$Amazon (AMZN.US)$ The first quarter delivered a robust financial report with substantial growth in both revenue and profitability; however, significant cost increases due to aggressive AI investments reignited investor concerns over profit margins and consumer demand.

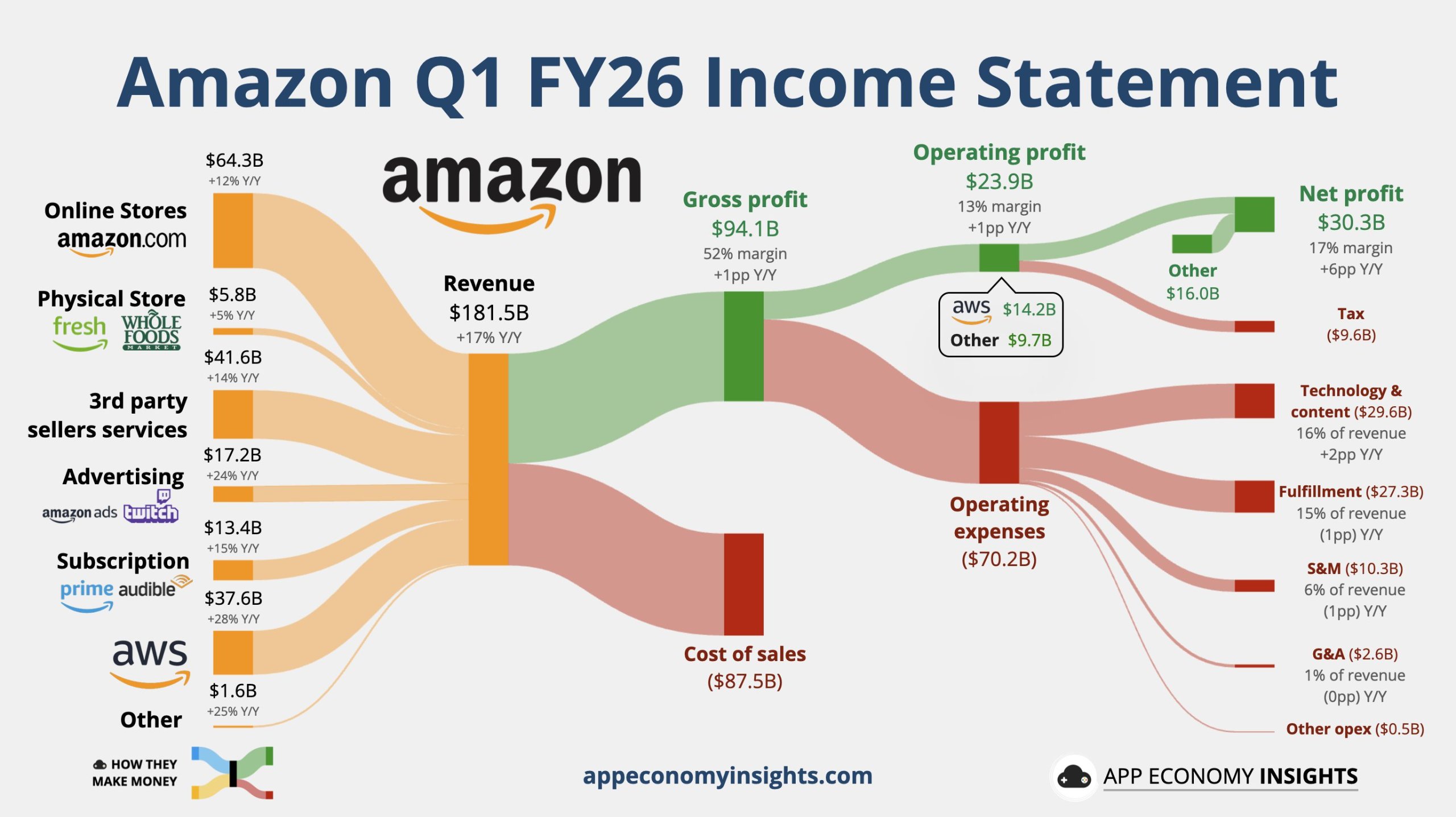

Amazon's first-quarter revenue and earnings per share (EPS) exceeded expectations, with year-over-year growth of 17% and 74%, respectively. Operating profit surged by approximately 30% year over year, while the overall operating margin improved from 11.8% in the same period last year to a record 13.1%. A major driver of this profit surge was gains from Amazon’s investment in Anthropic, a key rival of OpenAI, with pre-tax profits from this investment accounting for more than half of the quarter’s net profit.

AWS, Amazon's closely watched cloud computing services business, reported a 28% year-over-year increase in revenue, marking the highest quarterly growth rate in nearly four years. AWS remains Amazon's most critical profit contributor, generating nearly 60% of the company’s operating profit in the first quarter.

Amazon provided equally strong guidance for the second quarter. The midpoint of its net sales forecast stands at $196.5 billion. The lower end of the operating profit guidance range reflects a 4.2% year-over-year increase, while the upper end shows a 25% rise. Amazon also noted that Prime Day will take place in the second quarter, providing a boost to Q2 revenue.

Amazon provided equally strong guidance for the second quarter. The midpoint of its net sales forecast stands at $196.5 billion. The lower end of the operating profit guidance range reflects a 4.2% year-over-year increase, while the upper end shows a 25% rise. Amazon also noted that Prime Day will take place in the second quarter, providing a boost to Q2 revenue.

After the earnings report was released, Amazon's shares, which had closed up about 1.3% on Wednesday, initially turned negative in after-hours trading, falling nearly 4%. During the earnings call, the stock reversed its losses and rose nearly 5% at one point; during the U.S. overnight session, it gained more than 2%.

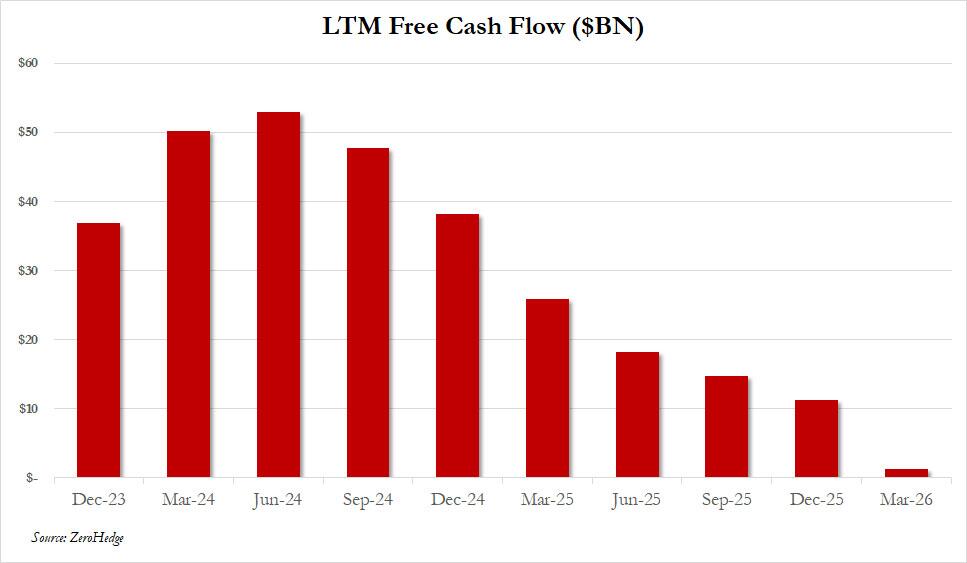

Analysts believe that the post-market price decline did not reflect skepticism about the quality of earnings growth but rather indicated investors’ heightened focus on more sensitive metrics such as cash flow and capital expenditures. In Q1, Amazon spent $44.203 billion on property and equipment, exceeding market expectations. Over the trailing twelve months as of quarter-end, such spending totaled $151 billion, a 160% year-over-year increase. Free cash flow over the past twelve months plummeted by 95% year-over-year to $1.232 billion, largely consumed by investments in AI infrastructure.

Investor concerns initially centered on AI-related capital expenditures significantly exceeding expectations, squeezed free cash flow, and elevated EPS due to gains from Anthropic investments. Subsequently, attention shifted to AWS’s reacceleration, strong revenue guidance for Q2, and the short-term growth certainty brought by the earlier timing of Prime Day. During the earnings call, Amazon confirmed that Prime Day would move from July to June.

Revenue and Profit Surpass Expectations with Double-Digit Growth; Net Profit Amplified by Gains from Anthropic Investment

Amazon's total revenue for the first quarter reached $181.519 billion, representing a 17% year-over-year increase, higher than the 14% growth rate in the fourth quarter. Excluding a favorable currency impact of $2.9 billion, revenue grew by 15% year over year.

From a revenue structure perspective, service revenue grew faster, with net service sales reaching $110.215 billion in Q1, up approximately 20% year-over-year, surpassing the roughly 12% growth rate of product sales. This trend continued to shift the revenue mix toward higher-margin businesses.

On the profit side, Amazon's operating profit surged by 30% year over year to $23.852 billion in the first quarter, significantly accelerating from the 17.9% growth rate in the fourth quarter. This indicates that the company is still unlocking operational leverage across multiple lines of business, including retail fulfillment, advertising, and cloud services.

Total operating expenses in the first quarter amounted to USD 157.667 billion, representing an increase of approximately 15% year-over-year, which was lower than the revenue growth rate. Sales and marketing expenses grew by only about 6%, while general and administrative expenses slightly declined.

However, the substantial growth in net profit needs to be analyzed in detail. Net profit in the first quarter reached USD 30.255 billion, a year-over-year increase of 77%. Amazon disclosed that this figure included a pre-tax non-operating gain of USD 16.8 billion from its investment in Anthropic. This USD 16.8 billion accounts for more than half of the total net profit.

In other words, the 'impressive' performance of GAAP net profit and EPS is partly driven by gains from investment fair value rather than entirely by improvements in core business operations. Consequently, the market is paying closer attention to operating profit, AWS growth, and cash flow rather than solely focusing on EPS beats.

AWS: Accelerated Growth Driven by AI Demand but with Rising Capital Intensity

AWS was the standout positive highlight in the first-quarter earnings report. The segment generated revenue of $37.587 billion during the quarter, up 28% year over year—the highest quarterly growth rate since the second quarter of 2022—marking a notable acceleration compared to the 17% growth rate in the same period last year.

Over the past few quarters, AWS’s revenue growth rate has steadily increased from 17%, 20%, and 24% to 28% in the current quarter, reflecting that enterprise cloud spending and AI-related demand are once again driving Amazon's cloud business.

AWS’s operating profit in the first quarter was USD 14.161 billion, representing a year-over-year increase of 23%. The operating margin improved to 37.7% from 35.0% in the previous quarter but remained below the 39.5% recorded in the same period last year. This reflects two trends: on one hand, AWS continues to demonstrate strong profitability; on the other hand, investments in AI computing power, chips, data centers, and depreciation costs are exerting pressure on profit margins.

Company management emphasized that AWS is currently in an expansion cycle for AI infrastructure. Amazon’s annualized revenue run rate for its self-developed chip business has exceeded USD 20 billion, maintaining triple-digit year-over-year growth. Over the past 12 months, the company has deployed more than 2.1 million AI chips, with over half being Trainium. Additionally, OpenAI has committed to utilizing approximately 2 GW of Trainium computing power through AWS infrastructure, while Anthropic will also secure up to 5 GW of Trainium chip resources.

These orders and customer commitments have enhanced the visibility of AWS’s future growth and explained the surge in capital expenditures. However, for investors, the key question becomes: when will such large-scale AI investments translate into sufficiently high cash returns?

North American Retail: Simultaneous Realization of Scale Growth and Efficiency Improvement

In the first quarter, Amazon's North American operations generated revenue of $104.143 billion, a year-on-year increase of 12%; operating profit reached $8.267 billion, up 42% year-on-year, with the operating margin rising from 6.3% in the same period last year to 7.9%. This is an important signal of improvement in Amazon's core retail business.

The company disclosed that the number of paid items globally increased by 15% year-on-year, marking the highest growth rate since the end of COVID-19 lockdowns. Meanwhile, online store revenue amounted to $64.254 billion, a year-on-year increase of 12%, while third-party seller services revenue reached $41.578 billion, up 14% year-on-year. This indicates that demand for Amazon's e-commerce platform has not significantly weakened, and platform-driven income continues to grow faster than direct sales of self-operated goods.

However, fulfillment and delivery costs continue to rise. Global shipping costs reached $25.709 billion, a year-on-year increase of 14%, close to the growth rate of item volumes. Amazon continues to promote faster delivery options, including one-hour and three-hour delivery for more than 90,000 products in the United States, as well as expanding ultra-fast delivery services like Amazon Now. While faster delivery helps enhance customer stickiness and order frequency, it also implies that continuous investment in logistics infrastructure remains necessary.

International Business: Profitability Continues to Improve, but Currency Effects Play a Significant Role

In the first quarter, international business revenue reached $39.789 billion, a year-on-year increase of 19%; however, excluding currency effects, the growth rate was 11%. This suggests that favorable exchange rates have made a substantial contribution to the strong overseas performance.

On the profit side, international business operating profit amounted to $1.424 billion, higher than $1.017 billion in the same period last year, with the operating margin increasing from 3.0% to 3.6%. However, the company disclosed that favorable currency impacts contributed approximately $347 million to international business operating profit, meaning that the year-on-year increase in operating profit, excluding currency effects, was only about 6%.

This indicates that profitability in international markets is indeed improving, though the extent of improvement is not as robust as the headline figures suggest. Compared to years of losses from overseas operations weighing on profits, Amazon’s international business has now entered a phase of sustained profitability, which remains a positive signal in the earnings report.

Advertising and Subscriptions: High-margin Service Revenue Continues to Expand

The advertising business remains a key pillar of Amazon’s profit structure. In the first quarter, advertising service revenue reached $17.243 billion, a year-on-year increase of 24%; excluding currency effects, growth was 22%. The company stated that advertising revenue over the past 12 months has exceeded $70 billion.

Amazon's advertising advantages stem from retail search, shopping data, Prime Video, and collaborations with external platforms. The company mentioned this quarter that advertisers can utilize Amazon Audiences for Netflix ad placements to reach target audiences through Amazon shopping, streaming, and browsing signals. Brand prompts in the AI shopping assistant Rufus and Sponsored Products are also expanding the scope of ad monetization.

Subscription services revenue reached $13.427 billion, a year-over-year increase of 15%, including non-AWS subscription businesses such as Prime membership, video, music, and e-books. The continuous growth of advertising and subscriptions has further increased the proportion of Amazon’s service revenue, providing a buffer for overall profitability.

Q2 Guidance: Revenue Significantly Exceeds Expectations While Profit Guidance Midpoint Slightly Misses Expectations

Amazon forecasts Q2 net sales between $194 billion and $199 billion, representing a year-over-year growth of 16% to 19%. The midpoint of the range at $196.5 billion is notably higher than the market consensus midpoint of $189.15 billion.

Based on the midpoint of the guidance, Amazon expects Q2 revenue to grow by 17.2% year-over-year, reflecting robust growth. However, it is important to note that the company assumes Prime Day will occur in Q2, thus some of the increase is attributed to changes in promotional timing.

The guidance for operating profit ranges from $20 billion to $24 billion, compared to $19.2 billion in the same period last year. While the midpoint of $22 billion falls slightly below expectations, the revenue guidance clearly surpasses forecasts. Therefore, the profit guidance does not constitute an unequivocal 'beat' like the revenue guidance.

This is one reason for the after-hours stock price pressure: investors recognize strong revenue elasticity but also observe that more revenue may be absorbed by investments in AI infrastructure, logistics acceleration, depreciation, and operational expenditures. In other words, the market is not questioning growth but is reassessing whether incremental revenue can convert into free cash flow quickly enough.

Upgraded performance updates help you stay ahead in seizing opportunities!Come and experience it >>

Editor/joryn