In addition to affecting borrowing costs (eroding corporate profit margins), the rise in U.S. Treasury yields could also trigger a rotation of funds from the stock market to the bond market, casting a shadow over the currently robust global stock market outlook.

According to Zhitong Finance, amid an energy shock triggered by conflicts in the Middle East, which exacerbated inflationary pressures and dampened market expectations for the Federal Reserve's easing of monetary policy, U.S. Treasury yields surged rapidly. As of this writing, the yield on the 10-year U.S. Treasury bond, often referred to as the 'global asset pricing anchor,' is nearing 4.5%, currently at 4.481%.

As the 'global asset pricing anchor,' the 10-year U.S. Treasury yield profoundly influences global borrowing costs, ranging from mortgage loans and corporate loans to sovereign debt. In addition to impacting borrowing costs (eroding corporate profit margins), the rise in U.S. Treasury yields may also trigger a rotation of funds from the stock market to the bond market, casting a shadow over the currently robust global stock market outlook.

However, according to Max Kettner, HSBC Holdings' Chief Multi-Asset Strategist, despite rising bond yields, the stock market still has room for further gains due to a strong recovery in corporate earnings and relatively low market positioning.

However, according to Max Kettner, HSBC Holdings' Chief Multi-Asset Strategist, despite rising bond yields, the stock market still has room for further gains due to a strong recovery in corporate earnings and relatively low market positioning.

Kettner stated that he is currently 'extremely bullish' on equities. He noted that corporate profits have experienced a V-shaped recovery, 'rising even higher from an already elevated base.' He added that the performance of this earnings season has been 'insane, absolutely insane,' with approximately 87% of companies surpassing market expectations, comparable to the period following the post-pandemic economic reopening.

At the same time, in Kettner's view, current stock valuations have not yet reached bubble-like levels. He pointed out that overall investor positioning remains relatively low, and whether considering systematic funds or actively managed funds, their capital flows are 'far from signaling a sell-off.'

Kettner believes that the current level of U.S. Treasury yields does not yet pose a threat. However, he acknowledged that if the Federal Reserve raises interest rates more than once, 'the market might find it somewhat difficult to handle.' He stated that interest rate risks mainly stem from the possibility of stronger-than-expected economic growth.

Kettner also mentioned that the current stock market rally is 'a phenomenon observed almost globally, except in Europe.' He believes that Europe is particularly vulnerable to the impact of Middle Eastern conflicts, heavily reliant on the reopening of the Strait of Hormuz, while lacking positive drivers from technology and artificial intelligence (AI).

On the other hand, Kettner highlighted that U.S. consumer data remains strong, including credit card spending and weekly retail sales figures, reflecting the continued resilience of the U.S. economy. Regarding Asian markets, he specifically noted that South Korea's stock market remains attractive, despite the Kospi index having surged 86% year-to-date driven by the AI boom. He stated, 'Positioning in the Korean market is actually not heavy,' and the valuation of South Korea’s main index remains reasonable.

A sharp reversal in policy expectations causes 'the global asset pricing anchor' to swing dramatically.

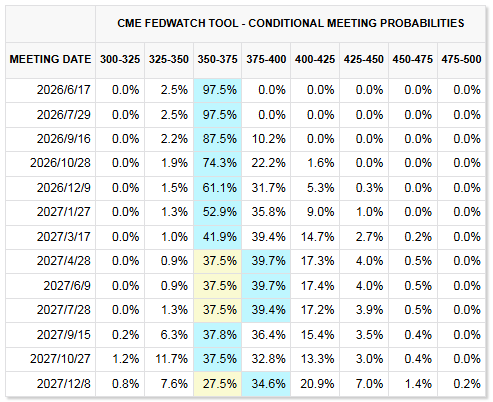

The dramatic shifts in the oil price and inflation environment have forced a historic reversal in market pricing of the Federal Reserve's policy path. Just before the outbreak of the Middle East war in mid-February, the overnight index swap market showed that traders widely expected the Fed to cut interest rates by about 50 basis points throughout 2026. However, the energy shock triggered by the war has completely shifted the interest rate outlook. Currently, interest rate swaps linked to the Fed’s rate decisions indicate that the probability of a rate hike by next April has exceeded 50%, with expectations for rate cuts being further postponed. The CME Group's 'FedWatch' tool shows that the probability of at least a 25-basis-point rate hike in December has risen to about 32%, with pricing now largely ruling out any rate cuts from now until the end of 2027.

Naokazu Koshimizu, Senior Interest Rate Strategist at Nomura Securities, commented: “There is now a strong trend of position adjustments in the market. The outlook has become highly uncertain—not only regarding how much rate cuts might be delayed but also whether there will be another rate hike next. Previously, the market had assumed that rate cuts would happen at some point, which supported buying behavior.”

This sharp reversal in expectations is also reflected in divisions within the Fed. Last month's Federal Open Market Committee (FOMC) meeting saw the highest level of dissent since 1992, with as many as three officials voting against the policy statement that signaled an easing bias. Even Milan, previously the most dovish Fed governor, has significantly softened his stance, substantially lowering his expectations for rate cuts. Meanwhile, the position of Wash, the incoming Fed Chair, has drawn widespread market attention, with markets generally expecting him to face extremely challenging policy choices upon taking office.

Across market dynamics, yields on U.S. Treasuries of all maturities have surged. In addition to the 10-year Treasury yield nearing 4.5%, the 30-year Treasury yield has broken through 5%, becoming the first long-term bond to surpass this psychological threshold. The 5-year Treasury yield has stabilized above 4%, while the 2-year Treasury yield has climbed to 4%.

10-Year Treasury Yield Nears 4.5%! Wall Street Engages in Intense Bull-Bear Debate

As the 10-year Treasury yield hovers near the 'psychological line in the sand' of 4.5%, Wall Street is embroiled in one of the fiercest debates in nearly two decades. On one side are the 'new hawks,' who believe inflation has structurally spiraled out of control and that yields are bound to surge toward 5%. On the other side are the 'bottom-fishing bulls,' who argue that high rates have reached their limit and that the bond market is presenting a golden buying opportunity. The outcome of this debate will directly determine the direction of the global asset pricing anchor.

Hawkish Warning: 5% May Not Be the End; Inflation Enters an 'Unfavorable Scenario'

The bearish camp, represented by Steven Barrow, Head of Strategy at Standard Bank, argues that the current rise in yields is not a short-term fluctuation but rather a fundamental reshaping of the global macroeconomic logic. Their core thesis is built upon a triad of 'war, policy, and structural factors.'

First, the impact of the Middle East conflict on the global energy supply chain is no longer a temporary shock but has transformed into a long-term premium cost. When energy prices remain elevated for more than 18 months, inflationary pressures will inevitably spread from fuel to services and wages. Second, the Fed's sluggishness in cutting rates early in 2026 has been interpreted by hawks as a compromise on inflation expectations, which could cause inflation expectations to lose their anchor due to this perceived 'soft monetary policy.'

A deeper reason lies in the return of structural inflation. From green costs driven by climate change, to tightened immigration policies restricting labor supply, to the fragmentation of global supply chains, these factors collectively create a 'high inflation, high interest rates, high volatility' new normal. In the eyes of hawks, the 10-year Treasury yield reaching 5% merely represents a return to pre-2007 norms rather than an extreme anomaly.

In its analysis on May 12, ING Groep noted that 'a 10-year Treasury yield of 4.5% is already within sight.' Once this level is reached, it will attract significant structural buying. However, this yield 'can just as easily continue to rise further,' especially given the absence of any signs of easing price pressures. The bank warned that if the war persists, inflation could rise to 5%, making it impossible for the Fed to cut rates in such an environment.

In its latest briefing in May, JPMorgan warned that 'the floor for inflation has risen.' They believe the 60/40 stock-bond portfolio is facing challenges, and the stickiness of inflation—particularly after the energy shock—could lead to further declines in bond prices.

Bulls Hold Firm: High Coupon Rates Are Justice, 4.5% Is the Stock Market Red Line

Meanwhile, the bulls have built a solid defense around the 4.5% mark. Charles Schwab and some asset management firms believe that the U.S. bond market has been oversold, and current yield levels already present extremely high allocation value.

Analysts who are optimistic about the bond market argue that while inflation data remains elevated, the resilience of American consumers will eventually run out. Rising borrowing costs have begun to suppress expansion in real estate and manufacturing, and slower economic growth will ultimately serve as an 'automatic brake' to curb rising yields. For long-term investors, locking in a risk-free return above 4.5% will be an excellent hedge during future recessionary cycles.

Moreover, the bulls are pinning their hopes on a 'technological miracle.' Although seasoned strategists like Barrow remain skeptical, some analysts at institutions like JPMorgan still believe that artificial intelligence’s boost to productivity will begin to show in the second half of 2026, offsetting energy-driven inflation by lowering production costs, thereby creating room for the Federal Reserve to cut interest rates.

Paul Hickey of Bespoke Investment Group's assessment in March perhaps best encapsulates the current market's delicate sentiment: seeing 4.5% by the end of the year would be less concerning; however, if it breaches 4.5% within a month or two, it will be a significant issue. Now, this 'major issue' seems to be approaching — the yield on the 10-year U.S. Treasury bond is just a step away from the 4.5% threshold, while the yield on the 30-year U.S. Treasury bond has already broken through 5%.

The market stands at a critical juncture. Bears hold the trump cards of energy shocks and fiscal deterioration, while bulls hope for slowing growth and central bank pivots. Regardless of which side prevails, once the psychological threshold of 4.5% is substantially breached, it will redefine the benchmark for global asset pricing.

Editor/Deng