This marks the first time that the U.S. Treasury issued a 30-year bond with a coupon rate of 5% since August 2007. The Treasury has witnessed two consecutive auctions of 30-year bonds where the winning interest rates were higher than the pre-auction rates, signaling weak demand. The bid-to-cover ratio for this auction hit a six-month low.

The U.S. long-term Treasury bond market has once again sounded the alarm.

On Wednesday, August 13, Eastern Time, the U.S. Treasury completed a 30-year Treasury bond auction with a total scale of $25 billion. The final auction rate was 5.046%, marking the first time since August 2007 that the coupon rate for the same period reached 5%. This also highlights that, amid renewed inflation concerns and persistently widening fiscal deficits, investors are demanding higher returns to hold U.S. ultra-long-term bonds.

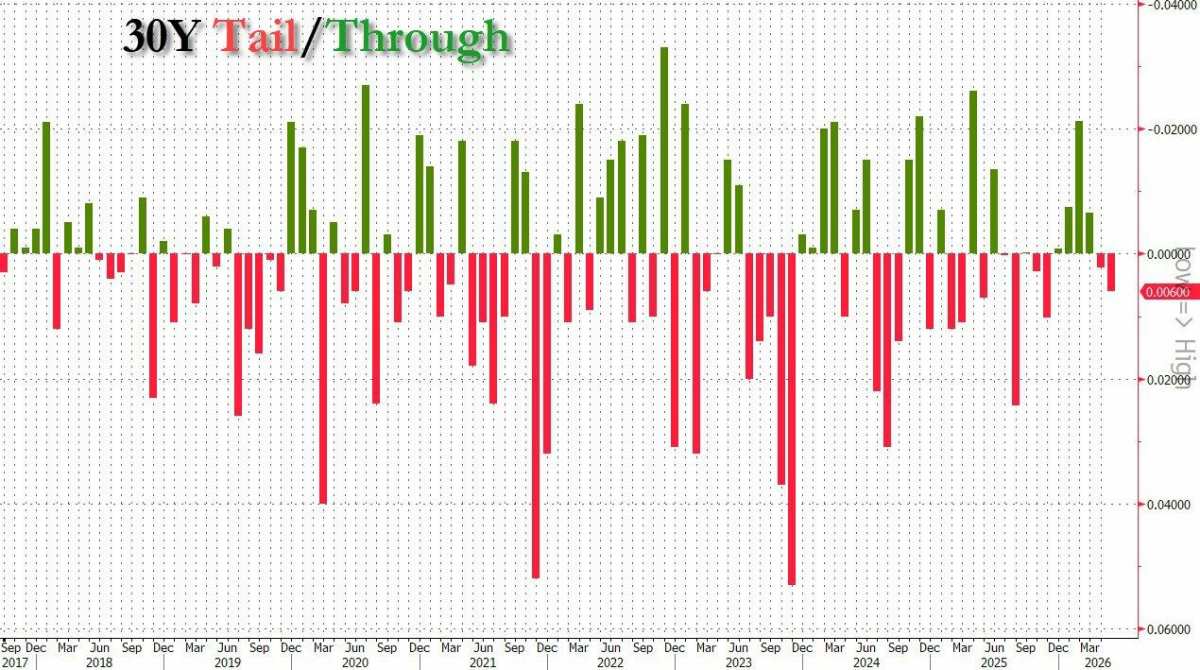

The results of this auction were evidently weak. The winning interest rate of the 30-year Treasury bond on Wednesday was significantly higher than the 4.876% rate from the previous auction in April. It was slightly above the secondary market trading level before the deadline for this auction, specifically the pre-issue rate of 5.041%, forming what is commonly referred to as a 'tail'—a signal typically viewed by the market as indicative of weak demand. Thus far, the U.S. Treasury has experienced a tail in two consecutive 30-year Treasury bond auctions.

The results of this auction were evidently weak. The winning interest rate of the 30-year Treasury bond on Wednesday was significantly higher than the 4.876% rate from the previous auction in April. It was slightly above the secondary market trading level before the deadline for this auction, specifically the pre-issue rate of 5.041%, forming what is commonly referred to as a 'tail'—a signal typically viewed by the market as indicative of weak demand. Thus far, the U.S. Treasury has experienced a tail in two consecutive 30-year Treasury bond auctions.

A financial blog described the outcome of this Treasury auction as 'ugly,' noting that this was the first time since the quantitative collapse in August 2007 that a 30-year Treasury yield reached 5%. As senior traders recalled, the historically significant 'quantitative collapse' in August 2007 not only marked the peak of the S&P index at the time but eventually evolved into a global financial crisis.

The bid-to-cover ratio for this auction was 2.303, down from 2.385 in the previous auction, lower than the average ratio of 2.43 over the past six auctions, and hit its lowest point since November 2025.

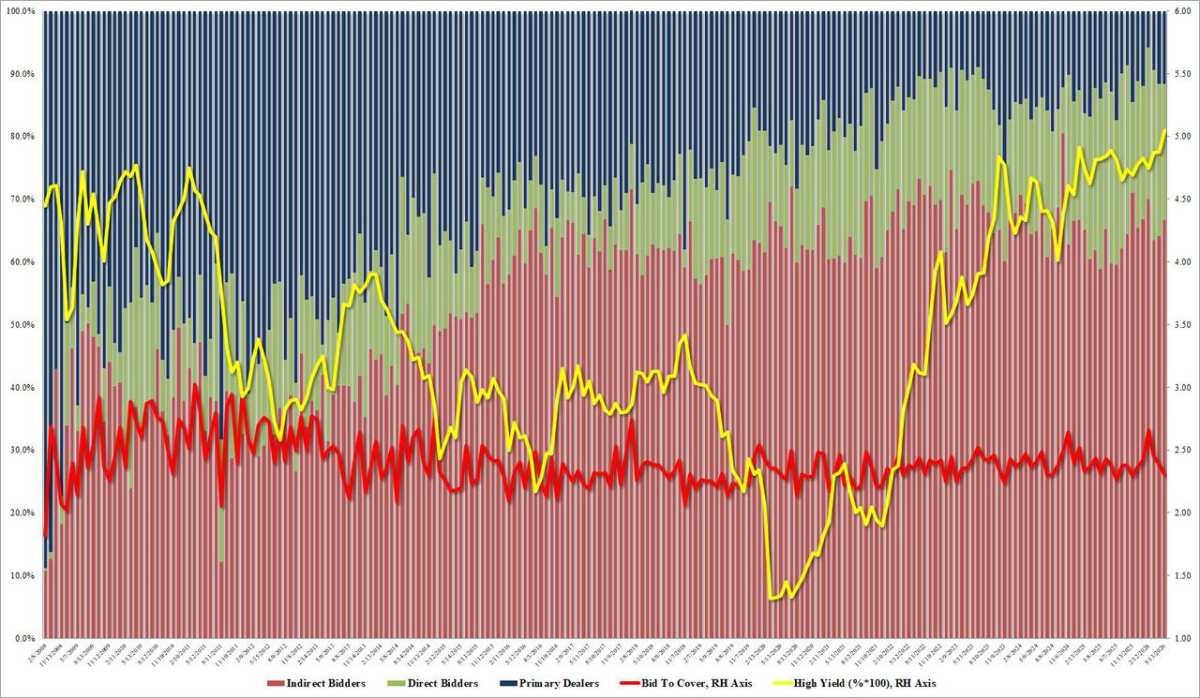

However, the internal structure data of the auction did not appear as dire: the allocation proportion for indirect bidders, which reflects demand from investors outside the U.S., including foreign central banks and other institutions, stood at 66.6%, higher than 64.1% in the April auction, and only slightly below the recent average of 66.8%. Direct bidders received an allocation of 21.74%, while primary dealers, who provide a backstop for the auction, took up the remaining 11.7%.

This auction continued the overall pressure seen in U.S. Treasury issuance this week. Previous auctions for 3-year and 10-year Treasuries both faced weaker-than-expected demand, indicating that investors’ ability to absorb large-scale U.S. debt supply is being tested as yields continue to rise.

What does it mean for the 30-year Treasury bond coupon to return to 5%?

According to U.S. Treasury regulations, if the auction rate for Treasury bonds falls between 5% and 5.124%, the corresponding bond coupon will be set at 5%. This means that this Wednesday marked the first time since 2007 that the U.S. Treasury issued a 30-year Treasury bond with a coupon rate of 5%.

Media outlets pointed out that the last time the U.S. issued a 30-year Treasury bond with a 5% coupon, it was on the eve of the global financial crisis and the U.S. economic recession. In the nearly two decades since, the coupon rate for 30-year Treasury bonds has never exceeded 4.75%.

During the peak of the COVID-19 pandemic, U.S. Treasury yields plummeted to historic lows. In May 2020, a 30-year Treasury bond issued by the U.S. Department of the Treasury carried a coupon rate of only 1.25%. Following the Federal Reserve's aggressive interest rate hikes thereafter, the price of the 30-year Treasury bond has now fallen to less than 50 cents on the dollar in order to attract buyers.

This also reflects the reality of a significant revaluation in the global bond market over the past few years:

The Federal Reserve has cumulatively raised interest rates by more than 500 basis points;

The U.S. fiscal deficit has continued to widen;

Long-term inflation expectations have resurfaced;

Investors are demanding a higher 'term premium' for holding U.S. Treasuries long-term.

Although the yield on 30-year U.S. Treasuries in the secondary market has risen above 5% multiple times in recent years, including during the Federal Reserve’s aggressive tightening in October 2023, what makes this time different is that the U.S. Treasury officially issued long-term bonds at a financing cost of 5%.

Rising energy prices fuel expectations of 'higher long-term interest rates'

The recent sustained rise in international oil prices is considered one of the key factors driving the renewed upward trend in long-term bond yields.

Market participants are concerned that escalating tensions in the Middle East and rising energy costs could push U.S. inflation higher again, forcing the Federal Reserve to maintain elevated interest rates for a longer period.

Meanwhile, the fiscal financing needs of the United States continue to expand rapidly.

In recent years, the US Treasury Department has continuously increased the scale of treasury bond auctions to fill the widening fiscal deficit. Media reports have pointed out that when the yield on long-term bonds first broke through 5% in 2023, the expansion of auction sizes by the Treasury was also one of the key contributing factors.

The market is increasingly concerned that the US government will need to conduct large-scale financing at high interest rates in the coming years, while demand for US Treasuries from overseas central banks and long-term investors has not grown correspondingly.

It is worth noting that the demand for 20-year US Treasuries has been consistently weaker than for 30-year bonds in recent years, resulting in higher yields. Since the US Treasury resumed issuing 20-year bonds in 2020, their yields have mostly remained above those of 30-year bonds. A 20-year bond issued in May this year has already reached a coupon rate of 5%.

Surging long-term bond yields trigger repricing of global assets

The yield on 30-year US Treasuries is considered one of the most crucial long-term interest rate benchmarks in global financial markets.

Its continued rise indicates: further increases in corporate borrowing costs in the US; upward pressure on mortgage rates; sustained pressure on valuations of technology growth stocks; and tighter global financial conditions.

Currently, the yield on 30-year US Treasury bonds is approaching the high point of this cycle, prompting the market to reassess whether 'higher for longer' interest rates could become the new norm for global markets in the coming years.

Some Wall Street institutions believe that a 5% yield on long-term US Treasuries is beginning to regain appeal for asset allocation. However, some investors are concerned that if the US fiscal deficit, inflation, and energy prices continue to deteriorate, the long-term bond market may still not have truly bottomed out.

Editor/Stephen