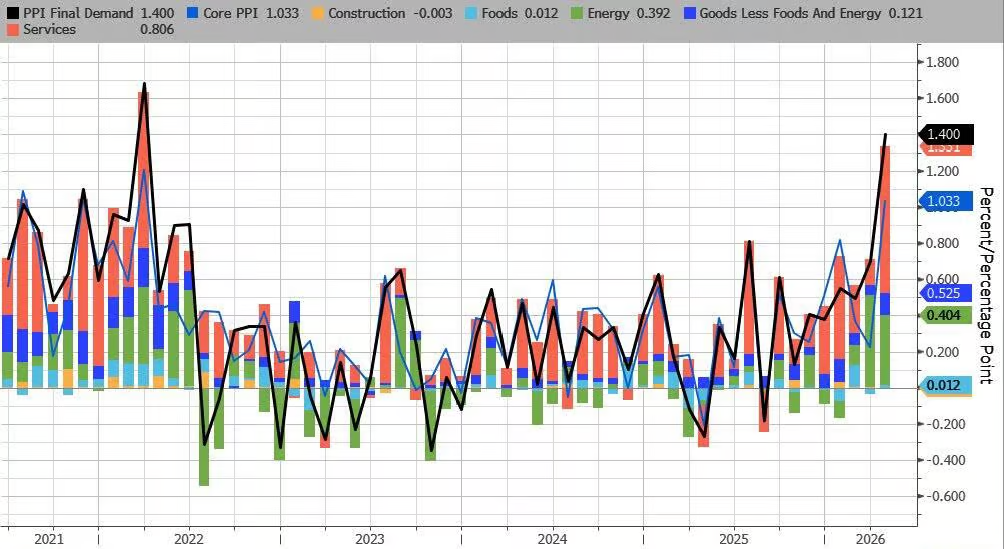

The U.S. PPI increased by 6% year-over-year and 1.4% month-over-month in April, with both figures marking the highest levels since 2022. The PPI has recorded month-over-month increases for eight consecutive months. Rising energy and transportation costs pushed service sector inflation to a four-year high. The market is pricing in approximately a 50% probability of one interest rate hike by the end of 2026.

Driven by a sharp rise in energy prices due to the Middle East conflict, the US Producer Price Index (PPI) for April significantly exceeded expectations, posting the largest increase in over three years. Consequently, US Treasury yields jumped, and market bets on Federal Reserve rate hikes notably intensified.

On the 13th, data released by the US Bureau of Labor Statistics showed:

The US PPI for April rose 6% year-over-year, reaching its highest level since December 2022. The forecast was 4.8%, and the previous value was 4%.

The US PPI for April increased 1.4% month-over-month, marking the largest single-month rise since March 2022. The forecast was 0.5%, and the previous value was also 0.5%.

The US core PPI for April rose 5.2% year-over-year. The forecast was 4.3%, and the previous value was 3.8%.

The US core PPI for April increased 1% month-over-month. The forecast was 0.3%, and the previous value was 0.1%.

Following the release of the data, the yield on 10-year US Treasuries rose by approximately 2 basis points, reaching about 4.49%, the highest level since July. The 2-year yield returned above 4.00%, hitting a new high since March. The money market has now priced in around 24 basis points of Fed rate hikes ahead of the June 2027 policy meeting, up from 21 basis points at Tuesday's close, with the market assigning roughly a 50% probability to one rate hike occurring within 2026.

Lindsey Piegza, Chief Economist at Stifel, stated on Bloomberg Television, "The discussion about rate hikes may be reopening, but the Fed's top priority is to remove accommodative language from its statement and reaffirm its wait-and-see stance." She also warned, "More concerning is that today’s report shows that the impact of inflationary pressures has not yet fully materialized." The PPI data followed Tuesday’s April CPI report, which also indicated a significant acceleration in consumer-side inflation driven by a sharp rise in energy prices.

Dual increases in energy and transportation costs push service sector inflation to a four-year high

The key drivers behind the sharp rise in April PPI were dual increases in energy and service prices. Data showed that energy costs surged 7.8% year-over-year in April, following an even larger increase the previous month; overall commodity price growth also reached its highest level since 2022.

Prices in the services sector rose 1.2% month-on-month, marking the largest increase in four years. Notably, transportation and warehousing service prices surged by 5%, driven primarily by rising road freight costs and expanding profit margins among fuel retailers. Analysts had previously identified this category as one of the most sensitive areas to energy price increases fueled by Middle Eastern conflicts. Against the backdrop of a fragile ceasefire and an unresolved conflict in the region, rising energy and transportation costs are gradually spreading to broader goods and services sectors, with mounting pressure on businesses to pass on these costs.

Notably, construction costs experienced a slight month-on-month decline this month, representing one of the few softer components in the report.

Components related to PCE remained relatively moderate, providing some buffer.

The core PPI, excluding food and energy, rose 5.2% year-on-year, surpassing market expectations and reaching its highest level in over three years. The month-on-month increase reached 1.0%, approximately three times the expected value of 0.3%.

Despite the alarming overall figures, certain components directly linked to the Federal Reserve's key inflation indicator—the Personal Consumption Expenditures Price Index (PCE)—showed relatively stable performance, offering some reassurance to market sentiment.

Specifically, portfolio management fees fell 2.4% month-on-month, while the month-on-month increases in various healthcare subcategories did not exceed 0.3%. Although airfare prices rose 3% month-on-month, the direct transmission to PCE-related components was limited overall.

This suggests that the direct impact of April’s PPI on PCE may not be as severe as the headline figures suggest. However, analysts warn that this is insufficient to fully alleviate concerns about inflation risks.

Treasury yields surged, reigniting discussions about interest rate hikes.

Two consecutive days of higher-than-expected inflation data have significantly shifted market expectations regarding the Federal Reserve's policy direction. Lindsey Piegza noted that the Fed is more likely to remove accommodative language from its policy statements and reiterate a wait-and-see stance rather than immediately raising rates. However, she emphasized that the pressures revealed by current inflation data have yet to fully permeate the broader economic system, and subsequent risks should not be overlooked.

Previously, the market widely anticipated that the Fed would maintain a wait-and-see approach or even pivot toward rate cuts. Following the release of the latest data, however, markets have begun pricing in the possibility of rate hikes, with the 2-year yield climbing back above 4.00%. Market estimates now assign roughly a 50% probability to at least one rate hike occurring by the end of 2026.

Editor/Deng