but mobile business under pressure

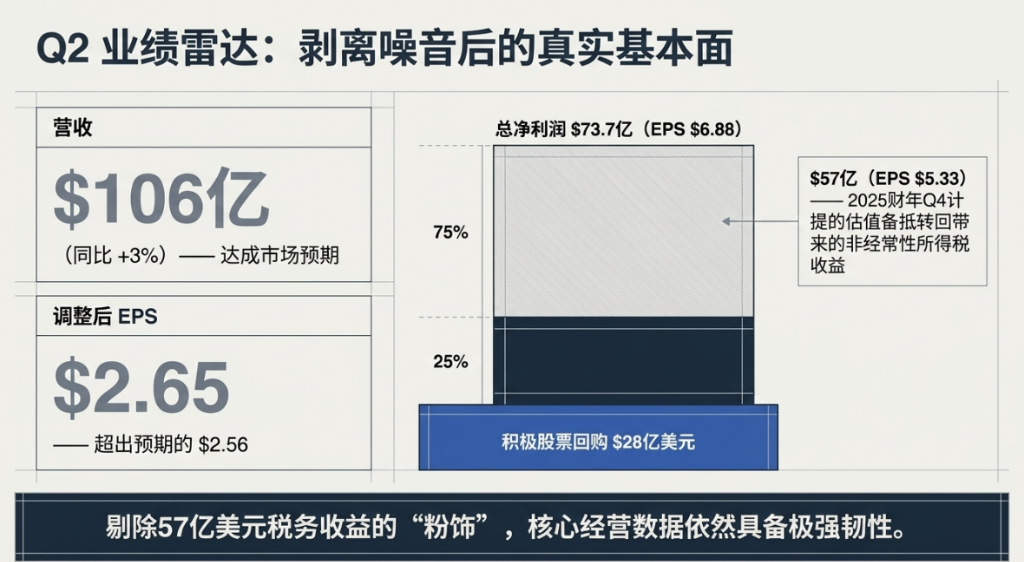

Qualcomm reported adjusted earnings per share of $2.65 in the second fiscal quarter, surpassing analysts' expectations of $2.56; revenue increased 3% year-over-year to $10.6 billion, roughly in line with market forecasts.

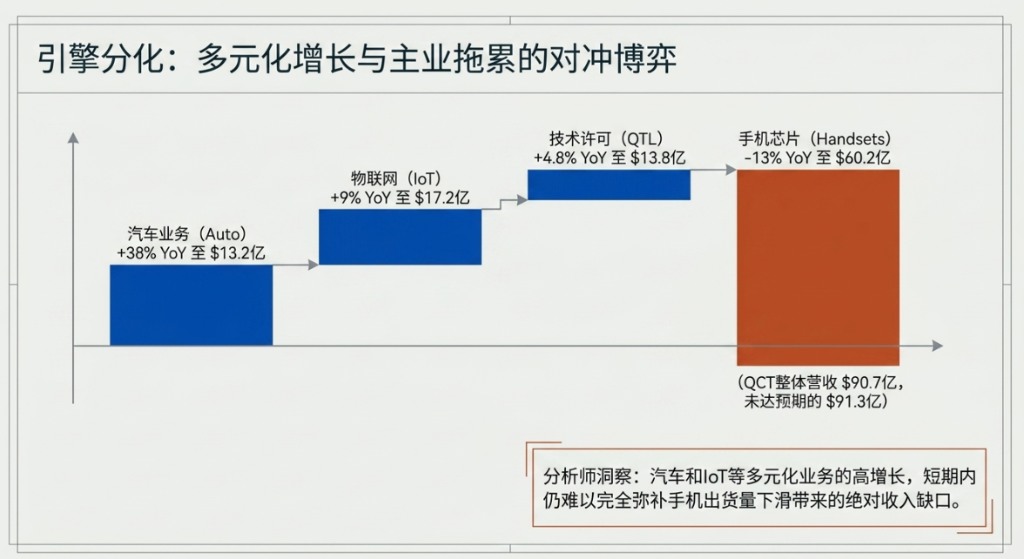

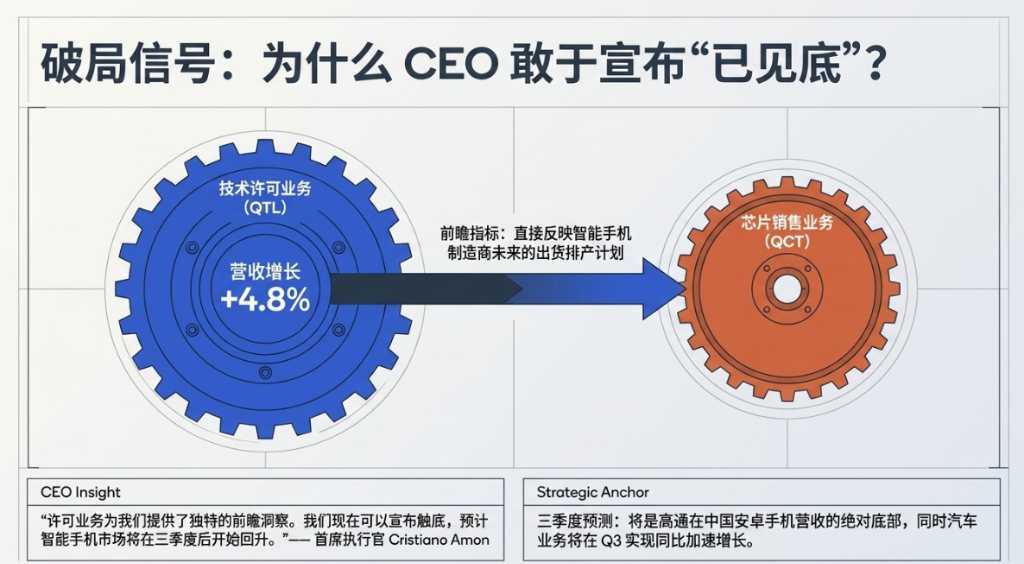

By segment, automotive revenue grew 38% year-over-year to $1.32 billion, Internet of Things (IoT) revenue increased 9% to $1.72 billion, and technology licensing (QTL) revenue rose 4.8% to $1.38 billion, all showing strong performance.

Revenue from the mobile chip business declined 13% year-over-year to USD 6.02 billion, becoming the largest drag on performance this quarter. Overall chip business (QCT segment) revenue was USD 9.07 billion, slightly below analyst expectations of USD 9.13 billion.

Notably, the company recorded a USD 5.7 billion income tax benefit (or USD 5.33 per share) this quarter, stemming from the reversal of a valuation allowance previously booked in the fourth quarter of fiscal year 2025, driving net profit for the quarter to USD 7.37 billion, or USD 6.88 per share.

Additionally, the company spent USD 2.8 billion on its stock repurchase program during this quarter.

Third-quarter guidance fell below expectations as the shadow of memory shortages persists.

Qualcomm expects third-quarter revenue to range between USD 9.2 billion and USD 10 billion, with a midpoint of approximately USD 9.6 billion, compared to prior analyst forecasts of USD 10.26 billion.

Adjusted earnings per share are projected to be in the range of USD 2.10 to USD 2.30, also below market expectations of USD 2.43.

The company also anticipates third-quarter chip business (QCT) revenue to be between USD 7.9 billion and USD 8.5 billion, significantly lower than analyst estimates of USD 8.93 billion.

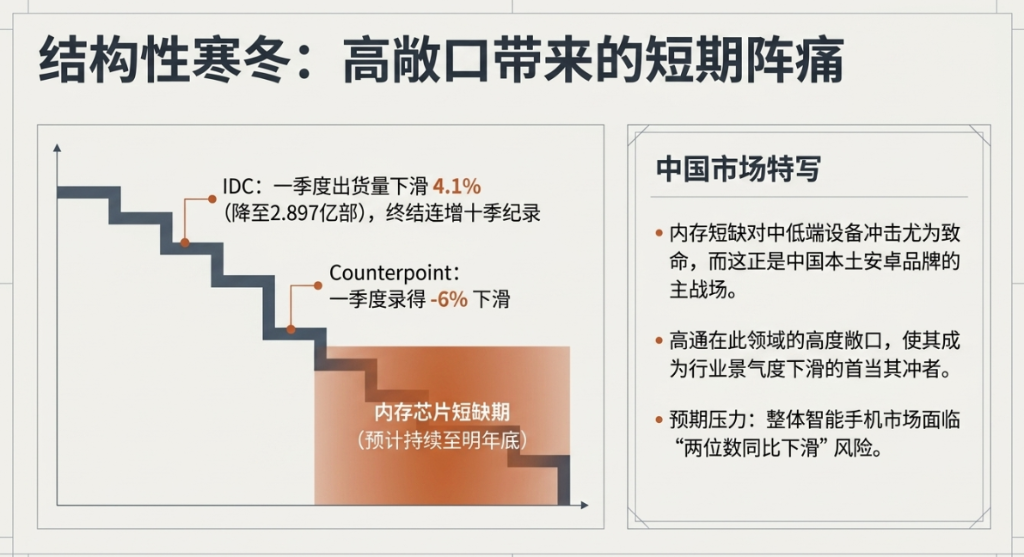

According to Counterpoint Research, global smartphone shipments declined 6% year-over-year in the first quarter of this year, with the memory chip shortage expected to persist until the end of next year.

International Data Corporation (IDC) also noted that first-quarter shipments fell by 4.1% to 289.7 million units, breaking a streak of ten consecutive quarters of growth since mid-2023, and warned that this is merely a 'moderate harbinger' of deeper pressures anticipated through the remainder of 2026.

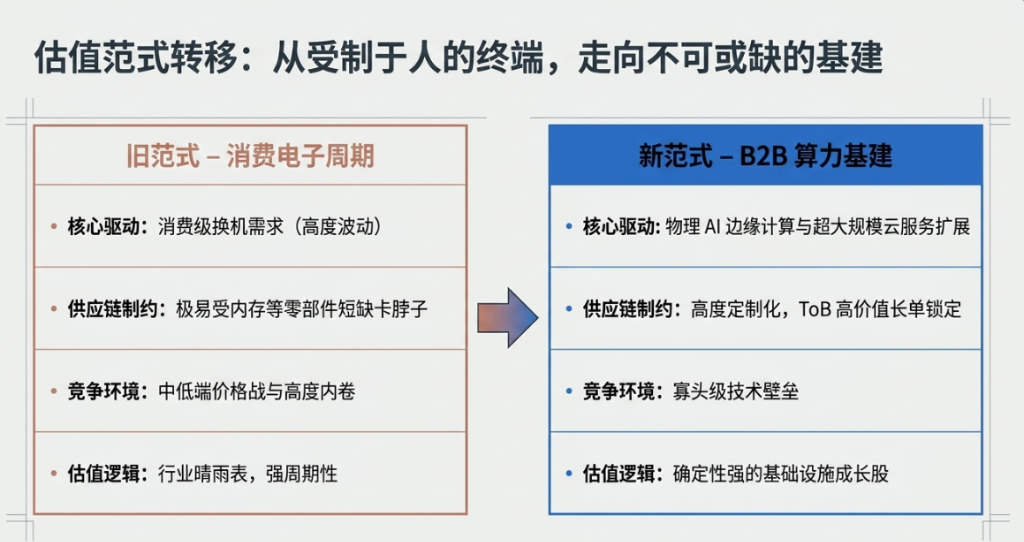

Stacy Rasgon, an analyst at Bernstein Research, stated that total smartphone market shipments this year may face a double-digit year-over-year decline. Qualcomm's significant exposure to the consumer electronics sector makes its performance widely regarded as a barometer of industry health.

However, Amon noted that the company's licensing business provides it with unique forward-looking insights, as licensing revenue directly reflects the shipment plans of smartphone manufacturers, supporting its view that the third quarter will mark the bottom.

Qualcomm stated in its earnings report that the third quarter would represent the bottom for its revenue from Chinese Android phones, while its automotive business is expected to achieve year-over-year accelerated growth in the same period.

Data center expansion has become a key focus for market attention.

Amid pressure on its mobile phone business, Qualcomm’s strategic progress in entering the data center chip market has drawn significant investor interest.

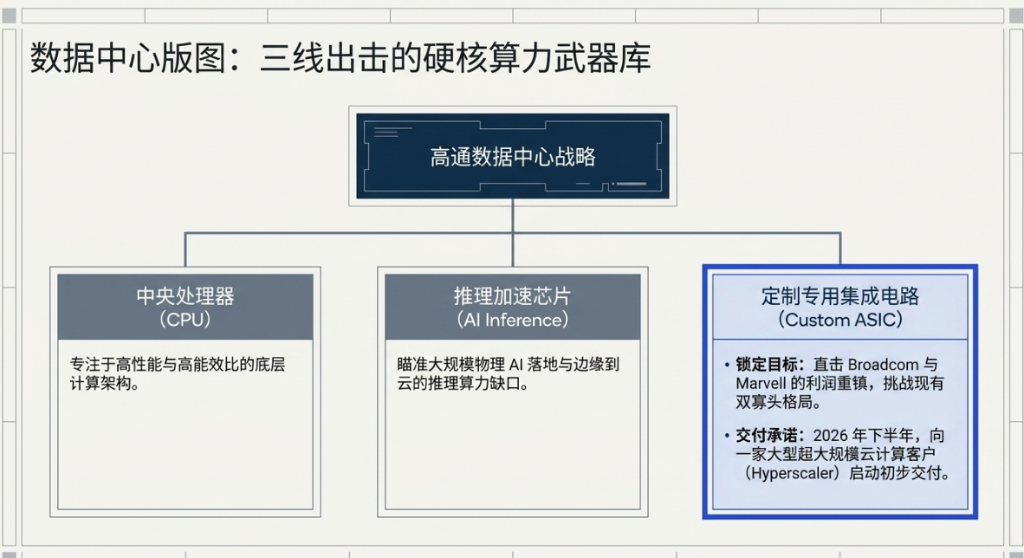

Amon stated that the company is collaborating with clients to develop three types of chips: central processing units (CPUs), inference acceleration chips, and custom application-specific integrated circuits (ASICs), the latter of which represents a major revenue source for competitors like Broadcom and Marvell.

He specifically highlighted that Qualcomm’s acquisition of AlphaWave provided critical connectivity intellectual property support for its custom ASIC business. Amon said:

We have secured customer collaborations for custom ASICs, which was precisely the goal of acquiring AlphaWave. We are advancing execution across all three types of chips.

Qualcomm expects to initiate preliminary delivery of custom chips to a large hyperscale cloud computing client in the second half of 2026.

Analysts at Stone Fox Capital pointed out that the expected EPS for fiscal year 2027 exceeds $11. Based on this, the current price-to-earnings ratio is less than 14 times, making the stock attractive for purchase during pullbacks.

Investors will seek a clearer roadmap for Qualcomm’s data center strategy during the Investor Day on June 24 and Cristiano Amon's presentation at the Computex event in Taiwan, China.

Upgraded performance updates help you stay ahead in seizing opportunities!Come and experience it >>

Editor/Rocky