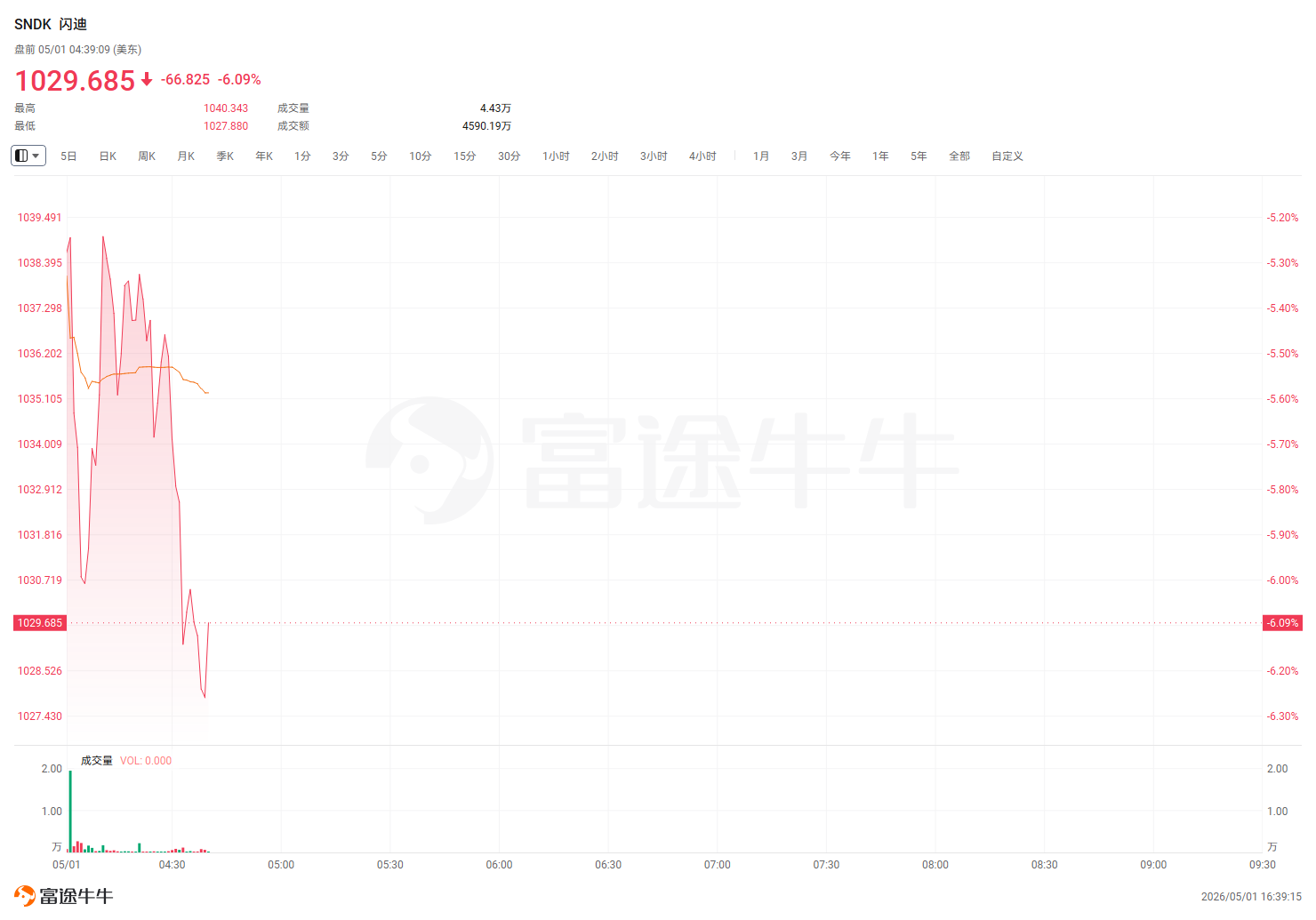

Despite Sandisk's stock price falling more than 6% in pre-market trading, analysts attribute this to excessively high prior expectations and have significantly raised the 12-month target price from $700 to $1200, with an average increase of about 55% in EPS forecasts. The short-term decline is more a release of sentiment and positions rather than an issue with fundamentals. "We expect the stock price will eventually rise."

Both the earnings report and guidance exceeded expectations, yet the stock price initially dropped—a phenomenon that reveals a market logic about 'expectations already being too high.'

On April 30, $SanDisk (SNDK.US)$ The company released its first-quarter earnings report for fiscal year 2026. On the same evening, a research report from Wall Street was promptly issued, providing a detailed analysis of the earnings report and the company’s prospects.

Goldman Sachs believes the short-term decline is more about the release of sentiment and positioning rather than fundamental issues. The bank stated, 'We expect the stock price to eventually rise,' and significantly raised its 12-month target price from $700 to $1,200, with an average increase of approximately 55% in EPS forecasts.

Goldman Sachs believes the short-term decline is more about the release of sentiment and positioning rather than fundamental issues. The bank stated, 'We expect the stock price to eventually rise,' and significantly raised its 12-month target price from $700 to $1,200, with an average increase of approximately 55% in EPS forecasts.

Why did an 'explosive earnings report' lead to a decline?

The earnings data itself was without any suspense—comprehensively surpassing expectations, and by a remarkably wide margin.

Sandisk’s Q1 revenue reached $5.95 billion, exceeding analyst expectations of $5.101 billion by 16.6% and the broader market expectation of $4.781 billion by 24.5%. The gross margin hit 78.4%, nearly 9 percentage points higher than the expected 69.8%. Non-GAAP earnings per share were $23.41, surpassing analyst expectations of $17.00 by 37.7% and the broader market expectation of $15.11 by nearly 55%.

However, the stock price fell as much as 6% in after-hours trading, and Sandisk remains at a 6% loss in pre-market trading today on the U.S. stock market.

Before the earnings report was released, Sandisk’s stock price had already experienced a significant surge—tight supply and demand for NAND storage, explosive demand for data center SSDs, and strengthening industry pricing expectations had all been priced in by the market in advance. Investor expectations had already been pushed to a very high level before the release of the earnings report.

In the words of the report: 'We believe that due to the substantial rise in stock price prior to the earnings report, investor expectations have significantly increased.'

In other words, no matter how good the earnings report is, it needs to exceed 'already high expectations' to drive further stock price increases. The short-term decline reflects more the release of sentiment and positions rather than fundamental issues.

The report clearly stated: "Despite an initial 6% drop in stock prices, we expect the stock price to eventually rise."

Q2 Guidance: Another Significant Beat

If the Q1 earnings report was described as 'better than expected,' then the Q2 guidance can be characterized as 'another significant beat.'

The midpoint of Sandisk's Q2 revenue guidance is $8 billion (ranging from $7.75 billion to $8.25 billion), which is 20.3% higher than the analysts' forecast of $6.649 billion and 14.8% higher than the market consensus expectation of $6.968 billion.

The gross margin guidance is 80%, approximately 5.5 percentage points higher than the analysts' forecast of 74.5%.

The non-GAAP earnings per share guidance range is $30 to $33, with a midpoint of $31.50, which is 30.1% higher than the analysts' forecast of $24.21 and 21.3% higher than the market consensus expectation of $25.96.

On a quarter-over-quarter basis, the midpoint of the revenue guidance represents an increase of approximately 34.5% compared to the actual Q1 revenue, with a year-over-year growth rate as high as 372%.

This set of figures leaves almost no room for potential 'disappointment.'

$42 Billion Supply Agreement: Securing the Future, but Further Observation Needed

Another noteworthy piece of information in the earnings report is Sandisk's disclosure of the progress on its 'New Business Models' (NBMs).

In simple terms, Sandisk is signing long-term supply agreements with customers—customers secure supply in advance, and Sandisk gains stable and predictable revenue. This model is akin to a 'pre-sale plus long-term contract' arrangement, benefiting both parties: customers avoid supply shortages, while Sandisk can lock in revenue and profits ahead of time.

Currently, Sandisk has signed five such agreements and is actively negotiating with other customers. The total contract value of three of these agreements amounts to $42 billion, including $11 billion in guaranteed revenue and $400 million in upfront payments. These three contracts cover approximately 35% of Sandisk's planned production capacity for FY27, and management indicated that this proportion could potentially increase further in the future.

The report commented: 'We view these agreements as a positive first step; however, it is premature to declare a structural shift in the industry until more details about the agreements and the customer base are disclosed.'

NAND Supply and Demand: Continued Tightness, Gross Margin with Further Upside Potential

Sandisk's management clearly stated during the earnings call that the NAND industry will remain in a state of constrained supply throughout 2026 and beyond. The company currently has no plans to alter its annual bit supply growth rate of approximately 20%.

Meanwhile, enterprise market demand is accelerating—with enterprise bit demand growth projected to reach over 60% in 2026.

The report believes that, driven by both constrained supply and accelerating demand, Sandisk's gross margin still has room for further improvement. However, given that the company has already provided guidance of approximately 80% gross margin, the scope for further upward revisions may narrow.

Enterprise SSD: Starting from a Small Base, Significant Room for Market Share Growth

Sandisk's enterprise SSD (eSSD) business is growing rapidly. Currently, data center products account for 25% of the company’s total revenue.

At the product level, Sandisk has completed certification of its TLC enterprise solid-state drives for multiple hyperscale cloud computing customers and plans to begin shipments of QLC enterprise solid-state drives in the June quarter of this year.

The report concluded: "We believe that SanDisk will achieve a significant market share increase in the coming quarters, starting from a relatively low base."

Target price significantly raised, with EPS forecasts comprehensively revised upwards.

Based on this assessment, the report raised SanDisk's 12-month target price from $700 to $1,200, representing a 71% increase.

The target price is based on a price-to-earnings (P/E) ratio of 22 times (unchanged multiple), with the normalized EPS estimate revised upward from $32 to $55.

At the stock price of $1,096.51 at the time of the report’s release, the target price implies a potential upside of approximately 9.4% to 9.8%.

Regarding EPS forecasts, the report increased projections by an average of 55% across all years:

CY2026 EPS forecast was raised from $101.90 to $155.00, an increase of 52.1%.

CY2027 EPS forecast was raised from $127.50 to $207.00, an increase of 62.3%.

CY2028 EPS forecast was raised from $120.00 to $177.00, an increase of 47.5%.

The report also noted that Micron is expected to have a positive reaction, as Micron has similar exposure to the NAND end-market.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/Lambor