Microsoft's revenue in the third fiscal quarter increased by 18% year-over-year, with EPS growing by 23%, surpassing analyst expectations by more than 5%. Annualized AI revenue exceeded $37 billion, representing a 123% year-over-year increase, and commercial RPO doubled year-over-year. Intelligent Cloud revenue grew by 30%, with Azure revenue growth slightly exceeding expectations, but the intelligent cloud profit margin declined by 1.8 percentage points year-over-year. Capital expenditure growth slowed to 49% year-over-year from 66% in the previous quarter, decreasing nearly 15% from the record high in the prior quarter. Windows and Xbox showed weakness, with personal computing business revenue declining by 1%, although search advertising revenue increased by 12%. Shares fell over 3% in after-hours trading before reversing to positive territory.

The leader in artificial intelligence (AI) $Microsoft (MSFT.US)$ reported stronger-than-expected overall revenue and profit growth last quarter, but capital expenditures were a drag.

After the US stock market closed on Wednesday, Eastern Time on the 29th, Microsoft announced that for the third fiscal quarter of its 2026 fiscal year ending March 31, 2026 (hereinafter referred to as Q1), both revenue and earnings per share (EPS) maintained double-digit year-over-year growth rates.

The biggest highlight of Microsoft's Q1 performance still came from cloud and AI. Including products such as Office and Azure, the combined year-over-year revenue growth rate of Microsoft’s commercial cloud business slightly increased to 29%, with the revenue growth of Azure and other cloud services in the intelligent cloud segment rising to 40%. Microsoft CEO Satya Nadella stated that Microsoft's AI business annualized revenue grew 123% year-over-year, indicating that AI demand is rapidly converting into revenue.

The biggest highlight of Microsoft's Q1 performance still came from cloud and AI. Including products such as Office and Azure, the combined year-over-year revenue growth rate of Microsoft’s commercial cloud business slightly increased to 29%, with the revenue growth of Azure and other cloud services in the intelligent cloud segment rising to 40%. Microsoft CEO Satya Nadella stated that Microsoft's AI business annualized revenue grew 123% year-over-year, indicating that AI demand is rapidly converting into revenue.

Enterprise software business remained robust. Revenue from the Productivity and Business Processes division increased 17% year-over-year, with Microsoft 365 Commercial Cloud revenue growing 19%. Meanwhile, Microsoft's commercial remaining performance obligations (RPO) surged 99% year-over-year, providing strong visibility for future cloud and software revenue.

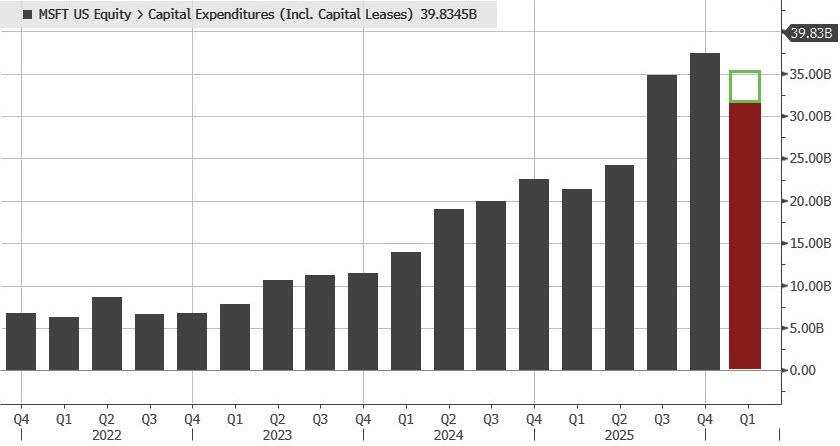

However, Microsoft's capital expenditure growth significantly slowed in Q1, with the year-over-year growth rate declining from 66% in the previous quarter to 49%, while analysts expected growth of about 65%. Commentators noted this indicates Microsoft's capital investment pace is not as fast as the market anticipated.

Following the earnings report, Microsoft’s stock price, which had fallen more than 1% during regular trading hours on Wednesday, did not rebound despite surpassing expectations for both revenue and EPS. Instead, it dropped further, falling over 3% in after-hours trading before slightly recovering.

Analysts believe that the post-market decline in stock price does not indicate weak earnings, but rather reflects a repricing of uncertainties regarding capital expenditures, cloud profit margins, and future guidance. Microsoft’s fundamentals remain strong, but amid crowded AI trades and high valuation demands, the market has become more sensitive to costs behind growth and uncertainties in future guidance. Investors are not only concerned with whether Q1 performance exceeded expectations, but also with when AI investments will translate into sustainable free cash flow and higher profit margins.

Revenue and profits both beat expectations; operating leverage remains intact.

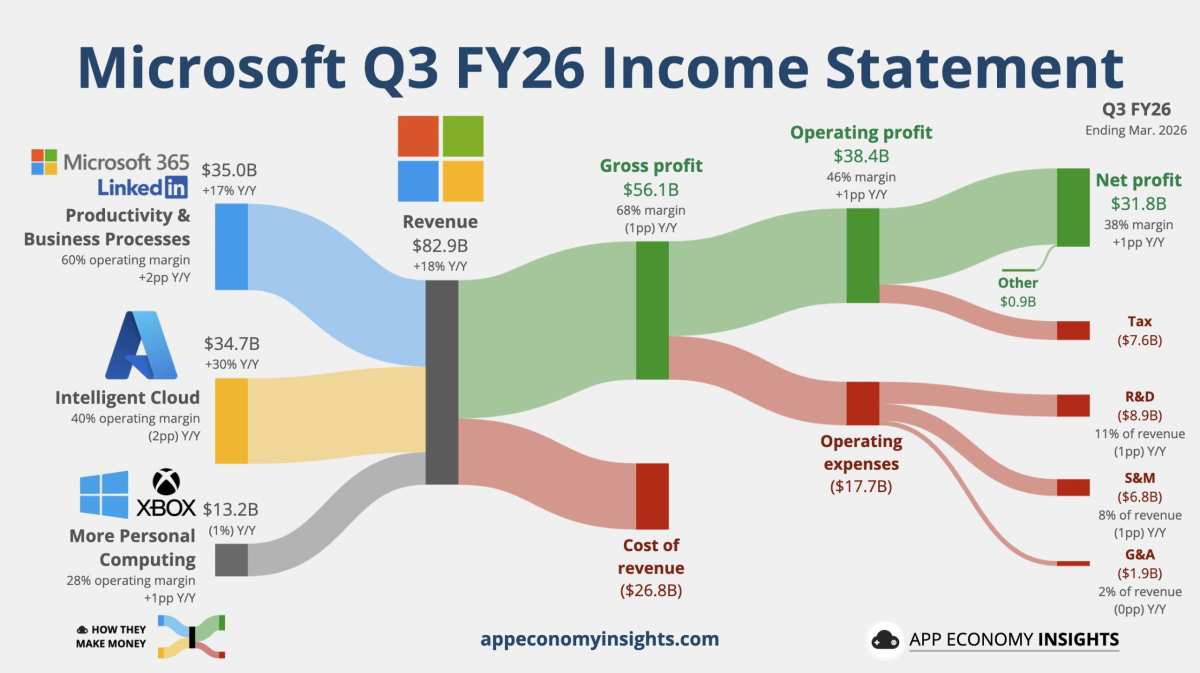

Microsoft’s Q1 revenue reached $82.886 billion, surpassing analyst expectations of $81.46 billion, representing an 18% year-over-year increase, up from 17% in the prior quarter, and a 15% increase at constant currency. This implies that exchange rates contributed positively to revenue this quarter, adding approximately $2.067 billion.

Profitability also remained strong. Microsoft’s Q1 operating profit reached $38.398 billion, a 20% year-over-year increase and a 16% rise at constant currency. The operating margin was approximately 46.3%, slightly up from about 45.7% in the same period last year. Net income was $31.778 billion, a 23% year-over-year increase. On a non-GAAP basis, diluted EPS was $4.27, a 23% year-over-year increase, slightly below the 24% growth rate in the previous quarter, surpassing analysts’ expectations of $4.07.

The non-GAAP metrics primarily exclude the impact of OpenAI investments. This quarter, the net loss related to OpenAI investments was only USD 14 million, with minimal impact on EPS; whereas in the same period last year, this impact was USD 583 million, equivalent to USD 0.08 per share. Therefore, from a comparable perspective, Microsoft's non-GAAP net profit grew by 20% year-over-year, and non-GAAP EPS increased by 21%.

It is worth noting that Microsoft’s gross margin in the first quarter declined slightly, with an overall gross margin of approximately 67.6%, lower than about 68.7% in the same period last year. This is related to rising costs in cloud and AI infrastructure, but the company maintained its operating margin through cost control: combined R&D, sales, and administrative expenses grew by approximately 9%, significantly lower than the 18% revenue growth rate.

Azure cloud revenue growth slightly exceeded expectations, with annualized AI revenue surpassing USD 37 billion.

Microsoft Cloud remains the core growth engine in the earnings report. In the first quarter, Microsoft’s total commercial cloud revenue reached USD 54.5 billion, higher than the analysts' estimate of USD 53.78 billion, growing by 29% year-over-year, up from the previous quarter’s growth rate of 26%, or 25% growth on a constant currency basis. This segment includes commercial cloud revenue from Azure, Microsoft 365, Dynamics, and others, and is the most closely watched vehicle for Microsoft’s “AI monetization.”

Revenue from intelligent cloud services in the first quarter was USD 34.681 billion, higher than the analysts' forecast of USD 34.32 billion, representing a 30% year-over-year increase, or 28% growth on a constant currency basis. Among this, Azure and other cloud service revenues grew by 40% year-over-year, slightly faster than the previous quarter’s growth rate of 39%. Excluding currency effects, growth on a constant currency basis was 39%, slightly above the analysts' expected growth rate of 38.2%.

For Azure, which is already operating on a massive base, a 40% growth rate remains very robust, indicating that enterprise demand for AI computing power, cloud migration, and data infrastructure continues to expand.

Nadella disclosed that Microsoft’s annualized AI revenue run rate exceeds USD 37 billion, growing by 123% year-over-year. This is not quarterly revenue but an annualized run rate based on current revenue levels. Nevertheless, it demonstrates that AI is no longer just a “narrative” but is generating substantial revenue across Microsoft Cloud, Copilot, developer tools, and enterprise software.

The remaining performance obligations (RPO) for commercial contracts grew by 99% year-over-year to USD 627 billion, another significant signal. This represents a substantial increase in signed but not yet recognized revenue contracts, reflecting stronger long-term commitments from enterprise customers to Microsoft Cloud and AI services. However, the ultimate conversion of these orders into revenue and profit will depend on delivery schedules, cloud capacity, and cost structures.

Cash Flow and Capital Expenditure: AI Construction Enters a Phase of Heavy Investment

Microsoft’s operating cash flow in the first quarter was USD 46.679 billion, higher than USD 37.044 billion in the same period last year, indicating that the core business remains highly cash-generative. Compared to cash flow, capital expenditure grew even faster, with spending on property and equipment reaching USD 30.876 billion, an increase of over 84% from USD 16.745 billion in the same period last year.

However, compared to the previous quarter, Microsoft's overall capital expenditure growth in the first quarter was significantly more moderate. Including assets acquired through financial leases, capital expenditure for the quarter totaled $31.9 billion, a year-over-year increase of 49%. In contrast, the previous quarter set a record with a year-over-year growth of 66%, while this quarter’s figure declined by nearly 15% from the record level of $37.5 billion in the previous quarter.

In the first three quarters of this fiscal year, Microsoft's cumulative spending on property and equipment reached $80.146 billion, an increase of nearly 69% year-over-year. This growth rate indicates that the company is aggressively scaling its capacity to meet AI cloud demand. On the balance sheet, net property and equipment rose from $204.966 billion at the end of June last year to $283.228 billion, further validating the scale of investment in data centers and AI infrastructure.

As of the end of March, Microsoft’s total cash, cash equivalents, and short-term investments amounted to $78.272 billion, down from $94.565 billion at the end of June last year. In the first quarter, Microsoft returned $10.2 billion to shareholders through dividends and share repurchases.

For a cash flow giant like Microsoft, the financial safety cushion remains robust. However, the market is now more focused on how long the peak in AI-related capital expenditures will last and whether these investments can continue to support Azure’s high growth trajectory and ultimately stabilize cloud business profit margins.

Productivity Business: Microsoft 365 and Dynamics Continue to Drive High-Quality Growth

Revenue from the Productivity and Business Processes division in the first quarter reached $35.013 billion, surpassing analysts’ expectations of $34.48 billion. This represents a year-over-year increase of 17%, slightly higher than the 16% growth rate in the previous quarter, or 13% growth at constant currency. Operating profit was $20.973 billion, growing approximately 21% year-over-year, with an operating margin approaching 60%, making it one of Microsoft’s highest-margin and strongest cash-flow businesses.

Microsoft 365 Commercial Cloud revenue grew 19% year-over-year, or 15% at constant currency, reflecting stable enterprise subscription demand and providing a foundation for upselling AI features such as Copilot. Microsoft 365 Consumer Cloud revenue grew even faster, increasing 33% year-over-year, or 29% at constant currency.

Dynamics 365 revenue increased 22% year-over-year, or 17% at constant currency, continuing the strong growth trend in enterprise application software. LinkedIn revenue grew 12%, or 9% at constant currency, achieving double-digit growth despite a macroeconomic environment where advertising and recruitment demand may not be particularly robust.

This division is crucial as it not only provides stable profits but also serves as an entry point for the commercialization of Microsoft’s AI products. The interconnected ecosystem of users and data across Copilot, Teams, Office, Dynamics, and LinkedIn is a key competitive advantage that differentiates Microsoft from pure-play cloud infrastructure providers.

Intelligent Cloud: The Most Impressive Growth but Concentrated Cost Pressures

The Intelligent Cloud division was the most closely watched business in Q1. Revenue for the quarter reached $34.681 billion, increasing by 30% year over year, slightly higher than the 29% growth rate from the previous quarter. Revenue from Azure and other cloud services grew by 40%, representing the most direct financial reflection of Microsoft's AI narrative.

However, this division also best explains the post-market pressure on the stock price. While revenue growth was high, costs increased even faster. The cost of revenue for the Intelligent Cloud division surged by approximately 47% year-over-year, significantly exceeding revenue growth, indicating that Microsoft is aggressively expanding its AI computing power and data center capacity. For investors, this raises two concerns: first, whether AI demand will be sufficient to absorb these capital expenditures over the long term; second, whether the profitability of the cloud business can be sustained amid rising depreciation and operational costs.

Based on this quarter’s performance, the answer remains somewhat positive but not perfect. Azure's 40% growth indicates robust demand, while the $627 billion in remaining commercial performance obligations suggests ample order backlog. However, the Intelligent Cloud division’s profit margin declined by approximately 1.8 percentage points year-over-year, reminding the market that AI infrastructure does not grow without costs.

Personal Computing: Windows and Xbox Underperform, Search Advertising Maintains Growth

The More Personal Computing segment, which includes the Windows operating system, Surface hardware, Xbox gaming consoles, and the video game company Activision Blizzard, reported Q1 revenue of $13.192 billion, down 1% year over year, an improvement compared to the 3% decline in the previous quarter, with a 3% decrease on a constant currency basis. This was the only one of Microsoft’s three business segments to report a revenue decline.

Specifically, Windows OEM and device revenue fell by 2%, or 3% when adjusted for constant currency, while Xbox content and services revenue declined by 5%, or 7% when adjusted for constant currency. This reflects ongoing cyclical pressures in the PC hardware and gaming content businesses.

The relative bright spot came from search advertising. Excluding traffic acquisition costs, search advertising revenue grew by 12% year-over-year, or 9% when adjusted for constant currency. This indicates that Bing, Edge, and AI-related search products are continuing to enhance their ad monetization capabilities.

The division's operating profit was $3.672 billion, representing a year-over-year increase of approximately 4%, with an operating margin of about 27.8%, up from approximately 26.4% in the same period last year. In other words, despite a slight decline in revenue, Microsoft maintained profit growth through cost control and improvements in business structure.

Upgraded performance updates help you stay ahead in seizing opportunities!Come and experience it >>

Editor/joryn