The three major indices of the U.S. stock market opened higher collectively, continuing the momentum of the largest single-month gain in years— in April, expectations of profit expansion driven by robust spending on AI computing power infrastructure overshadowed all risk factors.

Following the strongest April for the U.S. stock market in six years, Wall Street institutional investors and leveraged hedge funds have begun to anticipate that prospects for U.S.-Iran peace talks and the so-called 'AI bull market narrative' could completely overwhelm the 'May curse' that has long troubled investors. The U.S. stock market surged in April, with two core indices posting their strongest monthly performance in nearly six years.

Driven by improved corporate earnings prospects and a wave of artificial intelligence investments, market sentiment has significantly recovered, even as risks from Middle East conflicts and energy supply disruptions have not fully subsided, with investors remaining optimistic.$S&P 500 Index (.SPX.US)$The S&P 500 rose 10.4% in April, marking its best monthly performance since November 2020; the Nasdaq Composite surged 15.3%, its largest gain since April 2020.

As markets anticipate that U.S.-Iran peace talks will take an optimistic path, and strong AI-driven earnings reports outweigh oil prices and geopolitical risks, Wall Street expects the robust rally seen in April—the strongest monthly gain in years—to extend into May.

As markets anticipate that U.S.-Iran peace talks will take an optimistic path, and strong AI-driven earnings reports outweigh oil prices and geopolitical risks, Wall Street expects the robust rally seen in April—the strongest monthly gain in years—to extend into May.

U.S. stocks opened higher on Friday after Pakistani officials announced that Iran's latest response to the U.S.-proposed peace agreement terms had been delivered to the U.S. government, significantly boosting expectations for a long-term U.S.-Iran peace deal. The three major indices of the U.S. stock market opened higher collectively, continuing the momentum of the largest single-month gain in years— in April, expectations of profit expansion driven by robust spending on AI computing power infrastructure overshadowed all risk factors.

$Microsoft (MSFT.US)$、 $Alphabet-C (GOOG.US)$ and$Amazon (AMZN.US)$The stellar earnings reported by these three cloud computing giants on the same night highlighted the unexpectedly explosive growth of cloud computing businesses benefiting from the AI wave, prompting Wall Street to reevaluate the commercial returns of AI. A recent research report by Morgan Stanley's analyst team forecasted that the combined capital expenditures of five hyperscale tech giants (Amazon, Google, Meta, Microsoft) are expected to reach approximately $800 billion by 2026.$Oracle (ORCL.US)$By 2027, this figure is projected to exceed $1.1 trillion, revised upward from the previous estimate of $950 billion.

Morgan Stanley's analysts emphasized that the core logic behind these massive investments lies in heavy upfront investment to build capacity, followed by scaling revenue and ROIC based on AI computing resources. The surge in cloud computing backlog orders serves as the most direct evidence that this logic works. The unexpectedly rapid growth of these giants' cloud businesses has prompted Wall Street to reassess the commercial returns of AI.

Overall, these tech giants aim to convince more investors that their massive investments in artificial intelligence are set to yield record-breaking returns. Therefore, for the global equity bull market driven by the AI computing power supply chain and the AI bull market narrative, their increasingly robust AI capital expenditures represent a solid positive factor that will continue to support the trajectory of this bull market. This includes leaders in the AI computing power supply chain such as AI GPU/ASIC, data center CPUs, HBM/NAND/HDD storage, 2.5D/3D advanced packaging, liquid cooling systems, optical interconnect supply chains, and data center power chains, all underpinned by the AI bull market narrative.

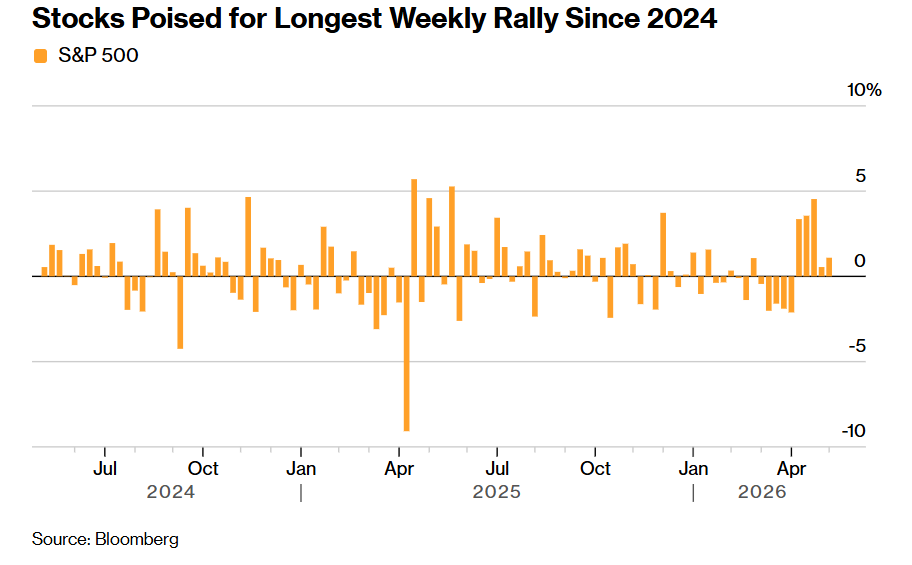

Does AI computing power overshadow everything? The strongest April in six years ignites Wall Street, while May’s market faces the 'endurance test.'

After experiencing the strongest monthly gains in years, U.S. stocks are preparing to push for further gains in May; the robust earnings season driven by AI computing power infrastructure spending remains the primary engine.

Friday's trading session will conclude a week packed with large-cap tech earnings reports and economic data. As the market enters May, investor attention is shifting to one key question: Can this rally continue? Historically, May often marks the start of a weaker six-month period for equities.

According to Fidelity data, from 1945 to April 2026, the S&P 500 Index averaged about a 2% increase during the May-to-October period. In comparison, the average gain during the November-to-April period was approximately 7%.

Although overall corporate earnings remain solid, some investors have expressed concerns about the tech giants’ frenzied AI spending spree. Questions about the sustainability of certain software business models have also emerged, prompting some investors who are relatively cautious about the AI computing power investment theme to reassess their portfolios.

Peter Vanderlee, portfolio manager at Mingce Group Investments, stated: 'The disruptive potential of AI in software, services, finance, and other industries has created uncertainty in the market regarding the longevity and endgame value of certain business models.'

Economic data released on Thursday further exacerbated market concerns that this frenzy of stock buying might need to face a reality check. Although U.S. economic growth regained momentum in the first quarter, consumer spending, the main engine of economic growth, showed signs of slowing, with the personal savings rate also declining, indicating that households are drawing down savings to support expenditures.

Moreover, these figures only account for one month of disruption caused by the conflict in the Middle East. With the potential for prolonged shipping disruptions in the Strait of Hormuz, rising oil prices could become an even heavier burden, especially as the boost from tax refunds in the first quarter begins to fade.

Samuel Tombs, chief U.S. economist at Pantheon Macroeconomics, remarked: 'On the surface, GDP in the first quarter expanded at a reasonably decent pace, but a closer look reveals that the underlying momentum of the U.S. economy was already quite weak before the full impact of the energy shock began to materialize.'

This time, is the 'May curse' no longer relevant?

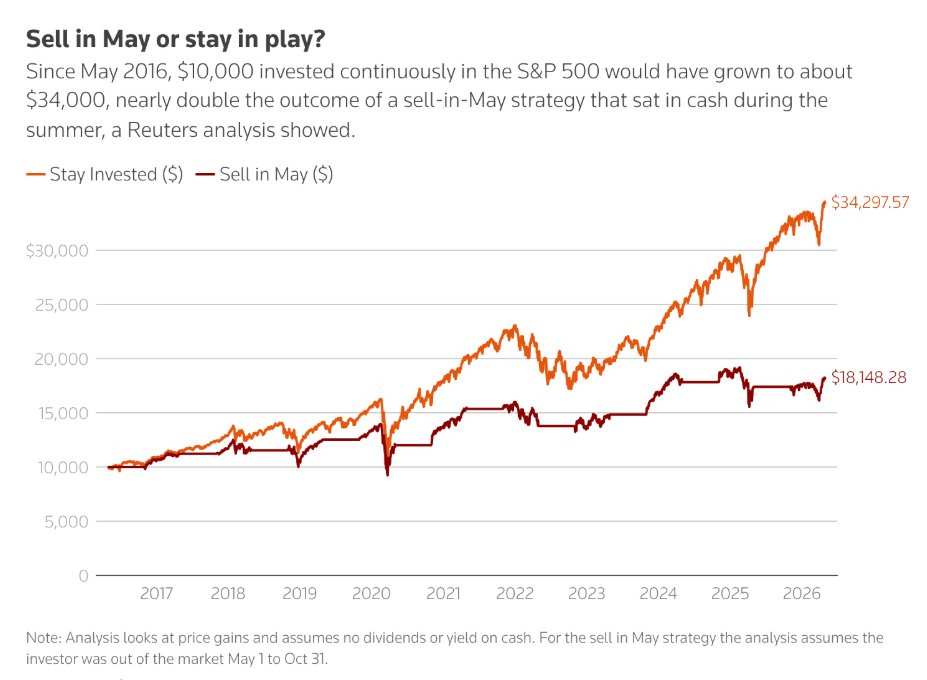

Blindly adhering to Wall Street's age-old adage 'Sell in May and go away' could prove costly for investors. As the market enters what is historically a more volatile period of the year, investors are weighing whether to conclude a strong market recovery rally.

The S&P 500 Index has staged a dramatic rebound; it took only 11 trading days to recover nearly 10% following a sell-off triggered by global oil supply disruptions. This rapid rebound has led investors to question whether the worst is over or if seasonal storms still lie ahead.

According to CFRA data, going back to 1945, the S&P 500 Index has seen lackluster long-term performance during the May-to-October period, with an average gain of 2%—far below the nearly 7% increase seen between November and April. However, the performance during this period over the past decade has been much stronger, averaging a 7% gain, including last year’s 22.1% surge.

Ryan Detrick, chief market strategist at Carson Group, commented: 'You really hate to say you should ignore the adage 'Sell in May and go away'... but over the past decade, it simply hasn’t worked.'

Referring to market performance over the past decade, he stated: 'If investors had blindly sold in May and shifted to cash or even defensive allocations, they would have significantly hurt themselves.'

An analysis report shows that if $10,000 had been continuously invested in the S&P 500 Index since May 2016, the investment would have grown to approximately $34,000, nearly twice as much as the "Sell in May" strategy, which holds cash during the summer months.

A senior strategist has indicated that several factors this year paint a more optimistic picture for the stock market, suggesting that being overly bearish simply due to calendar patterns is not appropriate.

As concerns over a large-scale escalation of the U.S.-Iran conflict ease, the stock market has strongly rebounded from a sharp sell-off. Strong corporate earnings have supported market sentiment, while the U.S. economy has demonstrated resilience amid the energy shock triggered by the Iran war.

Jim Carroll, portfolio manager at Ballast Rock Private Wealth, stated, "If there's any year you might consider throwing seasonal factors out the window, it might just be this year."

Since May 2016, $10,000 continuously invested in the S&P 500 Index would have grown to about $34,000, almost exactly twice as much as the "Sell in May" strategy. Additionally, long-term data compiled by CFRA shows that since World War II, when markets have fully recovered from pullbacks ranging from 5.5% to 9.9%, they typically rise by more than 8% in the subsequent three months.

Supported by the historical data of these positive perspectives and bolstered by a new wave of AI computing infrastructure spending exceeding $700 billion led by tech giants, as mentioned above, the robust upward trajectory of the global stock market driven by narratives around the AI computing supply chain and the AI-powered bull market may still have a long way to go.

The common signal from the latest earnings reports of the four major cloud giants is clear: even though individual stock performances diverge due to ROI, profit margin, or free cash flow pressures, total AI capital expenditure shows no signs of cooling down and is instead being revised upward.

For instance, Microsoft's earnings report was strong but not an impeccable celebration of AI achievements—investors acknowledged the increasing demand for computational resources around AI, yet they began demanding proof from management that massive AI CapEx could consistently translate into stronger revenue growth for cloud computing and software businesses, overall profit margins, and robust cash flow expansion. Nonetheless, Microsoft’s report confirmed the explosive expansion of AI computing needs (with $190 billion allocated for data center expansion and construction), Azure’s near-40% high growth rate, a solid foundation in enterprise software, and continued robust support for orders across the AI computing supply chain, including AI GPUs, AI ASICs, data center CPUs, and HBM.

For the AI computing supply chain, this represents a reinforcement at the level of 'order visibility': GPUs/ASICs, HBM/DRAM/NAND, HDDs, PCB/CCL/MLCC, optical modules, switches, copper cables, data center power equipment, liquid cooling, data center engineering, and power infrastructure will all benefit. Particularly, the current bottleneck is not only in GPUs but also extends to memory, storage, PCBs, networking, and power. Continued increases in CapEx by tech giants mean upstream hardware suppliers will maintain strong pricing power, capacity utilization, and order visibility.

Alphabet's cloud revenue grew by 63% year-over-year, with cloud backlog orders nearing USD 462 billion. Microsoft Azure grew by approximately 40%, with its AI business achieving an annualized revenue run rate exceeding USD 37 billion. These figures demonstrate that investment in AI is not merely停留在“叙事”层面 but has already materialized in cloud computing-related revenue generation, enterprise AI demand, and computational power consumption.

There is no doubt that the AI CapEx boom continues to serve as the main engine driving the bull market. However, the market is becoming increasingly discerning about “who can turn investments into actual revenue, profits, or even cash flow.” Alphabet rose due to strong cloud growth and high AI demand visibility, while Meta fell despite raising CapEx due to uncertainty about return on investment cycles. This suggests that the market is not indiscriminately rewarding spending but is instead identifying winners with clearer ROI. In conclusion, regardless of how individual earnings reports differ, the collective stance of the four major cloud giants—preferring to invest more rather than less—remains a strong support pillar for the AI computing supply chain and the AI-driven narrative fueling the current global stock market bull run.

Editor/Rocky