Global bond markets faced a sharp sell-off this week, beginning to spill over into risk asset markets that had previously been rallying strongly.

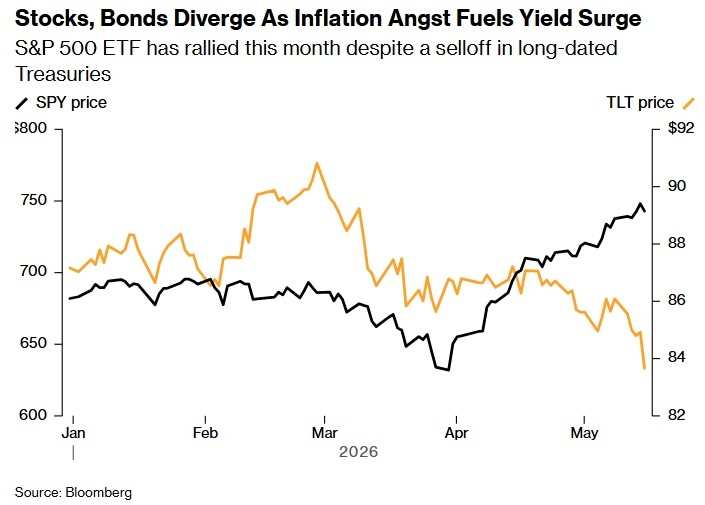

The global bond market experienced a sharp sell-off this week, starting to impact the previously booming risk asset markets. On Friday, the three major U.S. stock indexes retreated significantly, with technology stocks becoming the focal point of the sell-off.$S&P 500 Index (.SPX.US)$dropped more than 1.2%, while$U.S. 10-Year Treasury Notes Yield (US10Y.BD)$surged above 4.5%, triggering concerns over the prolonged duration of a high-interest-rate environment.

At the same time,$Japan 30-Year Treasury Notes Yield (JP30Y.BD)$rose above 4% for the first time in history, while the yield on UK long-term government bonds climbed to its highest level in 28 years. International oil prices also continued to rise, with Brent crude breaking through $105 per barrel.

Over the past few months, the market had repeatedly ignored risks such as escalating conflicts in the Middle East, a rebound in inflation, and supply chain disruptions. U.S. stocks kept setting new all-time highs, corporate bond credit spreads remained low, and high-risk trades such as AI-related stocks and cryptocurrencies continued to attract retail investors.

Over the past few months, the market had repeatedly ignored risks such as escalating conflicts in the Middle East, a rebound in inflation, and supply chain disruptions. U.S. stocks kept setting new all-time highs, corporate bond credit spreads remained low, and high-risk trades such as AI-related stocks and cryptocurrencies continued to attract retail investors.

However, conditions began to shift this week. Following the release of higher-than-expected inflation data in the U.S., long-term Treasury yields surged rapidly, prompting the market to reassess the possibility that the Federal Reserve may not only be unable to cut interest rates but could even tighten policy further.

Priya Misra, portfolio manager at J.P. Morgan Asset Management, stated: "After the 10-year U.S. Treasury yield broke through the psychological threshold of 4.5%, risks have started to become dangerous, impacting not only the bond market but also the entire risk asset system." She noted that as financial conditions continue to tighten, market focus is gradually shifting from 'pure inflation' to 'stagflation risks'.

Despite Friday’s adjustment, U.S. stocks had still risen for seven consecutive weeks prior. However, signs of fatigue have emerged within the market structure. Data shows that eight out of the S&P 500 Index’s 11 major sectors declined this month, with most gains concentrated in the technology sector. Meanwhile, despite surging bond yields, investment-grade and high-yield bond credit spreads remained stable, supported by robust corporate earnings and strong primary market demand.

Analysts pointed out that what truly unnerved the market this week was not just the rise in yields but the 'global synchronized surge.'$UK30-YearGovernmentBondYield (GB30Y.BD)$once rose above 5.8%, hitting a new high since 1998, fueling concerns that UK Prime Minister Starmer might face internal party challenges. Meanwhile, government bond yields in Japan, Germany, Spain, and Australia also moved higher in tandem.

Emmanuel Cau, head of European equity strategy at Barclays, said: "The resurgence of inflation is exacerbating pressures in an already fragile bond market." He believes that political risks in the UK are driving up risk premiums on UK government bonds, and this pressure has begun to spread to developed market bonds globally.

Meanwhile, an increasing number of Wall Street institutions have begun to worry about the impact of high interest rates on stock market valuations.

Lori Calvasina, strategist at Royal Bank of Canada Capital Markets, warned that if the yield on the 10-year U.S. Treasury rises to 5%, the U.S. stock valuation system could face significant compression. Bank of America had previously indicated that a 5% yield on 30-year U.S. Treasuries represents a critical market threshold, and if long-term interest rates continue to climb, they could place greater pressure on equity market risk appetite.

Nevertheless, market bulls remain confident in AI-driven trends.$Federated Hermes (FHI.US)$Deputy Chief Investment Officer Steve Chiavarone believes that the bond market and AI stocks actually reflect logic across different time horizons.

He stated that rising oil prices and bond yields reflect supply tightness and sticky inflation over the next three to six months, while AI stocks are betting on productivity improvements and a decline in inflation within one to three years.

Chiavarone noted that the current upward revisions in corporate earnings are among the strongest he has seen in the past 20 years and considers equities to be a better hedge against inflation than bonds, cash, or even precious metals.

However, bears worry that the current market logic cannot coexist in the long term. Gene Goldman, Chief Investment Officer at Cetera Financial Group, said, 'These asset classes are each telling their own plausible story, but they are not telling the same story.'

He believes that ultimately, either stock market valuations will be forced downward, or the bond market must reassess how tight the Federal Reserve's policy needs to be.

Editor/Rocky