In the previous fiscal quarter ended March, Apple reported record-high revenue and EPS for the same period, with year-over-year growth of nearly 17% and 22%, respectively. iPhone revenue increased by 22%, slightly above the average analyst estimate. Service revenue grew by 16%, marking a new quarterly high for the third consecutive year. Revenue from Greater China surged by 28%, while performance in European and American markets was lackluster. Apple raised its dividend by 4% and authorized an additional $100 billion for share repurchases. The guidance for the current fiscal quarter indicates revenue growth of 14%-17%, surpassing analysts' expectations, with gross margin projected to reach as high as 48.5%. After-hours stock price initially fell by over 1%, but rebounded to rise more than 4% following the announcement of the guidance.

As CEO Cook, who has been at the helm for over a decade, is set to step down, $Apple (AAPL.US)$ the company delivered its best performance during the historical off-season for smartphones, though iPhone sales growth was not as impressive as Wall Street had hoped. However, the revenue guidance for this quarter was stronger than expected.

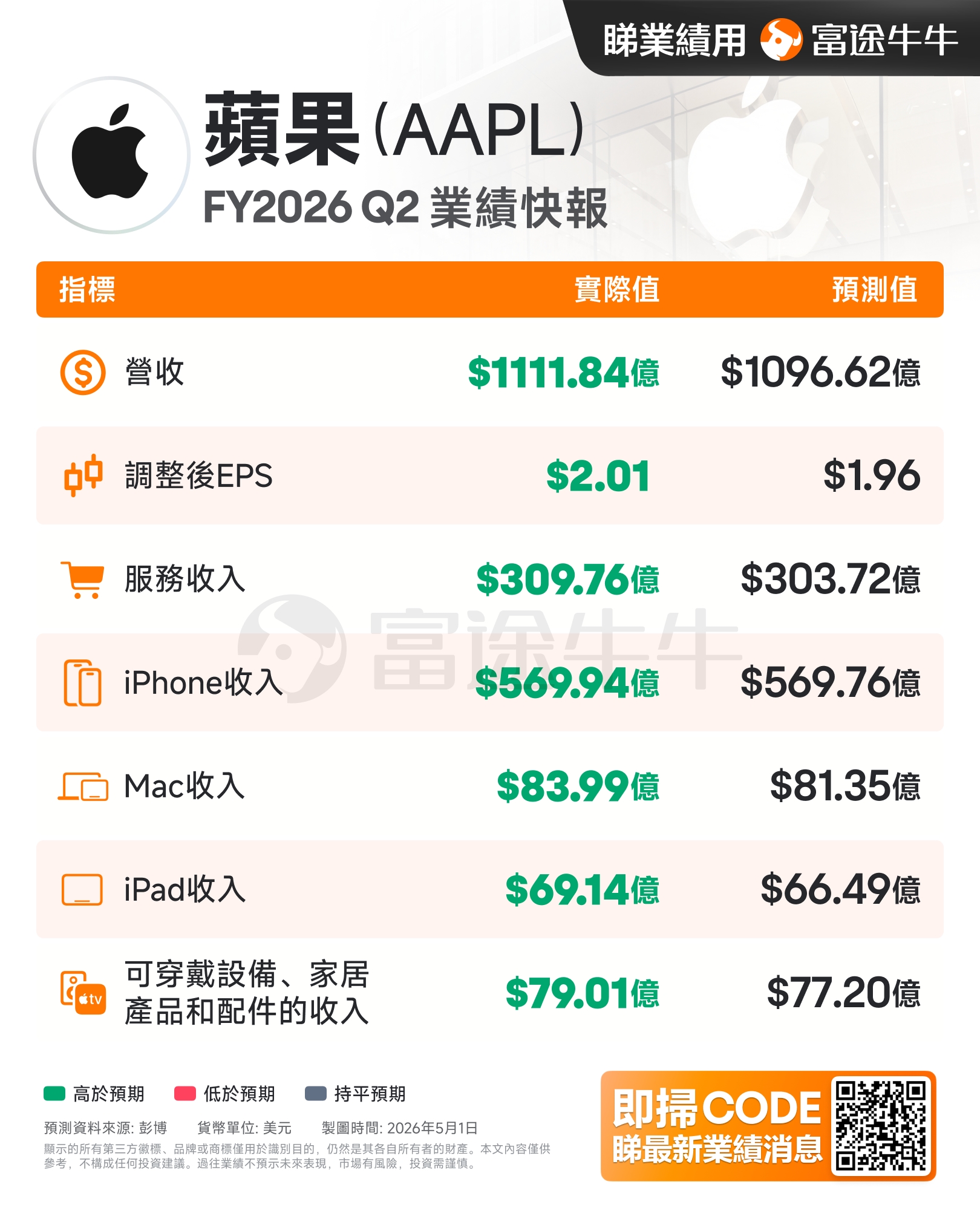

On Thursday, April 30, after the US stock market closed, Apple reported that for its fiscal second quarter ended March 28 (referred to as Q1), both revenue and earnings per share (EPS) maintained double-digit growth from the previous quarter, exceeding analyst expectations by approximately 1.4% and 2.6%, respectively. Net profit increased by nearly 20% year-over-year. Driven by revenue growth, improved gross margins, and reduced shares through buybacks, EPS growth outpaced net profit growth.

By business segment, the iPhone remains the largest revenue contributor. In Q1, iPhone revenue reached $56.99 billion, slightly above the analysts' consensus estimate of $56.98 billion, accounting for more than half of Apple’s total revenue and growing by over 20% year-over-year. Service revenue maintained a growth rate of over 10%, setting another quarterly record for the third consecutive year and continuing to serve as the 'stabilizer' for Apple’s profitability. This helped push the overall gross margin above 49%, surpassing expectations. Revenue from Mac, iPad, wearables, and home accessories also exceeded forecasts.

By business segment, the iPhone remains the largest revenue contributor. In Q1, iPhone revenue reached $56.99 billion, slightly above the analysts' consensus estimate of $56.98 billion, accounting for more than half of Apple’s total revenue and growing by over 20% year-over-year. Service revenue maintained a growth rate of over 10%, setting another quarterly record for the third consecutive year and continuing to serve as the 'stabilizer' for Apple’s profitability. This helped push the overall gross margin above 49%, surpassing expectations. Revenue from Mac, iPad, wearables, and home accessories also exceeded forecasts.

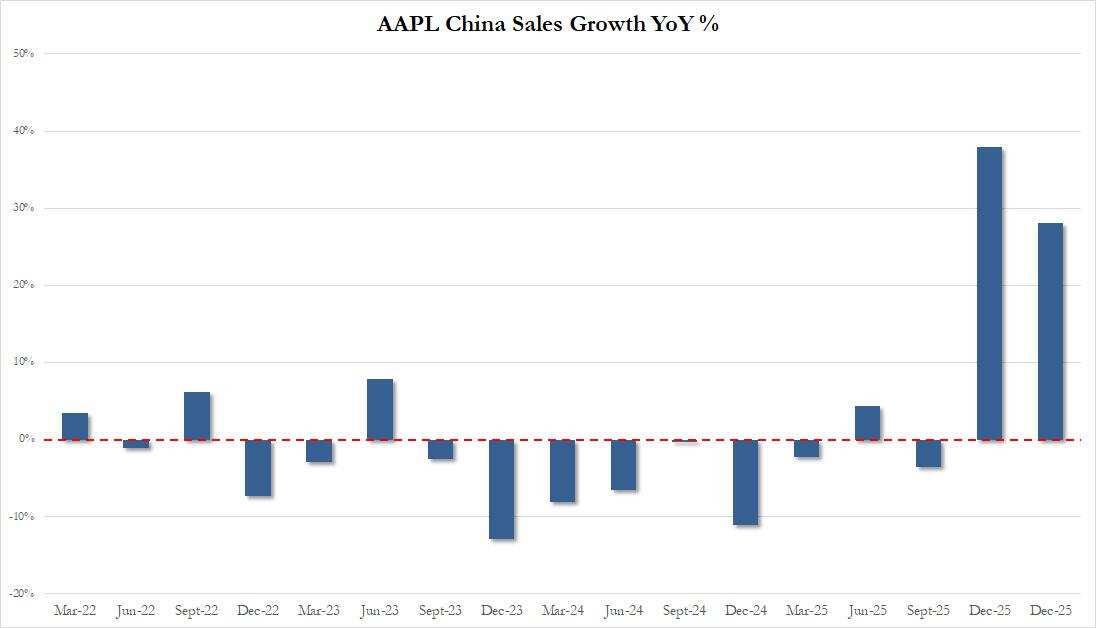

Regionally, following a significant rebound in sales last quarter, Apple sustained strong growth in China, the world’s largest smartphone market, during Q1. Revenue in Greater China grew by just over 28% year-over-year, surpassing analyst expectations by 8.4 percentage points and marking the fastest growth among major regional markets. However, revenue in Europe and the Americas fell short of market expectations.

In the earnings announcement, Tim Cook, Apple’s CEO who will step down in September, stated that the company delivered its best performance ever for a March-ending quarter, with all geographic regions achieving double-digit revenue growth. Apple’s Chief Financial Officer (CFO), Kevan Parekh, noted that robust business performance drove operating cash flow above $28 billion in Q1, while EPS both set new historical highs for a March quarter.

Parekh said, 'Continued strong demand for our products and services has once again helped us achieve record-high active installed devices—a key metric—across all major product categories and geographic regions.'

After the earnings release, Apple’s stock, which had gained over 0.4% during Thursday’s trading session, initially rose modestly in after-hours trading but then turned negative, dropping more than 1% at one point. During the earnings call, Apple executives revealed that revenue for the third fiscal quarter (the current quarter) would grow by 14%-17% year-over-year, significantly surpassing analysts’ expected growth of 9.1%. Following this, Apple’s stock reversed course, rising over 4% in after-hours trading.

The robust guidance became a key driver for the stock price reversal, while the less-than-stellar iPhone revenue growth last quarter weighed on the stock.

Commentary noted that Apple’s earnings guidance played a pivotal role in reversing the stock’s trajectory in after-hours trading. The revenue growth outlook, coupled with gross margin guidance of 47.5% to 48.5%, signaled that despite supply bottlenecks limiting near-term upside for the iPhone and Mac, underlying demand remained strong, and pricing strategies alongside product mix continued to perform well.

Meanwhile, rising memory chip costs posed an evident pressure point. However, during the earnings call, Cook did not elaborate further on specifics, suggesting that Apple still possesses various tools for adjustment—including pricing strategies, product mix optimization, and service business—to absorb these costs without significantly squeezing margins, at least in the short term.

The initial downturn in Apple's stock price was attributed to the fact that while the earnings report highlighted several bright spots, including revenue, profit, services, performance in the Chinese market, and share repurchases for the first quarter, the iPhone revenue, a key focus for the market, only narrowly exceeded expectations, disappointing some of the more optimistic investors. Additionally, revenue from the most mature markets, namely the U.S. and Europe, fell short of expectations, compounded by rapid growth in expenses, failing to meet the market’s anticipation of an 'explosive outperformance' by Apple.

Operating expenses grew rapidly in the first quarter, particularly with research and development costs surging approximately 34% year-over-year. While this is positive for long-term innovation, in the short term, it has led the market to pay closer attention to future profit margins and return on investment.

The post-market decline in Apple's stock price also reflects the high bar set for tech giants’ earnings reports: surpassing revenue and EPS expectations, reaching new highs in services, and announcing a $100 billion buyback were not enough to automatically drive share price gains; if the core iPhone business does not significantly exceed expectations, market sentiment can easily shift from initial optimism to caution.

Revenue and EPS both hit record highs for the same period, with gross margins continuing to rise.

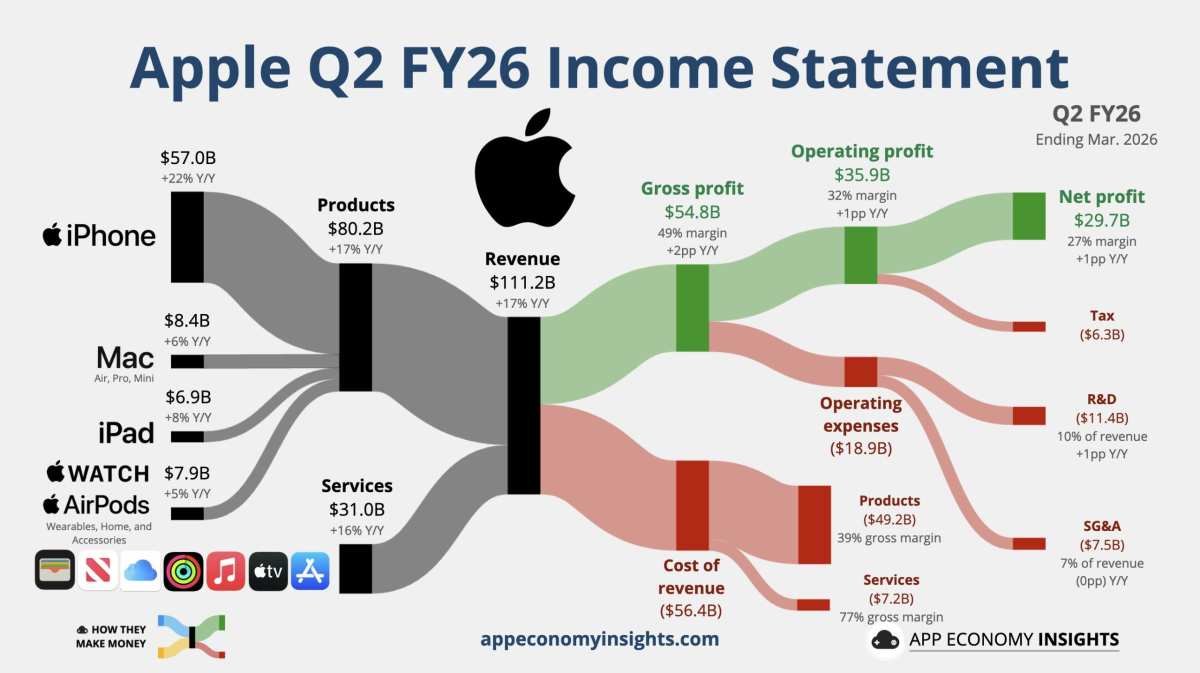

Apple reported total revenue of $111.184 billion for the second fiscal quarter, representing a 16.6% increase from $95.359 billion in the same period last year and surpassing market expectations of $109.66 billion. Specifically:

Product revenue reached $80.208 billion, growing by approximately 17% year-over-year and exceeding expectations of $79.26 billion;

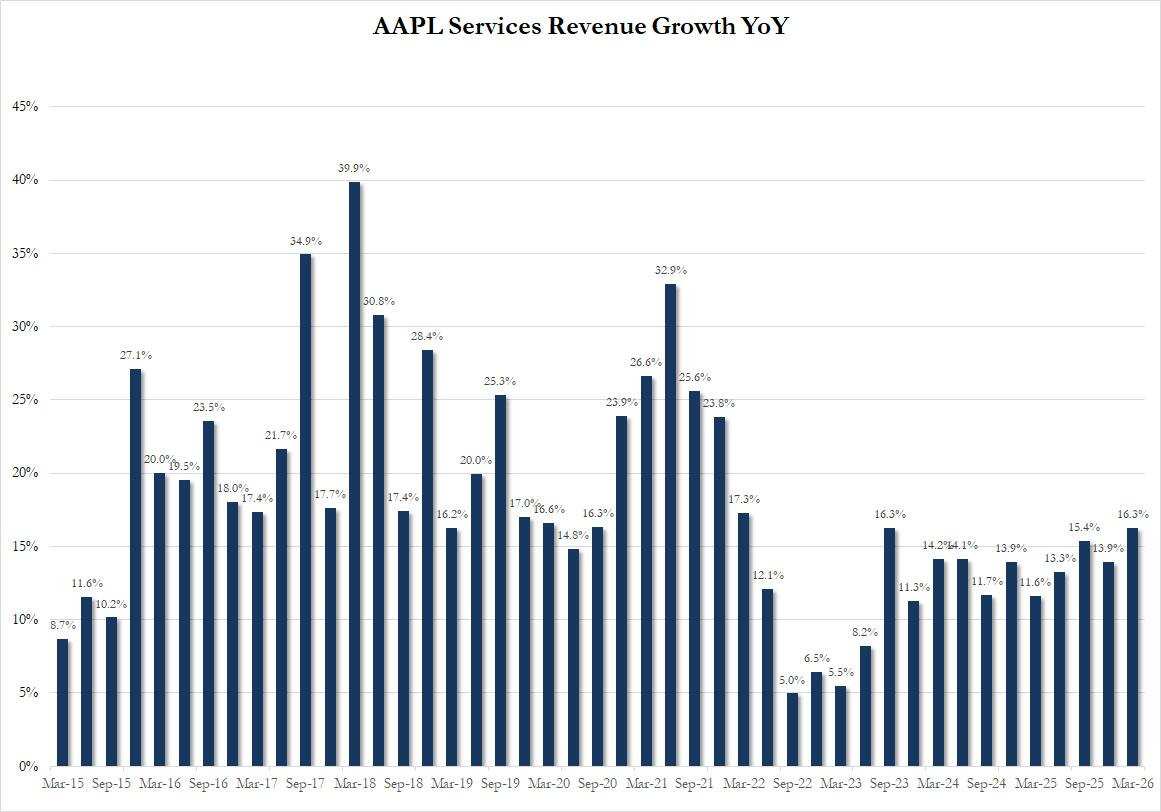

Service revenue amounted to $30.976 billion, increasing by about 16% year-over-year and surpassing forecasts of $30.37 billion.

Profitability remained robust as well. Apple’s net profit for the quarter was $29.578 billion, up approximately 19% from $24.780 billion in the same period last year; diluted EPS grew by 21.8% year-over-year to $2.01, higher than $1.65 in the prior year and surpassing market expectations of $1.96.

Gross margin was a key pillar of support in the first-quarter earnings report. Apple’s gross profit for the quarter reached $54.781 billion, corresponding to an overall gross margin of approximately 49.3%, up from around 47.0% in the same period last year and higher than 48.5% in the previous quarter. The product segment’s gross margin was approximately 38.7%, while the services segment’s gross margin was about 76.7%, with the high-margin nature of services continuing to bolster overall profitability.

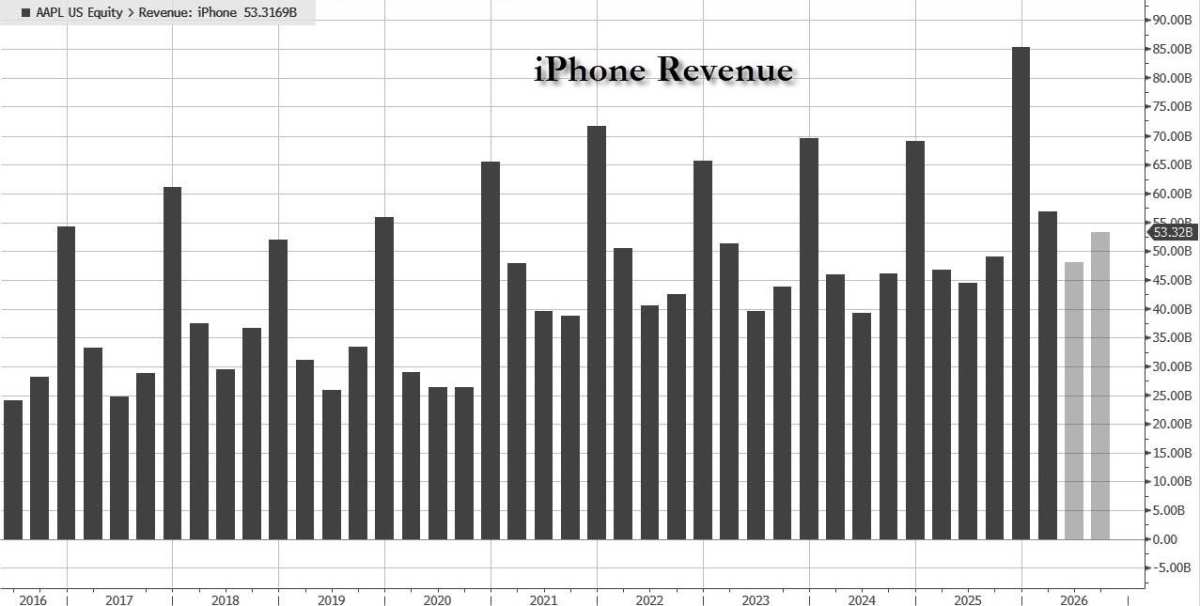

iPhone sales increased by 22% year-over-year, slightly above the average expectation, limiting market excitement.

iPhone revenue reached 56.994 billion US dollars, increasing by approximately 22% year-over-year, almost contributing the core part of Apple's quarterly revenue growth. Apple CEO Tim Cook stated that the iPhone set an income record in the March quarter, primarily driven by demand for the iPhone 17 series.

However, this is also one of the key reasons for the cautious market reaction after hours: although iPhone revenue showed strong year-over-year growth, it exceeded market expectations by only about 10 million US dollars, barely meeting the forecast line. For a highly valued giant like Apple, investors typically expect the iPhone to significantly surpass expectations to validate the strength of a new replacement cycle.

Other hardware categories performed relatively steadily:

Mac revenue was 8.399 billion US dollars, growing by approximately 6% year-over-year, surpassing the expected 8.13 billion US dollars;

iPad revenue was 6.914 billion US dollars, increasing by approximately 8% year-over-year, exceeding the expected 6.65 billion US dollars;

Wearables, Home, and Accessories revenue was 7.901 billion US dollars, rising by approximately 5% year-over-year, higher than the expected 7.72 billion US dollars.

Apple launched the iPhone 17e, the iPad Air equipped with the M4 chip, and the MacBook Neo among other new products in the first quarter. Although hardware maintained overall growth, market reactions indicate that investor expectations for Apple’s core business, the iPhone, are evidently higher.

The services business reached new highs and remains the 'stabilizing factor' for Apple's profit quality.

First-quarter services revenue was 30.976 billion US dollars, growing by 16.3% year-over-year, not only surpassing analysts’ expectations of 30.37 billion US dollars but also continuing its streak of setting new quarterly revenue records for over three years, accelerating from the previous quarter’s growth rate of 14%.

Apple CFO Kevan Parekh stated that the company’s active installed base of devices reached record highs across all major product categories and regions, providing a foundation for the sustained growth of the services business.

Compared to hardware, the revenue growth of the services business is more stable and its gross margin is higher. This quarter, the cost of services was $7.224 billion, corresponding to a gross profit of approximately $23.752 billion, with a gross margin close to 77%. This indicates that although the revenue share of the services business is less than 30%, its contribution to profits far exceeds its revenue share.

This is also the part of Apple's financial report that is harder to interpret negatively: the high-quality growth of the services business continues, demonstrating strong ecosystem stickiness, and the expansion of the installed base is still being continuously converted into revenues from subscriptions, the App Store, cloud services, payments, and more. The chart below shows Apple’s hardware and services business costs and gross margins for the first half of fiscal year 2026 as of the end of March.

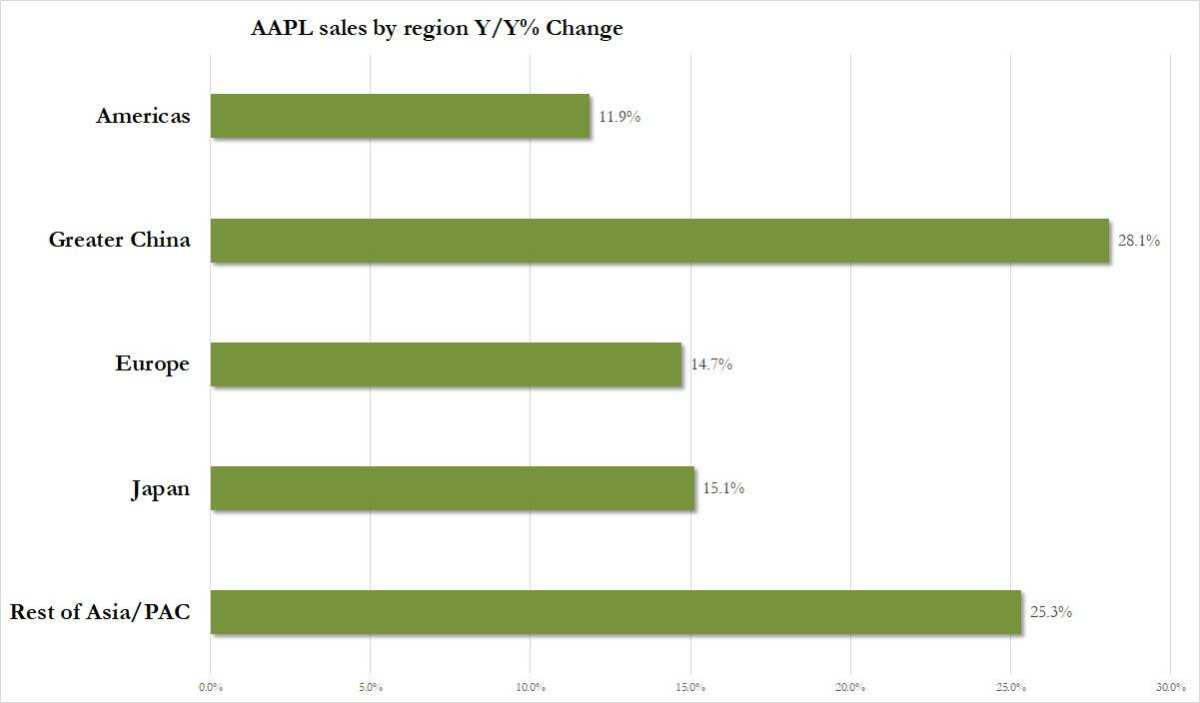

Revenue in Greater China surged 28% year-over-year, significantly surpassing expectations, while performance in Europe and the Americas lagged behind.

In terms of regional performance, Greater China stood out the most. In the first quarter, revenue in Greater China reached $20.497 billion, representing a year-over-year increase of approximately 28%. Although this growth rate slowed compared to nearly 38% in the previous quarter, it was significantly higher than market expectations of $18.91 billion.

This performance holds considerable significance for Apple. Over the past few quarters, the market has been closely watching how Apple navigates pressures such as competition from local brands and fluctuations in consumer electronics demand in the Chinese market. The better-than-expected revenue growth in Greater China during the first quarter indicates that demand for Apple’s premium smartphones in China remains resilient, alleviating concerns about weakening market share and demand in China.

Performance in other regions showed mixed results:

Revenue in the Americas amounted to $45.093 billion, growing by approximately 12% year-over-year but falling short of analysts’ expectations of $45.82 billion, marking the second consecutive quarter of underperformance.

Revenue in Europe reached $28.055 billion, increasing by approximately 15% year-over-year but below expectations of $29.08 billion.

Revenue in Japan totaled $8.401 billion, growing by approximately 15% year-over-year and surpassing expectations of $7.38 billion.

Revenue in other Asia-Pacific regions reached $9.138 billion, reflecting an annual growth of approximately 25% and exceeding expectations of $8.76 billion.

Thus, the regional performance was not uniformly 'off the charts': China, Japan, and other Asia-Pacific regions performed strongly, while the Americas and Europe fell short of expectations, partially offsetting the overall above-expectation results.

Rapid growth in expenses, with R&D investment increasing significantly year-over-year.

Apple's total operating expenses for the quarter were $18.896 billion, an increase of approximately 24% year-over-year, surpassing market expectations of $18.47 billion. Specifically:

R&D expenses amounted to $11.419 billion, up approximately 34% year-over-year;

Sales, general, and administrative expenses were $7.477 billion, increasing by about 11% year-over-year.

The growth rate of R&D expenses significantly outpaced revenue growth, potentially driven by investments in chips, AI, hardware platforms, and new product cycles. Such investments are necessary for long-term competitiveness; however, from a short-term profit perspective, the rapid rise in expenses has drawn investor attention to whether profit margins can continue to expand in the future.

Despite rising costs, Apple's operating profit in Q1 reached $35.885 billion, growing approximately 21% year-over-year, with an operating margin of about 32.3%, higher than last year’s 31.0%. This indicates that Apple still possesses strong cost absorption capabilities. The chart below shows Apple’s H1 2026 financial data.

Strong cash flow, with an additional $100 billion authorized for share repurchases.

Apple's operating cash flow in Q1 exceeded $28 billion, setting a record high for the March-ending quarter. In the first six months, Apple generated cumulative operating cash flow of $82.627 billion, significantly higher than $53.887 billion in the same period last year.

In terms of capital returns, Apple’s board announced:

Increase the quarterly dividend by 4% to USD 0.27 per share;

Authorize a new stock repurchase program of up to USD 100 billion.

As of March 28, Apple’s cash and cash equivalents amounted to USD 45.572 billion, higher than USD 35.934 billion at the end of the previous fiscal year; including marketable securities, the total cash and securities reached approximately USD 146.6 billion. During the same period, interest-bearing debt was about USD 84.7 billion, allowing Apple to maintain substantial net cash and capital return capacity.

However, for Apple investors, large-scale share repurchases have long been part of expectations. While the USD 100 billion repurchase authorization is positive news, it is insufficient to fully offset concerns over the iPhone’s “modestly above expectations” performance and regional disparities.

Editor/Rocky