The yield on the US 30-year Treasury bond has risen above 5%, with long-term bond yields in multiple countries climbing to new highs. South Korea’s KOSPI index plummeted by 6%, and global stock markets have generally come under pressure. The core reason lies in the Middle East conflict driving up energy prices, leading to rising inflationary pressures and causing market expectations for interest rate cuts to collapse. Currently, the upward structure reliant on liquidity and leverage is becoming increasingly fragile. Market attention has shifted to the Federal Reserve's policy signals due to be released next week, as well as NVIDIA's earnings report.

Global financial markets experienced a rare 'double sell-off' in stocks and bonds on Friday, with panic quickly spreading from the bond market to equities.

Long-term government bond yields in the United States, Japan, Germany, and the United Kingdom surged collectively, reaching multi-year or even all-time highs. Meanwhile, U.S. stock index futures declined across the board, with the Nasdaq 100 falling by 1.5%. Both Asia-Pacific and European stock markets came under broad pressure, with South Korea's key index plunging by 6%.

The core logic behind this sell-off was clear and severe: Rising energy prices driven by Middle East tensions have reignited inflationary pressures, causing market expectations for central bank rate cuts to systematically collapse. According to Xinhua News Agency citing Iran’s Tehran Times on the 15th, the United States has rejected Iran's '14-point' written proposal to end the war.

The core logic behind this sell-off was clear and severe: Rising energy prices driven by Middle East tensions have reignited inflationary pressures, causing market expectations for central bank rate cuts to systematically collapse. According to Xinhua News Agency citing Iran’s Tehran Times on the 15th, the United States has rejected Iran's '14-point' written proposal to end the war.

At the same time, signals from both the equity and bond markets are increasingly aligned—while stock indices remain at high levels, gains are heavily concentrated in a few AI leaders; the bond market, meanwhile, has already priced in higher interest rates and inflation. With oil prices breaking through $100 per barrel and long-term interest rates continuing to rise, markets are growing increasingly concerned that the current rally, which relies heavily on liquidity and leverage, is far more fragile than it appears on the surface.

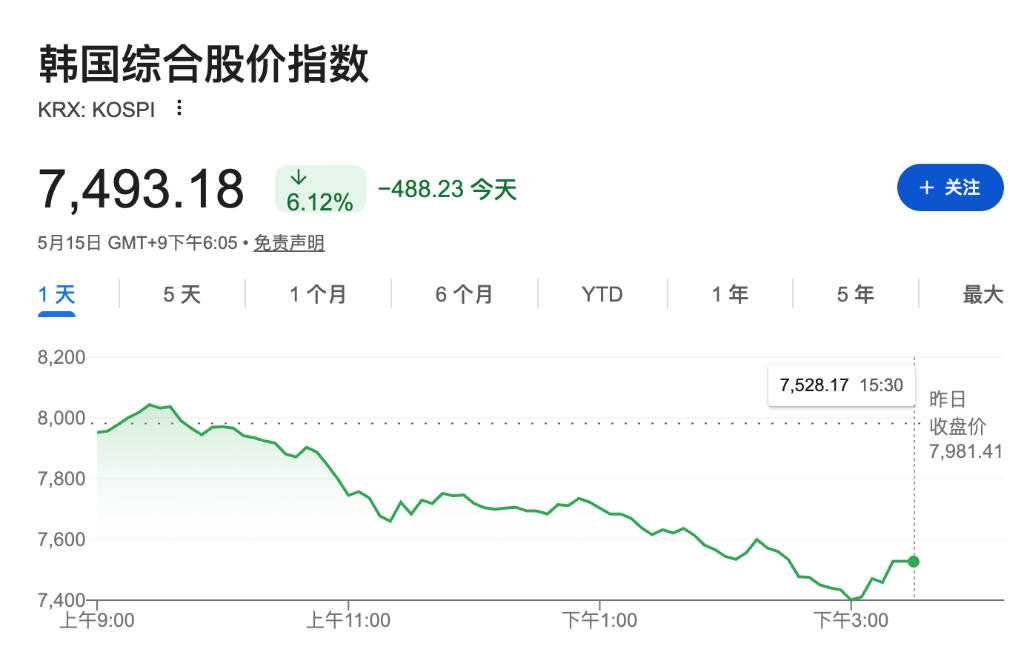

From a technical perspective, the yield on the U.S. 30-year Treasury bond firmly surpassed 5% on Friday, while the 10-year Treasury yield rose to 4.53%, hitting a new high since May 2025. The yield on Japan's 30-year government bond broke through 4% for the first time since its issuance in 1999. South Korea’s KOSPI index briefly touched an all-time high above 8,000 points during trading but then sharply reversed, closing down 6%. This indicates that in an environment of crowded trades and high leverage, shifts in market sentiment can occur much faster than anticipated.

South Korean stocks plunged shortly after hitting record highs, exposing vulnerabilities in the AI-driven bull market.

The world’s strongest-performing stock market hit the brakes abruptly on Friday.

South Korea’s KOSPI index briefly reached 8,000 points during early trading before plummeting, ending the day with a 6% loss. Samsung Electronics fell 8.6%, and SK Hynix dropped 7.7%. These two chip giants alone accounted for two-thirds of nearly 90% of the KOSPI’s gains this year.

Jun Gyun, a derivatives analyst at Samsung Securities, stated: 'The market is showing signs of fatigue, and caution is spreading. This pullback appears to be a result of exhaustion following rapid and steep gains rather than indicative of deteriorating earnings or a bubble burst. It is still too early to draw conclusions.'

The sharp volatility in South Korea’s stock market is emblematic of global markets today: when gains are overly concentrated in a handful of AI beneficiaries, profit-taking can trigger violent adjustments in indices within extremely short periods.

Surge in U.S. Treasury Yields: Inflation Takes Over as the Dominant Pricing Driver, Rate Cut Window 'Effectively Closed'

The pricing logic of the U.S. Treasury market is undergoing a fundamental shift.

The yield on 2-year U.S. Treasuries has climbed to 4.075%, significantly higher than the Federal Reserve's upper policy rate limit of 3.7%. The market signal is clear: financial conditions are tightening spontaneously. The market believes that at next month’s policy meeting, the Federal Reserve is no longer facing the question of 'how much to cut rates,' but whether a rate hike is necessary.

Economists at Goldman Sachs have postponed expectations for the next rate cut to December 2026, with a second adjustment pushed back to March 2027, both by 25 basis points. Meanwhile, the auction yield on 30-year U.S. Treasuries hit a new high since August 2007, reflecting growing pressures from long-end supply and inflation concerns.

As Wash succeeds Powell as the Fed Chair, the economic environment he faces is vastly different from his predecessor, replaced by the reality of energy prices driving CPI close to 4%. Currently, the market expects the probability of a rate hike before December is nearing 40%.

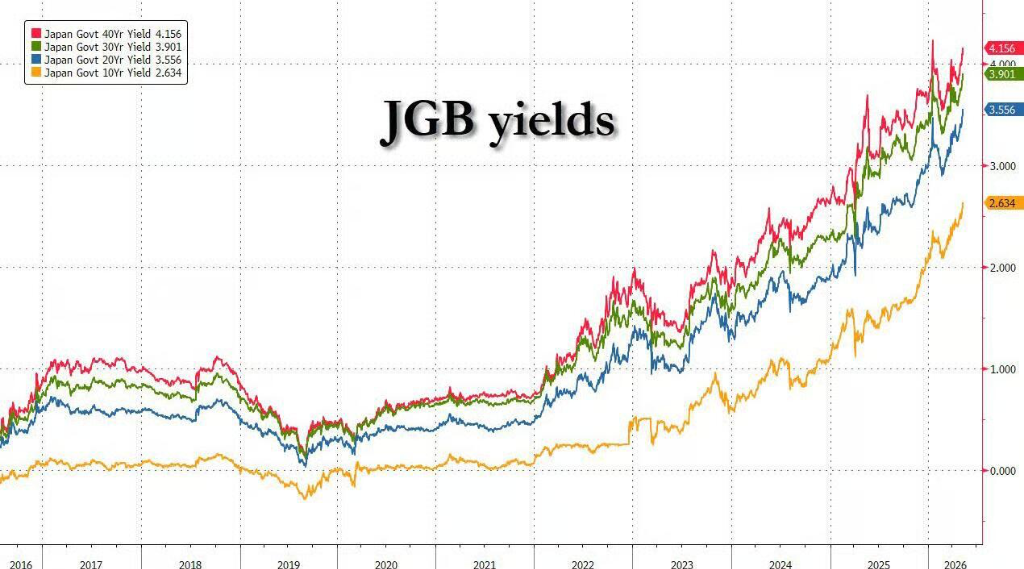

Japan’s 30-Year Government Bond Yield Breaks 4% for the First Time, Accelerating Exit from Deflation Era

Changes in Japan’s bond market carry profound implications for global asset pricing.

On Friday, Japan’s 30-year government bond yield broke through 4% for the first time, while the 40-year yield rose to 4.23%, both hitting record highs. The 20-year yield also climbed to its highest level since 1996. Japan, which has long been in a zero-interest-rate environment, is accelerating its exit from the deflation era.

According to Bloomberg, although Japanese Finance Minister Satsuki Katayama reiterated that there is currently no need to draft a supplementary budget, market concerns about fiscal discipline have clearly risen. More critically, the persistent depreciation of the yen is forcing markets to price in rate hikes by the Bank of Japan. Trinh Nguyen, senior economist at Natixis, pointed out that Japan is caught in a vicious cycle: the yen, used as a funding currency, continues to be sold off, imported inflationary pressures force the central bank to raise rates, and rate hike expectations further push up yields.

In April, Japan’s corporate goods prices recorded their largest year-on-year increase in 12 years, reflecting ongoing impacts from geopolitical conflicts on global supply chains. Rinto Maruyama, strategist at SMBC Nikko Securities, stated that for Japan, which has long been mired in deflation, the 30-year government bond yield breaking above 4% holds historic significance, suggesting that inflation may truly take root in Japan.

UK Bonds and Political Risks: A Double Blow to a Fragile Market

Amid a broad sell-off in global bond markets, UK assets experienced even sharper declines.

This week, the pound recorded its largest weekly drop since January 2025, with the 30-year UK government bond yield rising above 5.8% on May 12, hitting a near-three-decade high. Political turmoil amplified pressures from rising global interest rates.

The market attributed the additional declines to the pricing of a so-called 'Burnham premium.' Andy Burnham, the Mayor of Manchester, announced his intention to return to parliament and challenge incumbent Prime Minister Keir Starmer. Investors fear that a more left-leaning leader might implement looser fiscal policies, increasing bond supply. Pooja Kumra, a rates strategist at TD Securities, pointed out that the timeline for a by-election is proceeding faster than expected, potentially sustaining the selling momentum.

At the heart of market concerns is that expanding fiscal deficits and increased long-term government bond issuance will further drive up borrowing costs. The sharp volatility in UK markets indicates that investor tolerance for policy credibility is significantly diminishing amid the confluence of high inflation, elevated interest rates, and fiscal uncertainty.

Inflation Rises, Interest Rates Remain High, and Markets Sound the Alarm

Behind this wave of global selloffs, a clear macroeconomic narrative is gradually emerging: energy shocks are driving inflation back up, forcing central banks worldwide to reassess previous expectations of monetary easing. Meanwhile, with global equities at record highs, Faris Mourad, head of thematic investing at Goldman Sachs, warned: 'Persistently high interest rates spell trouble for equity markets.'

Market attention has now shifted to next week's Federal Reserve policy signals and NVIDIA's earnings report. Nomura analyst McElligott reminded that the 'gamma release'—a temporary decline in market volatility and sudden liquidity surge following large-scale options expirations—after Friday's options expiry may open a window for a potential reversal in next week’s trading. Regardless of direction, investors need to heed one fact: when the safest assets globally—government bonds—are undergoing systemic repricing, the valuation logic of risk assets cannot remain unscathed.

Editor/Deng