Oil Price 'June Judgment Day': If China and the US buffer runs out, Brent crude oil may surge to a historical high.

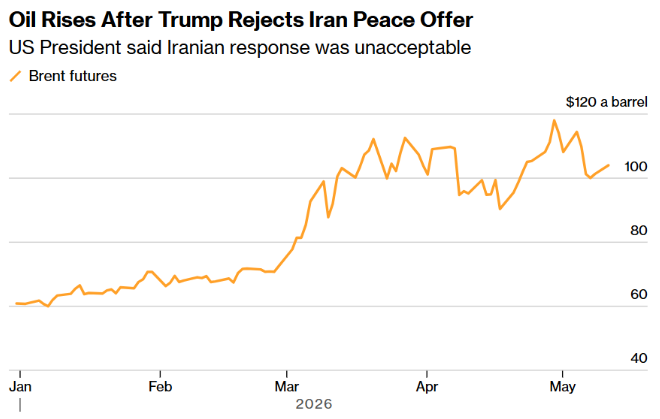

As the blockade of the Strait of Hormuz enters its eleventh week, Wall Street is reassessing the global crude oil pricing framework with unprecedented intensity. The U.S. and Iran again rejected each other's ceasefire proposals over the weekend, causing Brent crude to surge by 4.6% during Monday's trading session to $105.99 per barrel. Since the outbreak of the Iran war at the end of February, oil prices have risen nearly 50%. From Morgan Stanley’s 'race against time' to Citi's warnings of 'tail risk,' and Barclays' rare hawkish stance that 'risks can only go up,' Wall Street is collectively outlining a spectrum of oil price trajectories ranging from 'moderate upside' to 'record highs'—forming the core framework for evaluating potential global macro shocks in the coming months.

From $100 to $200: Wall Street’s Price Prediction Spectrum

Morgan Stanley: A Precise Framework for the 'Race Against Time'

In its latest research report, Morgan Stanley Chief Commodities Strategist Martijn Rats' team revealed a highly significant numerical fact with pricing implications: the U.S. increasing exports by 3.8 million barrels per day and China reducing imports by 5.5 million barrels per day together provide a supply buffer of up to 9.3 million barrels per day for the global market. This scale explains why, despite nearly one billion barrels of supply losses, Brent crude prices have yet to surpass their post-Russia-Ukraine war peak in 2022.

In its latest research report, Morgan Stanley Chief Commodities Strategist Martijn Rats' team revealed a highly significant numerical fact with pricing implications: the U.S. increasing exports by 3.8 million barrels per day and China reducing imports by 5.5 million barrels per day together provide a supply buffer of up to 9.3 million barrels per day for the global market. This scale explains why, despite nearly one billion barrels of supply losses, Brent crude prices have yet to surpass their post-Russia-Ukraine war peak in 2022.

However, this line of defense is approaching a critical point. Morgan Stanley explicitly warned that if the blockade persists until late June or July, the buffering mechanism will be completely exhausted. In its bullish scenario, Brent crude prices would rise to between $130 and $150 per barrel. The bank left a weighty statement in the report: 'The path is crucial—reopening in June with partial U.S.-China buffers still intact remains the baseline scenario; if the closure extends to the end of June or into July, Brent crude prices will inevitably feel pressures that had been avoided thus far.'

Even under the most optimistic scenario, Morgan Stanley made a sobering judgment for the market: even if the Strait of Hormuz were to reopen tomorrow, the time required to restart oil fields, repair damaged refineries, and reallocate tanker tonnage means the market will still face an irreversible loss of one billion barrels of crude oil supply for the remainder of 2026. The bank’s quarterly baseline forecast is as follows: Brent crude at $110 per barrel this quarter, $100 over the next three months, and falling back to $90 in the fourth quarter.

Goldman Sachs: $90—Silent but Intensive Upward Revision of Oil Price Forecasts

Goldman Sachs has released a series of intensive price reassessment signals over the past three weeks. On May 8, Goldman Sachs raised its 2026 Brent crude forecast from $77 to $85 in a research note sent to global institutional clients, characterizing the current supply shock as 'one of the largest supply disruptions in the history of the oil market,' comparable to the oil crises of the 1970s and the natural gas shock of 2022. According to the bank’s tracking data, global commercial crude inventories have fallen to an eight-year low of approximately 101 days of demand, expected to compress further to 98 days by the end of May; refined product buffers have rapidly contracted from 50 days of pre-war demand to 45 days—with jet fuel and naphtha stocks nearing operational stress levels.

More critically, Goldman Sachs introduced an observation in the report that had not been fully discussed by mainstream institutions: if normalization of the Strait of Hormuz remains delayed beyond mid-June, oil prices could surpass the peaks seen in 2008 and 2022. The bank simultaneously raised its fourth-quarter Brent forecast to $90, a full $10 increase from the previous prediction of $80.

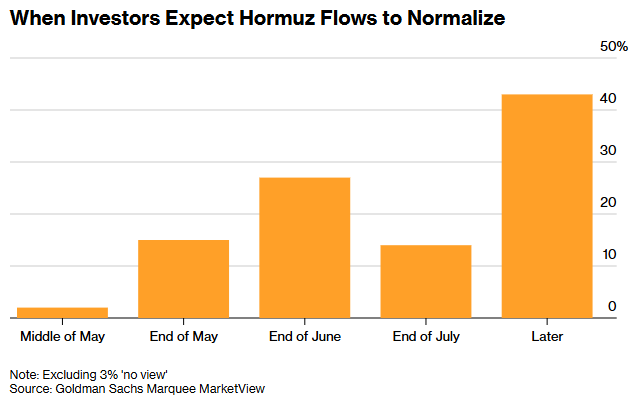

A survey of 837 institutional clients conducted by Goldman Sachs’ Marquee MarketView showed that 43% of respondents expect shipping to normalize only after July, while about one-third predict year-end Brent crude prices will fall within the $80 to $90 range. This indicates that a large number of investors are still betting on a more optimistic timeline, creating significant tension with Goldman Sachs’ increasingly upward forecasts.

Citi: $120 Price Level – Risk of Negotiation Deadlock

Citi occupies a position of 'high anchoring, increasing risk' in the current analysis on Wall Street. The bank has maintained its short-term forecast for Brent crude oil at $120 per barrel for the next three months, with an average price of $110 in the second quarter, dropping to $95 in the third quarter, and further declining to $80 in the fourth quarter.

However, the real marginal information from Citi does not lie in the forecast figures themselves, but rather in a key shift in their qualitative assessment of oil price risks. In their latest report, the bank emphasized: 'We continue to believe that the oil market is underestimating both the duration of the blockade and the tail risks.' Citi pointed out that the ongoing deadlock in U.S.-Iran negotiations has increased the short-term risk of oil prices climbing further from their current high levels, even though China's recent daily reduction of about 5.5 million barrels of crude oil imports has helped ease some supply pressures.

This implies that Citi is warning of asymmetry in risk distribution: after factoring in accelerating inventory declines, the release of strategic petroleum reserves, China’s import contraction, and intermittent signs of easing tensions, the true upside risk remains concentrated in the tail-end probability of a negotiation breakdown.

JPMorgan: 'If the blockade extends until mid-May, $150 is within reach.'

In a rapidly market-moving research report released by JPMorgan in April, it was predicted that if the blockade of the Strait of Hormuz persists until mid-May, Brent crude could rise in the short term to between $120-$130, or even exceed $150. However, JPMorgan’s true anchor point is closer to Goldman Sachs', assuming relatively quick resolution of the conflict and accelerated OPEC+ production recovery.

As of May 11, this early projection had partially materialized — with the arrival of the mid-May milestone, although oil prices did not reach $150, they have indeed remained in the $105-$109 range for several weeks. The latest pricing in derivatives markets shows that the probability of WTI crude reaching $150 has been priced at 39.5%.

Bank of America: '$100 is the New Normal' – A Comprehensive Reset of the Macroeconomic Framework

It was reported that Bank of America fully revised its economic outlook framework in April. Economist Claudio Irigoyen's latest analysis builds on an unprecedented benchmark: against the backdrop of the ongoing Hormuz crisis, annual oil prices will remain around $100 per barrel, starkly contrasting with Wall Street's forecasted range of $50 to $60 per barrel by the end of 2025.

Irigoyen characterizes the current situation as a 'mild stagflation shock' — where the transmission of rising energy prices into inflation occurs far faster than its drag on GDP. Based on this, Bank of America raised its 2026 U.S. inflation forecast from 2.8% to 3.6%, while lowering its economic growth forecast from 2.8% to 2.3%; global inflation forecasts were adjusted upward to 3.3%, and growth forecasts reduced to 3.1%. Under an escalated scenario, Bank of America warns that average oil prices could reach $130, with peaks potentially exceeding $150. Francisco Blanch, head of commodities research at the bank, presciently noted in March: 'If we find ourselves in the same situation by May, we may see oil prices spike to $160 per barrel. If the situation persists, Brent could break above $200.'

Stalemate in US-Iran Negotiations

The core differences between the US and Iran are concentrated on two key provisions of a 'one-page memorandum': Iran’s suspension of uranium enrichment activities and the transfer of its existing stockpile of highly enriched uranium abroad, and the US lifting sanctions and reopening the blocked Strait of Hormuz. On the duration of the uranium enrichment suspension, the US demands 15 to 20 years, while Iran agrees to only 5 years; currently, the compromise under discussion ranges from 12 to 15 years, after which Iran would be allowed to resume uranium enrichment up to 3.67% purity – whereas Iran currently holds approximately 60% purity highly enriched uranium, with nuclear weapons requiring 90% purity.

On Monday, Trump publicly rejected Iran’s response to the US’s latest peace proposal, while Iran's Foreign Ministry spokesperson described their own text as 'both reasonable and generous,' suggesting a significant gap remains between the two sides. The public statement by US Secretary of State Rubio has actually revealed a softening of strategic intent – Washington quietly abandoned the four major objectives it had previously proposed (destroying Iran’s ballistic missile capabilities, dismantling its navy, cutting off support for proxy armed groups, and ensuring Iran never acquires nuclear weapons), meaning that the US has shifted its bottom line at the negotiating table: prioritizing the resolution of the Hormuz issue, leaving the nuclear issue for subsequent negotiations.

However, it remains unclear whether Iran is willing to cooperate with this rhythm. The US Central Command continues to enforce a maritime blockade, having altered the course of 58 merchant ships since April 13 and rendered four vessels inoperable; meanwhile, Aziz, chairman of Iran’s parliamentary committee on national security and foreign policy, issued a rare warning to the international community: the Strait of Hormuz is a 'vital lifeline. Do not personally seal its gates.'

On the same day, the CEO of Saudi Aramco issued a rare stern warning: the global energy system has lost approximately one billion barrels of supply over the past two months, and even if the strait becomes navigable immediately, the energy system will require a 'considerable amount of time' to return to normal. A senior executive at German shipping giant Hapag-Lloyd revealed that since the outbreak of hostilities, the company has incurred an additional cost of at least $50 million per week, cumulatively approaching $500 million.

Summary

In the latest assessments from Wall Street’s six major banks, a common focal point is emerging – June. With almost mathematical precision, it anchors the critical juncture of logical divergence within each institution’s framework: Morgan Stanley uses June as the dividing line for whether the buffer mechanism between the US and China can be maintained, with the baseline scenario assuming a restart prior to that; Goldman Sachs sets mid-June as the threshold, beyond which continued blockades would trigger a pricing logic 'potentially surpassing the 2008 peak'; Citi designates the end of May as the deadline for the negotiation timetable, with upward risks intensifying if no agreement is reached by then; JPMorgan’s early projections identified mid-May as the turning point, which has now partially materialized; and Goldman Sachs’ investor survey shows that more than 50% of respondents expect shipping disruptions to continue beyond the end of June.

Behind this 'June window' lies a rigorous underlying logical chain: once the buffers for both the US and China successively peak, the global market will lose its final two safety valves, and prices will have no choice but to 'do what they have so far successfully avoided' – soar.

Synthesizing the assessments from the six major banks, a clear consensus on pricing is emerging from Wall Street’s meticulous analysis: if the Strait of Hormuz reopens around June under the baseline scenario, the annual average price of Brent crude will moderately retreat to the $85-100 range; however, if the 'June window' is easily breached, oil prices will inevitably surge to the vast range of $130-150 per barrel, potentially reaching a post-financial crisis high of $200. The 'truth about tail risk' warned by Citi is now unmistakably clear – this tail is not the 1% in probability but is rapidly approaching the center of the probability distribution.

Editor/Lee