Source: Xue Tao's Macro Notes

Authors: Song Xue Tao, Zhong Tian

Silicon-based to the left, carbon-based to the right; capital inflation, labor deflation.

The U.S. economy remains resilient from a total volume perspective, but the divergence between silicon-based inflation and carbon-based deflation is widening — with AI assuming greater macro systemic importance for the United States.

AI lowers the price of certain human capital but increases expenditures on computing power, electricity, data centers, and semiconductor equipment. AI does not simply lead to comprehensive deflation but instead causes 'human capital deflation and computing power capital inflation.' This structural divergence makes it difficult for the Fed in terms of monetary policy: aggregate data does not allow for easing, while structural data does not support tightening.

AI lowers the price of certain human capital but increases expenditures on computing power, electricity, data centers, and semiconductor equipment. AI does not simply lead to comprehensive deflation but instead causes 'human capital deflation and computing power capital inflation.' This structural divergence makes it difficult for the Fed in terms of monetary policy: aggregate data does not allow for easing, while structural data does not support tightening.

The current dilemma where cutting interest rates is undesirable and raising them even more so is exactly the hardest part for the Fed.

Over the past few years, the U.S. has experienced the pandemic, the Russia-Ukraine war, tariff wars, and conflicts in the Middle East—none of these four supply shocks were within the Fed’s control. The Fed under Warsh’s leadership will not become more independent but may instead become more passive amid presidential and market pressures. What Powell could not achieve, Warsh might not accomplish either, as these problems cannot be solved solely by a monetary policy framework but involve fiscal dominance, distribution structures, growth transitions, government reforms, and technological progress.

1. Silicon-based Inflation and Carbon-based Deflation

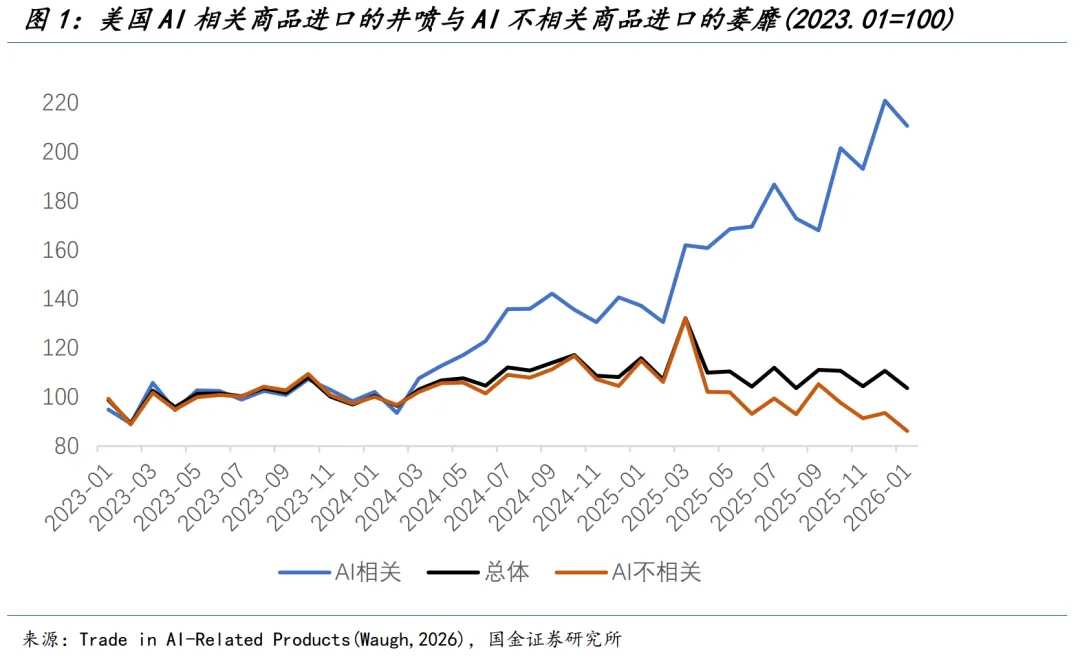

Computing chips, electric infrastructure, data centers, semiconductor equipment—these AI-related capital expenditures have shown extremely steep growth slopes, driving up real demand in relevant fields and significantly reflected in import price pressures.

The share of AI-related goods in U.S. imports has surged from 14.6% in 2023 to 22.7%, with the absolute scale nearly doubling (exceeding $650 billion for the whole year of 2025); meanwhile, imports of non-AI-related goods have seen almost no growth and may even show a downward trend after the ‘pre-emptive import’ effect fades in 2025.

Capital expenditure, Token consumption, and AI enterprises' B2B revenue are forming cycles in shorter periods, at the cost of a rapid increase in the U.S. AI core product import price index (IPI). Over the past year, its year-on-year growth rate rebounded from a low of -3.3% to 9.4%, rising by 12.7 percentage points within 12 months. Especially considering the ‘Moore’s Law’ of electronic products, this silicon-based inflation trend implies that related demand growth is steeper than the slope of prices.

Warsh, the next Fed Chair succeeding Powell, mentioned that AI can enhance productivity and thus bring about deflation, providing justification for continued interest rate cuts. If using AI-induced deflation as a rationale for rate cuts, one must explain: when will AI-driven efficiency gains outweigh the price pressures brought by computing and electricity capital expenditures? When will this spread from localized technical sectors to the broader economy? However, this transmission chain remains unclear in the short term.

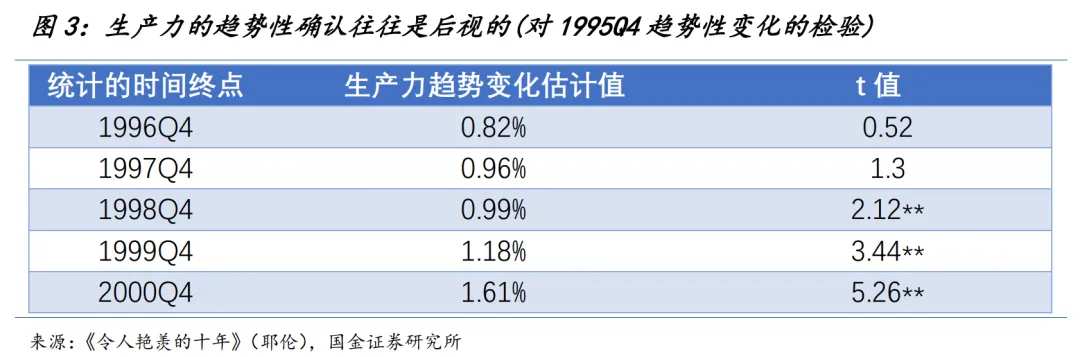

In recent years, a repeatedly discussed perspective is that productivity gains are often recognized only in hindsight—this is due not only to the need for frequent revisions of economic data but also to the time required to comprehend changes in production relations.

Former Fed Chair Janet Yellen once noted that if the fourth quarter of 1995 were taken as the observation point for a trend change in productivity, it would take until the fourth quarter of 1998 to reach a statistically significant conclusion (p-value = 0.03), and by the first quarter of 2000, it became even more significant (p-value = 0.0007).

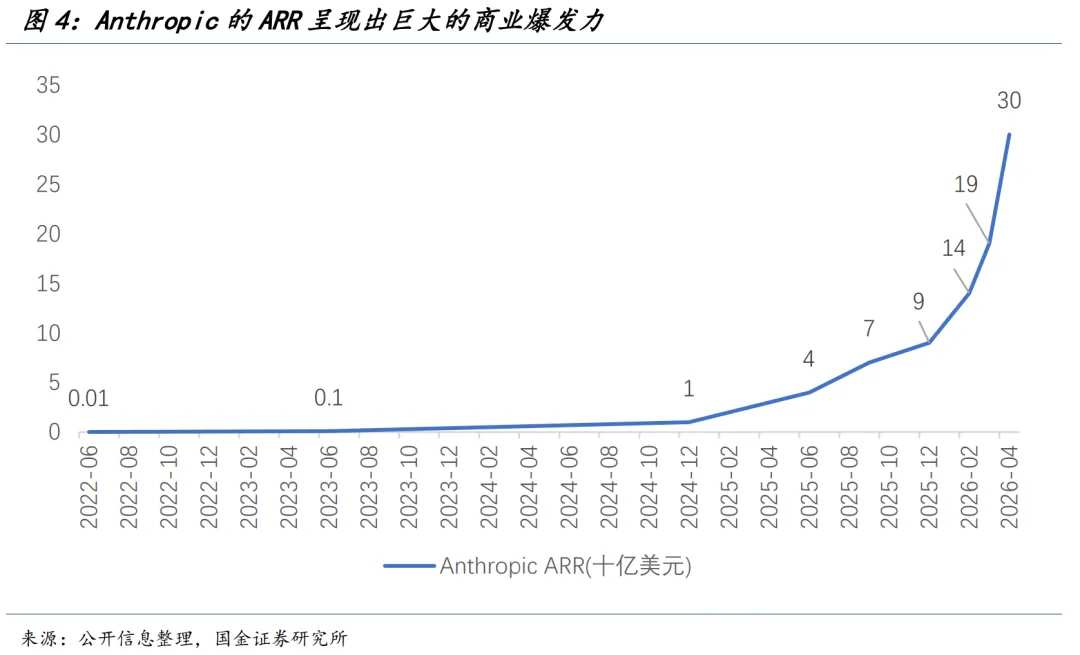

Therefore, even though AI capital expenditure continues to be revised upward, and Anthropic’s ARR shows an exaggerated vertical ascent, what we have observed so far may still represent a "short-term perspective" within the macroeconomic context.

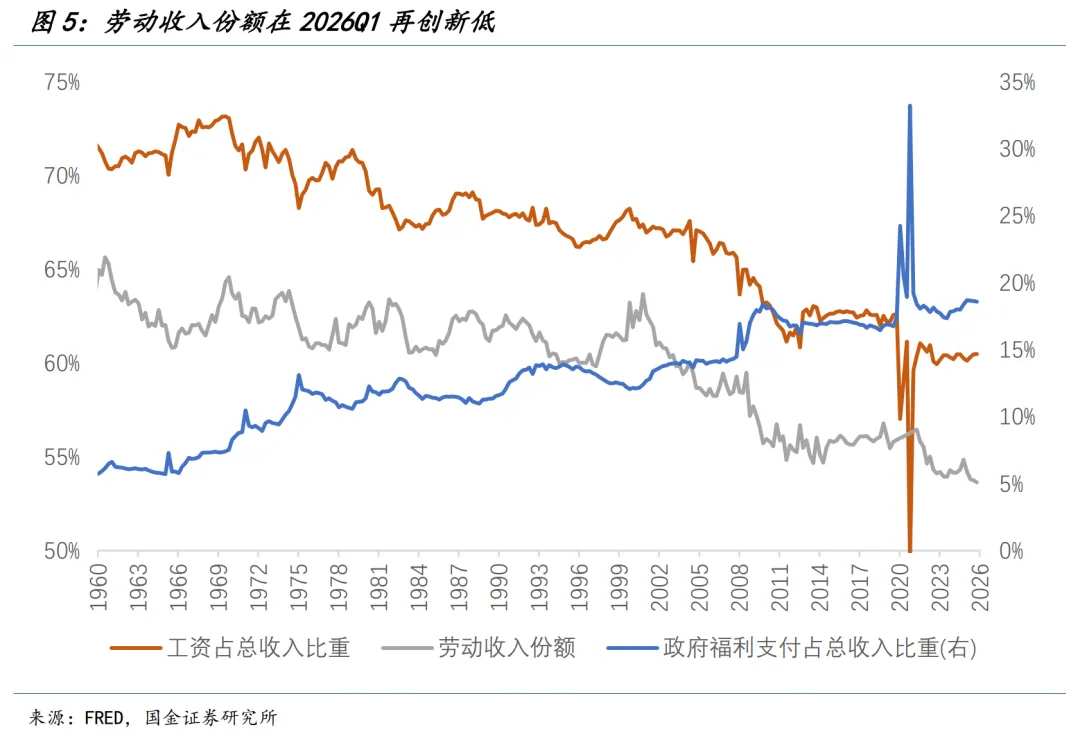

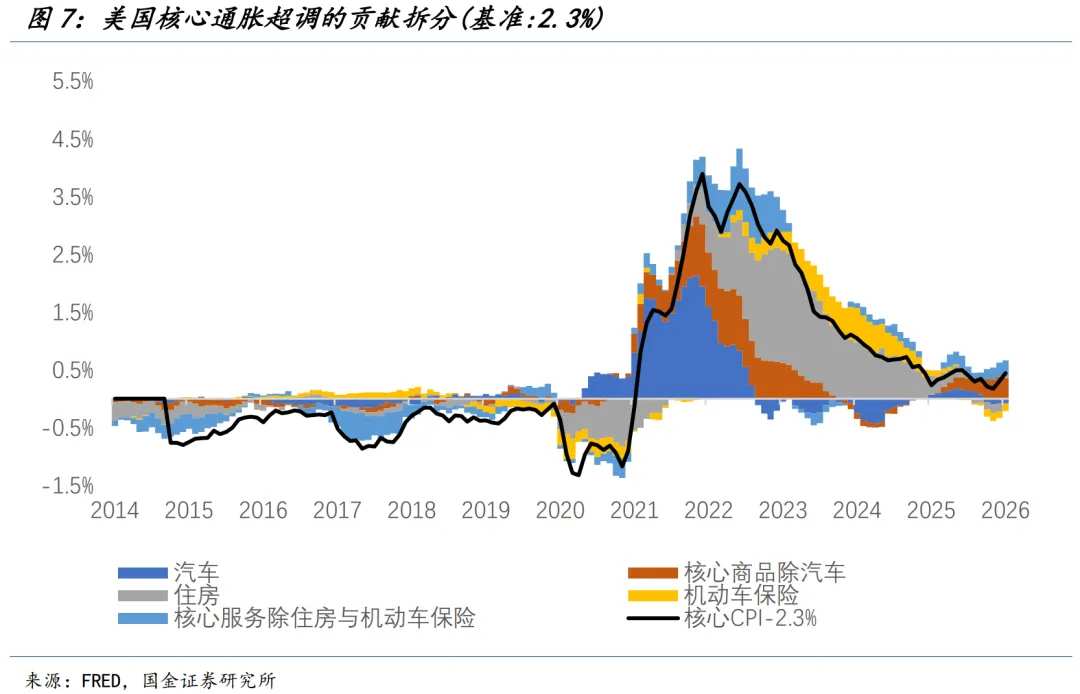

AI lowers the price of certain forms of human capital but drives up the prices of chips, storage, electricity, data center construction, power equipment, and other computing capital. In other words, AI does not simply lead to comprehensive deflation but instead causes 'deflation in human capital and inflation in computing capital.'

At the same time, areas related to human capital, general employment, and middle-class consumption—all fields closely tied to carbon-based life—are showing broad weakness. Labor participation rates continue to decline, labor income shares are falling, wage growth is slowing, and private-sector employment has seen almost zero growth. While the headline unemployment rate remains robust on the surface, the ongoing contraction in labor participation masks the true pressure in the labor market.

An economy, under the backdrop of continuously shrinking labor supply, relies on To B revenue growth from the AI industry to drive expansion at the cost of greater structural employment compression.

In April, U.S. non-farm payrolls added 115,000 jobs, with the unemployment rate remaining at 4.34%. The education and healthcare sectors remained the largest sources of job growth, while core private-sector employment continued to show weakness. Most notably, the U.S. labor participation rate has been declining continuously over the past year, indicating that real labor market pressures may be significantly higher than what the U3 unemployment rate suggests.

II. The Fed's Dilemma: Easier Said Than Done to Cut Rates, Harder Still to Raise Them

Structural divergences are making monetary policy decisions challenging for the Fed: aggregate data do not permit easing, while structural data do not support tightening. Facing its dual mandate, the Fed is confronted with a stagflation-like dilemma of high oil prices and weak employment.

The difficulty in cutting rates stems from oil prices. In April, U.S. CPI year-over-year rebounded to 3.8%, with energy CPI surging by 17.8% year-over-year. Gasoline alone recorded a 28.4% increase year-over-year, contributing one-third of the month-on-month CPI growth.

The precondition for the Federal Reserve to see through war-driven inflation is that the outcome of the war is predictable (whether it follows the toll booth model or a complete reopening). If uncertainty in the Hormuz region persists, oil prices will not return to pre-war levels, and the Fed will find it difficult to continue sending easing signals. It is important to be vigilant as this shock increasingly appears to be more than just a short-term disruption.

However, it is even harder for the Fed to implement substantial interest rate hikes. Core inflation in the U.S. CPI for April remains weak, particularly in service inflation. The jump in housing inflation primarily stems from statistical adjustments caused by prior government shutdowns. Excluding the impact of housing prices, the tariff effect is also gradually diminishing.

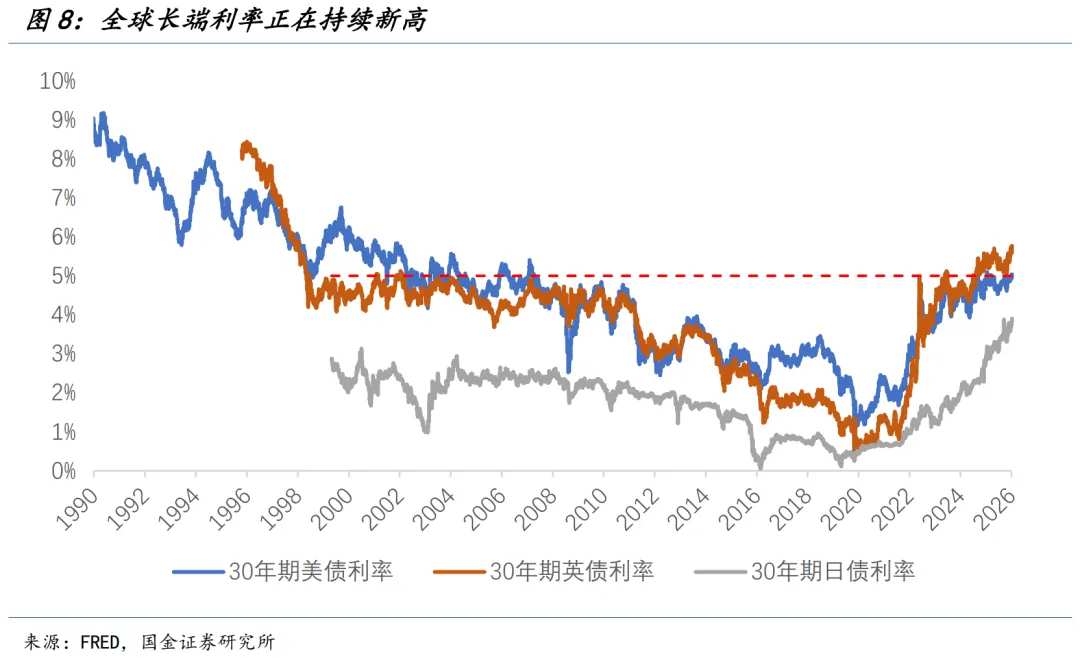

Against the backdrop of oil price shocks and renewed inflationary pressures, global long-term bonds are suffering significantly: the yield on the 30-year U.S. Treasury bond has broken through 5%, while the 30-year UK gilt has reached a new high since 1998. The spontaneous rise in long-end rates, coupled with a steepening yield curve, amounts to an additional credit contraction beyond the market's 'no rate cut' pricing. This will also transmit to more market-oriented interest rates, tightening financial conditions.

Past interest rate hikes typically required evidence of rising inflation expectations, accelerating wages, and the formation of a wage-inflation spiral. However, wage growth has not accelerated noticeably at present, long-term inflation expectations have not spiraled out of control, and the labor market appears more like 'superficial stability masking internal weakness.' The question of how long the current state of eroded real purchasing power and pressured household savings rates can persist requires ongoing observation. At least for now, there is no basis for raising interest rates.

This stagflationary environment, where cutting rates is difficult but hiking rates even harder, places the Federal Reserve in a dilemma. Rising oil prices do not necessarily demand interest rate hikes because monetary policy cannot suppress supply-side shocks in crude oil. However, rising oil prices elevate overall inflation, making rate cuts appear inappropriate. If the Fed were to cut rates amid high oil prices and unreturned inflation, the market might question its independence.

Over the past few years, the United States has experienced four supply shocks—public health crises, the Russia-Ukraine war, tariff wars, and Middle East conflicts—that were all beyond the Federal Reserve’s control. Supply shocks, fiscal expansion, de-globalization, and geopolitical risks have driven up inflation, but ultimately, the burden falls on the Fed to manage it through interest rates. Therefore, the decline in the Fed’s independence is not attributable to any single chairperson but rather the result of fiscal dominance, political pressure, and the restructuring of the global supply system.

The Federal Reserve under Kevin Warsh’s tenure would not gain more independence; instead, it might become even more passive under pressure from both the President and the markets. What Powell could not achieve, Warsh may also fail to accomplish, as these issues go beyond what monetary policy frameworks alone can resolve—they involve fiscal dominance, distribution structures, growth transitions, government reforms, and technological advancement.

On one hand, the current inflation structure is driven by energy and supply bottlenecks, so the marginal effect of monetary policy tightening or loosening on current prices is very limited, potentially pushing independence onto the judgment seat. Faced with questioning committees and a divided Fed, they may first seek consensus through 'procedural conservatism' rather than immediately opening the floodgates.

On the other hand, Warsh sees the real problems—for example, the decline in Fed independence, excessive official communication, and the failure of forward guidance—but if the solution is to reduce transparency, weaken the dot plot, compress internal expressions, and centralize the chair’s authority, this may not restore Fed credibility but instead undermine organizational transparency.

Regardless of how events unfold, adjustments to monetary policy are unlikely to be extreme and must align with a new era context: silicon-based inflation, carbon-based deflation.

Risk Warning

The uncertainty of Trump's military policy is relatively high, and the U.S. military's ground invasion could lead to a loss of control over the situation; the impact of energy shortages on demand is significantly greater than anticipated, dragging the global economy into a recessionary mode; central banks worldwide are rapidly shifting policies, introducing the risk of a second wave of global inflation.

Editor/melody