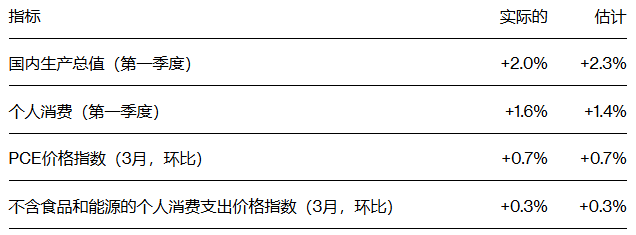

The U.S. GDP grew by 2% in the first quarter, indicating economic resilience; meanwhile, PCE inflation accelerated in March.

At the beginning of this year, driven by robust business and consumer demand, U.S. economic growth accelerated. According to preliminary estimates released by the U.S. Bureau of Economic Analysis on Thursday, inflation-adjusted Gross Domestic Product (GDP) grew at an annual rate of 2% in the first quarter, slightly below the expected 3%, but still significantly higher than the previous value of 0.5%. The longest federal government shutdown in U.S. history had constrained economic growth in the final months of 2024.

US economy shows resilience in Q1; inflation accelerates

Consumer spending, which accounts for about two-thirds of economic activity, grew faster than expected, reaching 1.6%, primarily driven by demand for services. Business investment in equipment and facilities surged by 10.4%, marking the fastest growth in nearly three years, supported by rapid investment in artificial intelligence.

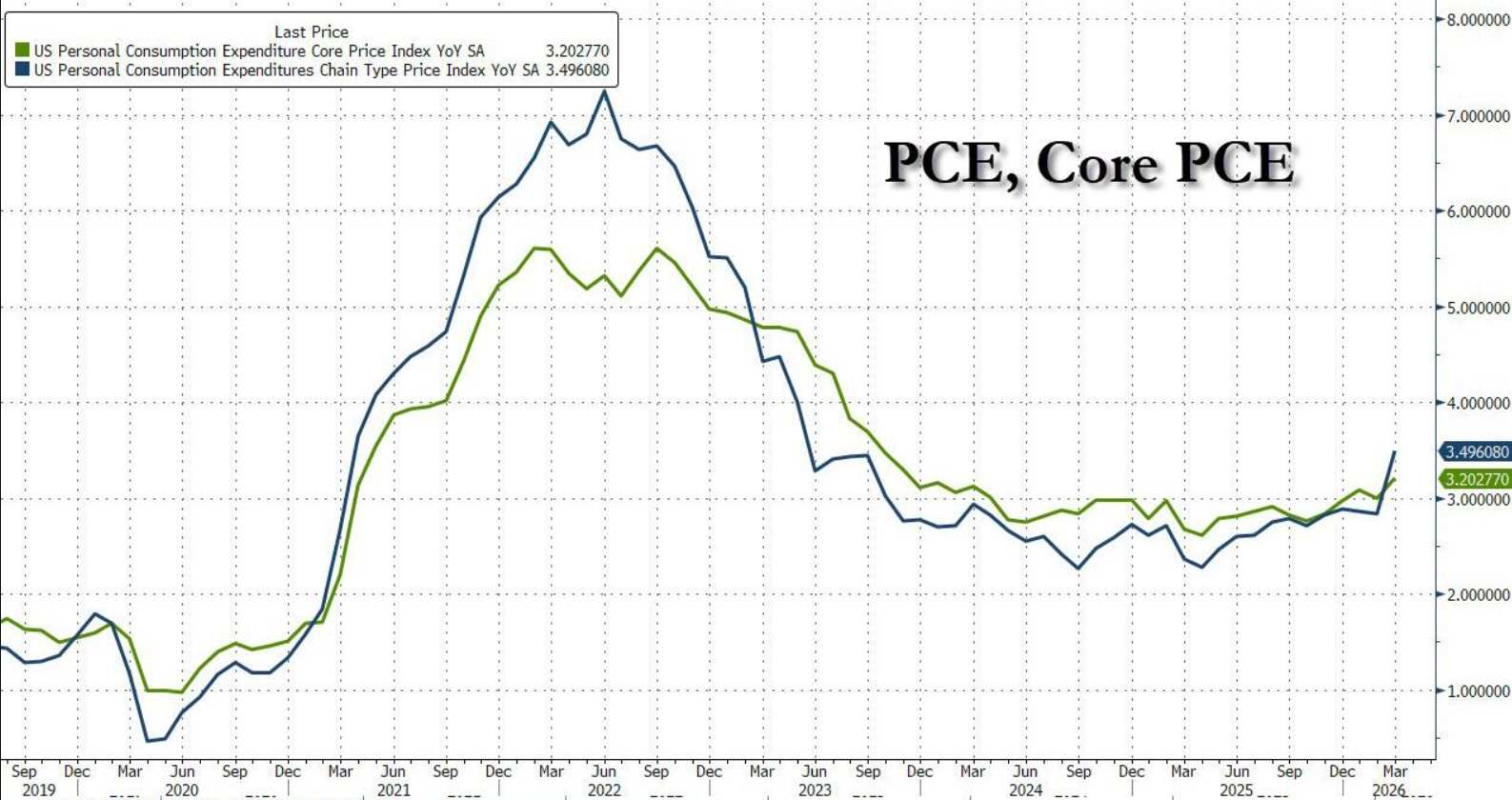

While higher tax refunds helped support household spending, the GDP report indicated that inflationary pressures surged sharply in March due to rising gasoline prices caused by the war. The Federal Reserve's preferred inflation gauge—the Personal Consumption Expenditures (PCE) price index—rose 0.7% in March, the largest increase since 2022. According to another data release from the BEA, the index increased by 3.5% compared to the same period last year. Since then, gasoline prices have continued to climb, reaching their highest level since 2022.

While higher tax refunds helped support household spending, the GDP report indicated that inflationary pressures surged sharply in March due to rising gasoline prices caused by the war. The Federal Reserve's preferred inflation gauge—the Personal Consumption Expenditures (PCE) price index—rose 0.7% in March, the largest increase since 2022. According to another data release from the BEA, the index increased by 3.5% compared to the same period last year. Since then, gasoline prices have continued to climb, reaching their highest level since 2022.

The core PCE price index, excluding food and energy prices and adjusted for seasonality, rose 0.3% in March, pushing the annualized inflation rate to 3.2%, both in line with widespread expectations. However, the core inflation rate hit its highest level since November 2023.

Meanwhile, the core PCE price index in the first quarter rose 4.3% year-over-year, surpassing expectations. The primary driver of accelerating inflation originated from the Middle East. According to data from the American Automobile Association (AAA), the national average gasoline price reached $4.18 per gallon on April 28, the highest level since the outbreak of the Iran conflict and the peak since April 2022. Since the outbreak of the conflict on February 28, nationwide gasoline prices have surged by approximately $1.20, representing a 40% increase.

On February 26, two days before the outbreak of the Middle East conflict, the national average gasoline price was only about $2.98 per gallon. Over the span of two months, additional spending by US consumers on gasoline has exceeded $150 per person, with economists predicting this figure will approach $800 by year-end.

More unsettling for markets, international oil prices briefly spiked above $126 per barrel on April 30, hitting a four-year high. On the same day, S&P revised its crude oil price assumptions for 2026 to $95 per barrel for WTI and $100 per barrel for Brent. The Strait of Hormuz continues to show no signs of resuming operations, with the geopolitical standoff between the US and Iran over control of the strait escalating.

Additionally, although household demand in the US cooled compared to the previous quarter, part of the reason may reflect the severe cold weather encountered across most of the country earlier this year. After adjusting for inflation, household spending grew 0.2% in March, primarily driven by increased consumer expenditure on goods such as automobiles and home furnishings, which fell short of expectations.

Meanwhile, the US Department of Labor reported that initial jobless claims for the week ending April 25, after seasonal adjustments, totaled 189,000, down by 26,000 from the previous week and significantly lower than the forecasted 212,000. This marked the lowest level since September 1969, while the US labor market has been characterized by low hiring and low layoffs over the past year.

Since trade and inventory fluctuations tend to distort GDP, economists closely monitor a narrower indicator of underlying demand—final sales (sales to domestic private purchasers). This indicator grew by 2.5% in the first quarter, rebounding from the previous quarter.

The report noted that despite the Middle East conflict causing a spike in oil prices and disrupting global supply chains, the U.S. economy has remained robust so far. However, if inflation-affected consumers become more cautious, geopolitical tensions could weaken the growth outlook.

In the first quarter of this year, employment growth averaged 68,000 jobs per month, compared to just 20,000 jobs per month in the same period last year. The labor market's growth has significantly slowed compared to 2023 and 2024. Some economists blame Trump’s trade and immigration policies, arguing that these measures reduced both labor demand and labor supply.

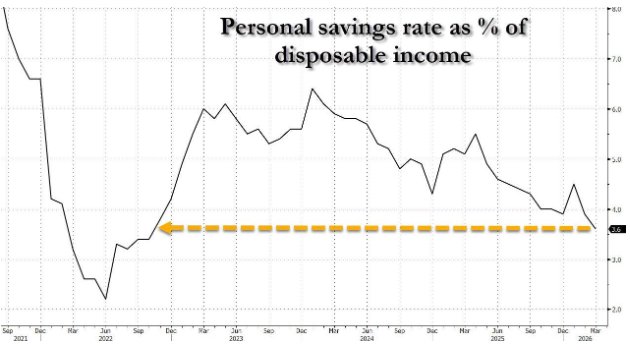

A weak labor market has curbed wage growth. Tariffs have driven up prices for some goods, though the impact on official inflation data has been relatively mild. Economists say that consumers are relying on savings or reducing savings to maintain spending, a situation they believe cannot last indefinitely. In March, U.S. household spending continued to grow faster than income growth (as wage growth lagged behind income growth), with the savings rate dropping slightly to a four-year low.

Economists warn that rising inflation could offset some of the anticipated stimulus effects of tax cuts. They expect the boost from larger tax refunds to fade quickly, leading to sluggish consumer spending this year. Economists predict that the Middle East war will begin pressuring economic growth starting in the second quarter.

AI Investment Drives Economic Growth

Amid macroeconomic turbulence, U.S. tech giants are unleashing an unprecedented surge in capital expenditures. Alphabet, Amazon, Meta, and Microsoft are projected to collectively spend $725 billion in 2026, primarily on building artificial intelligence and cloud data centers. This figure surpasses Switzerland’s GDP and represents an increase from the earlier estimate of approximately $650 billion.

Each company’s spending plan is staggering: Microsoft expects its capital expenditures to reach about $190 billion in 2026, surging over 60% year-on-year; Amazon maintains its forecast at $200 billion; Alphabet raised its guidance to between $180 billion and $190 billion; and Meta increased its full-year capital expenditure forecast to between $125 billion and $145 billion. Earnings reports also show that Amazon’s capital expenditures reached $44.2 billion in Q1, while Microsoft’s capital expenditures and financing lease payments hit $31.9 billion, marking a 49% year-on-year increase.

Fed Chair Powell, during his final press conference of his term on Wednesday, stated that the U.S. economy is “quite resilient,” partly due to what seems to be an insatiable demand for data centers across the country. However, this demand is facing significant headwinds: the Iran war caused oil prices to jump by about 50%, impacting every aspect of data center component manufacturing, starting from transportation. Whether AI investments can deliver commercial returns in a stagflationary environment has become the key question for capital markets in 2026.

Uncertainty Surrounding the Fed’s Rate-Cut Path

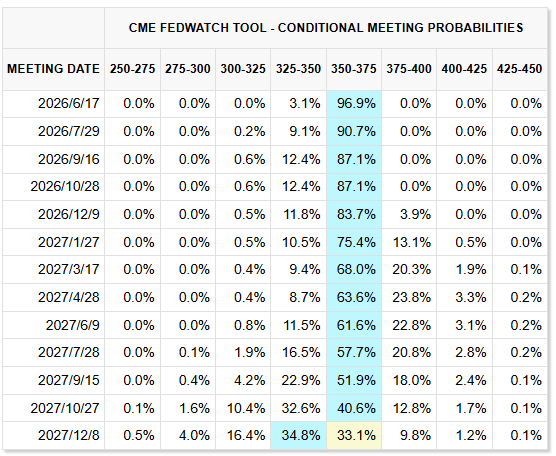

Federal Reserve officials kept interest rates unchanged this week, but growing uncertainty due to the war in Iran has deepened divisions among them regarding the policy outlook. What truly captured market attention, however, was the voting result: 8 in favor, 4 against, marking the highest number of dissenting votes since October 1992. The positions of the four dissenting members were not aligned: Federal Reserve Governor Stephen Milan advocated for a 25-basis-point rate cut, while Cleveland Fed President Hamak and two others supported keeping rates unchanged but opposed the inclusion of dovish language in the statement. This indicates that the divergence in views on the policy path between doves and hawks has become irreconcilable.

Regarding market expectations, Feroli, Chief U.S. Economist at JPMorgan, noted that although the energy shock poses downside risks to the economy, upward inflationary pressures are more pronounced. It is expected that the Federal Reserve will keep interest rates unchanged throughout 2026, with the next rate adjustment likely being a hike, anticipated to occur in the third quarter of 2027. Morgan Stanley, meanwhile, has abandoned its previous forecast of a Federal Reserve rate cut in 2026, now predicting that rate cuts will begin next year.

The pace of economic growth may support financial markets' expectations that the Federal Reserve will maintain unchanged interest rates as long as the labor market does not deteriorate. Interest rates might remain steady until 2027. In fact, data from U.S. interest rate futures shows that following the release of U.S. economic data, market expectations for a rate hike by the end of 2026 have slightly increased.