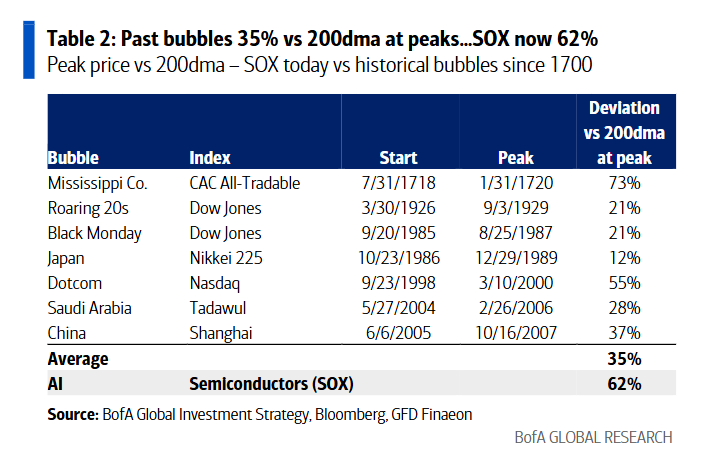

The frenzy surrounding AI, the massive inflow of capital, and rising inflation are pushing the market into a danger zone. According to Hartnett of Bank of America, when the US CPI exceeds 4%, risky assets typically enter a correction phase. Currently, the deviation of the semiconductor index from its 200-day moving average has surpassed that observed during the dot-com bubble period.

As the stock market hits a record high, Michael Hartnett, Chief Investment Strategist at Bank of America, issues a warning: with investors flocking to the stock market and inflation risks continuing to rise, early June will be a window for profit-taking.

According to TradingView, Hartnett wrote in the latest issue of 'The Flow Show' weekly report, "The bullish retreat into stocks and tech stocks may fully complete in the coming weeks, making early June an opportune time to reduce positions." He pointed out that June will see a series of key events densely packed, including the seventh OPEC meeting, the World Cup opening, the G7 summit, and Kevin Warsh's first Federal Reserve FOMC meeting, all of which could trigger market caution.

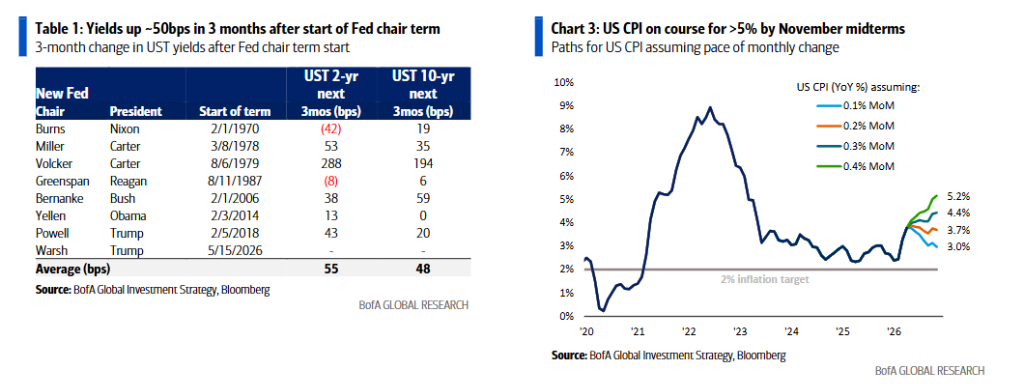

Inflation data provides direct evidence for this warning. The U.S. April PPI rose 6% year-on-year, the fastest increase since 2022; the CPI increased by 3.8% year-on-year, surpassing economists' expectations. Hartnett's team calculated that if the monthly 0.4% month-on-month increase over the past six months does not slow down quickly, the U.S. CPI will exceed 5% before the midterm elections in November. This prospect poses significant pressure on the stock market.

Inflation data provides direct evidence for this warning. The U.S. April PPI rose 6% year-on-year, the fastest increase since 2022; the CPI increased by 3.8% year-on-year, surpassing economists' expectations. Hartnett's team calculated that if the monthly 0.4% month-on-month increase over the past six months does not slow down quickly, the U.S. CPI will exceed 5% before the midterm elections in November. This prospect poses significant pressure on the stock market.

Inflation Warning Line: A CPI above 4% is the "dragon domain" for risk assets.

Hartnett defined a CPI rising above 4% as the tipping point where risk assets begin to become "restless."

He cited historical data from the past century to point out that once inflation crosses this threshold,$S&P 500 Index (.SPX.US)$it falls by an average of 4% in the following three months and 7% within six months.

Current inflationary pressures have shown widespread proliferation, covering energy, electricity, transportation, commodity prices, and rents, among other areas. Rising inflation expectations have pushed the yield on 10-year U.S. Treasury bonds above 4.5%, while the 30-year yield has surpassed 5%—a level Hartnett previously referred to as the "Maginot Line."

The Bank of America team predicts that if the monthly increase remains at 0.4%, the CPI will reach 5.2% by the end of the year; even if the growth slows to 0.3%, the year-end CPI will still rise to 4.4%, both far exceeding the Federal Reserve’s 2% target.

Bullish sentiment is approaching extreme levels, with multiple indicators issuing warnings.

Bank of America’s Bull & Bear Indicator rose from 7.2 to 7.6 this week, nearing the 8.0 trigger line for a "sell signal."

The Hartnett team pointed out that if global equity inflows reach $15 billion to $20 billion over the next two weeks, with emerging market bonds and high-yield bonds each attracting approximately $2 billion in inflows, and the May Fund Manager Survey shows a drop in cash positions from 4.3% to 3.8%, this indicator will trigger a sell signal within two weeks.

Position data from private clients also confirms the market's extreme optimism. Bank of America's private clients, who manage $4.5 trillion in assets, have increased their equity allocation to 65.7%, a record high, while cash allocation has dropped to 9.8%, an all-time low. Since the low on March 30, $S&P 500 Index (.SPX.US)$ it has rebounded by 18%,$NASDAQ 100 Index (.NDX.US)$with even larger gains of 29%. The AI boom has driven semiconductors and related stocks to repeatedly hit new highs.

The semiconductor index SOX is currently deviating by as much as 62% from its 200-day moving average. Hartnett compared this level to extreme historical cases such as the Mississippi Bubble and the Internet Bubble – where the average deviation at the peak of major historical bubbles was only 35%.

Equities and bonds attract capital simultaneously

The latest weekly fund flow data shows that bonds attracted $28.1 billion in inflows, equities saw $20.5 billion in inflows, cash received $5.8 billion in inflows, gold attracted $2 billion in inflows, while cryptocurrencies recorded an outflow of $1.3 billion, marking the largest weekly outflow since February 2026.

By market, U.S. large-cap stocks attracted $24.4 billion in inflows in a single week, the largest in five weeks; technology stocks received $5.4 billion in inflows, the highest in three months; infrastructure funds recorded a historic high of $1.5 billion in weekly inflows.

Investment-grade bonds accumulated $42.2 billion in inflows over the past four weeks, the largest four-week inflow since March 2026; government bonds have seen continuous inflows over the past three weeks, with a weekly inflow of $5.6 billion, the highest in six weeks.

The appointment of a new Federal Reserve Chair and political risks add extra variables

The Hartnett team also noted that historically, within three months of a new Federal Reserve Chair taking office, U.S. Treasury yields have risen by an average of about 50 basis points. If this pattern repeats with Kevin Warsh, the 2-year Treasury yield could rise to 4.53%, and the 10-year yield could climb to 4.93%.

On the political front, Hartnett cited data from UK local elections indicating that the vote share of non-mainstream parties, such as the Reform Party and the Green Party, surged from 3% to 41%, while traditional parties like Labour and the Conservatives saw their vote share plummet from 92% to 54%.

He believes that extreme politics and extreme price movements on Wall Street are mutually reinforcing, and the erosion of inflation on people's living standards is the quickest way for a ruling administration to lose voter support – Trump’s approval rating on inflation has dropped to 30%, close to the low point during Biden’s term. Hartnett warned that this slow-burning fuse could trigger a large-scale asset rotation from chips and commodities to consumer sectors by 2027.

Editor/Rocky