U.S. stocks remained range-bound ahead of the earnings reports from major technology companies, with the S&P index closing slightly lower. The Nasdaq rose by 0.04%. The yield on the 10-year U.S. Treasury bond increased by 7 basis points to 4.41%, reaching a new high since July 2025.Taiwan Semiconductor (TSM.US)ADR gained 0.38%, while AMD surged 4.3%.

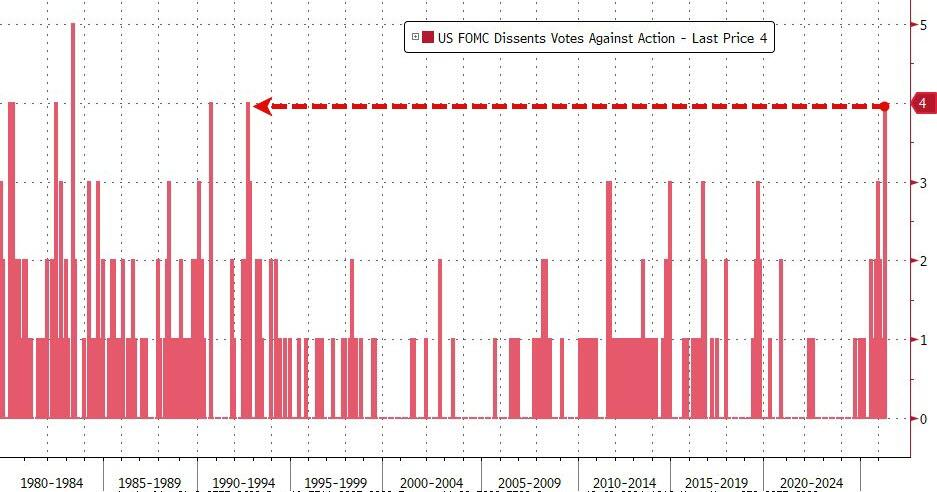

The Federal Reserve kept interest rates unchanged as expected but saw its most severe internal division in 34 years. Coupled with Brent crude hitting a new high since June 2022, U.S. Treasuries faced sell-offs, the dollar strengthened, and both gold and cryptocurrencies retreated in tandem.

U.S. stocks remained range-bound ahead of the earnings reports from major technology companies, with the S&P index closing slightly lower. The Nasdaq rose by 0.04%.

Earnings reports released after the market close quickly became the new focus: Meta's stock price fell after raising its capital expenditure outlook.Microsoft (MSFT.US)The growth of cloud business failed to dispel investors' concerns about artificial intelligence returns, while Alphabet rose due to robust sales data.

Earnings reports released after the market close quickly became the new focus: Meta's stock price fell after raising its capital expenditure outlook.Microsoft (MSFT.US)The growth of cloud business failed to dispel investors' concerns about artificial intelligence returns, while Alphabet rose due to robust sales data.

The Federal Reserve maintained interest rates unchanged, but this meeting saw four dissenting votes, making it the most divided decision since 1992.

Meanwhile, the Fed's statement underwent a significant adjustment, explicitly pointing out for the first time that 'developments in the Middle East are fueling high uncertainty in the economic outlook.'

Powell sent a hawkish signal at the press conference, stating that 'inflationary impacts related to oil still lie ahead,' and noted that the effects of energy price shocks on real economic growth typically take three to four months to appear in some consumer spending data.

Money markets promptly almost abandoned bets on rate cuts this year and began pricing in the possibility of a rate hike in 2027.

Jason Pride of Glenmede believes that if tensions de-escalate and energy prices do not significantly spill over into core inflation, there remains a baseline scenario of one to two rate cuts in the second half of the year.

This meeting also marks Powell’s final press conference as chair. The U.S. Department of Justice previously dropped its controversial criminal investigation into the Federal Reserve, clearing an obstacle for Kevin Warsh’s Senate confirmation process; the Senate Banking Committee had already advanced his nomination on the same day.

Powell stated that he would remain on the Federal Reserve Board. Jeffrey Roach of LPL Financial noted:

The phrasing of the statement suggests that the new chair will face additional headwinds when implementing a new policy framework after taking office.

Brent crude rose to its highest level since June 2022, while WTI crude surged 8.2% to $108.11 per barrel. Market concerns about a prolonged stalemate in the Strait of Hormuz have led to a rapid narrowing of global supply buffers.

Michelle Brouhard, Head of Policy and Geopolitical Risk at Kpler, stated:

The deadlock could persist for weeks, with the situation depending on whether global markets signal to Trump that such an oil shortage is unsustainable or Iran expresses a desire to resume oil exports.

Kpler data also shows that Iran’s crude oil storage capacity is rapidly running out, which may accelerate production cuts. Robert Yawger, Head of Energy Futures at Mizuho Securities, stated:

As long as there is no solution to end this turmoil or at least reopen the Strait of Hormuz, the market will continue to rise.

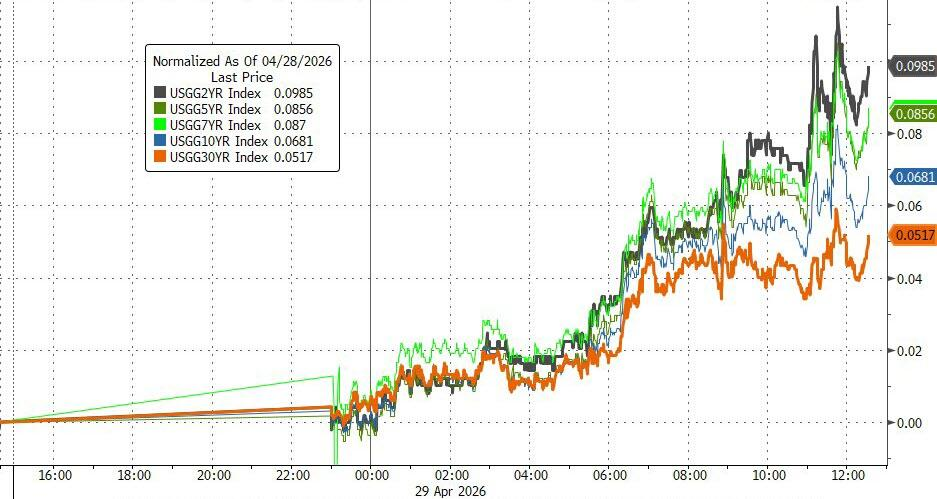

The surge in oil prices, combined with hawkish signals from the Federal Reserve, drove U.S. Treasury yields higher across the board. The 10-year yield rose by 7 basis points to 4.41%, reaching its highest level since July 2025.

The 2-year US Treasury yield surged 10 basis points in a single day to 3.93%, marking the largest increase of the day; the 30-year yield rose 5 basis points to 4.99%.

John Briggs, Head of North American Rate Strategy at Natixis, stated that the jump in front-end yields reflects the market's "recognition" that the continued blockade of the Strait of Hormuz will keep energy prices elevated, while the Fed’s overall stance has "clearly shifted towards hawkishness," further exacerbating the move.

Notably, the aforementioned bond sell-off occurred against the backdrop of the largest month-end pension rebalancing operation in recent times, where pensions typically reallocate equity positions into bonds at month-end, yet the bond market remained under pressure this time.

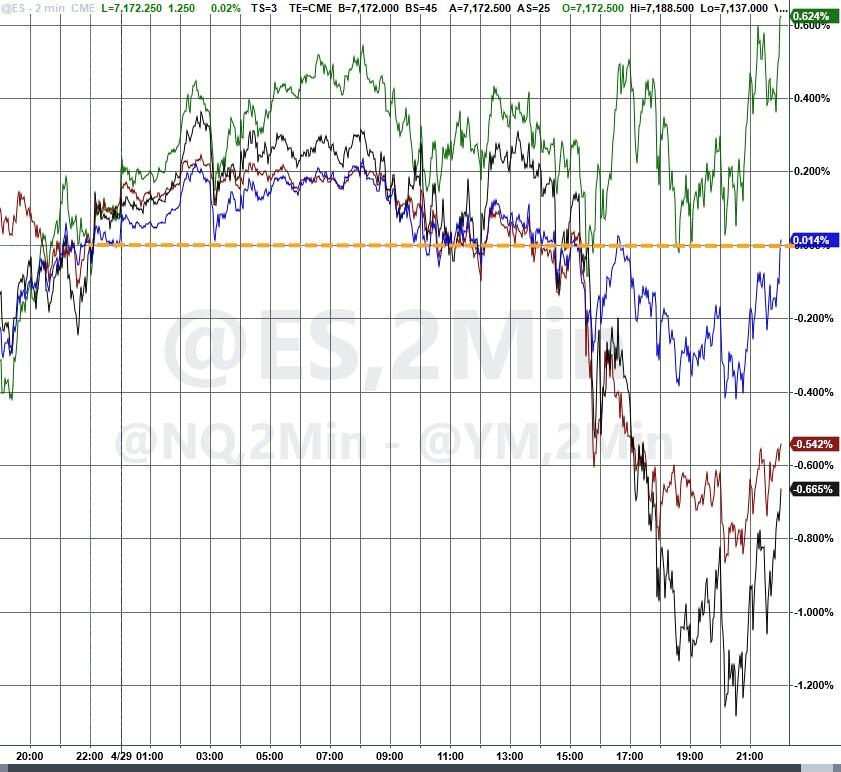

In the equity markets,$S&P 500 Index(.SPX.US)$closing levels were nearly flat,the Nasdaq 100 Index (.NDX.US)with the Nasdaq up 0.6%, the Dow Jones Industrial Average down 0.6%, and small-cap stocks performing the weakest.

It is worth noting that within 30 minutes of the FOMC statement release, the S&P 500 index briefly fell by 0.19%.

Goldman Sachs' trading desk observed low levels of market activity ahead of earnings reports, with shrinking trading volumes, and ETFs accounting for only 23% of total volume. Retail investor behavior has drawn attention.

According to Goldman Sachs’ latest fund flow report, retail participation in the 3x inverse semiconductor ETF (SOXS) and the 3x leveraged semiconductor ETF (SOXL) reached the 97th and 99th percentiles of a five-year look-back period, respectively, with both ends showing extreme crowding, posing significant risks as major technology companies prepare to release earnings.

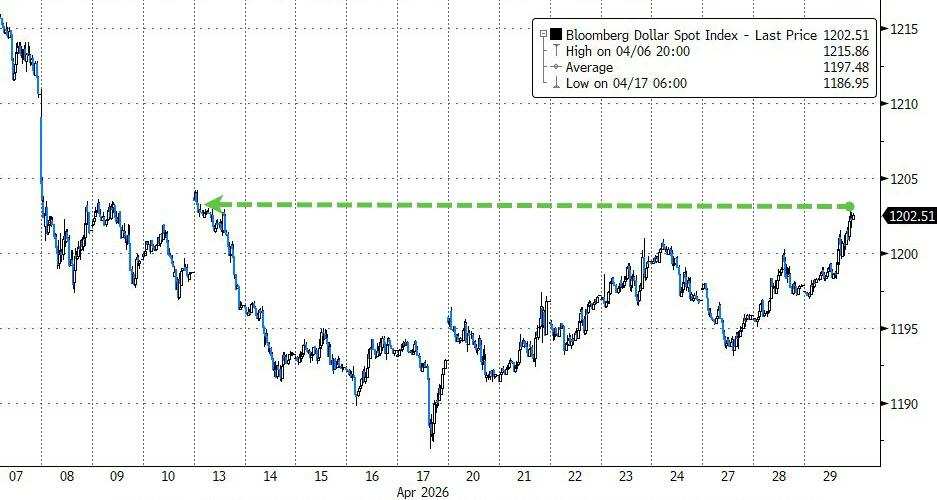

The US dollar strengthened, while gold and$Bitcoin (BTC.CC)$Synchronized decline.$美元指数(USDindex.FX)$The index rose by 0.4% on the day, reaching its highest level in nearly three weeks. Spot gold fell by 1.1%, retreating to a one-month low.

The cryptocurrency market faced synchronized pressure. Bitcoin exhibited an inverted V-shaped movement, rising by 1.8% at one point before dropping nearly 3% from its daily high and briefly falling below the $75,000 mark.

Trading sentiment on Wall Street was cautious on Wednesday. The S&P 500 Index closed slightly lower, the Nasdaq 100 edged up marginally, while the Dow Jones Industrial Average dropped by 0.6%, with small-cap stocks showing significant losses. Technology giants demonstrated relatively resilient performances.

U.S. benchmark indices:

The S&P 500 Index fell by 2.85 points, or 0.04%, to close at 7,135.95 points, displaying an overall W-shaped trend.

The Dow Jones Industrial Average declined by 280.12 points, or 0.57%, to close at 48,861.81 points.

The Nasdaq Composite Index rose by 9.441 points, or 0.04%, to close at 24,673.241 points. The Nasdaq 100 Index gained 157.973 points, or 0.58%, to close at 27,186.985 points.

Russell 2000 Index (.RUT.US)Closed down by 0.60% at 2,739.472 points.

The VIX Volatility Index, also known as the 'fear gauge,' rose by 5.33% to close at 18.78.

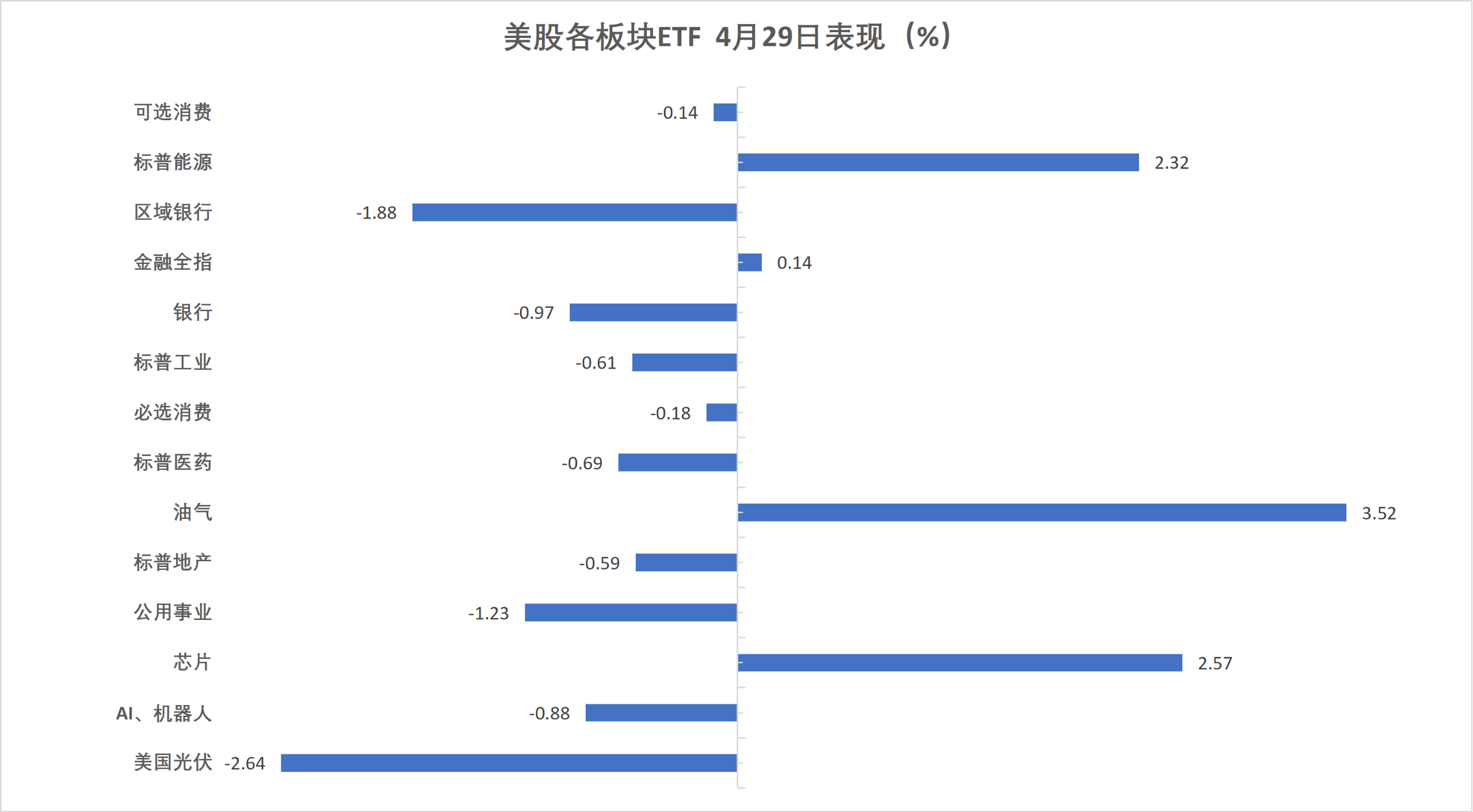

U.S. sector ETFs:

Oil and gas surged by 3.52%, the S&P Energy Sector gained 2.32%, and semiconductor stocks climbed by 2.57%. U.S. solar energy, however, fell by 2.64%.

Mag 7:

The Mag 7 index fell by 0.55% to close at 213.57 points.

$NVIDIA(NVDA.US)$A decline of 1.84%; Microsoft fell by 1.12%;$Tesla(TSLA.US)$A drop of 0.86%; Meta fell by 0.33%; Apple declined by 0.2%; Alphabet A rose by 0.05%;$Amazon(AMZN.US)$up 1.29%.

Chip Stocks:

Philadelphia Semiconductor Index (.SOX.US)Closed up by 235.72 points, gaining 2.35%, at 10,271.298 points.

Taiwan Semiconductor's ADR rose by 0.38%; AMD surged by 4.3%.

Chinese Concept Stocks:

The Nasdaq Golden Dragon China Index fell by 0.64% to close at 6,791.66 points, showing an overall long-tail L-shaped trend.

Among popular Chinese stocks,$Daquan New Energy (DQ.US)$A decline of 12.7%;$Pony AI (PONY.US)$A drop of 6.7%;Zai Lab (ZLAB.US)Down 6.1%,$Baidu (BIDU.US)$Down 3.8%, XPeng down 1.8%, Xiaomi, Tencent, and Alibaba down at least approximately 0.3%.

Other individual stocks:

$Circle(CRCL.US)$Up 1.32%.

Stocks related to storage, hydrogen energy, Apple-related concepts, computer hardware, and optical communication were among the top gainers.$NXP Semiconductors (NXPI.US)$Up more than 25%, Intel up over 12%,a hard drive manufacturer, Surging over 11%, $Lumentum(LITE.US)$ rose over 8%.$SanDisk (SNDK.US)$surging over 6%,$Western Digital (WDC.US)$Up more than 5%,Qualcomm (QCOM.US)with gains exceeding 4%.$HP Inc (HPQ.US)$、$Micron Technology(MU.US)$Up more than 2%. Cryptocurrency-related stocks and precious metals were among the top losers, $SoFi Technologies(SOFI.US)$ Down more than 15%,$Robinhood(HOOD.US)$Down more than 13%,Coinbase、$Golden Resource (GORO.US)$dropping over 6%,$Pan American Silver (PAAS.US)$Down more than 2%.

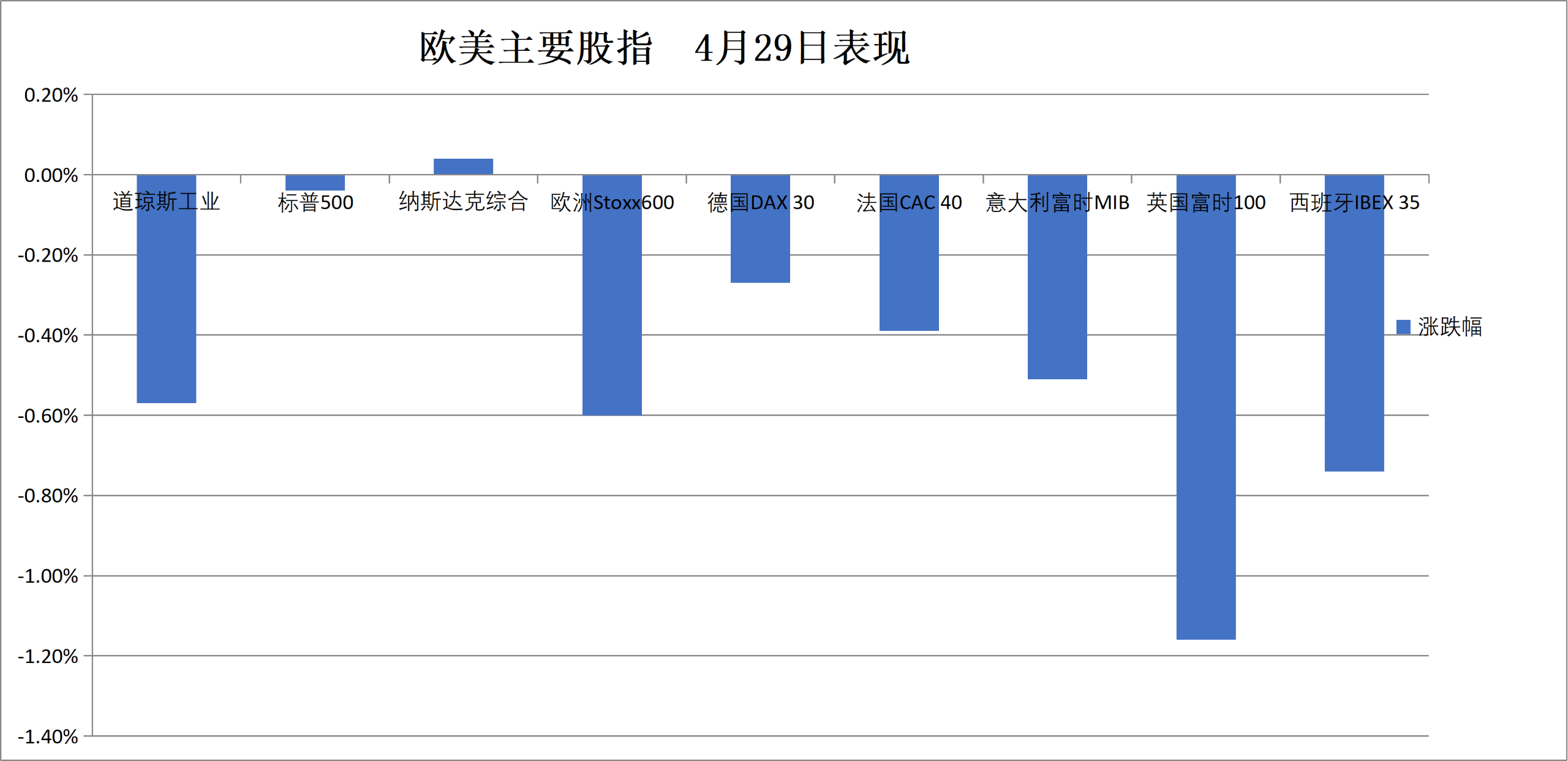

The UK stock market closed down more than 1.1%, the Danish stock index fell over 1.8%, and the Italian banking sector dropped more than 0.5%.

Pan-European stocks:

The European STOXX 600 Index closed down 0.65% at 602.64 points.

The Eurozone STOXX 50 Index closed down 0.34% at 5816.48 points.

Major Stock Indexes Around the World:

The German DAX 30 Index closed down 0.27% at 23954.56 points.

The French CAC 40 Index closed down 0.39% at 8072.13 points.

$FTSE 100 Index (.FTSE.GB)$Closed down 1.16% at 10213.11 points.

Sector and Stock Performance:

Among the blue-chip stocks in the Eurozone, Munich Re closed down 3.23%, ENEL fell 2.79%, Inditex Group dropped 2.35%, BMW declined 2.27%, and L'Oréal fell 2.17%.

Among all the constituent stocks of the European STOXX 600 Index, Kone Corporation closed down 13.54%, Aeroports de Paris fell 7.01%, and St James's Place Public Limited Company dropped 5.99%.GlaxoSmithKline (GSK.US)Dropped by 5.42%, ranking as the fifth-largest decline.

During Powell's final press conference, the yield on the two-year U.S. Treasury note rose above 3.95%.

U.S. Treasuries:

In late New York trading, the yield on the benchmark 10-year U.S. Treasury note increased by 8.62 basis points, reaching a new intraday high of 4.4318%.

The yield on the two-year U.S. Treasury note rose by 11.08 basis points to 3.9468%, trading within a range of 3.8340%-3.9510% during the day and hitting a new intraday high after Powell’s press conference began.

European debt:

At the European market close,$German 10-Year Government Bond Yield (DE10Y.BD)$Increased by 4.3 basis points to 3.110%, trading within a range of 3.058%-3.118% during the day.

The yield on the UK 10-year government bond (GB10Y.BD)Rose by 4.7 basis points to 5.053%.

$The yield on the 10-year French government bond (FR10Y.BD)$Increased by 4.5 basis points to 3.769%; the yield on the two-year French government bond rose by 8.0 basis points, reaching a new intraday high of 2.876%.

The U.S. Dollar Index rose more than 0.3% on the day of 'Powell’s final press conference.' Bitcoin showed an inverted V-shaped movement, rising by 1.8% at one point but then falling nearly 3% from its daily high and briefly dropping below the $75,000 mark.

US Dollar:

In late New York trading, the ICE U.S. Dollar Index gained 0.33% to 98.968 points, trending upward with persistent fluctuations throughout the day, trading within a range of 98.565-99.050 points.

The Bloomberg U.S. Dollar Index rose by 0.40% to 1202.65 points, trading within a range of 1196.91-1203.27 points during the day.

Yen:

In late New York trading, the US dollar rose 0.51% against the Japanese yen.

The euro rose 0.14% against the Japanese yen, while the British pound rose 0.16% against the Japanese yen.

Offshore Renminbi:

In late New York trading, the US dollar was quoted at 6.8474 yuan against the offshore renminbi, up 72 points from Tuesday's late New York session, with intraday trading ranging between 6.8313 and 6.8493 yuan.

Cryptocurrency:

Bitcoin reversed in an inverted V-shaped trend in late New York trading, rising as much as 1.8%, before dropping nearly 3% from its daily high and briefly breaking below the $75,000 mark.$Ethereum (ETH.CC)$Down 2.4% on the day.

NYMEX May natural gas futures settled at $2.647 per million British thermal units.

Crude Oil:

WTI June crude oil futures settled at $106.88 per barrel.

NYMEX May gasoline futures settled at $3.7411 per gallon.

Natural Gas:

NYMEX May natural gas futures settled at $2.647 per million British thermal units.

Gold hit a fresh daily low during early US stock trading. During the Federal Reserve’s policy announcement and Powell's press conference, it traded near $4,540 per ounce. Copper prices gave up earlier gains and fell for a fifth consecutive session amid macroeconomic concerns.

Gold:

At the New York close, spot gold fell by 1.15% to USD 4,544.05 per ounce, continuing its overall downtrend, with trading ranging between USD 4,610.29 and USD 4,510.32.

Silver:

At the New York close, spot silver dropped by 2.44% to USD 71.2949 per ounce.

Other metals:

LME copper futures closed down USD 32 at USD 13,004 per tonne. LME aluminum futures closed down USD 50 at USD 3,488 per tonne.

LME tin futures closed down USD 201 at USD 48,753 per tonne. LME nickel futures closed down USD 178 at USD 19,272 per tonne.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/Liam