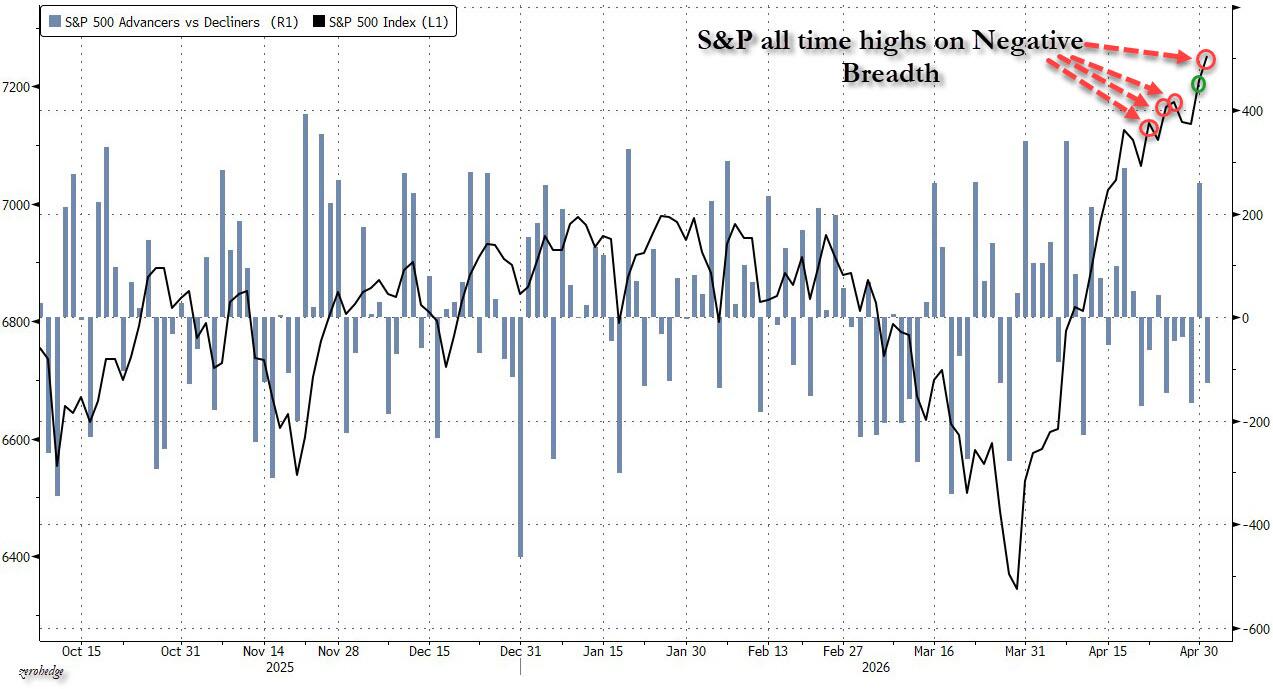

The S&P and Nasdaq hit new highs for two consecutive days and rose for five consecutive weeks. Trump expressed dissatisfaction with Iran's new proposal, causing the Dow to reverse gains; after earnings reports, Apple rose over 3%.SanDisk (SNDK.US)Surging more than 8%, software stock Atlassian and$Twilio(TWLO.US)$rose nearly 30% and over 20%, respectively;$Oracle(ORCL.US)$rose 6.5%; Spirit Airlines fell 25%.$美元指数(USDindex.FX)$After hitting a two-week low, it reversed in a V-shaped recovery, with the yen posting its largest weekly gain in over two months. Following news of Iran’s negotiation proposal, U.S. Treasury yields plummeted; gold and silver surged; crude oil hit a fresh daily low, with WTI briefly falling below $100 and dropping over 5%, but still posted gains for two consecutive weeks.

Iran submitted a new proposal regarding negotiations through a mediator, reigniting market hopes for the resumption of U.S.-Iran talks and long-term peace. The three major U.S. equity indexes initially rose in tandem, while crude oil prices plunged during trading. Although President Trump later stated that he was 'not satisfied' with Iran's proposal, dampening some market enthusiasm, strong earnings or guidance from certain companies subsequently drove tech stocks to push two major U.S. indexes to new all-time highs.

David Krakauer, Vice President of Portfolio Management at Mercer Advisors, commented that the positive momentum in the stock market could persist for some time. He expects the conflict in the Middle East to end in the short term, reopening the Strait of Hormuz.

Krakauer also believes that even if the conflict persists, the potential for earnings growth will continue to drive the stock market. 'We cannot rule out negative news triggering a minor pullback in the stock market, but overall we remain optimistic about equities.'

Krakauer pointed out that there will be winners and losers in the technology sector because not all AI-related capital expenditures will pay off, but he added, 'We believe the narrative around AI driving productivity improvements remains valid.'

In the last five trading sessions marked by new highs, Friday was the fourth day where the number of declining components in the S&P exceeded those rising, highlighting the risk of market support driven by a small number of high-momentum stocks.

According to CCTV citing Iranian media reports on Friday, May 1, Iran had submitted the text of its latest negotiation proposal to Pakistan on Thursday, with Pakistan acting as the intermediary for negotiations with the United States. Later, according to CCTV citing U.S. media, Pakistani officials stated that Iran's latest negotiation proposal had been forwarded to U.S. officials. The specific content of this new proposal has not yet been disclosed.

Following the report from Iranian media during European stock trading hours, the three major U.S. stock indexes opened higher collectively, with gains expanding in early trading, and the Nasdaq rising more than 1%. Near the end of the early trading session, Trump announced on social media that tariffs on EU cars and trucks would be increased next week. During midday trading, Trump stated at the White House that he was 'not satisfied' with Iran's new proposal. As a result, the S&P and Nasdaq pared some gains, while the Dow turned negative.

On Friday, Trump stated that Iran 'made some demands that I cannot accept,' but added that he 'would rather not' launch an attack on Iran. The White House sent a letter to Congress on the same day, stating that hostile actions against Iran had 'ended.' Tom Essaye, founder and president of Sevens Report Research, commented: 'In short, regarding U.S.-Iran relations, any ceasefire agreement will be positive for the market, while any resumption of attacks will be significantly negative.'

Among individual stocks, tech shares that reported earnings after Thursday's market close saw significant volatility. Apple, which posted record iPhone revenue for the previous quarter and provided surprisingly strong revenue guidance for the current quarter, opened higher and continued to rise, gaining nearly 6% in early trading. Two memory chip stocks, SanDisk and $Western Digital (WDC.US)$Western Digital, delivered impressive results but opened sharply lower on Friday, falling over 4% and approximately 7%, respectively, at the start of trading. However, SanDisk reversed losses and surged over 8% by the end of the session, while Western Digital briefly turned positive.

Analysts noted that the issue with SanDisk and Western Digital was not their performance itself, but rather that their valuations had become 'overextended'—with Western Digital's cumulative gain over the past year being approximately 900% and SanDisk’s cumulative gain since its IPO reaching around 3300%. Against this backdrop, strong earnings were already fully priced in, and the guidance issued by both companies on Thursday 'lacked sufficient surprises,' triggering profit-taking in the market.

Software stocks generally performed well, driven by better-than-expected earnings and guidance from workplace collaboration software company Atlassian and cloud communications software provider Twilio.

In commodities, international crude oil reacted sensitively to news of Iran submitting a new negotiation proposal, with declines rapidly widening. During early U.S. trading, WTI crude fell below the $100 mark, declining about 5.5% intraday. Brent crude also hit a fresh intraday low, approaching $106, down nearly 4% intraday. Gold, which had fallen over 1% during European trading, rebounded strongly and reached a fresh intraday high during U.S. morning trading, rising approximately 0.9% intraday.

In the foreign exchange market, the yen failed to maintain its strong rebound momentum. It refreshed its intraday high during Asian trading hours, surpassing Thursday's intraday peak when it rose 3%, but subsequently turned slightly negative. However, thanks to Thursday's sharp rally, the yen still recorded its largest weekly gain in over two months.

Japanese officials declined to confirm whether they had intervened in the currency market on Friday, while media analysis of central bank accounts suggested that the Japanese government may have used approximately $34.5 billion for forex intervention on Thursday. Traders believed that without further intervention, the yen's rebound driven by intervention risked fading, noting that the possibility of Japan re-entering the market to support the yen was increasing.

The U.S. dollar once fell 3% against the Japanese yen during Thursday's trading, amid reports that the Japanese government had intervened in the foreign exchange market for the first time since 2024. On Friday, the dollar-yen pair dropped below Thursday’s low, which some viewed as another possible intervention.

The S&P and Nasdaq closed at record highs for the second consecutive day and rose for a fifth straight week, marking the longest weekly winning streak since October 2024. Trump stated he was 'not satisfied' with the new proposal on Iran, causing the Dow to reverse gains. Following earnings reports, Apple rose over 3%, SanDisk surged more than 8%, while Western Digital, which had initially fallen 7%, ended down 0.6%. Software stocks Atlassian and Twilio jumped nearly 30% and over 20%, respectively. Oracle, which joined the Pentagon’s AI project, climbed 6.5%, while Spirit Airlines, reportedly preparing to suspend operations, plummeted 25%.

U.S. benchmark indices:

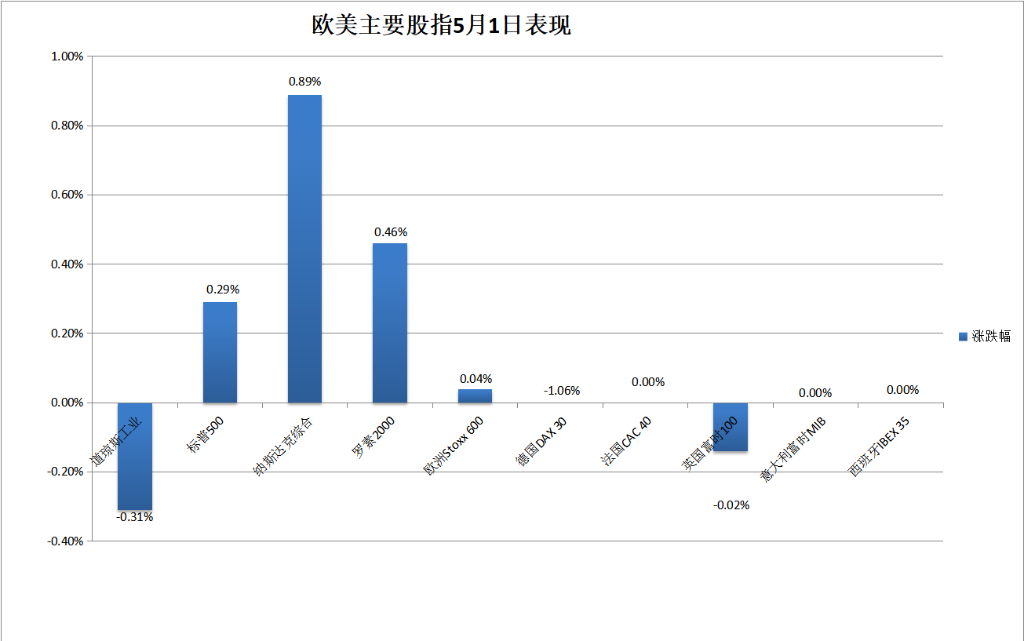

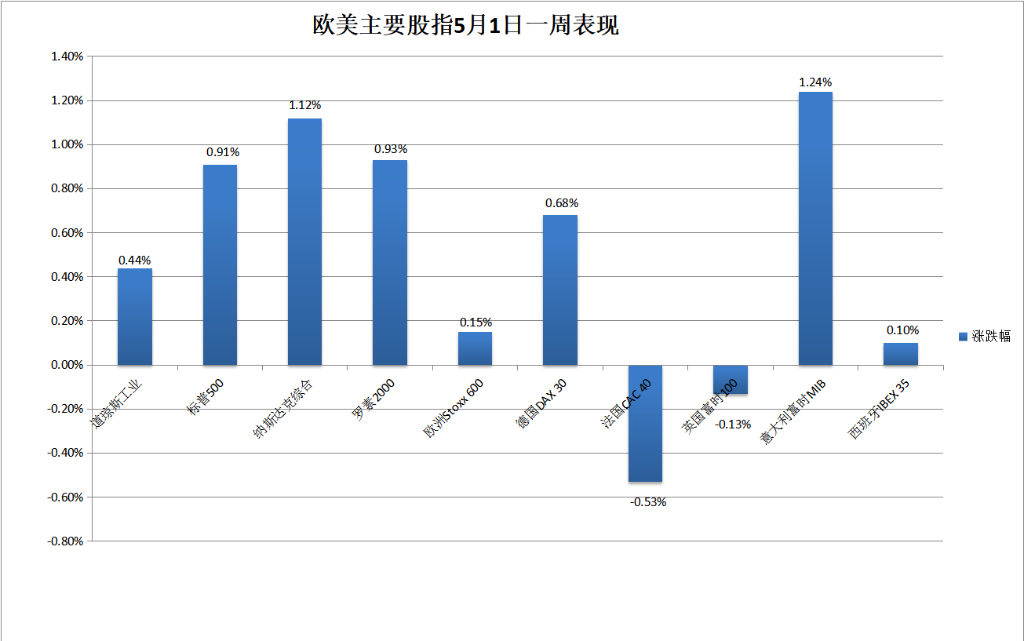

$S&P 500 Index(.SPX.US)$The index closed up 0.29% at 7,230.12 points, gaining 0.91% for the week.

The Dow closed down 152.87 points, or 0.31%, at 49,449.27 points, rising 0.44% for the week. This marked its fourth weekly gain in five weeks after rebounding last week.

The Nasdaq closed up 0.89% at 25,114.443 points, advancing 1.12% for the week.

the Nasdaq 100 Index (.NDX.US)The index rose 0.94% to close at 27,710.357 points, hitting a new all-time closing high for the second consecutive day. It, along with the S&P and Nasdaq, extended its winning streak to five weeks.

Russell 2000 Index (.RUT.US)The index gained 0.46% to close at 2,812.822 points, surpassing the 2,800-point mark for the first time ever. It advanced 0.93% for the week, marking its sixth consecutive weekly gain.

The Nasdaq Technology Market Value-Weighted Index rose 1.35% to close at 2,643.0291 points, reaching a new all-time closing high. It extended its winning streak to five weeks.

U.S. sector ETFs:

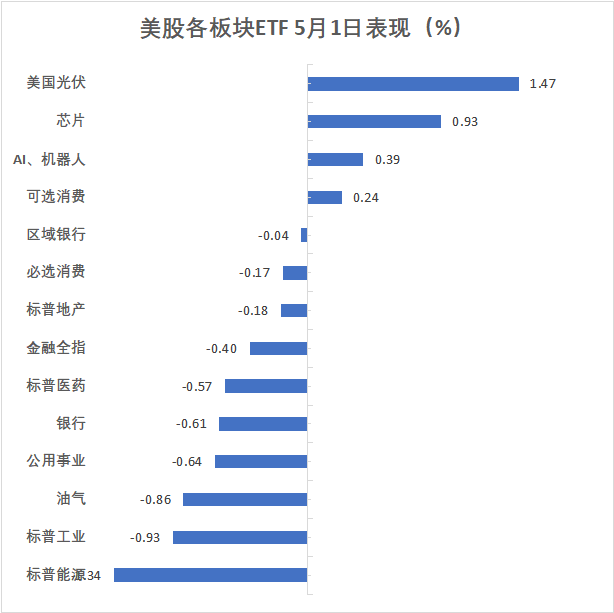

Sector ETFs including the Technology Sector ETF, Global Airline Industry ETF, Global Tech Stock Index ETF, and Internet Index ETF gained up to 1.49%. The Semiconductor ETF rose 0.61%, while the Banking ETF declined 0.19%, the Biotech Index ETF fell 0.84%, and the Energy Sector ETF dropped 1.34%.

Mag 7:

The Bloomberg Mag 7 Total Return Index rose 1.06% to close at 34,708.23 points.

Most of the Mag 7 closed higher on Friday, with Apple gaining nearly 3.3%.$Tesla(TSLA.US)$Up 2.4%,Microsoft (MSFT.US)Up nearly 1.6%,$Amazon(AMZN.US)$Up nearly 1.3%, Alphabet, the parent company of Google, rose over 0.3%, while$NVIDIA(NVDA.US)$Down nearly 0.6%, Meta fell 0.5%.

This week, the stock prices of several major companies that announced earnings showed mixed performance. Alphabet, which surged nearly 10% on Thursday after reporting earnings, gained almost 12%. Apple rose over 3%, Amazon increased by 1.7%, while Meta, which plunged over 8% on Thursday following its earnings report, fell nearly 10%, and Microsoft dropped over 2%. Additionally, Tesla gained nearly 4%, and NVIDIA, which fell nearly 5% on Thursday, declined close to 5%.

Chip Stocks:

Philadelphia Semiconductor Index (.SOX.US)Up 0.87% to close at 10,595.341 points, breaking the previous record closing high set on April 24, marking five consecutive weeks of gains.

AMD rose 1.7%,$Broadcom (AVGO.US)$Up over 0.9%,Taiwan Semiconductor (TSM.US)The U.S. stock market gained 0.4%, with Intel, which surged more than double in April, rising over 5.4%.

Among memory chip stocks, SanDisk, which had fallen more than 4% at the market open, closed up 8.25%.$Micron Technology(MU.US)$Western Digital, which had risen over 4.8% but fell 7% at the market open, closed down more than 0.6%.a hard drive manufacturer, It closed up 7.9%.

Chinese Concept Stocks:

The Nasdaq Golden Dragon China Index closed down 0.59% at 6,887.43 points, with a cumulative weekly loss of 0.94%, showing an overall V-shaped trend.

$Nio(NIO.US)$Nio fell 7.1%, XPeng dropped 2.7%, Li Auto declined 1.4%, Alibaba slipped 0.2%, while Tencent rose 0.3%.$NetEase (NTES.US)$It increased by 0.3%.$Yum China (YUMC.US)$It rose by 0.7%.

Earnings announcements for individual stocks:

Atlassian (TEAM), a workplace collaboration software company whose last quarter's revenue and full-year revenue growth guidance both exceeded expectations, closed up approximately 29.6%.

Twilio (TWLO), a cloud communication software provider whose first-quarter revenue and current quarter guidance both surpassed expectations, closed up over 23.8%.

First-quarter results were better than expected and announced a workforce reduction of 20%.Chicago Board Options Exchange (CBOE.US)closed up nearly 9%;

online gaming platform that cut its full-year order guidance and provided a second-quarter outlook below expectations$Roblox(RBLX.US)$closed down 18.3%;

after lowering its full-year profit forecast, raising investor concerns about consumers becoming more sensitive to spending, the household cleaning and personal care products manufacturerClorox (CLX.US)closed down nearly 9.7%.

Volatile individual stocks:

Oracle (ORCL) closed up nearly 6.5%. The U.S. Deputy Secretary of Defense for Research and Engineering announced on social media X that Oracle has officially agreed to join the list of AI companies collaborating with the Pentagon's classified networks.

Spirit Airlines (Spirit Aviation (FLYYQ.US)Shares closed down approximately 25.4%. Media reports indicate that Spirit Airlines is preparing to cease operations following the breakdown of bailout negotiations with the U.S. government. A company spokesperson declined to comment on ongoing discussions, stating that operations remain normal for now.

The pan-European stock index rebounded with two consecutive gains after four days of losses, narrowly posting a weekly gain. The German, French, Italian, and Spanish markets were closed for holidays, while energy and healthcare stocks weighed on the UK market, causing it to retreat.$AstraZeneca (AZN.US)$Fell more than 3%.

The pan-European stock index extended its winning streak to two days: the STOXX Europe 600 Index closed up 0.04% at 611.55 points, continuing to recover from the lowest level since April 7 hit on Wednesday. For the week, the index gained 0.15%, bouncing back from last week’s decline, marking the fifth weekly gain in six weeks.

STOXX Europe 600 sectors: Declines in crude oil prices dragged the oil and gas sector down by over 0.3%. Among its components, BP PLC fell 2.04% and Shell dropped 1.08%.$BP PLC (BP.US)$BP PLC shares closed down 2.04%,$Shell (SHEL.US)$The healthcare sector fell about 0.3%, with AstraZeneca listed in London dropping 3.13%.

Major European national indices: The German, French, Italian, and Spanish stock markets were closed on Friday. The UK market, which rebounded on Thursday, retreated.

For the week, most national indices posted cumulative gains. The German, Italian, and Spanish markets rebounded from last week’s declines, with the German index gaining in four out of the past five weeks, and the Italian and Spanish indices rising in five out of the past six weeks. Meanwhile, the French and UK indices saw two consecutive weeks of declines after four straight weeks of gains.

The impact of news on Iran negotiations sent oil prices fluctuating, causing a brief plunge in U.S. Treasury yields during trading hours. By the end of the session, performances diverged as long-term yields stabilized while short-term yields rebounded, flattening the yield curve.

U.S. Treasuries:

The yield on the benchmark 10-year U.S. Treasury note briefly surpassed 4.40% during early U.S. stock trading, hitting a fresh daily high. However, it quickly reversed gains and turned lower as crude oil prices hit a new intraday low during early trading, approaching 4.34%, a fresh daily low. It later resumed an upward trend, testing 4.39% during late U.S. stock trading. By the end of bond market trading, the yield stood at approximately 4.37%, unchanged from Thursday, with a cumulative weekly increase of about 7 basis points.

The yield on the 2-year U.S. Treasury note, which is more sensitive to interest rate expectations, rose above 3.90% during early U.S. stock trading, reaching a fresh daily high. It also reversed course during early trading, falling below 3.85% to hit a fresh daily low. By the end of bond market trading, the yield was approximately 3.88%, up about 1 basis point for the day. After ending three consecutive days of gains on Thursday, it rebounded, with a cumulative weekly increase of about 10 basis points. Both the 2-year and 10-year U.S. Treasury yields rose for a second consecutive week.

European debt:

By the end of bond market trading, the yield on the benchmark 10-year U.K. government bond was approximately 4.96%, down 5 basis points for the day. German bonds were closed for a holiday; on Thursday, the yield on the benchmark 10-year German government bond was around 3.03%, falling 7 basis points during the day.

This week, European bond yields continued to rise for two consecutive weeks. The 10-year UK bond yield climbed approximately 5 basis points cumulatively, while the 10-year German bond yield increased by about 4 basis points cumulatively.

The ICE U.S. Dollar Index (DXY) fell below 98.00 during trading, hitting a two-week low, before reversing in a V-shaped recovery. The Japanese yen, which had surged significantly the previous day, turned negative during trading but still recorded its largest weekly gain in over two months. The offshore Chinese yuan once rose more than 100 pips to break above 6.83 before giving back most of its gains. Bitcoin approached $79,000 during trading, rising more than 3% from the intraday low.

US Dollar:

The ICE U.S. Dollar Index (DXY) quickly turned negative before European stock trading and remained in decline. Losses widened during U.S. pre-market and early trading sessions, dropping to 97.72 during early U.S. stock trading, hitting the lowest level since April 17, down more than 0.3% for the day. During midday U.S. trading, it reversed to positive territory, and after U.S. stock trading ended, it reached a fresh daily high of 98.244.

By the end of Friday's foreign exchange trading, the U.S. Dollar Index was above 98.20, up nearly 0.2% for the day, but down more than 0.3% for the week. The Bloomberg Dollar Spot Index, which tracks the dollar against ten other currencies, rose approximately 0.1% during the day but fell nearly 0.3% for the week. Both indices rebounded after halting two consecutive days of gains on Thursday, retreating following last week’s rebound.

Yen:

The Japanese yen, which had surged by 3% on Thursday to record its largest intraday drop in nearly two years, fluctuated into negative territory several times during trading. Following a sharp rise of nearly 2.4% on Thursday, the yen posted its largest weekly gain since the week of February 13.

The USD/JPY pair hit a fresh daily high of 157.33 during Asian trading, up nearly 0.5% for the day. Before European stock trading, it plunged into negative territory, falling to 155.50, below Thursday's intraday low of 155.57, down about 0.7% for the day. It subsequently rebounded slightly multiple times, closing at 157.01 during foreign exchange trading, up nearly 0.3% for the day. However, it remained far from Thursday’s pre-plummet high above 160.70, which was the highest since July 2024. For the week, USD/JPY fell nearly 1.5%.

Renminbi:

The offshore Chinese yuan (CNH) against the U.S. dollar fluctuated into negative territory several times during Friday’s trading, hitting a fresh daily low of 6.8360 during European stock trading. It fully reversed losses before U.S. stock trading began, expanding gains during early U.S. trading to reach a fresh daily high of 6.8233, up 127 pips from the intraday low. After the U.S. stock market opened, it gave back most of its gains. At 4:59 AM Beijing time on May 2, it was quoted at 6.8310 yuan, up 10 pips from the New York close on Thursday. After last week’s retreat, it gained 36 pips this week, marking the fourth weekly gain in the past five weeks.

Cryptocurrency:

Bitcoin (BTC) fell below $76,200 during the early Asian trading session, hitting a new daily low. It then approached $78,900 near the U.S. stock market opening, marking a new daily high and representing a rise of over 3% from the day's low. This continues its recovery from Wednesday’s drop below $75,000, which had marked the lowest level since last Tuesday, April 21. At the close of the U.S. stock market, Bitcoin was above $78,300, with a gain of over 2% in the past 24 hours and nearly 1% over the previous week.

Looking to pick stocks or analyze them? Want to know the opportunities and risks in your portfolio? For all your investment-related questions,just ask Futubull AI!

Editor/Liam