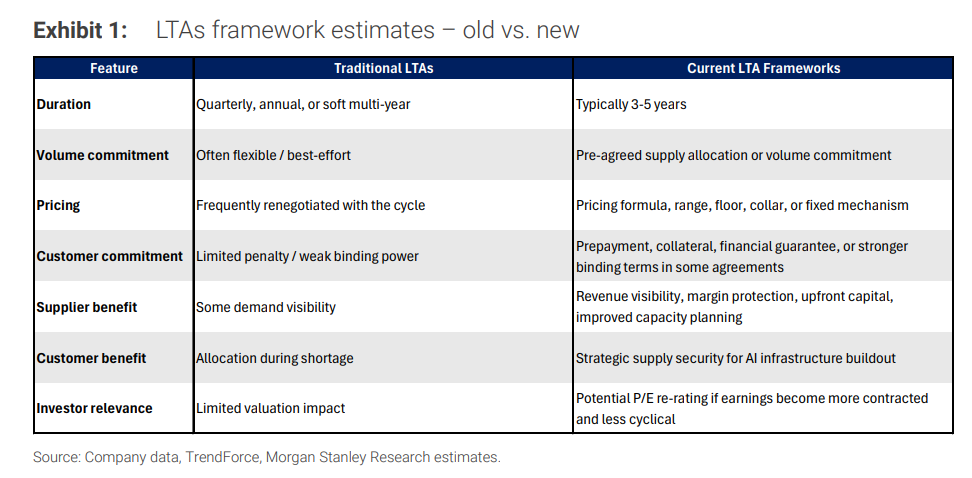

Memory chips are transitioning from cyclical commodities to becoming strategic resources for AI infrastructure. Morgan Stanley and J.P. Morgan have successively noted that long-term supply agreements (LTAs) are reshaping the traditional cyclical logic of price hikes, capacity expansion, and subsequent collapses into a new paradigm characterized by prepayment-based volume locking, price floors, and predictable profitability. Once the valuation framework shifts from the price-to-book (P/B) ratio to the price-to-earnings (P/E) ratio, leading companies such as SK Hynix may see a revaluation potential exceeding 38%, although the market has yet to fully reflect this.

Storage chips are evolving from cyclical commodities into strategic resources for AI infrastructure — and the core mechanism driving this transformation is called the Long-Term Agreement (LTA).

According to information from the Chasing Trends Trading Desk, Morgan Stanley and JPMorgan recently released in-depth research on the global storage industry, with both reports focusing on the same variable: Long-Term Agreements (LTA) for storage. In the past, the core narrative of the storage industry involved price hikes, capacity expansion, oversupply, price declines, and subsequent market clearing. Now, AI customers want to secure supply in advance, while storage manufacturers aim to lock in orders and prices ahead of time, potentially reducing the amplitude of cyclical fluctuations.

Shawn Kim of Morgan Stanley's Technology Hardware team wrote in the research: "Memory has become a key bottleneck in AI infrastructure. LTAs signed by clients to ensure supply are transforming a traditionally cyclical business into one with guaranteed, high-margin, long-term revenue streams." This statement encapsulates the bank's core view: if the market continues to value storage companies as traditional cyclical stocks, it may underestimate the stability of future revenues and cash flows.

Shawn Kim of Morgan Stanley's Technology Hardware team wrote in the research: "Memory has become a key bottleneck in AI infrastructure. LTAs signed by clients to ensure supply are transforming a traditionally cyclical business into one with guaranteed, high-margin, long-term revenue streams." This statement encapsulates the bank's core view: if the market continues to value storage companies as traditional cyclical stocks, it may underestimate the stability of future revenues and cash flows.

Jay Kwon's team at JPMorgan provided a more direct assessment: "LTAs pave the way for storage manufacturers to transition to a new valuation framework." His reasoning is that buyers are not just concerned about price increases but are even more worried about being unable to secure supply; sellers, meanwhile, are not only focused on raising prices but also want order visibility before committing to significant capital expenditures. The LTA embeds both parties' concerns into the contract.

What investors truly care about is not the "duration of the contract" but whether the contract is binding, whether cash is received in advance, and whether there is protection against price declines. If these terms are sufficiently robust, the profitability of storage companies will no longer fluctuate entirely with spot prices, and the Price-to-Book (P/B) valuation framework may give way to the Price-to-Earnings (P/E) framework.

LTAs are not a new phenomenon, but this time it is different.

The storage industry has seen "long-term agreements" before. During the 2017 DRAM shortage cycle, multi-year framework contracts were signed, but once demand cooled, prices fell by over 40%, and customers still pushed for discounts or delayed shipments, rendering the contracts ineffective.

The difference this time lies in the structure of the terms:

Scale of advance payments: Some suppliers have already collected 50% of prepayments for 2027 demand, with the figure reaching 100% for 2028.

Price mechanism: A price range is established, with both upper (collar/ceiling) and lower limits for protection, rather than floating prices tied to the market.

Cost of default: SanDisk's CEO directly stated on the earnings call, "Customers have mortgaged tens of billions of dollars through various financial instruments. If they fail to fulfill their quarterly purchase obligations, the money immediately becomes ours."

Kim Jae-jun, Executive Vice President of Samsung Electronics, was equally straightforward in his statement during the 1Q26 earnings call: "Unlike existing supply contracts based on mutual trust, these multi-year contracts involve higher-level binding commitments."

Guo Ruozheng, President of SK Hynix, said at the shareholders' meeting in March this year that the company is "comprehensively evaluating various structural solutions"—implying that simple penalty mechanisms are no longer sufficient and that exit paths for both parties need to be locked in at the contract architecture level.

The fundamental reason why such agreements are difficult to terminate lies in the accounting nature of advance payments: once paid, they are recorded as capital expenditures or prepaid assets on the customer's books, and the cost of renegotiation far exceeds the penalty for breach of contract.

Supply gaps are the root of negotiating leverage.

It is not out of goodwill that hyperscale cloud service providers (CSPs) are willing to sign such contracts; rather, they are compelled to do so.

The growth rate of AI inference demand far exceeds the physical expansion limits of DRAM production capacity. According to JPMorgan’s calculations, from 2026 to 2030, the cumulative shortage of wafer production capacity for the world’s top three DRAM manufacturers will amount to approximately 444,000 wafers per month (in equivalent monthly capacity).

On the demand side, the AI semiconductor market size is projected to grow by 50-60% by 2030. Taiwan Semiconductor recently raised its forecast for the total addressable market (TAM) of semiconductors from $1 trillion to $1.5 trillion. Meanwhile, DRAM supply is constrained by EUV lithography machine capacity bottlenecks, and bit shipment growth may be capped at less than 30% annually starting in 2027.

The divergence between these two trends forms the strongest bargaining chip on the memory manufacturers’ negotiation table.

In the past, the logic behind memory manufacturers expanding production was "Make-to-Stock"—build capacity first, then wait for demand. Now, hyperscale cloud companies, in order to secure volume, are driving memory manufacturers to shift toward a "Make-to-Order" model. Essentially, advance payments serve as a guarantee for the memory manufacturers’ capital expenditures.

What the sellers seek is not blind expansion of production, but guaranteed orders.

Memory manufacturers also face their own challenges: the cost of expanding production is rising.

The cost per bit of additional capacity is increasing due to factors such as infrastructure costs, wafer equipment value, and commitments to capital expenditures for backend packaging. Manufacturers are reluctant to expand based solely on demand forecasts because if AI demand falls below expectations or customer inventories accumulate again, the industry could return to a previous cycle of price declines.

The role of Long-Term Agreements (LTAs) is to convert 'potential demand' into 'more certain orders.' With prepayments, volume commitments, and price protection, production expansion becomes more aligned with confirmed demand rather than speculative bets on the next boom.

This also explains why a high proportion of LTAs may not necessarily incentivize suppliers to aggressively expand production. In an environment of severe shortages, suppliers are more likely to prioritize maintaining high-quality contracts over prematurely filling capacity. Contract quality outweighs sheer speed of expansion.

Buyers will not accept terms unconditionally. Possible protective measures include penalties for non-delivery by suppliers, bank or third-party guarantees, and discussions about capital expenditure subsidies. However, capacity subsidies may limit suppliers' operational flexibility, making them less popular in contract negotiations.

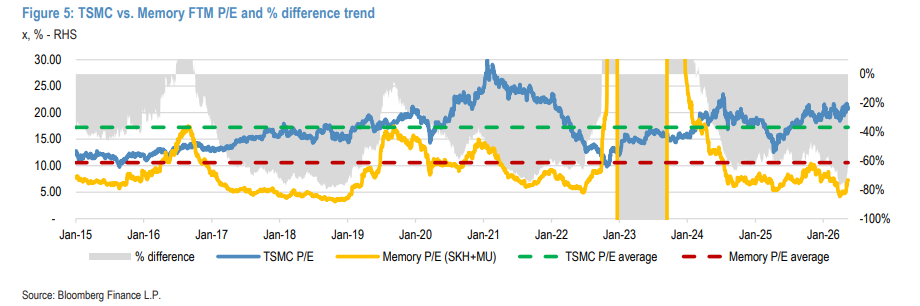

Valuation Framework Shift: Drawing Reference from Taiwan Semiconductor

For a long time, memory stocks have been priced using the Price-to-Book (P/B) ratio—because earnings volatility is too high, rendering the Price-to-Earnings (P/E) ratio meaningless. However, once LTAs lock in volumes and prices for the next three to five years, earnings predictability changes significantly.

The reference point is Taiwan Semiconductor. Prior to 2015, Taiwan Semiconductor was also considered a capital-intensive cyclical stock, valued using the P/B ratio. After securing Apple's exclusive supply contract in 2014, visibility of demand improved, prompting institutional investors to shift to the P/E framework. Since then, Taiwan Semiconductor's P/E ratio has fluctuated between 10 and 30 times, with an average of approximately 17 times.

Currently, the forward P/E ratio for memory stocks (SK Hynix + Micron combined) is approximately 7.3 times, with an average of about 9 times over the past 11 years (excluding the downturn period of 2022–2023). This figure consistently remains within a range of negative 50% to negative 80% compared to Taiwan Semiconductor.

Analysts believe that for the storage valuation to complete a framework shift, five conditions need to be met: significant weakening of cyclicality, durable pricing power, a continuously increasing proportion of LTA and HBM in revenue, disciplined capacity expansion while generating substantial free cash flow, and ongoing R&D collaboration to deepen the differentiated moat.

None of these five conditions can be easily checked off — this is also why JPMorgan stated that 'the path for investors will be very bumpy.'

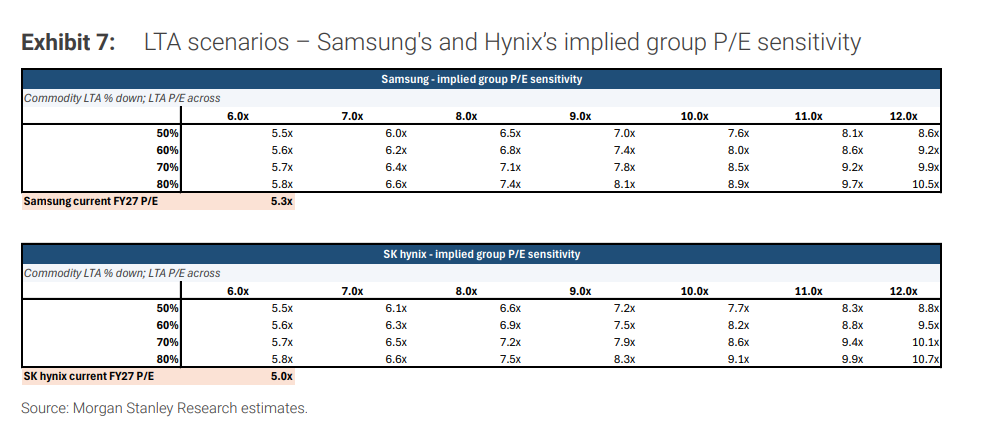

Morgan Stanley's specific estimation: How much undervaluation is there in market pricing?

The bank created a sensitivity matrix assuming that HBM has been fully integrated into LTA, with coverage of ordinary memory (commodity memory) ranging from 50% to 80%. For the LTA portion, a price-to-earnings ratio of 6-12 times was applied, while the non-LTA portion was given a multiple of 5 times.

Conclusion:

In the most conservative scenario (50% coverage + 6x LTA P/E): The implied overall P/E ratios for Samsung and SK Hynix are approximately 5.5x, already higher than Samsung’s current expected 2027 P/E of 5.3x and SK Hynix’s 5.0x.

In the neutral scenario (70% coverage + 10x LTA P/E): The implied P/E ratios for both rise to approximately 8.5-8.6x.

In the optimistic scenario (80% coverage + 12x LTA P/E): The implied P/E ratios for both increase to approximately 10.5-10.7x.

In other words, the market currently prices LTA-backed earnings in exactly the same way as cyclical commodity earnings — if these contracts are truly irrevocable and cash-guaranteed as companies claim, then this pricing is incorrect.

The actual impact of LTA on earnings forecasts

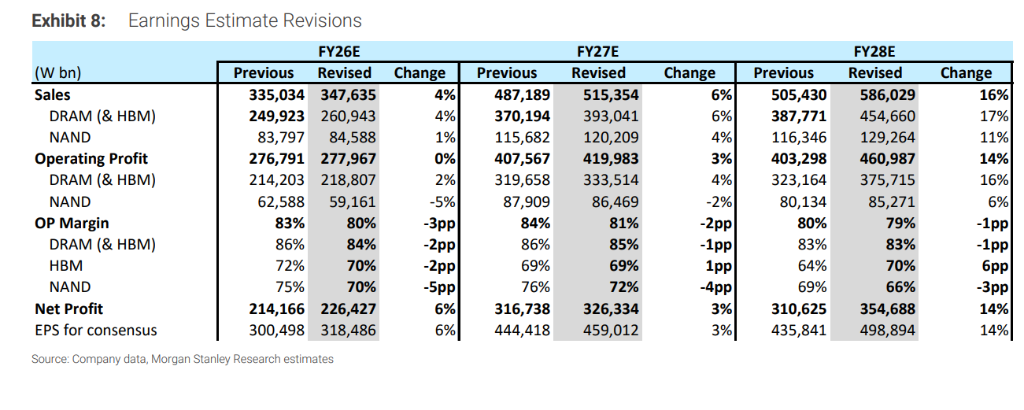

Taking SK Hynix as an example, Morgan Stanley raised its EPS forecasts for 2026-2028 by 6%, 3%, and 14%, respectively. The target price was increased from 1.7 million Korean won to 2.6 million Korean won, representing a 38% upside from the current share price (1.88 million Korean won).

There are two key changes in assumptions behind the adjustment:

Commodity DRAM pricing: Originally forecast to enter a downward cycle in 2028, it is now expected to remain stable in the first half of 2028 due to LTA providing a price floor protection.

HBM pricing: Previously projected to decline by 5-10% annually from 2026 to 2028 (considering competitive pressures), it is now revised to increase by 15% annually (driven by product upgrades). This change has a particularly significant impact on profitability in 2028.

Improvement in free cash flow is more pronounced: SK Hynix’s FCF forecasts for 2026-2028 are approximately KRW 82.8 billion, KRW 248.7 billion, and KRW 298.8 billion respectively (unit: KRW 10 billion), with the FCF yield gradually climbing from near zero to double digits.

Here, the bank also cited cases involving Apple and Japanese shipping companies: About 70% of Apple's excess returns over the past decade came from share buybacks and dividends rather than purely earnings growth; despite freight rates significantly retreating after the pandemic, Japanese shipping companies outperformed the broader market due to a substantial increase in dividend payout ratios. The logic remains consistent — sustained free cash flow can translate into shareholder returns, altering the valuation framework.

Based on this logic, JPMorgan raised its target price for Samsung Electronics to 480,000 Korean won (applying an 8x P/E ratio to expected EPS for 2026–2027), significantly increased SK Hynix's target price from 1.8 million Korean won to 3 million Korean won, and doubled Kioxia’s target price from 38,000 Japanese yen to 80,000 Japanese yen, making it the highest in the market.

LTAs do not provide immunity from cycles, as the lessons from 2017 still apply.

LTAs do not allow the memory industry to fully escape cyclicality. There have been past failures as well.

In 2017, during a DRAM shortage, the industry signed forward purchase agreements. However, when demand slowed and inventories rose, DRAM prices fell by more than 40% within 2-3 quarters, customers delayed deliveries, and contract commitments reset prices towards spot and market levels. That round of agreements failed to truly lock in the cycle.

This time, five factors need to be observed.

First, whether AI monetization continues to materialize. If AI capital expenditure enters a digestion period, clients’ willingness to lock in supply will decline.

Second, whether technological advancements alter memory requirements. Breakthroughs in model architecture, compression, KV cache, and tokenization may reduce the dependency of each generation of AI servers on memory.

Third, whether supply suddenly surges. If existing manufacturers significantly increase the supply of advanced memory or new players enter the market, the supply-demand balance will shift again.

Fourth, there are also risks at the contract level. If the LTA terms are unfavorable to memory manufacturers, or if prepayments, guarantees, and penalty mechanisms are insufficiently robust, the stability of profitability may be overstated.

Fifth, at the macro level, tariffs, sanctions, export controls on high-end AI chips, as well as pressures on clients' balance sheets, may also affect contract fulfillment.

Therefore, the core of an LTA is not the 'signing news' but cash flow. The evidence the market will look for in the future is straightforward: whether substantial cash inflows and corresponding deferred revenue obligations appear on storage companies’ balance sheets. Only when both money and obligations materialize does the LTA become more than just a narrative.

Editor/Lambor