Apple's second-quarter performance may exceed expectations, but the market is closely watching two key variables: the strategic direction under successor John Ternus and the impact of surging memory prices on profit margins. Amid Tim Cook's transition of leadership, the company faces dual pressures of elevated valuation and slowing growth. If Apple can stabilize gross margins through price increases and cost hedging, coupled with innovation catalysts from the new CEO, there remains upside potential for the stock.

$Apple (AAPL.US)$ The company released its second-quarter earnings after the U.S. stock market closed on Thursday (early morning Beijing time). However, investors have already looked beyond the numbers themselves, focusing on two core issues: the strategic direction of John Ternus, the incoming CEO, and the potential impact of surging memory chip costs on profit margins. The trajectory of these two variables will largely determine whether Apple's stock can break out of its underperformance relative to the broader market since the beginning of this year.

Apple announced last week that current CEO Tim Cook will transition to the role of executive chairman, and John Ternus, head of hardware engineering, will officially take over as CEO on September 1. This leadership change was announced a week before the earnings release. Ben Reitzes, head of technology research at Melius Research, noted in a report to investors that the timing of the announcement was intriguing, stating, "My intuition tells me that this announcement was deliberately timed before the earnings release to allow the market to focus on a fundamentally strong and outstanding quarter when Apple reports its results." Analysts generally believe that Cook’s decision to step down at a high point aligns with his consistent approach.

Wall Street expects Apple to report a 19% increase in profits and a 15% rise in revenue. JPMorgan forecasts second-quarter revenue of $112.7 billion, surpassing the consensus market expectation of $109.6 billion, with earnings per share projected at $2.05, higher than the market expectation of $1.96. However, beyond the revenue figures, the trend in gross margin and the new CEO’s strategic statements will be the true focal points of this earnings call.

Wall Street expects Apple to report a 19% increase in profits and a 15% rise in revenue. JPMorgan forecasts second-quarter revenue of $112.7 billion, surpassing the consensus market expectation of $109.6 billion, with earnings per share projected at $2.05, higher than the market expectation of $1.96. However, beyond the revenue figures, the trend in gross margin and the new CEO’s strategic statements will be the true focal points of this earnings call.

Earnings figures are expected to exceed expectations, but buyers' focus is on profit margins.

According to a JPMorgan research report, Apple's second-quarter performance is expected to surpass market expectations on the revenue side, primarily driven by robust demand for the iPhone 17 series and the recent launch of MacBook Neo.

JPMorgan forecasts iPhone revenue at $59.5 billion, representing approximately 27% year-over-year growth, exceeding the consensus market expectation of $56.7 billion. Mac revenue is projected at $8.6 billion, also above the market expectation of $8.2 billion. Service business revenue is estimated at $30.4 billion, in line with market expectations.

JPMorgan noted that revenue exceeding expectations is already anticipated by buyers, with the real test lying in the performance and guidance of gross margins. The firm expects the second-quarter gross margin to be 48.5%, in line with the midpoint of the company’s guidance range and slightly above the consensus market expectation of 48.4%.

For the third quarter, JPMorgan predicts that the gross margin will decline slightly to 47.6% following seasonal patterns, closely aligning with the market expectation of 47.7%. The firm believes that Apple, leveraging pre-purchased inventory and advantageous contract prices secured through economies of scale, is capable of maintaining the seasonal trend of gross margins despite memory cost pressures, thereby boosting confidence in its resilience.

Memory costs are the biggest variable, and pricing strategies for the iPhone 18 are under scrutiny.

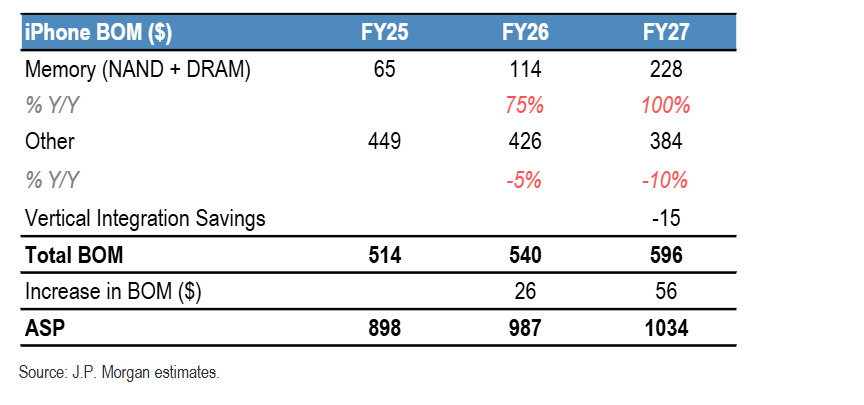

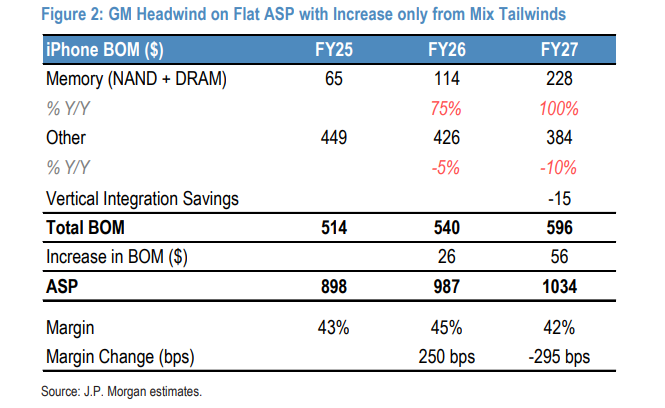

The sharp rise in memory chip prices represents Apple's largest current cost pressure.

According to Bloomberg data, the DRAM spot price index has surged over 500% since the end of August last year. JPMorgan’s supply chain research shows that the memory bill of materials (BOM) cost for Apple's iPhone will be approximately $65 per unit in FY25, expected to rise to $114 in FY26, and further jump to $228 in FY27, with NAND and DRAM combined accounting for over $200 of the iPhone 18 BOM cost.

In response to this pressure, JPMorgan’s base-case scenario assumes that Apple will implement a moderate price increase in the mid-single digits for the iPhone 18, with the average selling price rising by an additional $50 compared to the mix-driven base case, approaching $1,000.

The bank estimates that if Apple maintains current pricing and relies solely on product mix upgrades, the iPhone gross margin will face a hit of about 300 basis points, with the overall company gross margin under pressure by approximately 200 basis points; however, in the $50 price increase base case, the iPhone gross margin pressure could narrow to around 30 basis points, with an overall gross margin impact of about 20 basis points.

JPMorgan also pointed out that Apple has multiple hedging strategies:

First, leveraging scale advantages to compress non-memory component costs, with an estimated 10% year-over-year decline in non-memory BOM costs by FY27.

Second, replacing Qualcomm solutions with in-house modems, further reducing the BOM growth in FY27.

David Wagner, Portfolio Manager at Aptus Capital Advisors, stated, "The stocks most impacted are often those showing deteriorating profit margins. If memory cost pressures persist, it will start to pose a profit margin risk for Apple, and given the current valuation, downside risks cannot be ignored."

CEO transition raises questions about strategic direction.

John Ternus’s appointment as CEO makes this earnings call strategically significant far beyond the financial figures themselves.

Ternus has led the development of several key hardware products at Apple, but his strategic focus between hardware and services, as well as his leadership style amid a volatile macroeconomic environment, remains uncertain. It is currently unclear whether Ternus will attend this earnings call, and Apple’s spokesperson declined to comment.

Anthony Saglimbene, Chief Market Strategist at Ameriprise, stated, "The real focus of this earnings report is not on the numbers; we want to understand how the CEO transition will unfold."

Matt Stucky, Chief Portfolio Manager for Equities at Northwestern Mutual Wealth Management Company, pointed out that Apple is currently trading at approximately 30 times its forward price-to-earnings ratio, a significant premium compared to its 10-year average of around 23 times. Among technology stocks, its valuation ranks second only to Tesla. "If the new CEO’s innovations can provide growth catalysts, there is justification for sustained optimism, potentially driving valuations even higher. However, if the strategy merely involves steadily expanding market share and maintaining product updates, it would be positive but not transformative."

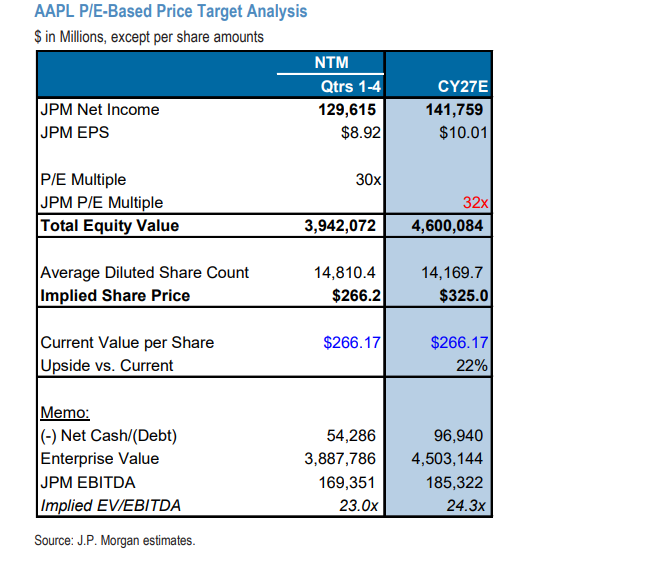

JPMorgan maintained its 'Overweight' rating on Apple with a December target price of $325, corresponding to approximately 32 times the CY27 forward price-to-earnings ratio, offering about 22% upside potential from the current share price of roughly $266. The bank also noted that the CEO transition poses company-specific risks. Tim Cook’s unparalleled execution during his tenure has set an extremely high benchmark, and whether the new leadership can sustain this level of execution remains uncertain.

High Valuation, Accelerated Growth Yet to Be Validated

Apple's stock price has fallen by less than 1% year-to-date, while the Nasdaq 100 Index has risen by 7.7%, and the S&P 500 Index has increased by 4.2%. This underperformance has further highlighted valuation pressure. JPMorgan expects Apple’s FY26 full-year revenue growth rate to reach 14.3%, the fastest since 2021, but still far below the technology sector's overall expected growth rate of over 26%.

Meanwhile, Apple's approach to artificial intelligence differs significantly from its peers. Unlike tech giants such as Google, Amazon, Meta, and Microsoft, which have made multi-billion-dollar bets on AI infrastructure, Apple has yet to join this wave of investment, somewhat diminishing the correlation between its stock price and broader technology sector movements.

After-hours trading on Wednesday saw Google's stock surge due to strong cloud business growth, while Meta faced market backlash after raising its capital expenditure forecast. This divergence in performance once again underscores the uncertainty surrounding AI investment returns and provides a reference point for Apple’s differentiated strategy.

AI-powered earnings insights in three steps to establish an options strategy! Open Futubull > Stock Page > Click [Company] >Earnings Express

AI-powered earnings insights in three steps to establish an options strategy! Open Futubull > Stock Page > Click [Company] >Earnings Express

Editor/Lambor