Google Cloud's backlog surged by $219 billion in a single quarter, nearly doubling, with the launch of TPU-based chips for external sales marking a new battleground; AWS's backlog exceeded expectations by $120 billion, with growth continuing to accelerate; the combined backlog of the three cloud vendors surpassed $1.5 trillion at the end of the quarter. Morgan Stanley believes that the acceleration of hyperscale cloud vendors' revenue is becoming the most critical validation signal this year for return on invested capital (ROIC) in generative AI investments.

Three tech giants released their earnings reports on the same night, with the explosive growth of cloud businesses prompting Wall Street to reevaluate the commercial returns of AI.

According to ZF Trading Desk, on April 30, a research report issued by Brian Nowak’s team at Morgan Stanley analyzed the latest financial results of Alphabet, Amazon, and Meta. They concluded that the revenue acceleration of hyperscale cloud providers is becoming the most significant validation signal for generative AI return on invested capital (ROIC) this year.

Google Cloud: Backlog Doubles, TPU Chip Sales Become a New Narrative

Google Cloud was the biggest surprise of this earnings season.

Google Cloud was the biggest surprise of this earnings season.

Quarterly revenue increased by 63% year-over-year, surpassing buy-side expectations of 60%. Growth stemmed from two key drivers: first, a substantial month-over-month increase in paying monthly active users for Gemini Enterprise Edition, with over 16 billion tokens processed per minute through direct API; second, sustained robust demand for AI infrastructure, as Google continued selling TPUs and GPUs to external customers.

Even more striking was the backlog figure. Google Cloud’s end-of-quarter backlog surged from $243 billion to $462 billion, adding $219 billion in a single quarter, nearly doubling. Morgan Stanley noted that this was driven by large private lab contracts and contributions from Google’s sales of TPU chips to third parties.

The sale of TPUs to external customers represents a new variable. Morgan Stanley estimates that, depending on chip sales volume and unit price, TPUs may have contributed between $20 billion and $100 billion to this quarter’s backlog (with a baseline assumption of approximately $55 billion). This indicates that Google is not just a cloud service provider but is also selling computing hardware externally—a scenario previously considered a 'bull case' assumption, which is now the base case.

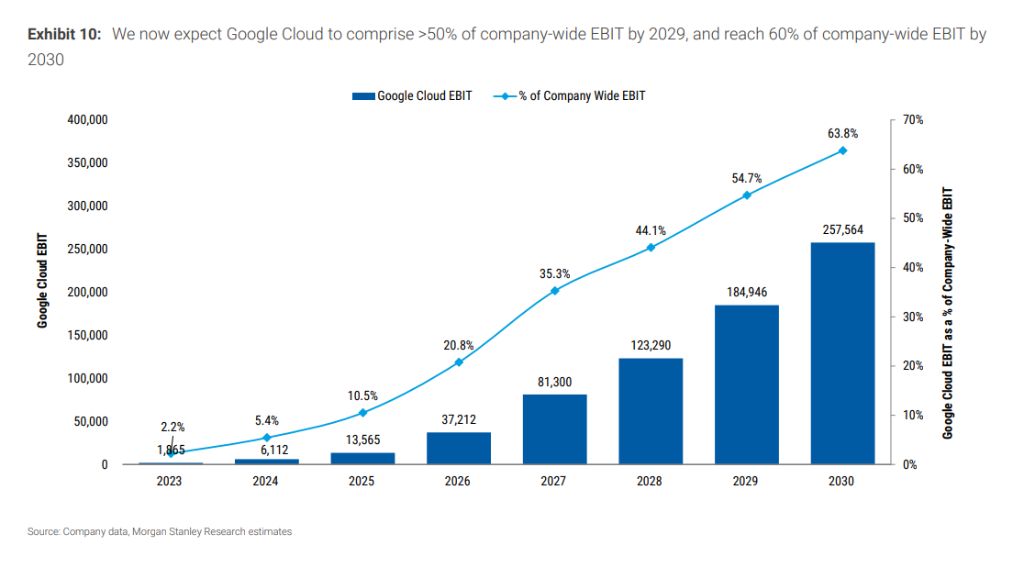

The financial impact is directly reflected in forecasts: Morgan Stanley raised its revenue projections for Google Cloud in 2026/2027 by approximately 11%/40%, expecting growth rates of 78%/86%. Looking further ahead, under the current model, Google Cloud’s EBIT contribution is projected to exceed 50% of the company’s total EBIT by 2029 and reach 64% by 2030.

Based on this, Morgan Stanley increased its target price for Alphabet from $330 to $375, corresponding to a 24x price-to-earnings ratio based on expected earnings per share of approximately $15.74 in 2027, maintaining an 'Overweight' rating. The 2027 EPS forecast was also raised by 14% to approximately $16.

AWS: Growth Below Expectations, but Backlog Indicates Stronger Future

AWS grew by 28% year-over-year this quarter, falling short of the buyers' expectation of approximately 30%, making it a relatively lackluster point in this earnings report.

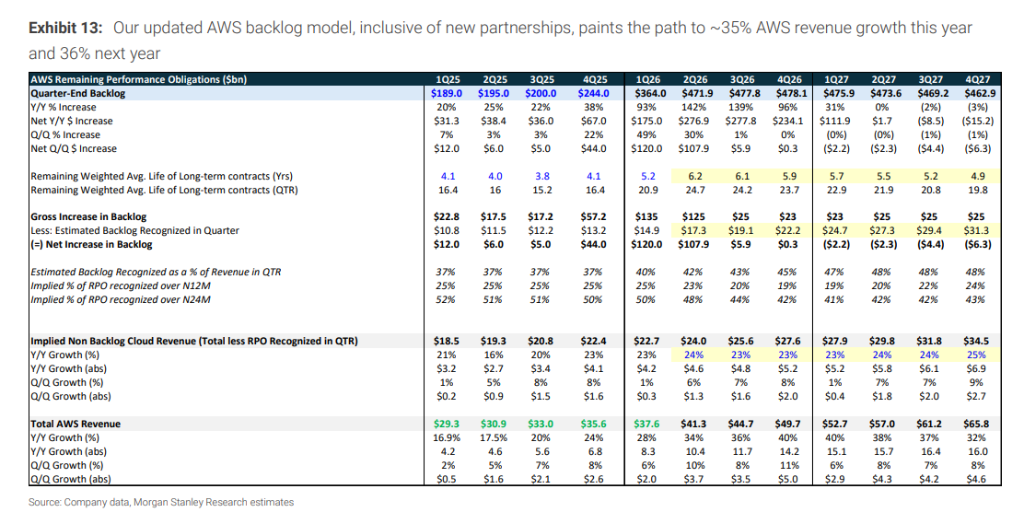

However, Morgan Stanley reminded investors not to focus solely on the quarterly figures. AWS accelerated by approximately 480 basis points compared to the previous quarter, and changes in backlog orders are more telling: the end-of-quarter backlog increased from $244 billion to $364 billion, with a net increase of $120 billion in a single quarter, surpassing Morgan Stanley's previous forecast of around $350 billion, primarily driven by large private lab contracts and new business.

Morgan Stanley forecasts that as capacity continues to be released, AWS's growth rate will further increase, reaching 35% and 36% in 2026 and 2027 respectively.

Amazon's retail business also exceeded expectations: EBIT in North America for the first quarter was about $1 billion higher than expected, with unit growth at approximately 15% year-over-year, surpassing expectations by about 400 basis points, while fulfillment and delivery costs were 2% lower than anticipated.

Taking into account both cloud services and retail, Morgan Stanley raised its EPS forecast for Amazon in 2027 by approximately 9% to around $11.3, and increased the target price from $300 to $330, corresponding to a price-to-earnings ratio of about 29x, maintaining an 'Overweight' rating.

Capital Expenditure: To exceed $1 trillion by 2027

Behind the rapid growth of the cloud business is a continuous increase in capital expenditure.

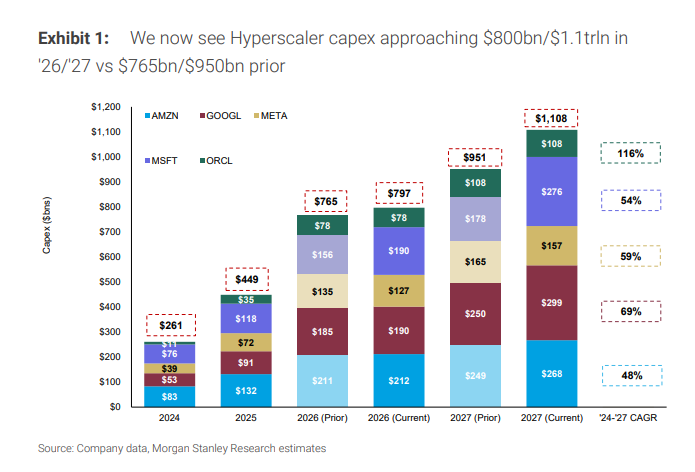

Morgan Stanley’s latest forecast indicates that the combined capital expenditure of the five hyperscale cloud vendors (Amazon, Google, Meta, Microsoft, Oracle) will reach approximately $800 billion in 2026 and exceed $1.1 trillion in 2027, revised upwards from the previous estimate of $950 billion.

Specifically, for individual companies: Google has raised its 2026 capital expenditure cap by $5 billion; Morgan Stanley predicts that Google and Amazon will reach $300 billion and $225 billion in data center capital expenditures respectively in 2027.

The logic behind this investment is: heavy upfront investment to build capacity, followed by revenue scaling and ROIC recovery. The surge in backlog orders is the most direct evidence that this strategy is viable.

META: Advertising remains strong, but lacks a cloud business card

META's situation is different from that of Google and Amazon.

First-quarter revenue was $5.631 billion, slightly below the expected $5.676 billion, but core advertising metrics continued to improve: Facebook video viewing time grew by more than 8% quarter-over-quarter, the largest increase in four years; Instagram Reels time increased by 10%; global average ad prices rose 12% year-over-year; and ad impressions grew 19% year-over-year.

Adjusted EBITDA profit margin reached 62%, far exceeding expectations of 56.3%.

However, Morgan Stanley pointed out that META does not have a high-growth business like Google Cloud or AWS that can directly demonstrate the return on AI investments, and also lacks forward-looking revenue visibility. Therefore, whether META's stock price can be further revalued hinges on whether new products driven by Muse (such as personal AI shopping assistants) can achieve commercialization, as well as changes in user adoption rates and payment behavior.

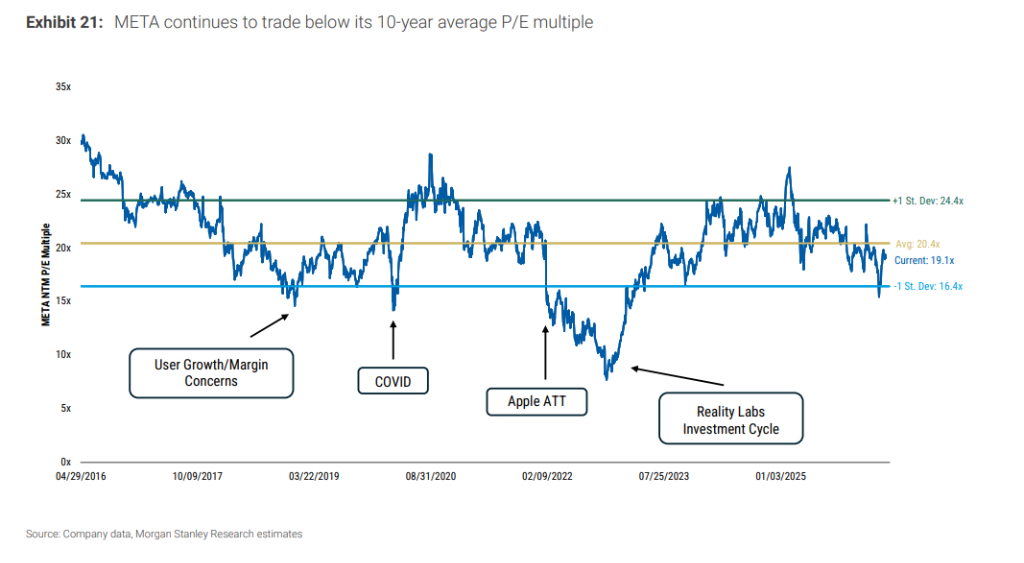

Morgan Stanley also noted that internal memos show management plans to cut about 10% of its workforce (approximately 8,000 employees) and close around 6,000 vacant positions (equivalent to an additional 8% reduction in headcount). For every 10% reduction in staff, it is expected to add approximately $0.50 to $1.50 to 2027 EPS. Currently, Morgan Stanley’s base forecast for META’s 2027 EPS is approximately $34, with a target price of $775, corresponding to a P/E ratio of about 23x, maintaining an “Overweight” rating.

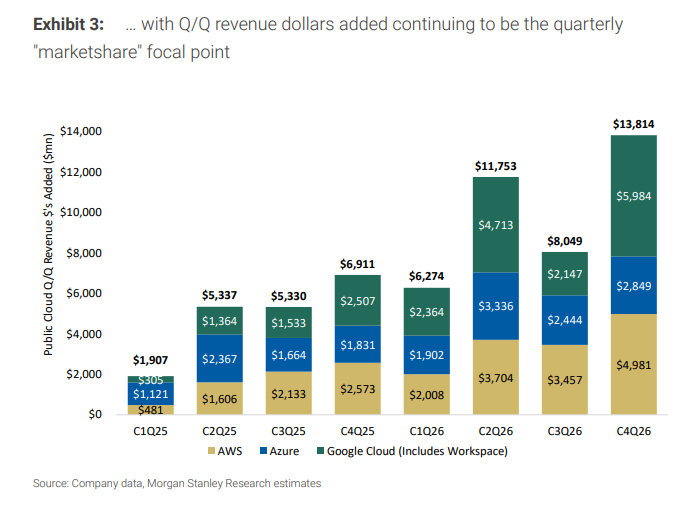

Cloud market landscape: Google surpasses AWS and Azure in quarterly incremental revenue for the first time

Looking at this 'market share barometer' of quarterly incremental revenue, Google Cloud added $2.3 billion in Q1, AWS added $2 billion, and Azure added $1.9 billion.

This is a noteworthy signal: Google Cloud’s quarterly incremental revenue exceeded that of AWS and Azure for the first time.

The combined backlog of orders at the end of the quarter for the three cloud providers has surpassed $1.5 trillion, signaling clear and sustained demand growth.

Editor/Lambor