The blockade of Hormuz has torn a "black hole" in global supply, with over 10% of crude oil supply vanishing overnight. Yet, the rise in oil prices remains "moderate"—the release of reserves is masking the true extent of the crisis. JPMorgan has warned: once inventories are depleted, Brent crude will soar to $150 per barrel, pushing global CPI annualized rates above 10% within three months and elevating the probability of a recession to 35%. Whether the strait can be reopened is now the sole variable determining the fate of the global economy.

This is an unprecedented energy shock — the 'black hole' on the supply side has opened, but market price signals have yet to fully awaken. Rapid inventory drawdowns, the release of strategic reserves, and optimistic expectations for a short-term reopening of the Strait have temporarily contained the explosive rise in oil prices.

However, the warning from JPMorgan economists is clear and stark: once inventories fall to operational minimums, a nonlinear price surge will become inevitable, and the fate of global economic expansion will be rewritten at that moment.

An unprecedented supply shock: Why has the increase in oil prices been so 'moderate'?

The blockade of the Strait of Hormuz has removed over 10% of global crude oil production — an unprecedented figure.

The blockade of the Strait of Hormuz has removed over 10% of global crude oil production — an unprecedented figure.

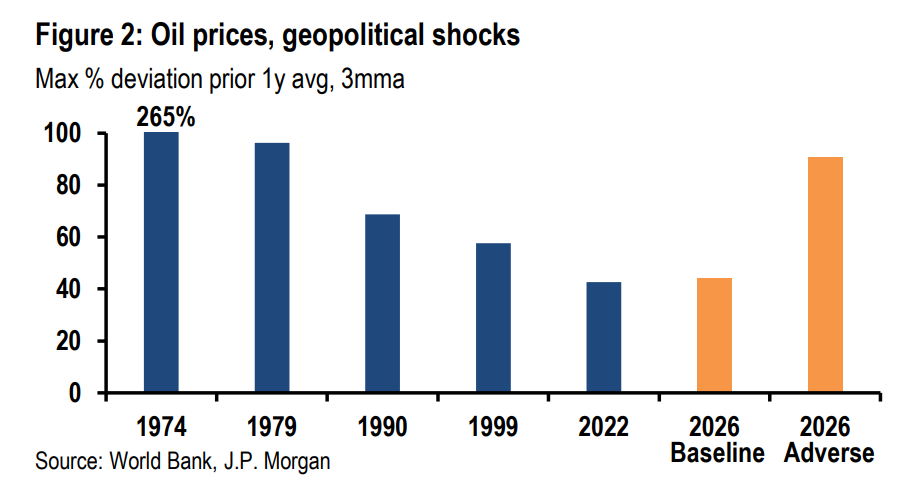

Nevertheless, Brent crude futures for April are only about 43% higher than the average over the past year, which appears 'restrained' compared with historic shocks such as those in 1973-74 and 1979.

The reason lies in the simultaneous activation of three buffering mechanisms: the large-scale release of commercial inventories and strategic reserves, optimistic expectations for the imminent reopening of the Strait, and spontaneous contraction on the demand side.

But JPMorgan explicitly pointed out that this 'calm' is fragile — once inventories are depleted to operational minimums, prices will face a nonlinear violent surge.

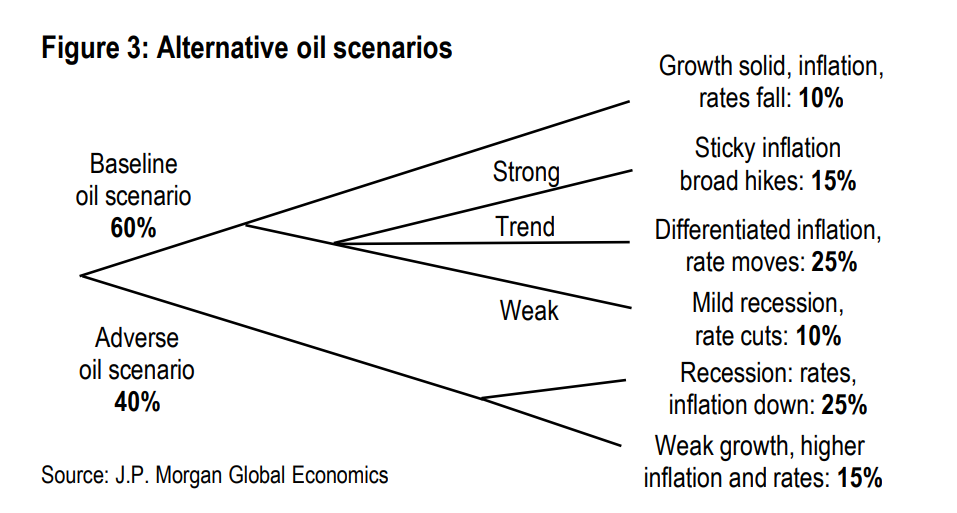

A two-scenario framework: baseline vs. adverse, the stark contrast between two worlds

JPMorgan has constructed two clear scenario pathways:

Baseline scenario (60% probability): The Strait reopens within the next few weeks. Brent crude oil's average price for this quarter is projected to reach $100 per barrel, then gradually decline, stabilizing at $80 per barrel by the fourth quarter of 2026.

The energy price shock will reduce the cumulative level of global GDP by 0.6% while pushing up the cumulative level of CPI by approximately 1%. Global growth is returning to its potential level, employment is recovering, the Federal Reserve is maintaining interest rates, and the European Central Bank is moving towards rate hikes.

Adverse scenario (40% probability): The blockade of the strait persists, with Brent crude oil surging to $150 per barrel over three months from May to July, followed by an incomplete retreat to about $110 per barrel in the fourth quarter.

Model estimates show that this scenario would reduce the cumulative level of global GDP by 1.6% and increase the cumulative level of CPI by 2.2%. The global economy would fall into stagflation, with recession risks rising significantly, potentially becoming a historic shock more severe than in 2022 and closer in magnitude to those of 1979 and 1990.

The probability of a global economic recession remains at a high of 35%, consistent with JPMorgan's assessment at the beginning of the year. Although strong growth momentum at the start of the year temporarily reduced recession risks, the outbreak of conflict in the Middle East posed an equivalent offsetting threat.

Three pillars of resilience supporting the baseline scenario

JPMorgan’s relatively optimistic baseline judgment is based on three layers of support for the underlying resilience of the global economy:

A robust engine of technology capital expenditure. Against the backdrop of explosive growth in AI-related capital demand, global capital expenditure grew by 5.1% over the past four quarters, with the United States recording double-digit growth.

JPMorgan’s real-time forecasting model for capital expenditure shows annualized growth tracking at 7% for global capital expenditure as of the first quarter of 2026. This wave of demand is strongly boosting Asian exports, with manufacturing output in related regions surging 12% on an annualized basis over the three months ending February this year.

Corporate profit recovery boosts confidence. Global corporate profits are expected to grow by 20% year-over-year in 2025, driving a significant rebound in business sentiment from depressed levels.

JPMorgan forecasts that as corporate caution eases, global employment growth will rebound to an annualized rate of 0.8% by mid-year, with average monthly increases in U.S. nonfarm payrolls returning to above 100,000.

The ability of households to smooth consumption. Despite a significant slowdown in employment growth, global consumer spending still recorded a robust annualized growth of 2% last year, supported primarily by fiscal stimulus, wealth effects, and credit channels.

Taking the United States as an example, households have maintained consumption by significantly lowering the personal savings rate, implying that this quarter’s 5% CPI shock will need to be absorbed through a further reduction in the savings rate.

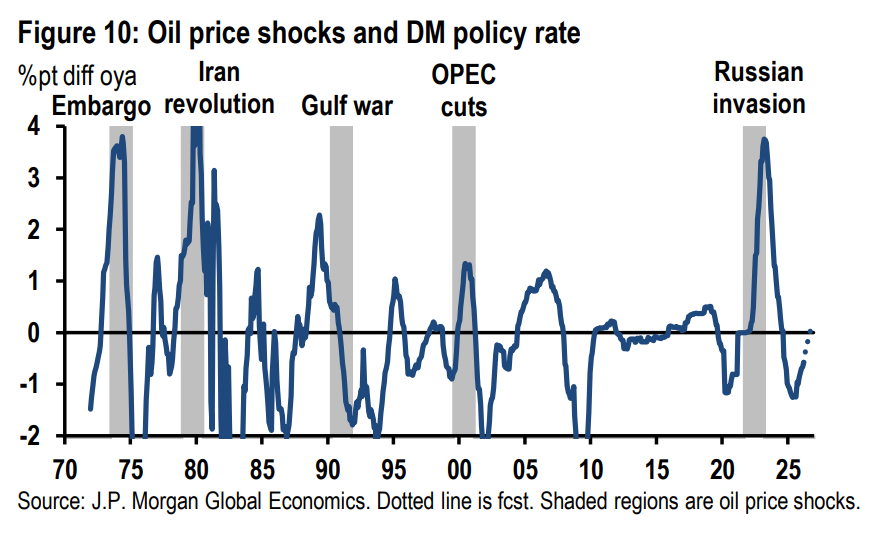

Central bank 'patience' – this time, it really is different.

History shows that aggressive tightening policies by central banks during various energy price shocks have often been a core factor amplifying economic downturns. During the two oil crises of the 1970s, policy rates in advanced markets surged significantly, contributing heavily to the global economic recession.

However, the current macroeconomic backdrop is entirely different.

Prior to this round of energy shocks, wage growth and core inflation had already been cooling persistently, with weak employment growth. Central banks had just concluded an easing cycle involving a total of 140 basis points in interest rate cuts, with the lagged effects of monetary policy gradually releasing stimulative forces. Meanwhile, the current financial conditions index remains at historically accommodative levels – such low levels of financial stress during a major global energy shock are unprecedented.

In the baseline scenario, the Federal Reserve is expected to remain on hold for the entire year, while the European Central Bank tends to raise interest rates.

If adverse scenarios materialize, JPMorgan believes that the Federal Reserve will not proactively raise interest rates solely due to oil price shocks. However, the risk of broader, synchronized tightening by major central banks will increase significantly, becoming a key variable determining financial conditions and overall economic resilience.

Inflation trajectory: Synchronized upward movement, but divergence intensifies.

Global inflation has remained consistently high over the past three years, averaging approximately 3% annually. The energy price shock is expected to push CPI growth further upward to an annualized rate of 5% this quarter, with full-year CPI increases projected to reach 4%.

However, there is a clear divergence in the trajectory of core inflation—core PCE inflation in the United States is projected to remain above 3% this year; inflation in Canada and continental European countries is expected to approach the 2% policy target; emerging markets as a whole are anticipated to exhibit a 'sticky, moderately high' state.

This divergence will directly lead to a divergence in global monetary policy paths, providing an important reference for relative value opportunities across asset classes.

Three 'fatal variables' in adverse scenarios

If the blockade of the Strait of Hormuz persists, JPMorgan has identified three critical risk points that could amplify nonlinear impacts:

A nonlinear spiral of soaring prices and supply shortages. Cumulative production cuts triggered by a prolonged blockade may induce panic-driven precautionary demand, driving oil prices far beyond the forecasted level of $150 per barrel. The depletion of strategic reserves will further trigger physical supply constraints, creating a vicious cycle where price increases and supply shortages reinforce each other.

Deep-seated vulnerabilities at the behavioral level. The current global economic expansion exhibits structural imbalances—technology demand is booming, but spending and employment in non-tech sectors remain weak overall, with household savings rates having been significantly compressed.

If Brent crude rises to $150 per barrel or higher, it will push global CPI to a peak annualized rate of 10% within three months, severely undermining consumer confidence and threatening the normalization of business sentiment that has just begun, thereby exerting a secondary blow to household income through slowing job demand.

The risk of central banks losing patience. In response to the initial inflation shock, central bank policies will diverge. JPMorgan expects the Federal Reserve not to raise interest rates as a direct reaction to the oil price shock, but if multiple central banks simultaneously tighten, it will have a decisive impact on financial conditions and overall economic resilience, potentially repeating the policy missteps seen during the 2021-23 inflation control cycle.

Editor/Lee