Goldman Sachs analysts pointed out that semiconductor valuations are relatively high, while hyperscale cloud service providers' valuations remain below historical averages, indicating room for recovery. Regardless of whether cloud giants improve their return on investment or cut capital expenditures, the cloud computing sector is expected to benefit, whereas chip stocks face downside risks.

Goldman Sachs believes that in the wave of AI infrastructure construction, investors should shift their positions from chip stocks to cloud computing giants.

On Thursday, Alphabet's share price surged 10% in a single day, adding $421 billion to its market value. This marked the largest single-day market capitalization increase in the company’s history and ranked as the second-largest single-day market value gain in U.S. corporate history.

At the same time, NVIDIA's share price fell more than 4%, breaking below the $200 mark, with a near $10 decline in value over the day.

At the same time, NVIDIA's share price fell more than 4%, breaking below the $200 mark, with a near $10 decline in value over the day.

In a client note, Goldman Sachs' senior semiconductor analyst Jim Covello recommended "going long on hyperscale cloud service providers while underweighting semiconductors."

Covello pointed out in the report that the current market's pricing for return on investment in hyperscale cloud providers already reflects "a significant degree of pessimism," leading to a substantial compression in valuation multiples. By contrast, semiconductor stocks are now evidently overvalued.

Strong growth in Google Cloud ignites market enthusiasm.

The trigger for this surge in Alphabet was an impressive quarterly earnings report.

Google Cloud's quarterly revenue growth reached 63%, impressing investors. The operating profit margin for the cloud business expanded significantly from 17.8% a year ago to 32.9%. Management attributed this to more efficient technological infrastructure and process innovation.

JPMorgan analyst Doug Anmuth wrote in a research report on Thursday:

We believe Google is generating clear, quantifiable returns on its AI investments.

He pointed out that Google Cloud's contract backlog nearly doubled quarter-over-quarter in the first quarter, reaching $462 billion. Anmuth also emphasized:

The virtuous cycle between underlying chips, model improvements, user engagement, and commercial monetization continues to compound.

Alphabet stated during the earnings call that AI solutions have become the primary growth driver for Google Cloud, with strong demand for Gemini-based AI agent products.

The company disclosed that Gemini processes over 16 billion tokens per minute, marking a 60% increase quarter-over-quarter.

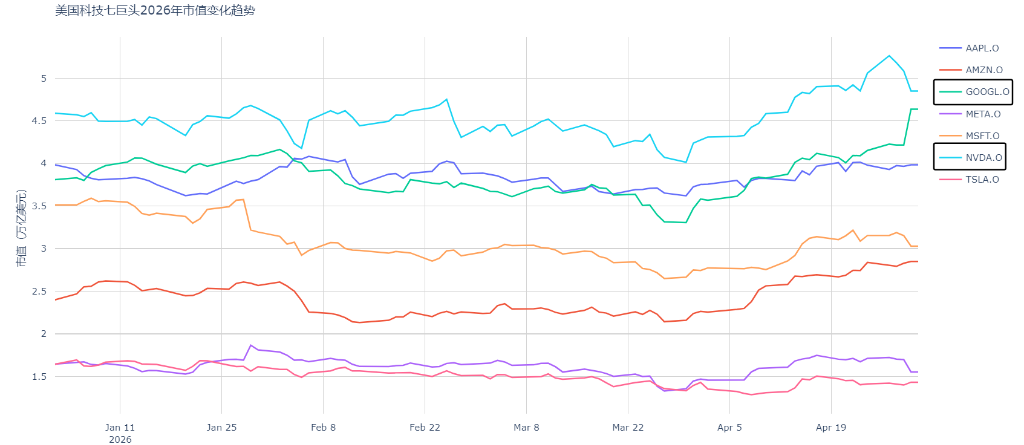

Alphabet’s market capitalization is approaching NVIDIA’s, with the gap narrowing to approximately $203 billion.

Strong performance has driven Alphabet's stock price to an all-time high. According to Dow Jones Market Data, the company’s cumulative gain this month has reached 33.8%, marking its best single-month performance since October 2004.

In terms of market capitalization rankings, the gap between Alphabet and NVIDIA has narrowed to approximately $202.9 billion, the smallest gap since February 5 of this year.

In January this year, Alphabet surpassed Apple to become the world’s second-largest company by market capitalization.

Over the past year, Alphabet’s stock price has cumulatively risen by 138.5%. The company has gradually dismantled the narrative that AI poses an existential threat to its business. Google Search revenue grew by 19% in the first quarter, with query volumes hitting record highs, underscoring the logic that AI expands rather than erodes search business.

According to Sensor Tower data, Gemini has become the world's second most downloaded AI application, trailing only ChatGPT under OpenAI.

Goldman Sachs: Chip valuations are high, while cloud giants are undervalued by the market.

Covello noted in the report that semiconductor stock valuations have clearly become overstretched, whereas hyperscale cloud service providers are trading below their historical averages.

The 12-month forward price-to-earnings (P/E) ratio of the Philadelphia Semiconductor Index has risen to approximately 24 times, higher than its 10-year average of 19 times. The forward P/E ratio for hyperscale cloud service providers is also around 24 times, but given their consistent cash flow and growth prospects, this sector typically commands a higher premium historically.

Over the past few months, semiconductors have been investors' favorite AI-themed investment target, with the Philadelphia Semiconductor Index gaining nearly 150% over the past year.

Meanwhile, hyperscale cloud service providers such as Amazon, Oracle, Microsoft, Alphabet, and Meta have underperformed due to investor concerns about massive capital expenditures on data centers.

Covello outlined two scenarios favorable to cloud service providers in the report:

First scenario: Cloud giants begin to demonstrate positive returns on investment, alleviating market concerns about their capital expenditures and driving valuation recovery, while upside potential in chip stocks is constrained as they are already fully priced in.

The second scenario, viewed by Covello as the "best-case scenario": If hyperscale cloud service providers continue to face pressure on return on investment and are forced to cut capital expenditures, "we believe cloud giants will experience a significant rebound due to improved cash flow prospects, while semiconductor stocks will sharply decline as reduced capital spending impacts revenues."

The only negative scenario is "maintaining the status quo": cloud giants continue to make significant expenditures amid questionable return on investment, further straining their cash flow dynamics while continuing to support chip stock valuations. Covello pointed out that this scenario would be the most detrimental to the aforementioned relative value trades.

Editor/Lambor